Print

PrintGabriel Rosenberg and Margaret Tahyar are partners and Betty Huber is counsel at Davis Polk & Wardwell LLP. This post is based on a Davis Polk memorandum by Mr. Rosenberg, Ms. Tahyar, Ms. Huber, Robert Cohen, Joseph Hall and Eric Lewin.

The SEC’s request for public input on climate disclosures attracted 297 institutional comments totaling 3,290 pages. The views range from questioning the SEC’s authority to imploring the SEC to mandate comprehensive, internationally aligned and assured disclosures in SEC filings. This post summarizes thirty comment letters we consider both important and representative of differing stakeholder views, in anticipation of a formal SEC proposal expected in or before October 2021.

Overview of the request for public input

The SEC took a first step toward the adoption of climate disclosure requirements by issuing a request for public input (the RFPI) on March 15, 2021. The RFPI requested comments from investors, registrants and other market participants “[i]n light of demand for climate change information and questions about whether current disclosures adequately inform investors.” To facilitate the SEC staff’s view of existing disclosure rules, the RFPI requested comment on fifteen questions, ranging from how the SEC could best regulate climate disclosures to whether the SEC should expand its focus from climate disclosures alone to a focus on environmental, social and governance (ESG) matters as part of a broader, comprehensive disclosure framework.

Comments on the RFPI were due June 13, 2021. The RFPI has attracted considerable attention and comments continue to be submitted well past the deadline. Commenters have written to the SEC to address the questions set out in the RFPI as well as a host of related topics. These comments include structural comments about the SEC’s authority and role; technical comments about what might be disclosed and how the SEC might work with standard setters and achieve international harmonization; legal comments about potential securities law liability considerations; comments about external and internal oversight of disclosures; and comments about whether the SEC’s forthcoming rulemaking should be limited to public issuers, as opposed to including private issuers, and should be limited to climate, as opposed to including the full suite of ESG topics. In some cases, the comments expressed highly divergent views. For example, some commenters opposed the SEC taking any action at all, while others stated that the need for SEC action is imperative.

The RFPI is part of a broader set of recent SEC climate and ESG developments, consolidated here on the SEC’s website and as previously discussed by us in our March client update available here. These have included a directive from then-Acting Chair Lee to the Division of Corporation Finance to review and update the SEC’s 2010 guidance on climate disclosures, [1] an announcement by the Division of Examination that its 2021 examination priorities would include a greater focus on climate-related risks and the creation of an ESG Task Force in the Division of Enforcement. The RFPI is one important part of a broader SEC climate and ESG agenda, and we expect further developments in the coming months given the SEC’s rulemaking agenda and public statements made by Chair Gary Gensler suggesting a continued SEC focus in this area. Specifically, according to the SEC’s portion of the Spring 2021 Unified Regulatory Agenda, the following ESG and climate items are listed under the Proposed Rule Stage:

- Climate Change Disclosure, Notice of Proposed Rulemaking, by October 2021

- Corporate Board Diversity, Notice of Proposed Rulemaking, by October 2021

- Human Capital Management Disclosure, Notice of Proposed Rulemaking, by October 2021

- Investment Companies and Advisers ESG Matters, Notice of Proposed Rulemaking, by April 2022

As of June 24, 2021, 297 comment letters from institutional commenters filed by the June 13 deadline had been posted by the SEC on its website. [2] Together, these letters amount to 3,290 pages—a vast amount of information for the SEC to consider. In addition, a plethora of unaffiliated individuals submitted comments, and numerous individuals and entities, whose identities were not made available on the SEC’s website, submitted four form letter comments that together were submitted over 5,700 times.

In this client update, we summarize the key aspects of the non-form letters submitted by institutional commenters, [3] including a description of the types of commenters and, at a high level, the comments relating to six key topics raised in comments responding to the RFPI. The Appendix sets out the specific recommendations made in thirty institutional comments of potential high interest to our clients either because of their topical relevance (e.g., comments from trade organizations representing banking institutions) or because they are likely to garner attention or influence (e.g., comments from political figures). The full set of comment letters, including letters from unaffiliated individuals and form letters, can be found here.

Analysis of comment letters

Commenter type

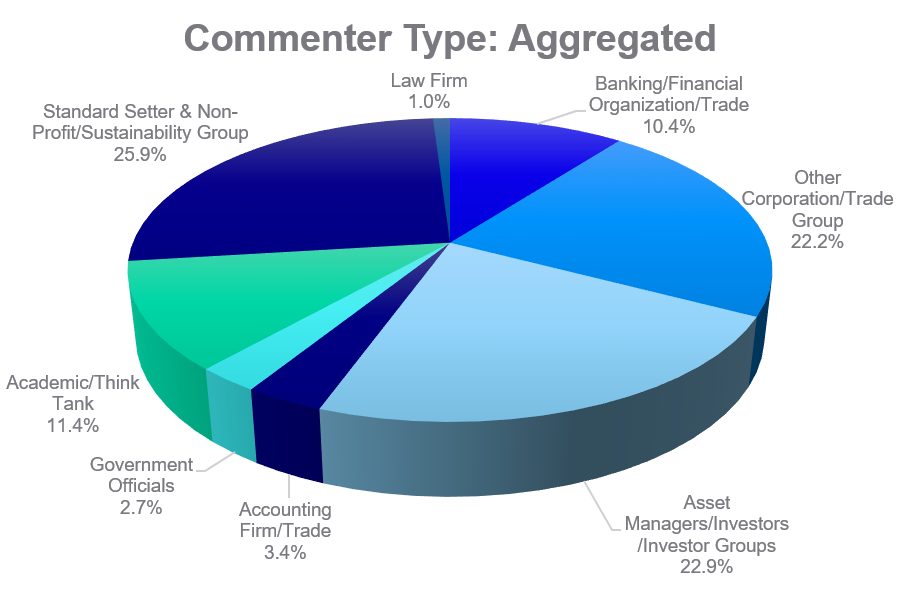

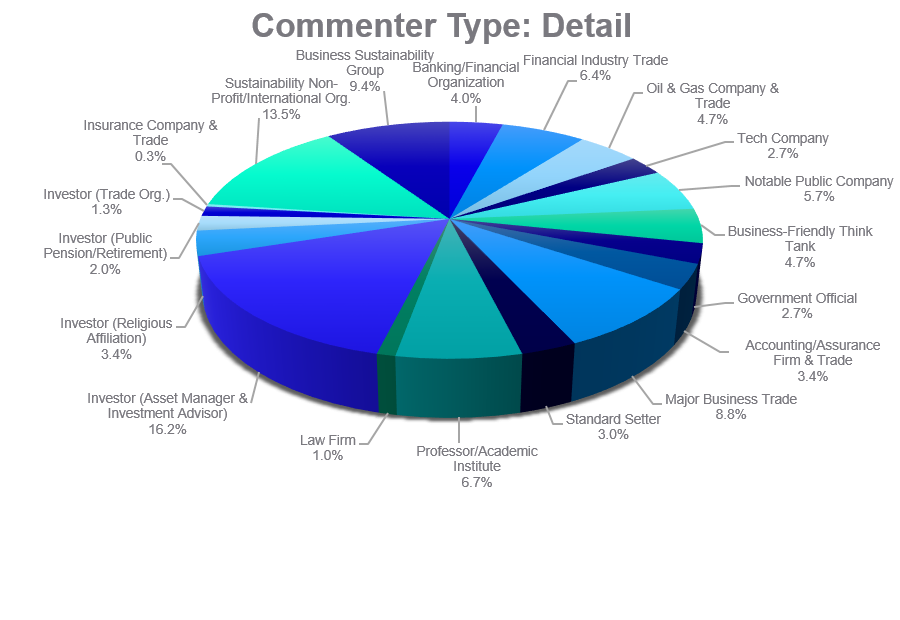

Comments were submitted by a wide variety of interested parties, from academics to political figures, individual companies to investors and trade organizations to environmental advocates. The distribution of all institutional non-form comment letters—that is, all letters other than letters from unaffiliated individuals and the over 5,700 form letters—by commenter type is illustrated in the pie charts below. The first chart presents a high-level breakdown of commenter type, while the second chart presents the same data at a more granular level.

Summary of key topics addressed in comments

Given the breadth of the issues raised by the comments, we focus in on six questions answered by commenters that we think are the most salient. These are:

- Does the SEC have authority to mandate climate disclosures, and would doing so survive the cost-benefit analysis required for rulemaking?

- Given a perceived desire for both meaningful and comparable climate disclosures, which types of disclosure standards (e.g., general or industry-specific standards, a single global standard or multiple standards around the world and a standard drawing on existing third-party frameworks or a novel framework) should the SEC use for any mandatory climate disclosure regime?

- If the SEC mandates climate disclosures, what information should the SEC require to be disclosed?

- Should the SEC provide protection from liability, whether through a safe harbor, having climate disclosures be furnished rather than filed or by requiring disclosures on a specialized form outside of 10‑Ks and 10-Qs?

- Should climate disclosures be subject to the same level of rigor as other types of SEC disclosures, such as financial disclosures, by imposing requirements for audit or assurance or internal controls?

- If the SEC creates a new disclosure mandate, should its scope include not only public companies but also private companies and not only climate disclosures but also ESG disclosures more broadly?

We discuss each of these areas in additional detail below, along with charts showing the distribution of the positions taken by commenters in these areas. Although the discussions are informed by the RFPI and comments broadly, the charts reflect only the thirty comments that we summarize in detail in the Appendix. For each chart, we present the distribution of these thirty commenters who supported, opposed or gave a mixed response on a particular topic within the six questions outlined above. [4]

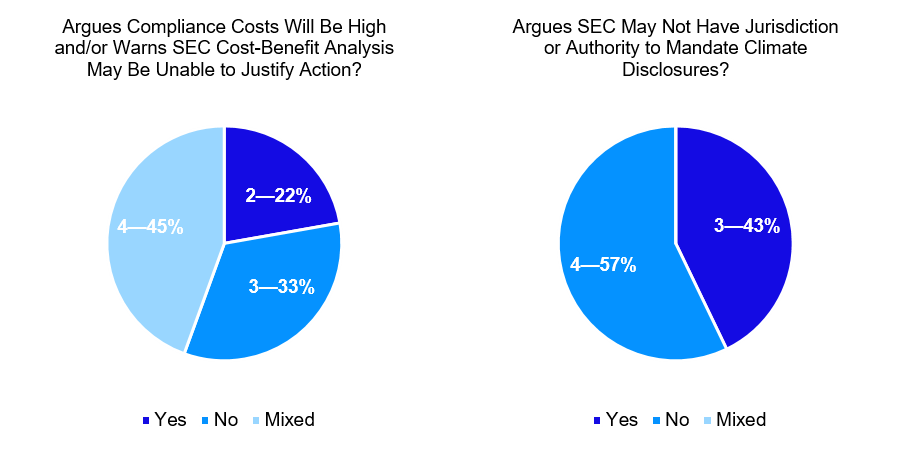

1. Does the SEC have jurisdiction and do benefits outweigh costs?

Some commenters emphasized that even if the SEC wishes to initiate a rulemaking to mandate climate disclosures, they believe that the SEC may not have the authority to do so. In our review of the comments, we observed several forms of this line of reasoning. Some argued that the SEC would need specific statutory authorization to mandate climate disclosures because its current rulemaking authority does not cover the disclosures at issue. Others argued that mandatory climate disclosures would be compelled speech in violation of the First Amendment. Still others highlighted the high compliance costs associated with climate disclosures, particularly for smaller registrants, and either stated or implied that an SEC mandate might not survive the cost-benefit analysis required for SEC rulemaking. [5]

In contrast, other commenters assumed the SEC would have the power to act or have made that argument explicitly. Commissioner Lee gave a speech in May 2021 to counter the “myth” that SEC disclosure rulemaking authority is limited to information that is material under the securities laws. Commissioner Lee argued that the SEC has broad rulemaking authority to require disclosures in the public interest, and that this authority is not limited by materiality. [6]

The following charts provide a graphical summary of the views on these questions among the set of thirty comments discussed in detail in the Appendix.

Does the SEC have jurisdiction and do benefits outweigh costs?*

* The pie charts include data for those of the thirty comment letters summarized in the Appendix that addressed the corresponding question. Because different comments focused on different topics raised in the RFPI, each pie chart reflects data for fewer than all thirty of the comment letters we summarize. A commenter’s response is designated as “mixed” if the comment both discussed the question and either provided some support and some opposition for the question or did not provide a clear directional view. Labels of “X—Y%” indicate the count of X responses followed by the Y% of the total in the chart they represent.

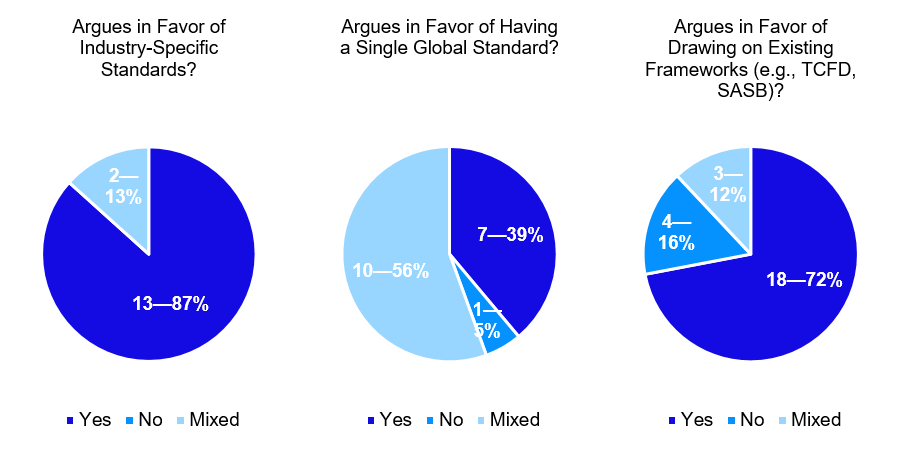

2. Which standards should the SEC adopt?

The RFPI raised multiple questions addressing which standards the SEC should use if it were to mandate climate disclosures. These included whether standards should vary by industry, how standards applicable to U.S. registrants should relate to other standards globally and how the SEC’s rules should draw upon frameworks already developed by standard-setting bodies.

Industry-specific standards present a potential trade-off between making climate disclosures meaningful and making them comparable. Some commenters expressed a strong desire for industry-specific standards, arguing that the climate aspects of various industries are sufficiently different such that industry-by-industry disclosures are necessary to meaningfully inform investors. Others stressed the importance of universal disclosures that apply to all registrants so that climate risks can be more easily compared across companies.

Aside from whether climate disclosure standards should be industry-specific or universal, commenters also opined on SEC coordination with global climate disclosure efforts. Many commenters encouraged the SEC to contribute to, and work through, international efforts to establish a harmonized global standard. This would promote consistency of disclosures across jurisdictions. Others stressed the need to act quickly or called attention to unique features of the U.S. securities law regime that would merit the SEC establishing its own standards, even if those standards differ from others around the globe.

On the related question of whether the SEC should leverage the work of existing climate standard-setting bodies, including international bodies, some commenters argued that the SEC should draw upon existing standards—such as those created by the Task Force for Climate-Related Financial Disclosures (TCFD) or the Sustainability Accounting Standards Board (SASB)—for international harmonization, among other reasons. Others argued against doing so, either because of substantive disagreement with those standards, procedural concerns about the governance and funding of those standard setters or both.

The following charts provide a graphical summary of the views on these questions among the set of thirty comments discussed in detail in the Appendix to the complete publication.

Which standards should the SEC adopt?*

* The pie charts include data for those of the thirty comment letters summarized in the Appendix that addressed the corresponding question. Because different comments focused on different topics raised in the RFPI, each pie chart reflects data for fewer than all thirty of the comment letters we summarize. A commenter’s response is designated as “mixed” if the comment both discussed the question and either provided some support and some opposition for the question or did not provide a clear directional view. Labels of “X—Y%” indicate the count of X responses followed by the Y% of the total in the chart they represent.

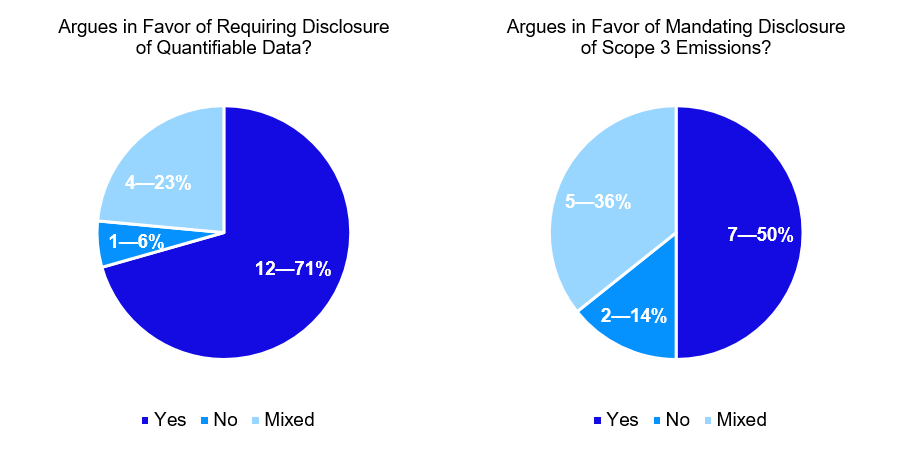

3. Qualitative vs. quantitative disclosures?

Beyond questions of whether the SEC should mandate climate disclosures and what standards it should use if it were to impose a disclosure mandate, the RFPI asked whether climate risk information can and should be quantified and disclosed, including, in particular, Scope 3 emissions. Unsurprisingly, commenters took opposing views.

Some commenters maintained that the SEC should require only qualitative climate disclosures, noting the difficulty of quantifying climate data, particularly Scope 3 emissions—those emissions that “are the result of activities from assets not owned or controlled by the reporting organization, but that the organization indirectly impacts in its value chain,” [7] such as the greenhouse gas emissions attributable to commercial real estate or motor vehicles that a bank finances. Others stressed that it is feasible and appropriate to require quantitative disclosures, which would allow for greater standardization and comparability across companies. These questions are intertwined with the question of whether disclosure standards should be industry specific, discussed above, or whether they should be tiered by company size or market capitalization, as quantification may be less burdensome for companies in certain industries as compared to others—for example, it is arguably easier for a large-cap technology company to measure and disclose accurately its Scope 3 emissions than it is for a small-cap financial institution whose customers are primarily private companies. As noted in their comments, some commenters already voluntarily disclose quantitative climate information, including Scope 3 emissions, which they cite as support that other registrants should be required to do the same.

The following charts provide a graphical summary of the views on these questions among the set of thirty comments discussed in detail in the Appendix to the complete publication.

Qualitative vs. quantitative disclosures?*

* The pie charts include data for those of the thirty comment letters summarized in the Appendix that addressed the corresponding question. Because different comments focused on different topics raised in the RFPI, each pie chart reflects data for fewer than all thirty of the comment letters we summarize. A commenter’s response is designated as “mixed” if the comment both discussed the question and either provided some support and some opposition for the question or did not provide a clear directional view. Labels of “X—Y%” indicate the count of X responses followed by the Y% of the total in the chart they represent.

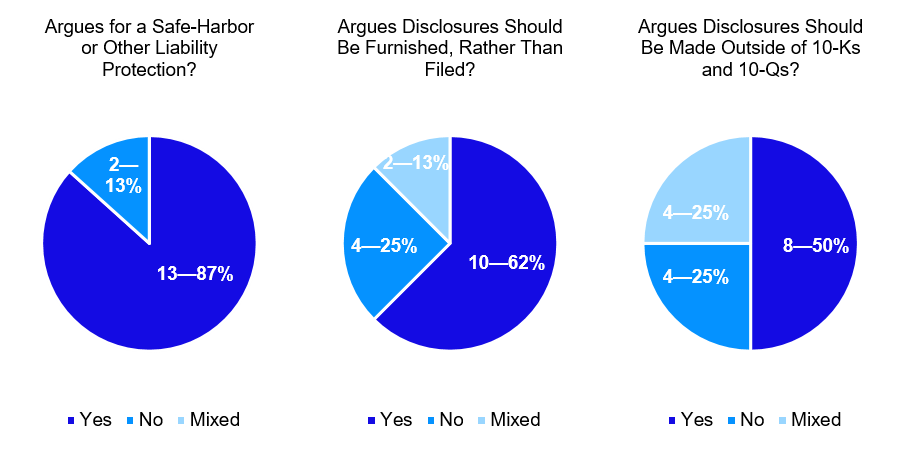

4. How should the SEC address potential liability?

A critical question for issuers is whether and, if so, how the SEC will “address the inevitable litigation risk that will come with such sweeping new disclosure requirements.” [8] In the comments on the RFPI, registrants and their trade organizations supported a number of different mechanisms to reduce potential liability. They argued that climate disclosures would present a heightened liability risk given the infancy of climate disclosures and unique features of climate disclosures, such as, for some registrants, necessary reliance on third parties to produce disclosures. Other commenters supported a robust liability regime as a means to enforce climate disclosure requirements and protect investors.

As evidenced by the comments, there are a number of forms that liability for climate disclosures could take. Although not addressed directly in the RFPI, some commenters recommended that the SEC provide a safe harbor from liability for climate disclosures, a position Commissioner Elad L. Roisman has also supported. [9] As part of the question of the form and provenance of liability, several commenters focused on where disclosures would be made and how they would be submitted to the SEC, topics on which the RFPI explicitly solicited comment. Some argued that climate disclosures should be furnished, rather than filed, to limit which securities law liability provisions would apply to the disclosures. [10] Similarly, some argued that disclosures should be provided on a separate, specialized disclosure form outside of 10-Ks and 10-Qs to limit potential application of certain liability provisions in the federal securities laws.

The following charts provide a graphical summary of the views on these questions among the set of thirty comments discussed in detail in the Appendix.

How should the SEC address potential liability?*

* The pie charts include data for those of the thirty comment letters summarized in the Appendix that addressed the corresponding question. Because different comments focused on different topics raised in the RFPI, each pie chart reflects data for fewer than all thirty of the comment letters we summarize. A commenter’s response is designated as “mixed” if the comment both discussed the question and either provided some support and some opposition for the question or did not provide a clear directional view. Labels of “X—Y%” indicate the count of X responses followed by the Y% of the total in the chart they represent.

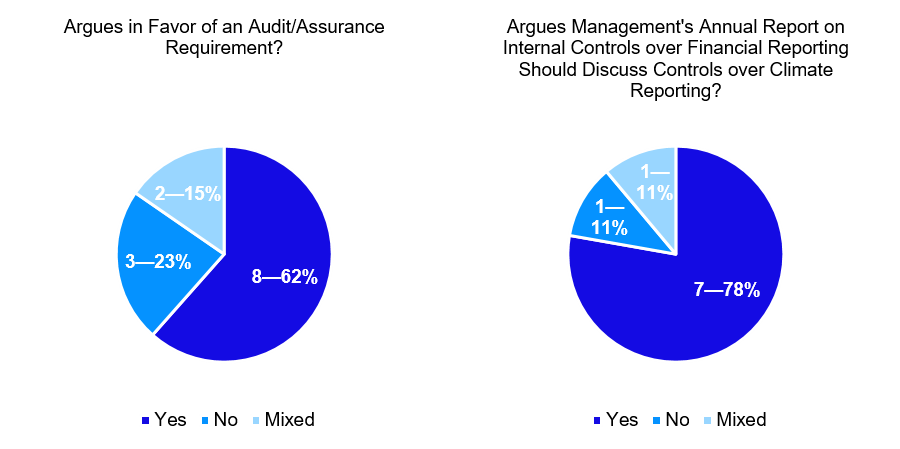

5. Audit or assurance of climate disclosures?

Several questions in the RFPI relate to measures the SEC might take to promote the reliability of climate disclosures, including measures similar to those used for SEC financial reporting. For example, the RFPI asked whether climate disclosures should be subject to audit or some other form of assurance and, if so, by whom. Another question asked whether management’s annual report on internal control over financial reporting should address controls over climate reporting and whether the CEO, CFO or other corporate officer should be required to certify climate disclosures.

Although some commenters were supportive of auditing or assurance, many others thought they would be a bridge too far. [11] Some of the opposition came from commenters who argued climate disclosures are not yet at the stage where it would be reasonable to apply the same degree of rigor as applicable to financial disclosures. Others appealed to more pragmatic reasons, citing insufficient expertise to conduct climate disclosure audits and explaining that the audit process for climate disclosures is currently so time consuming that disclosures would be stale by the time they were audited. Others—including third-party accounting and audit firms and some international investors—disagreed, highlighting the importance of having an audit or assurance process and explaining that, for some registrants, certain climate disclosures, such as GHG emissions, are already being assured.

The following charts provide a graphical summary of the views on these questions among the set of thirty comments discussed in detail in the Appendix.

Audit or assurance of climate disclosures?*

* The pie charts include data for those of the thirty comment letters summarized in the Appendix that addressed the corresponding question. Because different comments focused on different topics raised in the RFPI, each pie chart reflects data for fewer than all thirty of the comment letters we summarize. A commenter’s response is designated as “mixed” if the comment both discussed the question and either provided some support and some opposition for the question or did not provide a clear directional view. Labels of “X—Y%” indicate the count of X responses followed by the Y% of the total in the chart they represent.

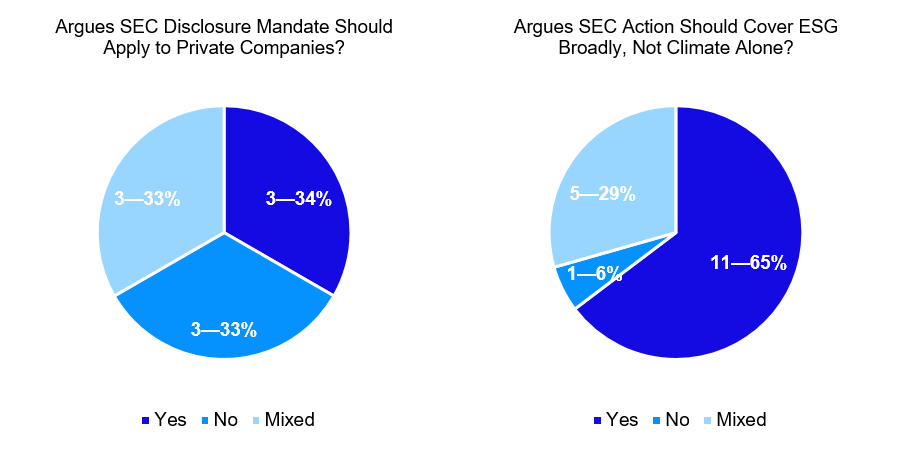

6. What should be the scope of any SEC action?

The RFPI raised important questions regarding to whom and over what subject matter any new SEC disclosure requirements might apply. Although much of the RFPI focused on the details of how to implement a climate disclosure regime, these big-picture scoping issues remain open questions.

With respect to scope of covered companies, the RFPI asked whether the SEC should subject private companies to a climate disclosure requirement. Some commenters, such as certain standard setters and investors, supported expanding the requirements to private companies, explaining that investors would benefit from climate disclosures from private companies just as they would from public companies. Some argued that failure to treat public and private companies similarly could result in regulatory arbitrage and could discourage private companies from going public, as well as create a different regulatory regime as compared to the one developing in Europe. In contrast, other commenters argued it would be unnecessary, or even inappropriate, for the SEC to impose a mandate on private issuers, citing reasons including the limited scope of impact of exempt offerings and jurisdictional grounds.

With respect to the scope of subject matter, the RFPI asked whether the SEC should address only climate disclosures at this time or should instead address climate disclosures as part of a broader ESG disclosure framework. Some commenters argued that climate is so important that the SEC should address it first, while acknowledging the importance of ESG matters more broadly. Others opposed mandatory ESG disclosures altogether. Still others supported including climate as part of a broader ESG disclosure package.

The following charts provide a graphical summary of the views on these questions among the set of thirty comments discussed in detail in the Appendix.

What should be the scope of any SEC action?*

* The pie charts include data for those of the thirty comment letters summarized in the Appendix that addressed the corresponding question. Because different comments focused on different topics raised in the RFPI, each pie chart reflects data for fewer than all thirty of the comment letters we summarize. A commenter’s response is designated as “mixed” if the comment both discussed the question and either provided some support and some opposition for the question or did not provide a clear directional view. Labels of “X—Y%” indicate the count of X responses followed by the Y% of the total in the chart they represent.

What’s next?

Although the SEC’s RFPI was exploratory and not an official proposal, it is widely expected that the SEC will proceed next to a notice of proposed rulemaking with the SEC’s initial answers to the questions above. As noted above, in the Spring 2021 Unified Agenda of Regulatory and Deregulatory Action published on June 11, 2021, the SEC included that it intends to issue a notice of proposed rulemaking on climate disclosures in or before October 2021. This intention was crystalized in SEC Chair Gensler’s June 23, 2021 speech, in which he noted that he is “really struck by the call for enhanced disclosures” in comment letters responding to the RFPI. He stated that he has asked SEC staff to develop recommendations on mandatory climate disclosures, including evaluating a range of metrics and considering potential requirements for companies that make forward-looking climate commitments.

Separately, we understand from SEC staff that they are hard at work evaluating the comments on the RFPI. And although SEC staff met with dozens of stakeholders regarding the RFPI in the lead-up to the June 13, 2021 submission deadline, as the SEC has memorialized here, since the deadline the SEC staff have reported only one meeting.

All this points to an upcoming SEC proposal, which, like the RFPI, is sure to solicit a high volume of feedback from key stakeholders with diverse perspectives. Unlike the RFPI, any SEC notice-and-comment rulemaking would be subject to the requirements of the Administrative Procedure Act (APA), [12] and the SEC would be required to respond in a final rule to “materially cogent” comments. [13] The rulemaking process would therefore give the public a second bite at the apple beyond the RFPI, and one the SEC would have to address head on.

On the international front, global bodies focused on climate disclosures also continue to forge ahead. For example, on June 28, the board of the International Organizations of Securities Commissions (IOSCO) issued a report on sustainability-related issuer disclosures. The report, developed by IOSCO’s Sustainability Finance Taskforce, highlights the need to enhance consistency, comparability and reliability of sustainability reporting for investors, citing the recent June 5 G7 Finance Ministers and Central Bank Governors Communiqué to a similar effect. IOSCO’s report is supportive of the work of the International Financial Reporting Standards Foundation (IFRS Foundation) to establish an International Sustainability Standards Board (ISSB) for developing a climate reporting standard. The report notes that IOSCO has established a Technical Expert Group (TEG)—which is co-led by the SEC—to engage with the IFRS Foundation on the ISSB, and calls for creating standards leveraging the work of existing frameworks, including those of TCFD, the Global Reporting Initiative (GRI) and SASB, among others.

We will continue to monitor developments both domestically and internationally as the SEC evaluates public input and moves toward a proposal and, later, a final rule.

The complete publication, including appendix, is available here.

Endnotes

1See SEC, Commission Guidance Regarding Disclosures Related to Climate Change, 75 Fed. Reg. 6290 (Feb. 8, 2010).(go back)

2Comment letters are typically uploaded to the SEC’s website with a lag. We use the SEC’s June 13 comment deadline as a cutoff for the letters in scope for our analysis, but it is possible additional letters submitted prior to the deadline were uploaded subsequent to preparation of this client update. In addition, some comments were submitted subsequent to the June 13 deadline, and the SEC has been uploading these comments to its website, but these letters are not included in our analysis. As discussed further below, we also exclude from our analysis form letter comments that may have been submitted by either institutions or individuals.(go back)

3Neither the comments from individual commenters nor the form letter comments are included in our analysis.(go back)

4For any particular topic, commenters are excluded from the chart if they did not address the issue. We recorded a response as “mixed” if a commenter both discussed the topic and either provided some support and some opposition for the topic or did not provide a clear directional view.(go back)

5See 15 U.S.C. §§ 77b(b), 78c(f) (requiring, as part of any rulemaking under the Securities Act of 1933 and Securities Exchange Act of 1934, respectively, in which the SEC “is required to consider or determine whether an action is necessary or appropriate in the public interest,” that the SEC “also consider, in addition to the protection of investors, whether the action will promote efficiency, competition, and capital formation”); see also, e.g., Business Roundtable v. SEC, 647 F.3d 1144, 1148–49 (D.C. Cir. 2011) (vacating the SEC’s proxy access rule for failure to “adequately assess the economic effects of a new rule,” as required by Section 3(f) of the Securities Exchange Act of 1934 and Section 2(c) of the Investment Company Act of 1940, 15 U.S.C. §§ 78c(f), 80a-2(c), by, among other things “inconsistently and opportunistically fram[ing] the costs and benefits of the rule” and “fail[ing] to adequately quantify the certain costs or to explain why those costs could not be quantified”).(go back)

6For this proposition, Commissioner Lee cited to the SEC’s rulemaking authority under the Securities Act of 1933 and the Securities Exchange Act of 1934, 15 U.S.C. §§ 77g(a)(1), 78m(a), 78l(b), and 78o(d).(go back)

7U.S. Environmental Protection Agency (EPA), EPA Center for Corporate Climate Leadership, Scope 3 Inventory Guidance (May 18, 2021), available at https://www.epa.gov/climateleadership/scope-3-inventory-guidance. The EPA explains that Scope 3 emissions are often the majority of an organization’s greenhouse gas emissions, and the EPA distinguishes these from Scope 1 and Scope 2 emissions. See id. As defined by the EPA, “Scope 1 emissions are direct greenhouse (GHG) emissions that occur from sources that are controlled or owned by an organization (e.g., emissions associated with fuel combustion in boilers, furnaces, vehicles),” and “Scope 2 emissions are indirect GHG emissions associated with the purchase of electricity, steam, heat, or cooling.” EPA, EPA Center for Corporate Climate Leadership, Scope 1 and 2 Inventory Guidance (Dec. 14, 2020), available at https://www.epa.gov/climateleadership/scope-1-and-scope-2-inventory-guidance.(go back)

8Commissioner Elad L. Roisman, Putting the Electric Cart before the Horse: Addressing Inevitable Costs of a New ESG Disclosure Regime (June 3, 2021), available at https://www.sec.gov/news/speech/roisman-esg-2021-06-03.(go back)

9See id.(go back)

10The difference may appear to be one of semantics, but it is far from that. Unlike filings with the SEC, furnished reports are not subject to potential liability under Section 18 of the Securities Exchange Act of 1934. See 15 U.S.C. § 78r. Moreover, certain standard filings, such as 10-Ks and 10-Qs, are routinely incorporated by reference in the securities offering documents of issuers, to which potential liability attaches under several provisions—including some strict liability provisions—of the Securities Act of 1933.(go back)

11This observation relates to the institutional comments at large, as our set of thirty comments discussed in detail in the Appendix—which includes several audit firms—may not be representative with respect to this question.(go back)

12See 5 U.S.C. § 553.(go back)

13See, e.g., United States v. Nova Scotia Food Products Corp., 568 F.2d 240, 252 (2d Cir. 1977) (“Appellants additionally attack the ‘concise general statement’ required by APA, 5 U.S.C. § 553, as inadequate. We think that, in the circumstances, it was less than adequate. It is not in keeping with the rational process to leave vital questions, raised by comments which are of cogent materiality, completely unanswered. The agencies certainly have a good deal of discretion in expressing the basis of a rule, but the agencies do not have quite the prerogative of obscurantism reserved to legislatures.”).(go back)