Print

PrintDon Fancher is Principal of Risk & Financial Advisory at Deloitte Financial Advisory Services LLP; Robert Lamm is an Independent Senior Advisor and Debbie McCormack is Managing Director, both at the Center for Board Effectiveness, Deloitte LLP. This post is based on their Deloitte memorandum.

Introduction

The responsibilities of boards of directors continue to evolve and increase, particularly given the events of the past year. In addition to perennial topics such as strategy, succession, financial reporting, compliance, and culture, boards are experiencing broader demands on their oversight from expanding stakeholder and shareholder considerations; continuing challenges of the ongoing global pandemic and its aftermath; and addressing the changing role of the corporation in society at large on matters such as racial justice and climate. The growth in the number and complexity of board responsibilities is taking place in an environment of growing skepticism towards our various institutions.

Against that background, companies and their boards can help to address these multiple challenges by considering one of the most critical assets not on their balance sheets―trust.

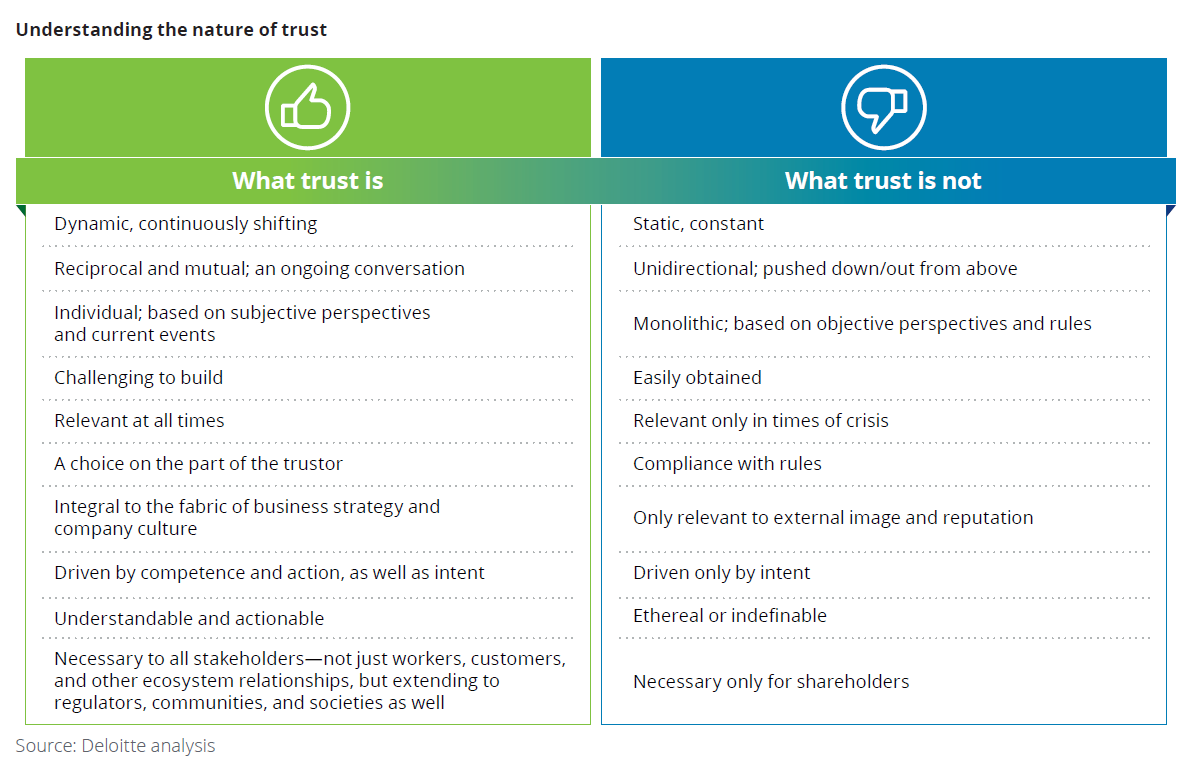

What is trust?

Trust has been defined as “our willingness to be vulnerable to the actions of others because we believe they have good intentions and will behave well toward us.” [1] However, particularly for a business enterprise, trust is not an ephemeral quality or attitude. Rather, it is a critical asset, albeit one that is not reported on the balance sheet or otherwise in the financial statements, as it has no intrinsic value.

However, trust is very real and concrete. When invested by leaders in relationships with stakeholders, it enables activities and responses that can help build or rebuild an organization and enable an organization to achieve its intended purpose. Trust can also be created across various groups within the organization―between the board and management, employer-employee, among the workforce, organization and stakeholder, vendors and customers. Conversely, a breach of trust can cause a company to lose significant value. For example, a Deloitte Canada analysis found that three large global companies, each with a market cap of more than $10 billion, lost from 20% to 56% of their value, or a total of $70 billion, when they breached their stakeholders’ trust. [2]

In other words, although trust does not appear on the balance sheet, it is a critical asset that can have a huge impact―positive or negative―on an organization’s market value.

The role of the board and basics

There seems little doubt that boards are responsible for overseeing trust as a corporate asset. Oversight of trust is critical to the board’s key role in overseeing strategy―increasing trust and thereby increasing value―and risk-mitigating reductions in trust and resultant reductions in value. Moreover, boards cannot ignore an asset that can so greatly influence the value of the enterprise.

Sandra Sucher, Harvard Business School Professor of Management, studies the role of executive leadership and trust. She emphasizes the important role boards play:

“Great boards lead when it comes to creating an atmosphere and philosophy of trust. Directors serve as a critical link between the management inside an organization and those stakeholders on the outside. Fundamentally, trust in an organization is built on both competence and intent―specifically the perception of an organization’s motives, means and impact. An effective board will cultivate trust within the board, and relationships in and outside the organization to ensure that trust is nurtured and maintained.” [3]

To effectively oversee trust, a board should start with some basic understandings, as follows:

- Trust is manageable: Leaders can build and maintain trust by acting with competence and intent. Competence refers to the ability to execute―to follow through on what you say you will do. Intent refers to the meaning behind a business leader’s actions― taking decisive action from a place of genuine empathy and true care for the wants and needs of stakeholders while being transparent in doing so. [4] The effectiveness with which an organization acts with competence and intent can be measured, managed and tracked over time.

- Trust is owned by management; the board’s role is oversight: Trust is built from the inside out. [5] The C-suite has the in-depth understanding of the company and its strengths and vulnerabilities needed to effectively manage trust through competence and intent across the entire organization. The board’s role with respect to trust is oversight rather than ownership.

- Trust is all-encompassing and ever-changing: Trust―or its absence―extends to all aspects of the company, and permeates the culture of the company. Trust constantly evolves as the company changes and responds to internal and external developments and challenges. For example, companies’ responses to the pandemic have had significant impact on how their workforces and other stakeholders viewed them from the perspective of trust. [6]

- Trust is a critical part of the “tone at the top”: Trust is a critical component of how the board and management function, both within themselves as well as in their dealings with each other. Can directors have candid discussions and even disagreements without losing trust in each other? Will the constructive tension between the board and management render trust between the two difficult or impossible to maintain?

Practical steps for the board

Beyond the basics, there are steps that boards can take to build and maintain high levels of trust in the organization.

The board can, and arguably should, govern and influence the strategic direction that the company needs to develop and maintain high levels of trust in everything it does. As noted above, the board needs to make it clear that management, rather than the board, “owns” and is responsible for the trustworthiness of the organization.

For the board to effectively oversee trust, management needs to provide a trust “baseline” so that the board can determine the extent to which, and the areas in which, the company is trusted or where trust needs to be established or strengthened. For example, a company may be trusted for the quality of its products but not for its approach to workforce wellness or diversity, equity, and inclusion. In other words, the company may be trusted in some areas but not in others. Accordingly, establishment of a baseline requires that trust be measured across the company’s various constituencies and across operating areas. To create this baseline, management can conduct a survey or leverage trust measurement tools to assess stakeholder trust in specific operating domains such as customer experience, cyber security, the company’s ethics program or overall culture.

Once the board understands the overall level of trust across the organization, it can then help management to address areas where trust may need to be developed or strengthened by prioritizing those areas and following up to evaluate whether and how management is handling them. This also entails helping management to:

- identify or question vulnerabilities or factors that may undermine trust;

- prioritize which factors or areas require attention; and

- allocate resources to establish, maintain, and/or enhance trust with various stakeholders—even in cases that may require conflicting or inconsistent approaches.

Once the baseline is established, the board should monitor trust, through periodic reports from management, follow-ups with measurement processes and tools as referred to above, and to act, directly or through management, as needed when monitoring indicates that trust is at risk.

One method of monitoring and holding management accountable for trust is compensation―rewarding executives when performance meets or exceeds metrics, and reducing or withdrawing compensation when the metrics are not achieved. Currently, there is little indication that boards are adding trust metrics to the list of factors influencing executive compensation. However, given recent trends to include metrics for other “intangibles,” such as workforce health and well-being, into the mix of compensation metrics, trust may be added to that mix in time.

The board’s oversight of trust can be significantly impacted when a crisis occurs, and the board’s approach to the crisis is often based upon a calculus involving trust. In some cases, the board demonstrates solidarity with management and works with management to address the crisis and its causes in order to restore trust. In others, the board may view management, or one or more members of management, as the reason for a diminution of trust and may replace the management members―sometimes with a board member to serve on an interim basis. There are also situations in which the board’s initial support for an executive declines when trust is not restored.

Questions for the board to consider asking:

- What is our current “baseline” of trust? In what areas is trust strongest? Weakest?

- Are we looking at others in the marketplace to evaluate our relative strengths, weakness, and vulnerabilities with respect to trust?

- Where are our trust vulnerabilities? Do we have plans to address these?

- What areas need to be priorities in building, sustaining, or re-establishing trust?

- What resources do we have/need to build/maintain/ increase trust?

- Do all in management understand their roles in building and maintaining trust?

- Do some of our stakeholders have different needs when it comes to building and maintaining trust? Are we considering how to address these different needs and possible conflicts among them?

- Does the board have the right skill sets/competencies to engender trust (e.g., industry expertise, demographics)?

- Where does trust “reside” in the board? A committee― and if so, which one? Or at the full board level?

- How can we appropriately incentivize management to address trust?

Trust issues affecting global companies

Given the differences in culture and other norms across different countries and regions, issues that global boards may face include:

- Does “trust” mean different things in different countries and cultures?

- How do boards of global companies reflect cultural and value-based norms given the variations in these norms across different countries and regions?

- Given the view that building and maintaining trust calls for competence and intent, how do boards of global companies “enforce” intent across geographical regions with different policies and expectations?

Avoid common pitfalls

In addition to the risks posed by a lack of trust within the board and/ or between the board and management, discussed earlier, there are some other pitfalls that boards should be aware of as they monitor and seek to enhance trust.

Boards as well as managements need to be aware of and seek to avoid “normalcy bias”―the tendency for people to avoid or deny change. Particularly in times of disruption, it can be easier to take the path of least resistance by saying, in effect, “there’s too much going on now; let’s hold off on acting until things calm down.” Aside from the fact that things may not calm down or may take a long time to do so, companies may be able to engender trust more effectively during a crisis if management and the board appreciate the potential impact of the disruption and assiduously seek strategies to address that impact.

In addition, it may be difficult for a board to effectively oversee trust if its members do not have sufficient experience in areas that are critical for the company. As a result, board composition can be an important factor in establishing and maintaining trust. Boards whose members have diverse skills or backgrounds may be better positioned to ask the important questions that prompt the organization to explore opportunities or risks that will impact trust. For example, a manufacturing organization should consider having on its board someone with an understanding of safety features relevant to that industry to better probe for the biggest company risks.

Wrapping it up

Demonstrable trust―including proactive oversight and management of trust―can be a great influencer of value and minimizer of risk, and can be a significant component of being a resilient organization. Consequently, boards need to engage in oversight of trust as they oversee other areas. With appropriate levels of board engagement and oversight of trust, companies can enhance their trustworthiness and increase value.

Endnotes

1Sandra Sucher and Shalene Gupta, “The Trust crisis,” Harvard Business Review, July 23, 2021.(go back)

2See “Trust as a Driver of Enterprise Value,’ at https://deloitte.wsj.com/riskandcompliance/2021/03/04/Trust-as-a-driver-of-enterprise-value/.(go back)

3Sandra Sucher, Professor of Management Practice Harvard Business School, email communication with the authors, April 2, 2021.(go back)

4See https://www2.deloitte.com/us/en/insights/economy/covid-19/building-trust-during-covid-19-recovery.html.(go back)

5See Note 1.(go back)

6See https://www2.deloitte.com/us/en/insights/economy/covid-19/building-trust-during-covid-19-recovery.html.(go back)