Print

PrintJohn Borneman is Managing Director, Tatyana Day is Senior Consultant, and Kevin Masini is a Consultant at Semler Brossy Consulting Group LLC. This post is based on a Semler Brossy memorandum by Mr. Borneman, Ms. Day, Mr. Masini, Matthew Mazzoni, and Jennifer Teefey. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) and Will Corporations Deliver Value to All Stakeholders?, both by Lucian A. Bebchuk and Roberto Tallarita; For Whom Corporate Leaders Bargain by Lucian A. Bebchuk, Kobi Kastiel, and Roberto Tallarita (discussed on the Forum here); and Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy—A Reply to Professor Rock by Leo E. Strine, Jr. (discussed on the Forum here).

As the use of ESG metrics in incentive plans continues to grow, we see a diverse set of models by which companies incorporate these metrics. As with many ‘non-financial’ metrics, the use of ESG metrics within a ‘scorecard’ is a common approach, although this is certainly not the only solution. We anticipate the evolution toward incorporating more weighted and prominent ESG structures into plan design to continue to grow in the coming years.

In this post, we analyze the reported design approach to incorporating ESG metrics into incentives within the S&P 500. For purposes of this analysis, we have categorized these design approaches into four groups:

ESG Metric Structure In Incentive Plans

The most common approaches to incorporating ESG metrics in incentive plans are to use them as part of a scorecard of non-financial or strategic objectives or as part of an individual performance assessment that is used to adjust incentive plan performance. Both of these models typically include a degree of subjectivity in assessing performance, especially in the case of individual performance assessments, which are often based on discretionary evaluations. While more formulaic and specifically-weighted metrics or modifiers are also used, these are less common for ESG metrics relative to the typical approach used for financial objectives. This finding is especially true for environmental and social sustainability measures, likely as a result of difficulties in quantifying, setting, and measuring goals and outcomes.

We note that regardless of the approach, metrics of focus in any incentive plan do not need to have a large weighting to be effective. Even a relatively limited impact on inventive payouts can be meaningful by signaling the importance of core principles and objectives of the business.

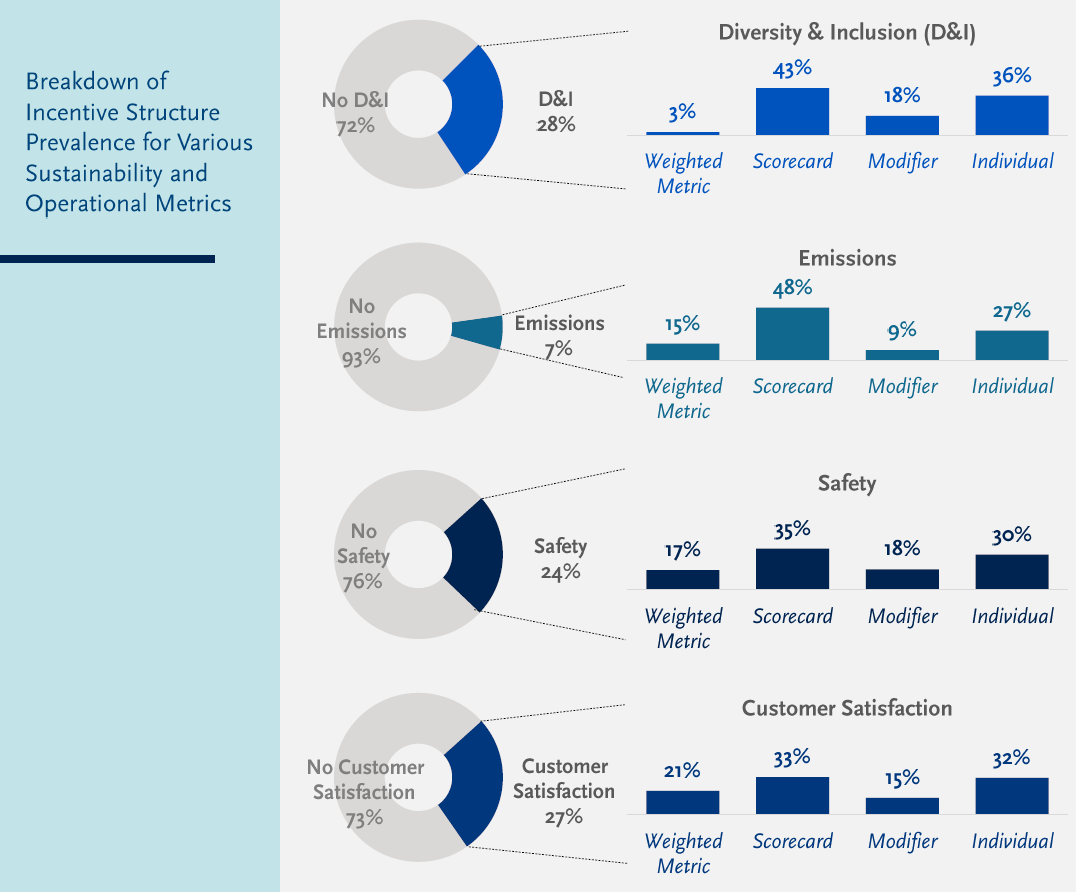

Examples of Sustainability vs. Operational Metrics

Looking at the most common ESG metrics in incentive plans in more detail, we see these trends highlighted even more prominently. Diversity & Inclusion (D&I), for example, is rarely a separate and individually weighted metric, and both D&I and Emissions are frequently part of scorecards. Customer Satisfaction, on the other hand, is more often explicitly weighted, likely because it is easier to quantify. That said, scorecards or individual performance assessments are still the most frequently used across measurement types.

ESG Metric Structure In Long-Term Incentives

Currently, it is rare for companies to adopt ESG metrics in long-term plans. With less than 5% of companies in the S&P 500 using ESG in performance shares, the practice is far less common than ESG adoption in annual plans (57%). However, where there are longer-term ESG metrics, the measures tend to be incorporated as stand-alone weighted components or as part of a broader scorecard. The greater prevalence of weighted metrics in long-term vs. annual plans is not surprising, as fixed accounting requires that specific and quantifiable goals for performance shares are set in advance. With the focus on more quantitative goals, it’s also no surprise that long-term ESG measures focus mostly on operational metrics, such as Customer Satisfaction, rather than sustainability metrics.

In addition to the accounting complexities and the desire to maintain an element of discretion in the assessment of sustainability objectives, some companies have intentionally selected the annual incentive plan to drive greater accountability for progress toward a longer-term goal. Annual incentives have a degree of ‘immediacy’ in terms of making progress of ESG goals that may not be as strong as in a long term plan. That said, we expect the adoption of ESG in performance shares to increase over time as overall shareholder feedback continues to push for ESG within long-term designs.

Conclusion

Quantitative measures are one way of defining ESG success, but they are not the only way to successfully incorporate these metrics into incentives. It is not surprising that most ESG incentive metrics today are included as part of a broader scorecard or as part of a more discretionary individual assessment. The adoption and higher prevalence of these structures make sense when considering the recent stakeholder focus on sustainability measures, many of which can be difficult to calculate and quantify. Naturally, the harder it is to quantify a goal or outcome, the more likely companies will lean toward a more discretionary approach. In addition, many companies have always measured non-financial metrics in a more discretionary framework, and this trend will likely continue as more and more companies adopt ESG in pay. At the same time, as companies continue to evaluate the importance of ESG, those that currently use a more discretionary structure might consider whether a more prominent and discrete role for ESG may be appropriate.

The complete publication is available here.