Print

PrintAudra Cohen and Melissa Sawyer are partners at Sullivan & Cromwell LLP. This post is based on a Sullivan & Cromwell memorandum by Ms. Cohen, Ms. Sawyer, Eric Krautheimer, and Matthew Goodman.

Executive Summary

Within the consumer industry, mega-cap (>$70B market cap) and large-cap ($20B to $45B market cap) companies show varying degrees of conformity in corporate governance practices. Notably, slight differences between mega-cap and large-cap consumer companies exist regarding board composition, committee structure, diversity, shareholder rights, shareholder composition and corporate disclosures. [1]

In regard to board composition, mega-cap consumer companies have less board refreshment, greater recruitment of board members with consumer or retail industry knowledge, and greater likelihood of having separate CEO and Chair positions when compared to large-cap consumer companies. Furthermore, although each consumer company has at least an audit committee, a compensation committee, and a corporate governance committee pursuant to stock exchange rules, mega-cap consumer companies on average have more committees dedicated to discrete oversight areas, such as innovation or technology development, than large-cap companies. Mega-cap companies also tend to make more public disclosures regarding their diversity, equity, and inclusion data, though they have a slightly lower percentage of their boards composed of female directors and have a slightly higher percentage of their boards composed of racially or ethnically diverse directors. Regarding shareholder rights, mega-cap consumer companies are slightly more likely to grant the right to call a special meeting of their shareholders and have lower shareholder ownership thresholds for calling special meetings. They are also more likely to grant shareholders the right to act by written consent. However, mega-cap consumer companies have lower say-on-pay approval rates compared to large-cap companies. Notably, as compared to large-cap consumer companies, mega-cap consumer companies are also less often controlled by their founders’ family members and tend to have more dispersed share ownership. Finally, while both mega-cap and large-cap consumer companies commonly publish disclosures and reports concerning various metrics, including metrics related to sustainability and social responsibility, there are differences in the types of disclosure frameworks used and kinds of information disclosed.

For purposes of our analyses, we reviewed the corporate governance practices of the 18 consumer companies identified in Annex A. Of these consumer companies, eight are mega-cap consumer companies and ten are large-cap consumer companies. While broad industry trends are informative, boards of consumer companies should tailor their governance models to the particular characteristics of their companies and the needs of their investors and other stakeholders.

I. Trends in Board Composition

A. Board Refreshment

In recent years, nearly all mega-cap and large-cap consumer companies have adopted mandatory director retirement ages in their corporate governance guidelines. Some companies have also adopted specified term limits for non-employee directors.

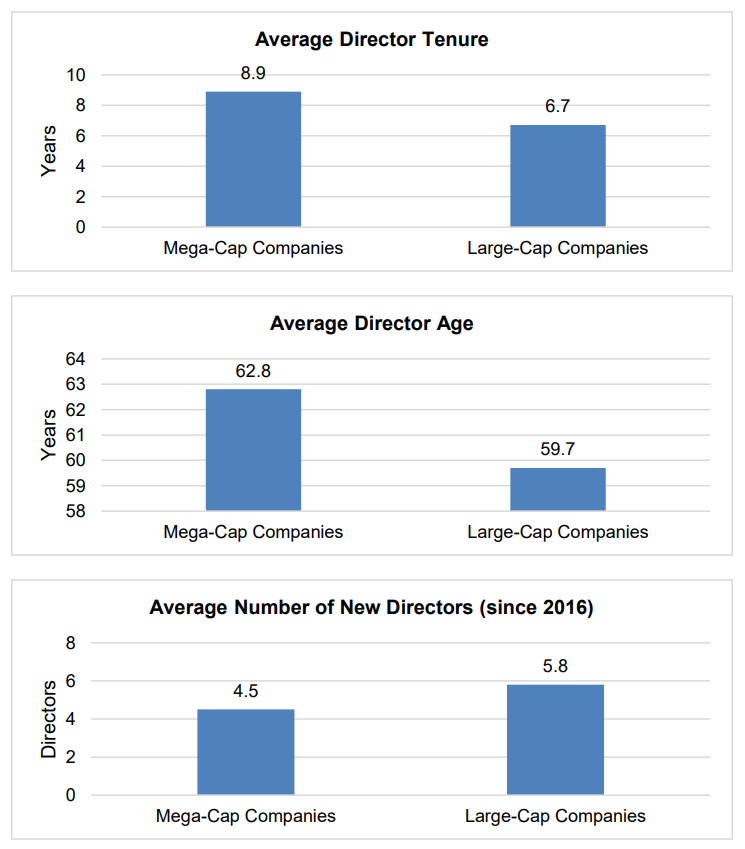

As compared to mega-cap consumer companies, large-cap consumer companies appear to have more frequent board refreshment. On average, directors of large-cap consumer companies have lower ages and shorter tenures than directors of mega-cap companies. Large-cap consumer companies have elected an average of 5.8 new directors to the board in the past five years as compared to only 4.5 for mega-cap companies, and large-cap companies have an average director tenure of 6.7 years as compared to mega-cap consumer companies, with an average director tenure of 8.9 years. One caveat to this general trend, however, is that the average tenure of mega-cap consumer companies may have been skewed to the higher end by an outlier—directors in one mega-cap company (Estée Lauder) have an average tenure of 17.3 years, whereas directors in the remaining seven mega-cap companies examined have an overall average tenure of 7.7 years. Regardless, even excluding this outlier, the average tenure in mega-cap companies still exceeds the average tenure in large-cap companies by approximately one year.

B. Board Evaluation

All consumer companies sampled conduct annual board evaluations and director self-evaluations overseen by their respective governance committees. All mega-cap and large-cap consumer companies also have a lead independent director that is appointed annually when the board chair is not an independent director, and this lead independent director is often involved with the evaluation process. Two large-cap consumer companies also noted in their proxy statements that they periodically engage a third-party consultant to conduct interviews with each director for the evaluation process, while no mega-cap consumer companies did the same.

C. Board Expertise

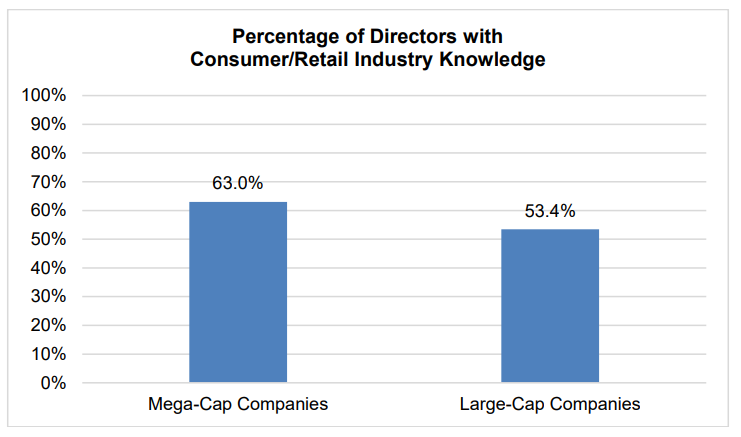

On average, mega-cap consumer companies have elected a larger percentage of directors with industry-specific knowledge than large-cap consumer companies. Boards of both mega-cap and large-cap consumer companies also recruit directors with expertise in technology, e-commerce, finance, government and regulation, and international or emerging markets.

To provide a clearer presentation of director expertise, most mega-cap consumer companies use summary charts, graphs, and diagrams to highlight specific areas of expertise in their proxy statement disclosures about their board composition. While some large-cap consumer companies have started to use similar visuals in their proxy statements, others still rely purely on traditional narratives.

D. CEO/Chair Structure

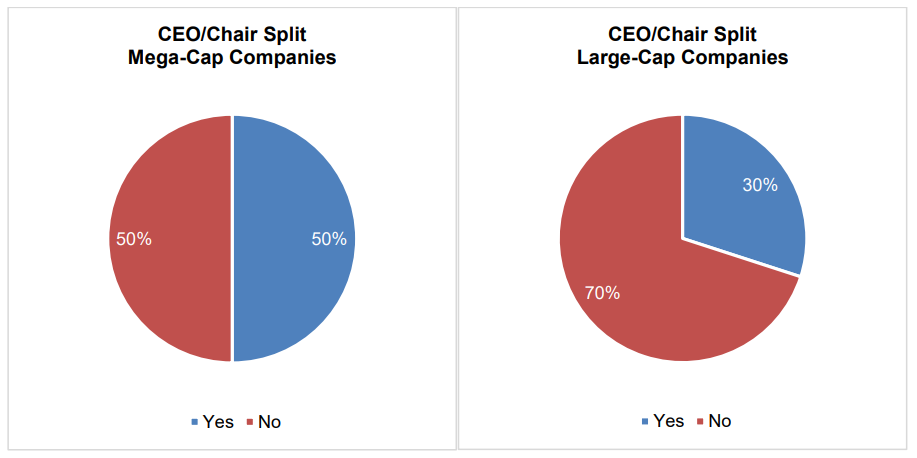

Over the past decade, many S&P 500 companies have split their CEO and Chair roles. [2] Institutional investors pushing for this change have argued that combined CEO/Chairs dominate decision-making processes and make it hard for boards to evaluate management performance objectively. In the face of this pressure from institutional shareholders, 50% of mega-cap consumer companies separate CEO and Chair positions, but only 30% of large-cap companies have followed suit. As noted above, companies that retain combined CEO/Chair positions have established the role of lead independent director and generally emphasized in their proxy statements that the authority granted to the lead independent director sufficiently ensures the independence of board decision-making. To preserve flexibility with respect to their future leadership structure, some companies that currently separate their CEO/Chair roles have declined to adopt a policy mandating a permanent CEO/Chair split in their governance guidelines.

E. Number of Board Meetings

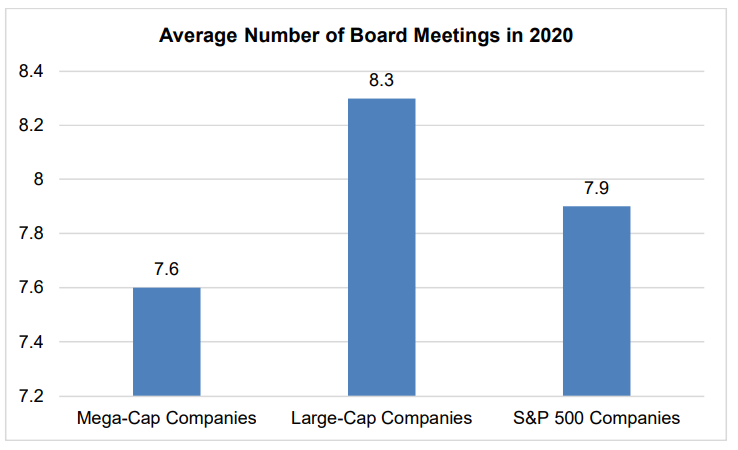

In 2020, boards of S&P 500 companies held 7.9 formal meetings on average. [3] This aligns with the average number of formal meetings held by both large-cap and mega-cap consumer companies in 2020. However, large-cap consumer companies met slightly more frequently than mega-cap consumer companies, with an average of 8.3 meetings in 2020 as compared to 7.6 meetings for mega-cap companies. There did not appear to be a significant increase in the number of board meetings in 2020 for either large-cap or mega-cap companies as a result of the COVID-19 pandemic as compared to the number of meetings in 2019.

II. Trends in Committee Structure

A. Number of Committees

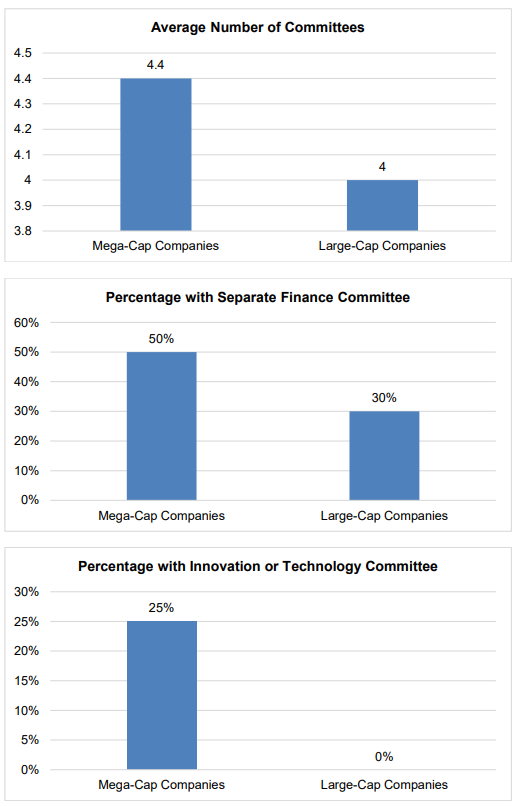

S&P 500 companies have an average of 4.2 committees per company, which has remained mostly unchanged during the past decade. [4] Consumer companies have generally followed this trend. Mega-cap consumer companies have an average of 4.4 board committees, while large-cap consumer companies have an average of 4.0 committees, which falls slightly below the S&P average. In accordance with stock exchange rules, each mega- or large-cap consumer company has at least three standing committees—an audit committee, a compensation committee, and a corporate governance committee—but mega-cap consumer companies more often than large-cap consumer companies have committees dedicated to certain other specific functions. For example, a larger percentage of mega-cap consumer companies have a separate finance committee. Moreover, some mega-cap consumer companies have established a dedicated committee for innovation or technology development, which no large-cap consumer company in the sample has done.

B. Committee Responsibilities

Consumer companies have also delegated certain key responsibilities to their existing board committees by reflecting a broader scope of responsibility for the particular committee in their committee charters. Nearly all consumer companies have charged their audit committees with cybersecurity oversight. Similarly, while only a small percentage of consumer companies have established a separate social responsibility committee, most companies surveyed have delegated social responsibility to their existing corporate governance committees. Boards of many consumer companies have also delegated human capital and diversity, equity, and inclusion oversight to their compensation and corporate governance committees.

III. Trends in Diversity, Equity and Inclusion (“DEI”)

A. Board Diversity [5]

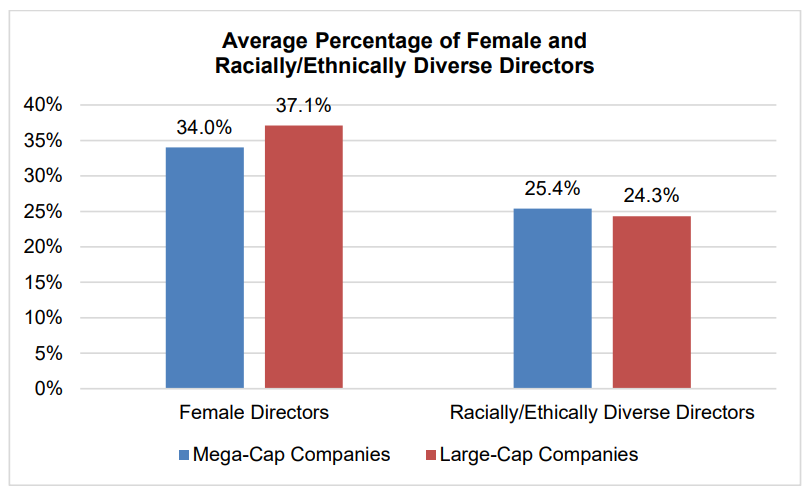

A small percentage of companies (one mega-cap company and two large-cap companies in the sample) still do not expressly disclose the gender and racial/ethnic composition of their directors in their most recent proxy statements. Additionally, many companies that have disclosed such data provide director diversity information only on an aggregate basis, and not on a director-by-director basis. Among companies that have disclosed their board composition data, the gender diversity of both mega-cap and large-cap consumer companies exceeds the S&P 500 average of 28.8%. [6] With an average of 34.0% female directors, boards of mega-cap consumer companies are slightly less diverse on average than large-cap consumer companies, where women hold 37.1% of board seats. Additionally, nearly every consumer company board has at least one female committee chair.

Mega-cap consumer companies tend to have a slightly larger percentage of racially or ethnically diverse directors than large-cap consumer companies. The greater racial or ethnic director diversity among mega-cap consumer companies, however, does not correlate to more racial or ethnic diversity in committee leadership roles. In our sample, only 50% of mega-cap consumer companies have racially or ethnically diverse committee chairs, as compared to 80% of large-cap consumer companies.

Of the companies sampled that are subject to various diversity requirements imposed by stock exchanges or state laws, all fulfilled these requirements. For example, all three companies listed on the NASDAQ Stock Exchange complied with NASDAQ’s requirement for a certain minimum number of diverse directors. [7]

B. Formal Diversity Policies and Oversight

Many S&P 500 companies have begun to include the so-called “Rooney Rule” diversity policy in their corporate governance guidelines. This formal diversity policy typically requires the board to interview at least one or more diverse candidates for open board positions. Consumer companies, however, generally have not followed this trend. While all mega-cap and large-cap consumer companies expressly state in their proxy statements that they consider diversity an important factor in evaluating director candidates, few have adopted a formal “Rooney Rule” type of diversity policy. Only one mega-cap consumer company and two large-cap consumer companies of those surveyed have disclosed a commitment to identifying and interviewing diverse director candidates.

C. Release of EEO-1 Data

All private-sector employers with 100 or more employees are required to submit their demographic workforce data to the U.S. Equal Employment Opportunity Commission in annual EEO-1 filings. [8] These filings provide information regarding the race, gender, and ethnic breakdown of various categories of employees, such as executives, professionals, sales workers, and laborers. Facing pressure from certain institutional investors, the majority of mega-cap consumer companies have released their EEO-1 data in the past few years. In comparison, only one large-cap consumer company in our sample has disclosed this information, with another one having expressed the intention to do so in the future. However, there is likely to be a shift in this disclosure trend in the future. In the 2021 proxy season, the number of shareholder proposals submitted relating to EEO-1 reporting and EEO policies nearly tripled compared to the previous season. [9] The average percentage of shareholder votes cast in favor of such proposals also increased from an average of 25% in 2020 to an average of 70% in 2021. [10] Organizations like State Street and the Office of the New York State Comptroller have also taken actions encouraging the disclosure of EEO-1 data in 2020 and 2021, respectively. [11]

IV. Trends in Shareholder Rights

A. Special Meeting Rights

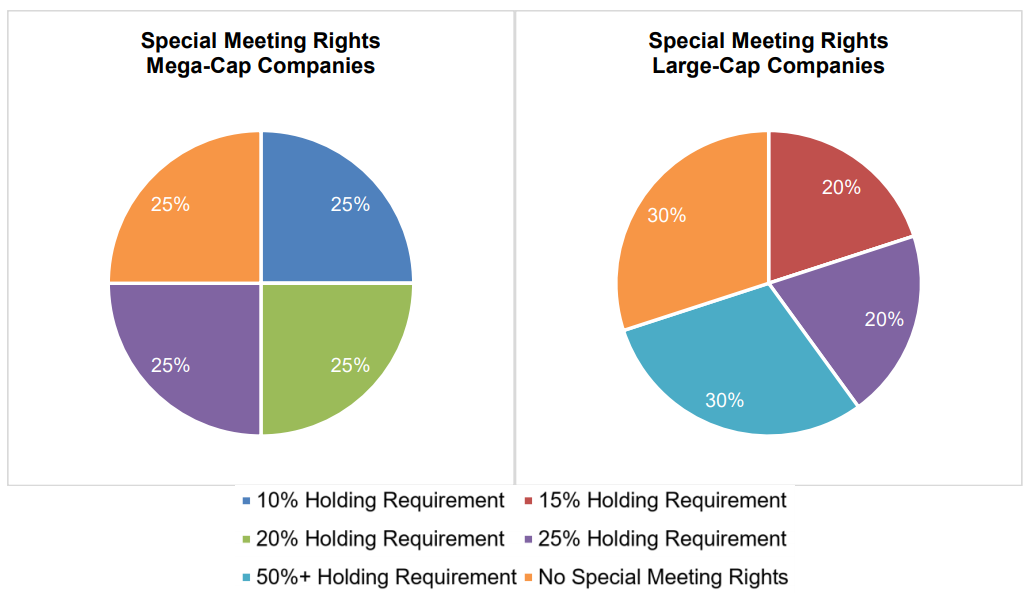

The majority of consumer companies allow shareholders owning a specified percentage of shares to call special meetings. As compared to large-cap consumer companies, mega-cap consumer companies are slightly more likely to grant special meeting rights to their shareholders. Additionally, mega-cap consumer companies often have adopted lower ownership thresholds as a prerequisite to calling the special meeting. While all mega-cap consumer companies that grant special meeting rights set the threshold at or below 25%, a large proportion of large-cap consumer companies require as many as 50.01% of the shares to call a special meeting.

However, the percentage of shares required to call special meetings is evolving. Shareholders of one large-cap consumer company just approved at its 2021 annual meeting a proposal to reduce the special meeting threshold from 25% to 15%. [12] Similarly, shareholders of one mega-cap consumer company also recently voted to reduce the threshold from 25% to 10%. [13]

B. Written Consent Rights

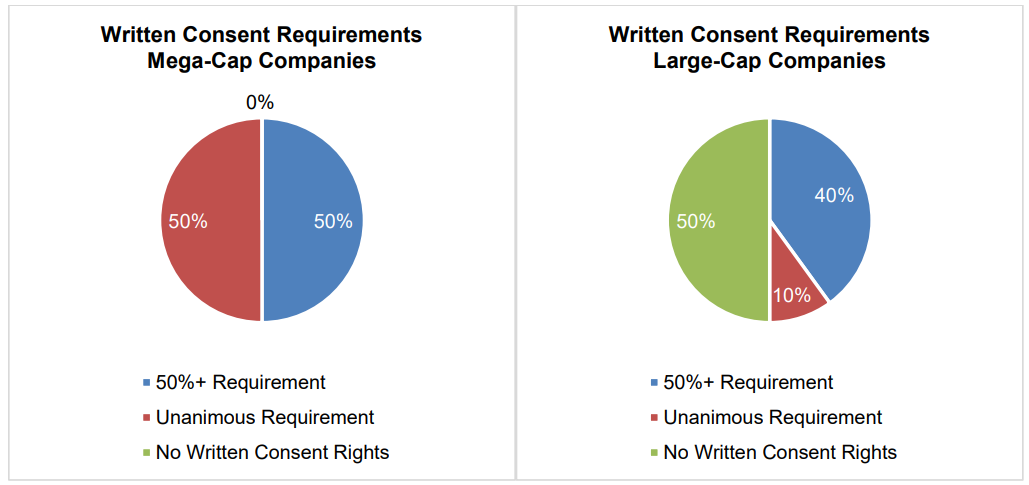

Some consumer companies have granted shareholders the right to act by written consent in lieu of a meeting. Although all mega-cap consumer companies have granted shareholders the right to act by written consent, 50% of them only allow actions to be taken with unanimous shareholder consent, making it impracticable for shareholders to exercise the right. Similarly, a majority of large-cap consumer companies either require unanimous consent or do not grant the right to shareholders at all.

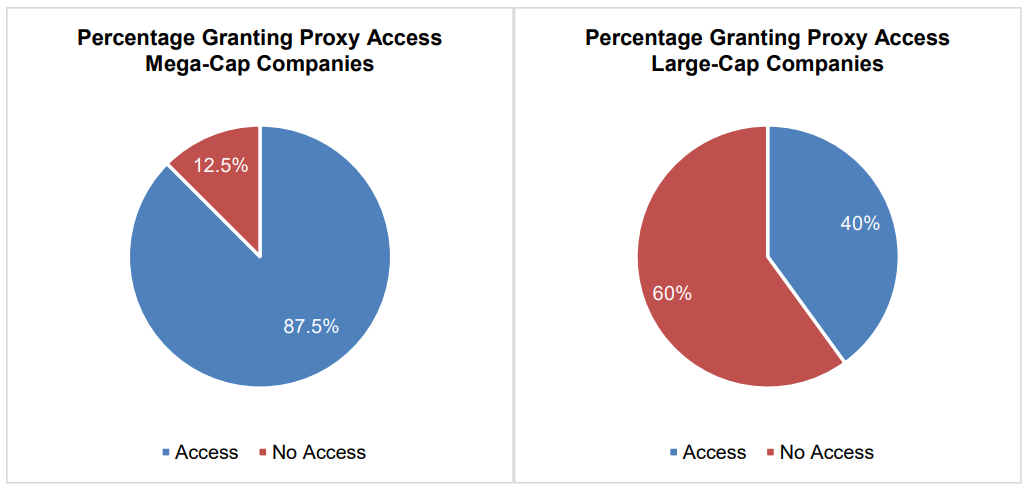

C. Proxy Access

Proxy access provides shareholders with the ability to place alternative director candidates on a company’s proxy card for its annual shareholder meeting. As of 2020, approximately 76% of S&P 500 companies have granted proxy access rights to shareholders. [14] Exceeding this overall average, nearly all mega-cap consumer companies in our sample have granted proxy access rights to shareholders as compared to only 40% of large-cap consumer companies.

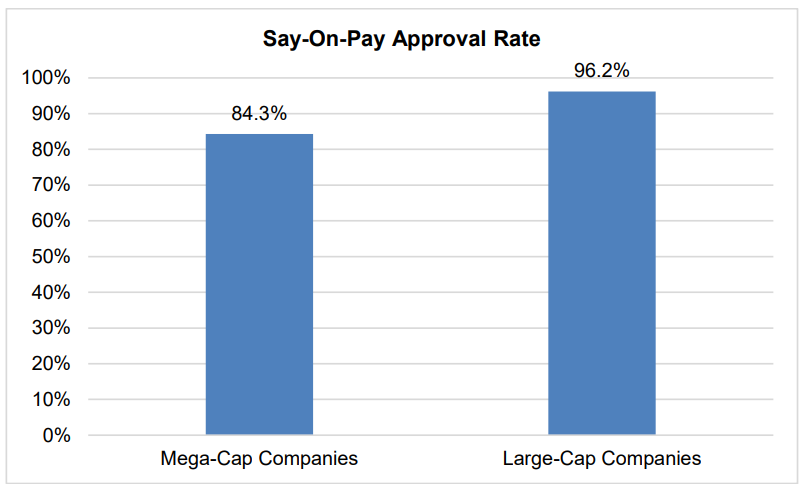

D. Say-On-Pay Approval

Pursuant to the Dodd-Frank Act, all public companies are required to conduct a non-binding, advisory shareholder vote on the compensation packages of executive officers. In 2020, shareholders of S&P 500 companies approved executive compensation packages at an average rate of 90%. [15] Large-cap consumer companies exceeded this overall average with an average approval rate of 96.2%, [16] but mega-cap consumer companies on average were below the S&P 500 company average. Notably, the say-on-pay proposals at two mega-cap consumer companies only received around 50% support from their shareholders, significantly dragging the group average down. In comparison, approximately 93% of public companies in 2021 had say-on-pay approval rates of at least 70%. [17] In response to the low approval rates, one of the mega-cap companies conducted follow-up shareholder outreach, consulted with external compensation advisors, and reviewed its plans in the context of market trends. [18]

E. Shareholder proposals

Mega-cap companies are more likely than large-cap companies to have shareholder proposals in their proxy statements for voter consideration at their annual meetings. In their most recent proxy statements, 87.5% of mega-cap companies noted at least one potential shareholder proposal for voter consideration, compared to only 30% of large-cap companies.

V. Trends in Shareholder Composition

One notable feature of the consumer industry is that founders’ family members maintain significant control over many of these companies, either directly or indirectly through foundations or trusts. This phenomenon is more pronounced among large-cap consumer companies, about half of which have family members either owning a majority or near majority of voting shares or exercising control over corporate decisions through dual-class structures. In contrast, with two exceptions, the ownership of mega-cap consumer companies is more dispersed, with their largest shareholders being typically institutional investors each owning less than 10% of their shares. As one would expect, family-controlled consumer companies generally grant fewer rights, such as special meeting rights, proxy access rights, and written consent rights, to the public shareholders.

VI. Trends in Corporate Disclosures

A. Corporate Responsibility Reports

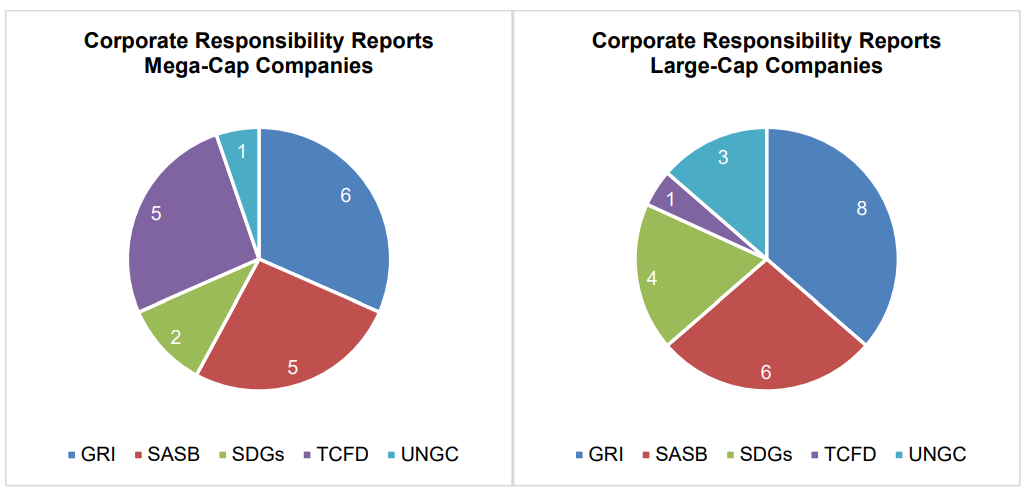

Among all the consumer companies we examined, all but two large-cap consumer companies publish corporate social responsibility (CSR) or similar reports, although some large-cap companies do not appear to update their CSR reports annually.

Among consumer companies, the two most popular disclosure frameworks that inform their CSR reports appear to be Global Reporting Initiative (GRI) and Sustainability Accounting Standards Board (SASB) metrics. Task Force on Climate-related Financial Disclosures (TCFD) standards are also widely used among mega-cap consumer companies, although not as prevalent among large-cap consumer companies. [19] In addition, while nearly all consumer companies voluntarily align their disclosures to existing third-party standards, one mega-cap consumer company instead uses its own “sustainability matrix” based on a mix of GRI, SASB, SDGs, and TCFD metrics. [20]

B. Pay Equity Statistics

Consumer companies often state on websites or in their proxy statements that they are committed to promoting workplace equality at their companies. Many of these companies also report that they conduct third-party annual reviews of their racial and gender pay equity performance and find no statistically significant inequality. Some mega-cap consumer companies provide more information by disclosing the average gender and racial/ethnic pay ratio, but very few large-cap consumer companies have done so.

Conclusion

As illustrated above, mega-cap and large-cap consumer companies have adopted slightly different approaches to various areas of corporate governance. Going forward, individual consumer companies should continue to review their governance approaches against industry trends and adopt the structure that aligns best with their particular characteristics.

Annex A: Consumer Companies Reviewed

| Mega-Cap Consumer Companies | Large-Cap Consumer Companies |

|---|---|

|

|

Endnotes

1To evaluate current governance trends in the consumer industry, we reviewed the recent proxy statements, annual reports, and website disclosures of a representative sample of eight mega-cap consumer companies and ten large-cap consumer companies. A list of the specific companies reviewed is provided in Annex A to this post. Thank you to Victoria Wang and Angela Wu for their research contributions to this publication.(go back)

2Spencer Stuart, 2020 U.S. Spencer Stuart Board Index (2020), https://www.spencerstuart.com/research-and-insight/us-board-index.(go back)

3Id.(go back)

4Id.(go back)

5Where a company did not explicitly disclose the demographic characteristics of directors in relation to gender, race/ethnicity, sexual orientation, etc. in its official publications, we did not make assumptions or inferences on the basis of individual director photos, biographies or other publicly available information.(go back)

6Jeff Green, Women Gained 22 Seats on S&P 500 Boards in January Surge, Bloomberg (Feb. 23, 2021), https://www.bloomberg.com/news/articles/2021-02-23/women-gained-22-seats-on-s-p-500-boards-in-january-surge.(go back)

7Nasdaq, NASDAQ’s Board Diversity Rule (Aug. 17, 2021), https://listingcenter.nasdaq.com /assets/Board%20Diversity%20Disclosure%20Five%20Things.pdf.(go back)

8EEO-1 Data Collection, U.S. Equal Employment Opportunity Commission (May 5, 2021), https://www.eeoc.gov/employers/eeo-1-data-collection.(go back)

9Sullivan & Cromwell LLP, 2021 Proxy Season Review: Part 1—Rule 14a-8 Shareholder Proposals (July 27, 2021), https://www.sullcrom.com/files/upload/sc-publication-2021-Proxy-Season-Review-Part-1-Rule14a-8.pdf.(go back)

10Id. (go back)

11Diversity Strategy, Goals & Disclosure: Our Expectations for Public Companies, State Street Global Advisors (Aug. 27, 2020), https://www.ssga.com/us/en/individual/etfs/insights/ diversity-strategy-goals-disclosure-our-expectations-for-public-companies; NY State Comptroller DiNapoli Calls on Corporate America to Address Lack of Diversity, Equity & Inclusion, Office of the New York State Comptroller (Feb. 25, 2021), https://www.osc.state.ny.us/press/releases/2021/ 02/ny-state-comptroller-dinapoli-calls-corporate-america-address-lack-diversity-equity-inclusion.(go back)

12See Kimberly-Clark Corp., Form 8-K (Apr. 29, 2021).(go back)

13See Colgate-Palmolive Comp., Form 8-K (May 13, 2021); Colgate-Palmolive Comp., 2021 Proxy Statement: Notice of Annual Meeting of Stockholders (Mar. 24, 2021).(go back)

14Holly J. Gregory et al., Proxy Access: A Five-Year Review, Harvard Law School Forum on Corporate Governance (Feb. 4, 2020), https://corpgov.law.harvard.edu/2020/02/04/proxy-access-a-five-year-review.(go back)

15Semler Brossy, 2021 Say on Pay & Proxy Result (Apr. 15, 2021), https://www.semlerbrossy.com/wp-content/uploads/SBCG_SOP-Report_2021-04-15.pdf.(go back)

16Shareholders of one large-cap consumer company (Peloton Interactive) approved a proposal to reduce the say-on-pay vote frequency to every three years, and it did not conduct a say-on-pay vote in 2020.(go back)

17Sullivan & Cromwell LLP, 2021 Proxy Season Review: Part 2—Say-on-Pay Votes and Equity Compensation (Aug. 23, 2021), https://www.sullcrom.com/files/upload/SC-Publication-2021-Proxy-Season-Review-Part-2-Say-on-Pay-Votes-Equity-Compensation.pdf.(go back)

18See Altria Group Inc., 2021 Notice of Annual Meeting of Shareholders and Proxy Statement (Apr. 08, 2021).(go back)

19Other frameworks used include the United Nations Sustainable Development Goals (SDGs) and the United Nations Global Compact (UNGC).(go back)

20Colgate-Palmolive Comp., 2021 Proxy Statement: Notice of Annual Meeting of Stockholders (Mar. 24, 2021).(go back)