Print

PrintMatt Filosa is Senior Managing Director, Faten Alqaseer is Managing Director & Co-Head of Diversity, Equity & Inclusion, and Morgan McGovern is Vice President at Teneo. This post is based on a Teneo memorandum by Mr. Filosa, Ms. Alqaseer, Ms. McGovern, Martha Carter, and Jeff Sindone. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) and Will Corporations Deliver Value to All Stakeholders?, both by Lucian A. Bebchuk and Roberto Tallarita; For Whom Corporate Leaders Bargain by Lucian A. Bebchuk, Kobi Kastiel, and Roberto Tallarita (discussed on the Forum here); and Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy—A Reply to Professor Rock by Leo E. Strine, Jr. (discussed on the Forum here).

Executive Summary

The significant events of 2020 have caused companies, institutional investors and regulators to re-energize their efforts towards sustainability initiatives. Institutional investors have dramatically enhanced their focus on issues relating to climate, diversity, human capital management and board governance (collectively, “ESG”).

Under the Biden Administration, U.S. regulators are on the verge of mandating greater transparency from all companies on their sustainability initiatives. While many companies have a long history of focusing on sustainability issues, communicating those initiatives to stakeholders is a relatively new endeavor. And stakeholders are evolving their demands for company sustainability disclosure faster than ever before, especially on critical issues like climate change and diversity. There has never been a more important time to ensure that company sustainability disclosure is robust, clear and credible—while also keeping pace with the rapidly evolving demands of stakeholders.

Yet, unlike proxy statements and other company documents, there is no clear disclosure framework for company sustainability reports. And despite ongoing initiatives from the U.S. Securities & Exchange Commission and the International Financial Reporting Standards Foundation, a uniform global sustainability reporting framework seems unlikely to emerge in the near-term. So how are companies evolving their sustainability reporting to meet the increased demands from stakeholders? What should the title be? And how many pages should it include? In short, what does a “good” sustainability report look like?

To help companies answer these and other important questions about future sustainability reports, we analyzed 200 sustainability reports from S&P 500 companies published between January 1, 2021—June 30, 2021 (“Sustainability Reports”).

In this post, we have included market statistics for many common formatting and content elements of 2021 Sustainability Reports, as well as examples that we believe are particularly well communicated. In addition, we have included the following callouts:

- Ten Practical Considerations for 2022 Sustainability Reporting;

- Unique Naming Conventions of 2021 Sustainability Reports;

- Essential Design Considerations for 2022 Sustainability Reports; and

- Key Statistics of 2021 Sustainability Reports (Appendix to the complete publication, available here.)

We hope that this post is a helpful, practical tool to aid all U.S. companies in their 2022 Sustainability Report strategies.

Ten Practical Considerations for 2022 U.S. Sustainability Reporting

- There is No “I” in ESG: No one person can be an expert in “E,” “S” and “G.” Assembling a

cross-functional team that includes representation from key business units can help ensure all stakeholder views on ESG issues are being represented. Disclosing this collaborative approach can also signal that your company’s sustainability strategy is not being managed in isolation. - Keep Your Eyes on Other People’s Paper: While every company’s sustainability story is unique, benchmarking recent sustainability reports from peer companies, as well as those companies generally considered “best-in-class” can help gauge your company’s ESG disclosure progress and inform future sustainability reports.

- Understand Your ESG Report Card: We understand they can be confusing. But reviewing your company’s primary ESG ratings reports for any alleged deficiencies can help inform your sustainability strategy and potentially enhance your company’s ESG rating. Remember that you can download a copy of your MSCI and Sustainalytics ESG rating reports via their online portals free of charge at any time, as well as submit feedback.

- It’s a Matter of Trust: Sustainability disclosure is now included in a variety of company documents, including sustainability reports, proxy statements and 10-Ks. Consistent narratives and a commitment to transparency within these and other corporate communications can help a company further build trust with its stakeholders.

- Ask and You Shall Receive Feedback: Routine engagement with shareholders, employees and other stakeholders is a great opportunity to solicit feedback on your sustainability report. Include specific questions in your employee surveys and/or shareholder engagement materials, track any feedback and report it to your internal ESG team.

- Aim to Make it Easy for Investors: Many investors have expressed frustration over not being able to easily locate a company’s sustainability data. Incorporating a downloadable ESG table that includes all relevant ESG data and multi-year trends to show progress can alleviate this frustration and build goodwill with investors.

- Don’t Let Perfection Be the Enemy of the Good: Begin reporting to the Task Force on Climate-related Financial Disclosures (TCFD) and Sustainability Accounting Standards Board (SASB) disclosure frameworks even if you are not ready to disclose all elements of those frameworks. Investors and other stakeholders are likely to give companies latitude if they are making continued and meaningful progress on their sustainability disclosures.

- Investors May Trust, but Will Want to Verify: Investors and other stakeholders are increasingly focused on the reliability of sustainability disclosures. Internal and external audits can help ensure the integrity of sustainability reports to the highest assurance level possible.

- Allocate Appropriate Time for ESG Education: The world of ESG ratings, rankings, indexes and frameworks is complex and evolving rapidly. These terms can also be counterintuitive. Understanding the nuances of these similar yet distinct initiatives helps set clear priorities and allocate company resources appropriately.

- Remember That You Can’t Be Everything to Everyone: No company can tackle every ESG issue. Including a “materiality matrix” in sustainability reports is an effective way to signal to stakeholders which ESG issues are a priority for the business (and which issues are not). If using the term “material” causes legal concerns, then substituting the term “priority” or something similar may help.

Research Background

We analyzed 200 sustainability reports of S&P 500 companies published between January 1, 2021—July 31, 2021 (“Sustainability Reports”). For the purposes of this post, all references to “Sustainability Reports” include any annual company disclosure relating to ESG issues—regardless of the report’s actual naming convention.

As to be expected from a review of S&P 500 companies, a large majority of sustainability reports included in this post were published by large-cap companies.

2021 Sustainability Reports: Format

The naming conventions of 2021 Sustainability Reports are quite varied. In fact, we found 18 distinct ways in which companies titled their reports. “Sustainability” was the most commonly used term in report titles (43%), while “CSR” and “ESG” appeared in the report title 24% and 23% of the time, respectively. Regardless of what your company’s sustainability report is titled, companies should be consistent with how they refer to their sustainability initiatives in all of their company communications—including press releases, proxy statements and investor presentations.

Unique Naming Conventions of 2021 Sustainability Reports

- “Business & Sustainability Report”

- “Citizenship and Sustainability Report”

- “Corporate Citizenship Report”

- “Corporate Responsibility Report”

- “Corporate Social Responsibility Report”

- “Environmental, Social and Governance (or ESG) Report”

- “Global Citizenship Annual Report”

- “Global Citizenship & Sustainability Report”

- “Global Environmental & Social Impact Report”

- “Global Impact Report”

- “Global Responsibility Report”

- “Impact Report”

- “Integrated Sustainability Report and Annual Report”

- “Responsible Business Report”

- “Social Impact and Sustainability Report”

- “Stakeholder Sustainability Report”

- “Sustainability Report”

- “Sustainable Impact Report”

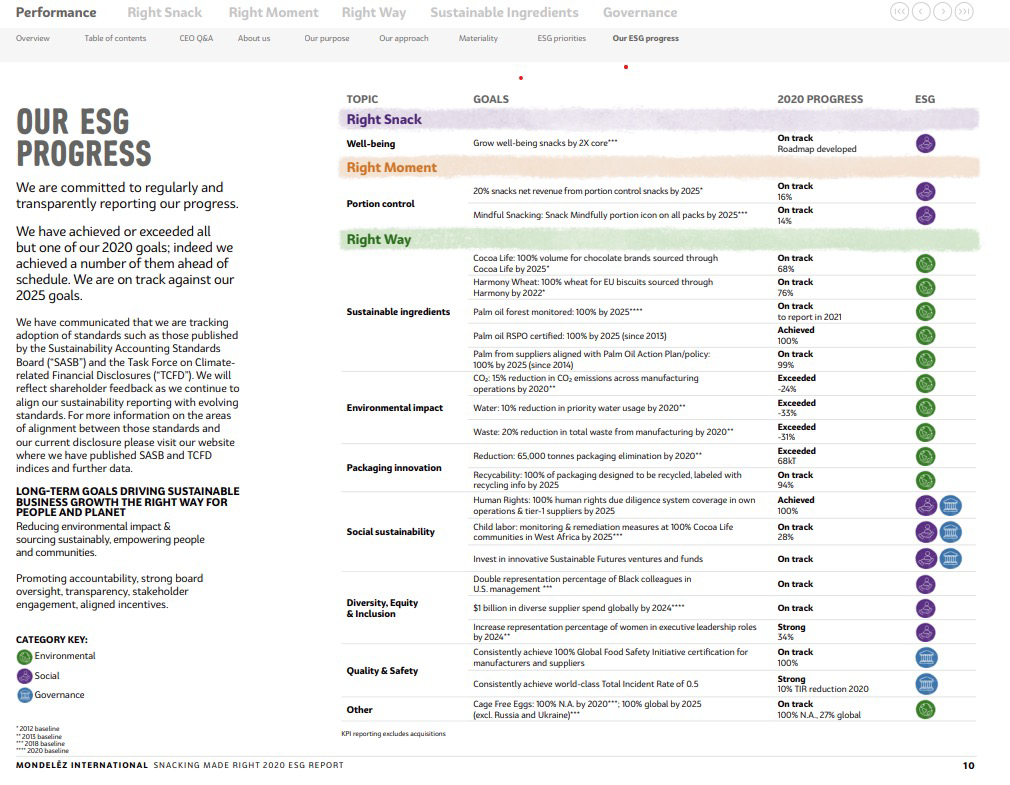

The average length of a 2021 Sustainability Report was 70 pages, ranging from a low of 12 pages to a high of 243 pages. 26% of the 2021 Sustainability Reports that we reviewed also published a summary or “highlights” version of its sustainability report (see Figure 1 for an example). While there is no “right” length of a sustainability report, producing a summary or “highlights” version can provide stakeholders with an efficient means to assess a company’s sustainability initiatives. This can be especially helpful when updating stakeholders on a company’s progress towards sustainability goals.

Figure 1: Mondelez International 2020 ESG Progress Report

95% of 2021 Sustainability Reports were available to be downloaded in PDF format, while less than 5% were only available on the company’s dedicated sustainability microsite. Sustainability reports offered in web-only format generally do not provide stakeholders the ability to search for content with the same degree of ease as a downloadable Adobe® PDF.

76% of 2021 Sustainability Reports were accompanied by a press release. The press releases typically included a quote from the CEO and/or sustainability lead as well as highlights from the sustainability report. Companies can utilize the sustainability report’s press release to also announce either the setting or achievement of sustainability goals, such as those relating to climate or diversity.

June was the most popular month for the release of sustainability reports (32%), followed by April (27%) and May (22%). While it may be a challenge, some companies are beginning to implement strategies to better align the release of sustainability reports with the filing of proxy statements and annual reports.

For example, Prudential Financial released an ESG Summary Report in March alongside its annual report and proxy statement in order to provide investors with updated ESG information ahead of the company’s annual shareholder meeting. Other companies are thinking about creative ways to deliver updates to sustainability initiatives beyond the annual cycle of sustainability reports, such as interim sustainability updates or issue-specific reports (e.g.; diversity).

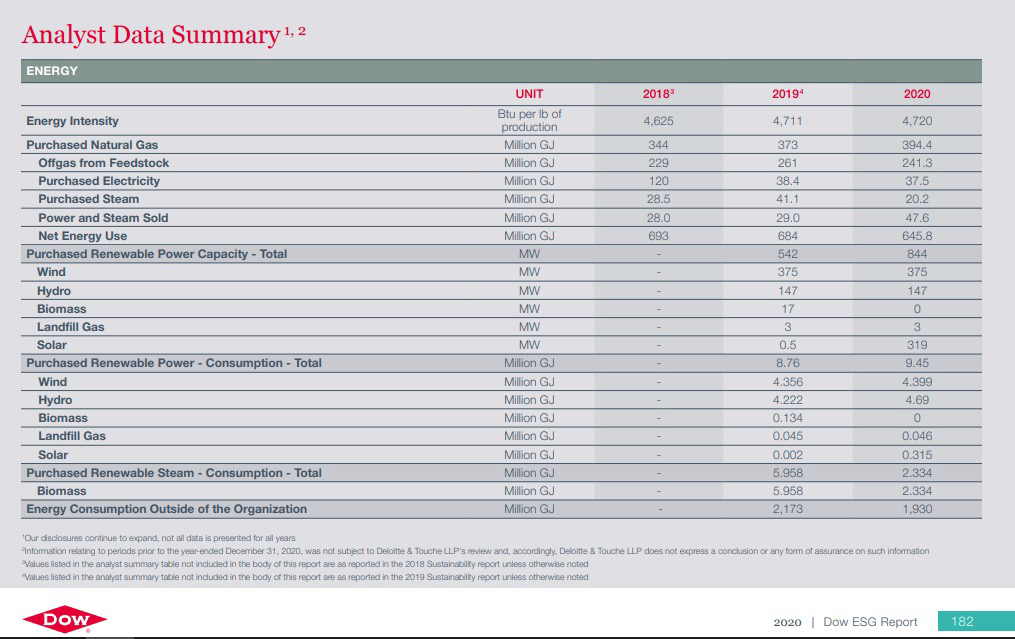

Just over 75% of 2021 Sustainability Reports included some form of sustainability data table (see Figure 2 for an example). Sustainability data tables can help investors easily find the information most important to them. In addition, consider providing downloadable sustainability data tables to make it even easier for investors to utilize the data.

Figure 2: 2020 Dow ESG Report

2021 Sustainability Reports: Content

Over 96% of 2021 Sustainability Reports included a letter from the CEO. CEO letters provide companies with the opportunity to appropriately signal to stakeholders that ESG is a priority for senior leadership. In a few instances, the CEO letter was penned together with the company’s head of sustainability. A newly appointed CEO can utilize the CEO letter to communicate his or her refreshed vision for the company and its sustainability strategy.

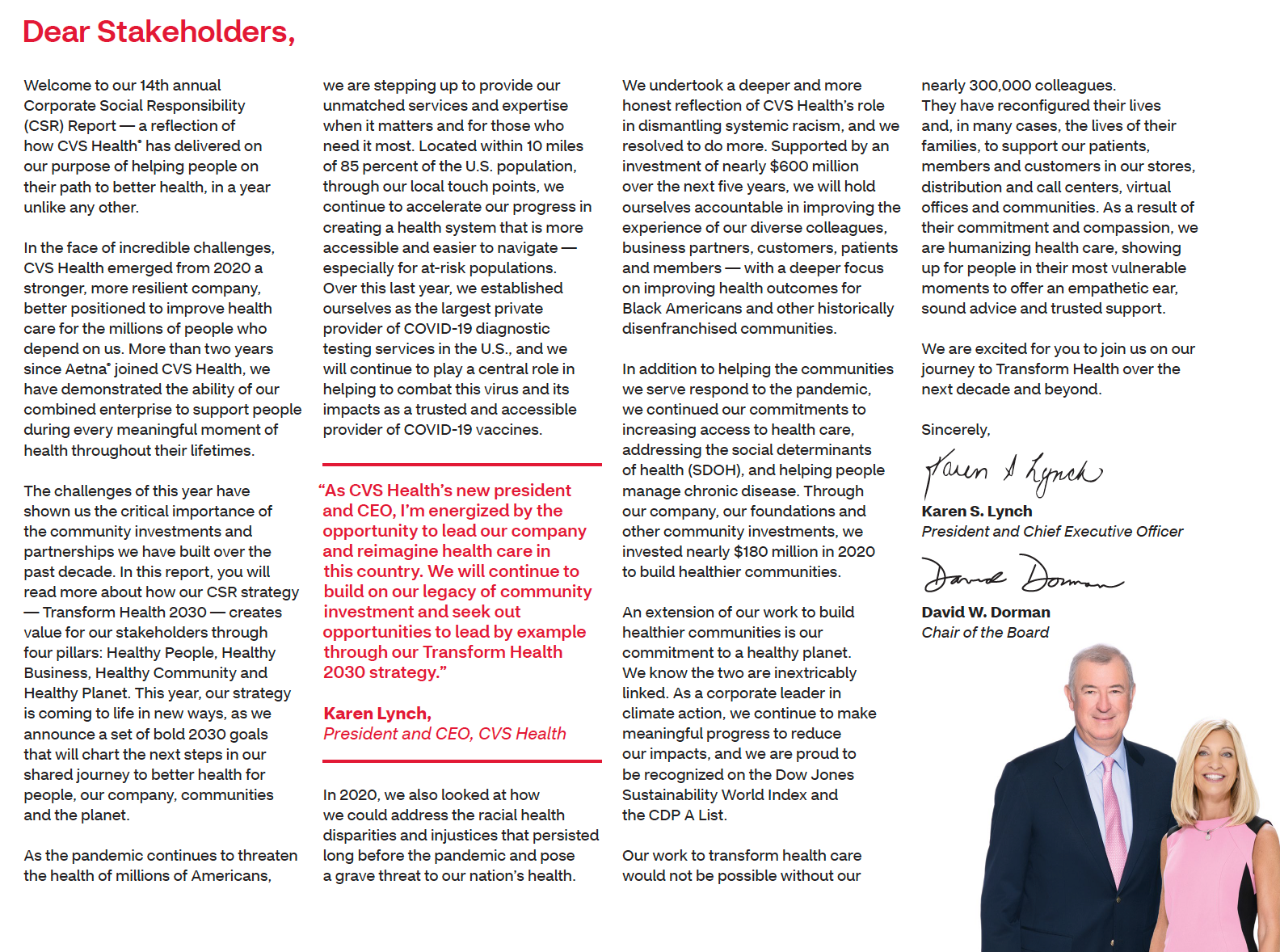

Figure 3: CVS Health 2020 Corporate Social Responsibility Report

Less than 15% of companies included either a combined letter from the CEO/board or a separate letter from the board (see Figure 3 for an example). A few companies such as Walgreen’s Boots Alliance also included a Q&A with a board member. Including messaging from the board of directors can help signal to stakeholders that directors are engaged and actively working with management to oversee the company’s sustainability strategy.

Stakeholders increasingly want to know how the company’s sustainability strategy is managed internally. A majority of companies included a description of internal oversight in 2021 Sustainability Reports, typically in the form of cross-functional sustainability or ESG committees led by senior executives. Internal sustainability committees typically include representatives from key business units, such as investor relations, legal, corporate communications, human resources and risk, and regularly report to senior management and/or the board of directors.

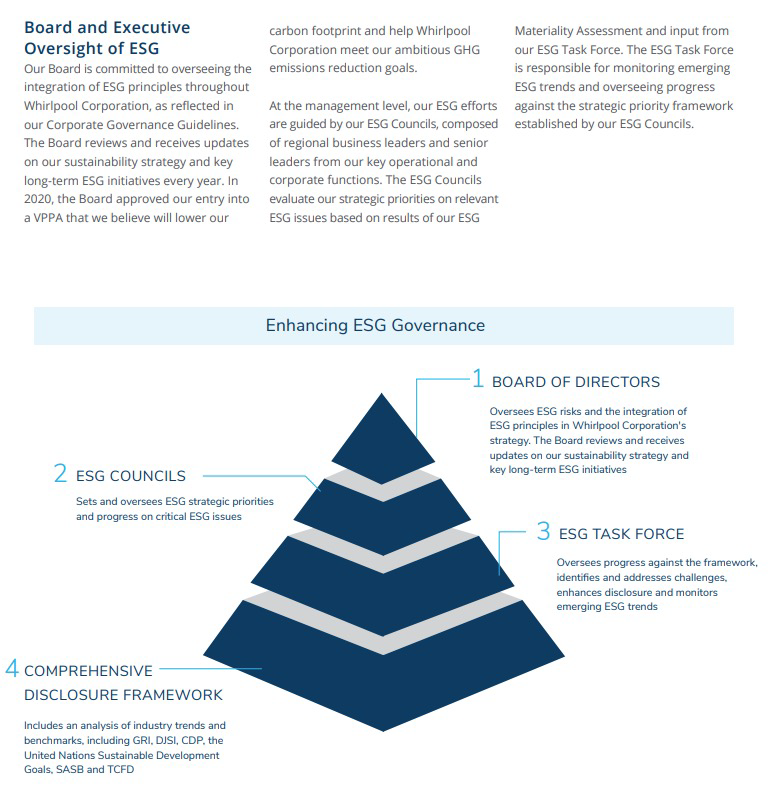

Similarly, a majority of companies included a description of how the board of directors oversees the risks associated with sustainability issues (see Figure 4). Some boards utilize their committee structure to oversee sustainability risks, while others utilize the full board of directors. Regardless of how a board oversees a company’s sustainability risks, it is imperative to describe the formal mechanisms the board utilizes in order to provide investors and other stakeholders with the appropriate level of transparency.

“Boards have become increasingly engaged on companies’ ESG initiatives in recent years, particularly in regard to climate and human capital management,” said Patricia F. Russo, Senior Advisor to Teneo, Chair of Hewlett Packard Enterprise and board member of General Motors, Merck and KKR Advisors. “But this can’t really be done on an ad hoc basis. Establishing formal oversight mechanisms is critical for the board and its committees to effectively oversee ESG initiatives and ensure they are appropriately integrated into the company’s overall strategy.”

Figure 4: Whirlpool Corporation 2020 Sustainability Report

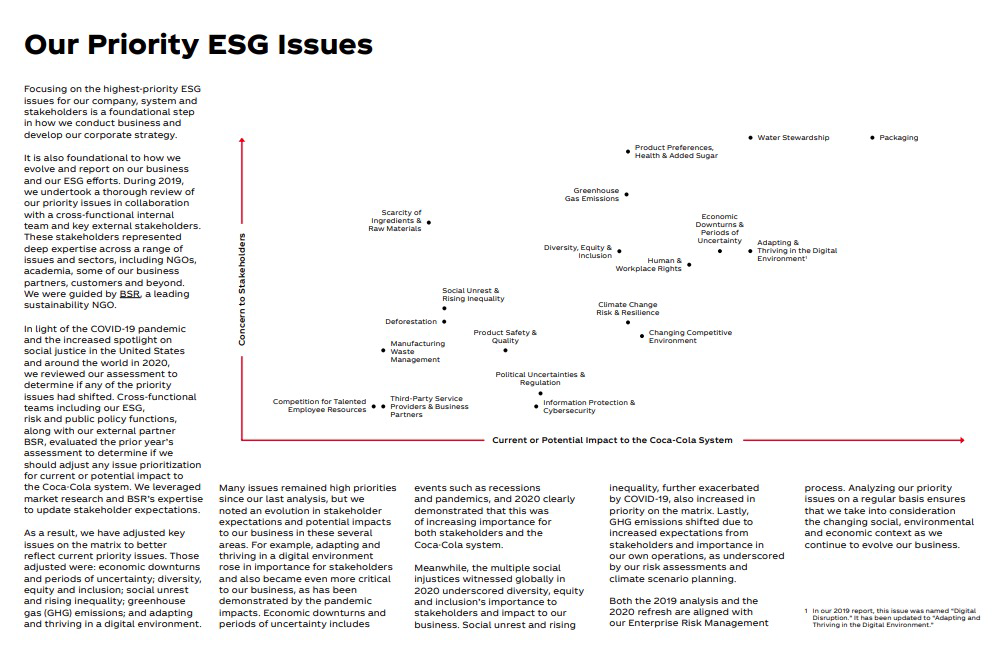

A majority of companies utilized a “materiality matrix” to highlight which sustainability issues are most important to their business, as well as their stakeholders (see Figure 5). These materiality matrixes can be a very useful tool for stakeholders to gain insight into how the company determines its sustainability strategy. There is also a growing interest in “dynamic materiality”—a belief whereby a company’s most important sustainability issues may change over time. Stakeholder engagement, another common component of sustainability reports, is the primary mechanism to ensure that the company is focusing on the most important sustainability issues. While the term “materiality” can be a concern for many companies given its legal connotations, it is critical to describe to stakeholders which sustainability issues are most important to your company.

Figure 5: Coca-Cola Company 2020 Business & ESG Report

The “S” of ESG covers a comprehensive set of important issues, from labor and human rights (employee safety training and child labor policies) to product-related issues (fair-trade policy and obesity risk) and community impact (philanthropic giving). For this post, we primarily focused on diversity, equity and inclusion (“DEI”) as it is one of the most detailed and evolving disclosure topics within sustainability reporting.

93% of 2021 Sustainability Reports disclosed employee demographic data, with the vast majority including employee data on both gender and racial/ethnic representation. 64% of reports disaggregated the data into individual racial/ethnic groups, while the remaining 23% reported on racial/ethnic minorities in aggregate. It is clear that disclosing employee demographic data, particularly female and racial/ethnic minority representation, is no longer viewed as optional.

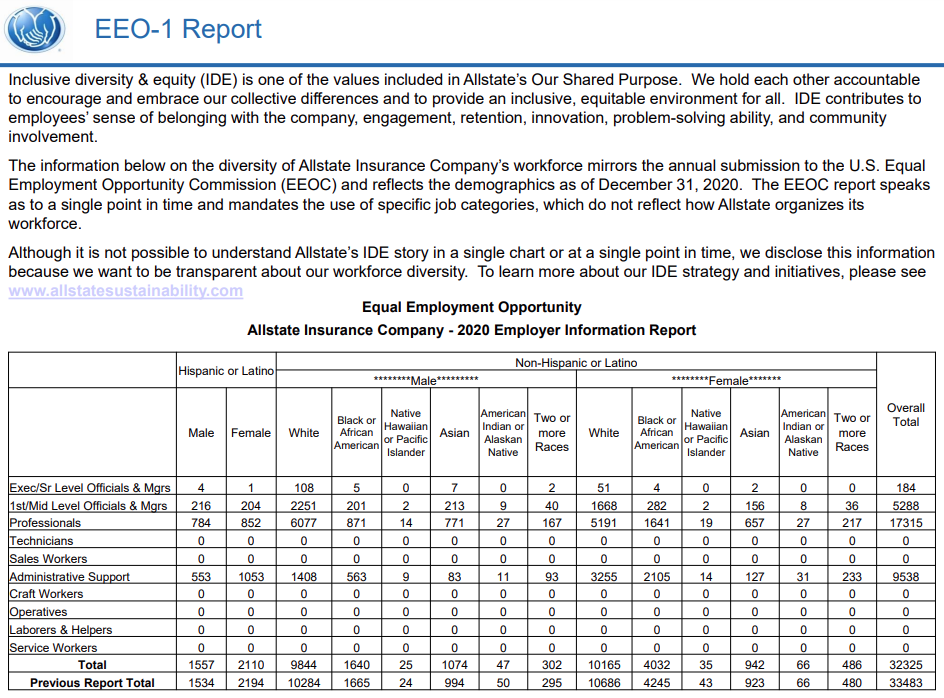

But while companies now provide greater diversity disclosure, there is a lack of uniformity in how the data is presented. For example, classifications of job functions, executives and even ethnicities can vary greatly, making it challenging for stakeholders to track and compare data across companies. As a result, many institutional investors and other stakeholders have called for U.S. public companies to disclose their complete EEO-1 Report as filed with the Equal Employment Opportunity Commission.

The EEO-1 Report offers greater uniformity with regard to a company’s demographic data, including gender (2 defined categories), race/ethnicity (8 defined categories) and job function (10 defined categories). As a result of pressure from investors, 33% of companies disclosed their unabridged EEO-1 Report in 2021, [1] and we expect that number to continue to grow as more large investors state that they will vote against board members if the company does not disclose its EE0-1 Report (see Figure 6). Companies that are concerned that their EEO-1 Report does not accurately reflect the level of diversity within the organization can supplement the EEO-1 Report disclosure with additional narrative and data using company-specific job categories. They can also enhance disclosure by reporting recruiting, promotion and retention rates of diverse employees.

Figure 6: Allstate Insurance Company EEO-1 Report

Over one-third of 2021 Sustainability Reports included at least some information on employee pay gaps. 30% reported both the gender pay gap for employees globally and the ethnic/racial pay gap in the U.S. [2] Only 8% of companies reported their global gender pay gap. Showing progress against pay inequity can help signal the company’s overall commitment to DEI. A small but growing number of companies disclose both the adjusted and median pay gap, [3] starting with Citibank in 2019. These two data points can offer a more complete assessment of pay disparities among roles with “equal work” and across the company.

In addition to the disclosure of diversity data, companies are also setting measurable and timebound DEI targets. Over half of 2021 Sustainability Reports included at least one demographic target, with 42% of companies including both gender and racial/ethnicity goals. The scope of these goals varies, covering the employee population as a whole or focusing on subsets like diversity within senior ranks or client-facing roles.

In addition to diversity data and targets, sustainability reports can illustrate a holistic approach by outlining action to drive equity and inclusion within the company, its community and supply chain.

Figure 7: Delta Air Lines 2020 Corporate Responsibility Report

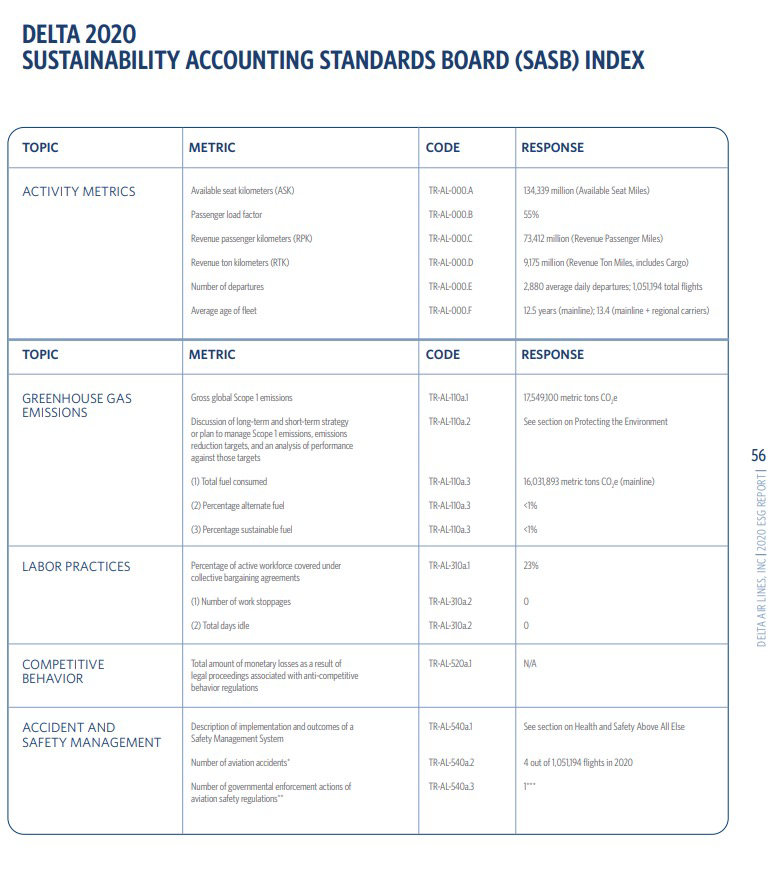

The use of third-party ESG disclosure frameworks increased dramatically this year as a vast majority of companies referenced the SASB and TCFD. This is a result of many large institutional shareholders essentially mandating that companies report to these disclosure frameworks (see Figure 7) or risk losing their support for certain incumbent directors at the next annual shareholder meeting.

Not all SASB or TCFD disclosures looked the same, as some companies did not disclose every component within the TCFD and SASB frameworks. And while cross-referencing SASB and TCFD indexes in other company disclosures is common, investors and other stakeholders may prefer to have the substance of TCFD and SASB disclosures included directly in the indexes. At the very least, companies that produce TCFD and/or SASB indexes outside the sustainability report run the risk of investors not being able to find such indexes and concluding that the company is not disclosing the information. Regardless, all companies that have not yet disclosed to the TCFD and/or SASB disclosure framework should begin to do so next year.

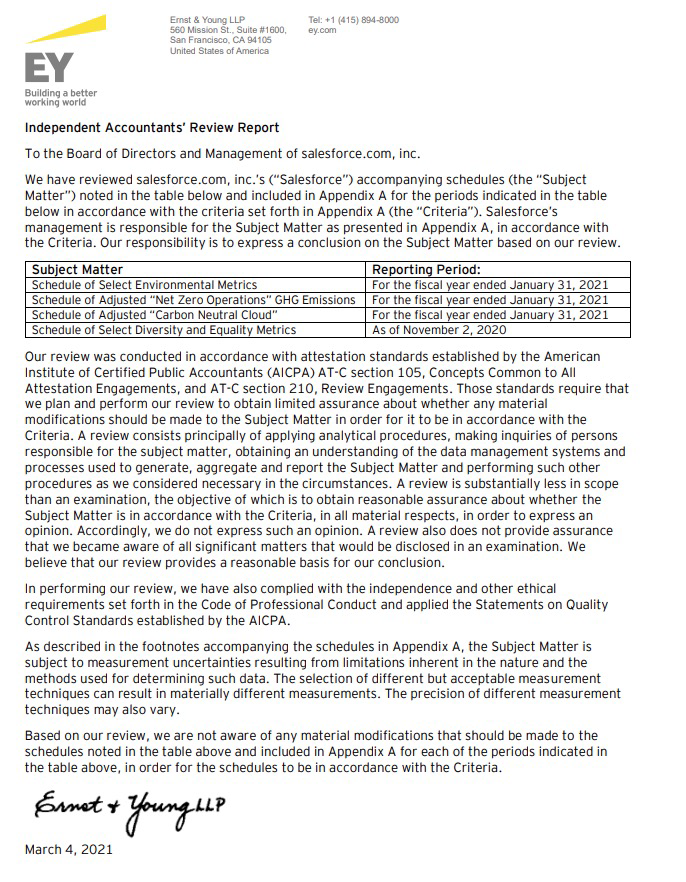

External assurance of sustainability reports is going to be one of the most important sustainability reporting developments in the coming years. In our review, 53% of 2021 Sustainability Reports included at least some degree of external assurance (see Figure 8 for an example). But just as with sustainability reports themselves, there is not yet a universally agreed framework or methodology for the external assurance of sustainability information. This is likely to change given the rapidly increasing interest from investors and other stakeholders on the reliability of sustainability information.

“Investors, regulators and raters want assurance that sustainability disclosures are made with the proper processes and controls in place and that the information provided is accurate and reliable,” said Mark A. Weinberger, Senior Advisor to Teneo and former Global Chairman and CEO of EY. “As a result, assurance standards are likely to evolve to a more rigorous examination of the information and assertion that it is free of material misstatement.” And with so many boards and executives elevating sustainability on their agenda, external assurance of sustainability information is quickly becoming an important component of a company’s sustainability reporting journey.

Figure 8: Salesforce FY21 Stakeholder Impact Report

The Future of U.S. Sustainability Reporting

While we have hopefully established some clear and informative trends and considerations from 2021 Sustainability Reports, many important questions still remain unanswered. How should “material” issues be defined—how sustainability issues impact the company or how the company impacts society? Is reasonable external assurance of sustainability reports achievable in the short-term? Will a standardized global sustainability reporting framework eventually emerge, and will it be successful? How will pending disclosure regulations in the U.S. and Europe impact a company’s sustainability reporting moving forward? And many more.

But we believe a few things are certain. Global regulators will continue to push for mandatory sustainability disclosure from companies and shareholders. Institutional investors will continue to advocate for more robust sustainability disclosure beyond any regulatory requirements, including clear narratives and explanations around any required ESG data. The sustainability ecosystem of ESG ratings, rankings, indexes and disclosure frameworks will continue to expand given the intense demand for sustainability risk analysis on a company-by-company basis. So in our view, it is critical that companies ensure that they are providing stakeholders with robust, clear and credible sustainability disclosure that aligns with the company’s overall strategy. And such disclosure should be consistent among the various corporate communications documents, including the company’s proxy statement, annual report and website. We hope this post is a useful tool to help companies continue to make progress towards that goal.

Essential Design Considerations for 2022 Sustainability Reports

Today’s time-challenged audiences have very little time to read and digest information. A powerful design is required to deliver information in an easily digestible format, tailored to engaging audiences with the content.

- Know Your Stakeholders: One Size Does Not Fit All

- Before heading into design, conduct a stakeholder mapping exercise that helps prioritize your information by audience.

- Develop an annual stakeholder engagement plan to track and gather feedback on your

sustainability initiatives and incorporate the feedback into your design process.

- Reporting Style & Content: Storytelling is Critical

- While every company’s sustainability story is unique, benchmarking recent sustainability

reports from peer companies, as well as those companies generally considered “best-in-class” can help gauge your company’s ESG disclosure progress and inform future

sustainability reports. - Apply an editorial design approach that helps bring company initiatives to life. Consider

adding a theme line on the cover or inside front cover of the report. Having a theme begins the storytelling narrative, captures your readers’ attention and leads them into the report where it acts as a tether to tie the story together visually and contextually. - Internal and external stories bring context to your initiatives and create a humanized view to your reporting. Try to incorporate at least one relevant story for each section of your report.

- Create bespoke visuals (data visualizations, infographics, illustrations, original photography, etc.) to distinguish your report from peer reports. As stock agencies have become all too prevalent, utilizing visuals that do not feel trite or dated is more important than ever. Reports that create custom visuals and use original photography (i.e.; using real employee images for the DEI section) conveys authenticity and transparency.

- Utilize effective wayfinding to help readers navigate and move through the report. Applying proper UX design and hierarchy of content will help your stakeholders find the

information that is most relevant to them.

- While every company’s sustainability story is unique, benchmarking recent sustainability

- Design Format and Style: Digital First

- Apply a digital first design approach that elevates the content across various digital

devices. - Deliver content in a format and through channels that are most relevant to target stakeholders. Think beyond the printed book and provide rich content in multiple formats such as sustainability microsites, films and animations, digital flipbooks and infographics.

- Leverage design to serve multiple purposes, including internal communications, sales/

marketing and employer branding/recruiting activities.

- Apply a digital first design approach that elevates the content across various digital

The complete publication, including footnotes, is available here.

Endnotes

1Includes EEO-1 Reports that were disclosed separate from 2021 Sustainability Reports.(go back)

2Some U.S. companies are subject to UK regulations mandating gender pay gap disclosure. These mandated disclosures are not reflected in the statistics.(go back)

3Median pay gap (also known as the raw or unadjusted pay gap) measures the difference between the median total compensation of two groups, while the adjusted pay gap accounts for factors like job function, level, tenure and geography.(go back)