Print

PrintGeorge Casey, Scott Petepiece, and Lara Aryani are partners at Shearman & Sterling LLP. This post is part of the 19th Annual Corporate Governance Survey publication prepared by Shearman & Sterling LLP, by Mr. Casey, Mr. Petepiece, Ms. Aryani, and Vita Zhu. Related research from the Program on Corporate Governance includes The Long-Term Effects of Hedge Fund Activism by Lucian Bebchuk, Alon Brav, and Wei Jiang (discussed on the Forum here); Dancing with Activists by Lucian Bebchuk, Alon Brav, Wei Jiang, and Thomas Keusch (discussed on the Forum here); and Who Bleeds When the Wolves Bite? A Flesh-and-Blood Perspective on Hedge Fund Activism and Our Strange Corporate Governance System by Leo E. Strine, Jr. (discussed on the Forum here).

After years of growth in shareholder activist activity, the onset of COVID-19 across the world caused a decline in shareholder activism campaigns in the spring and summer of 2020. Economic recovery in the second half of the year coincided with the end-of-year proxy season and gave rise to a renewed appetite for activist campaigns in Q4 that continued through the first half of 2021. While uncertainty remains, particularly on a regional basis due to variations in vaccination rates and the impact of new variants of COVID-19, we expect to see renewed vigor in shareholder activism to continue through the second half of 2021 and into 2022.

Shareholder Activism in 2020

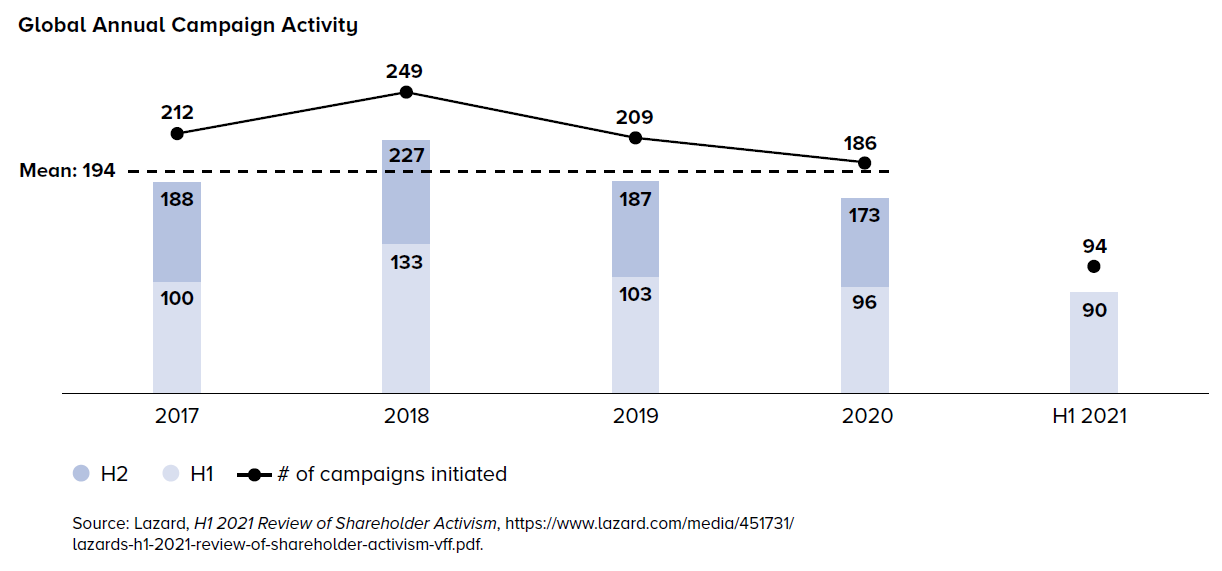

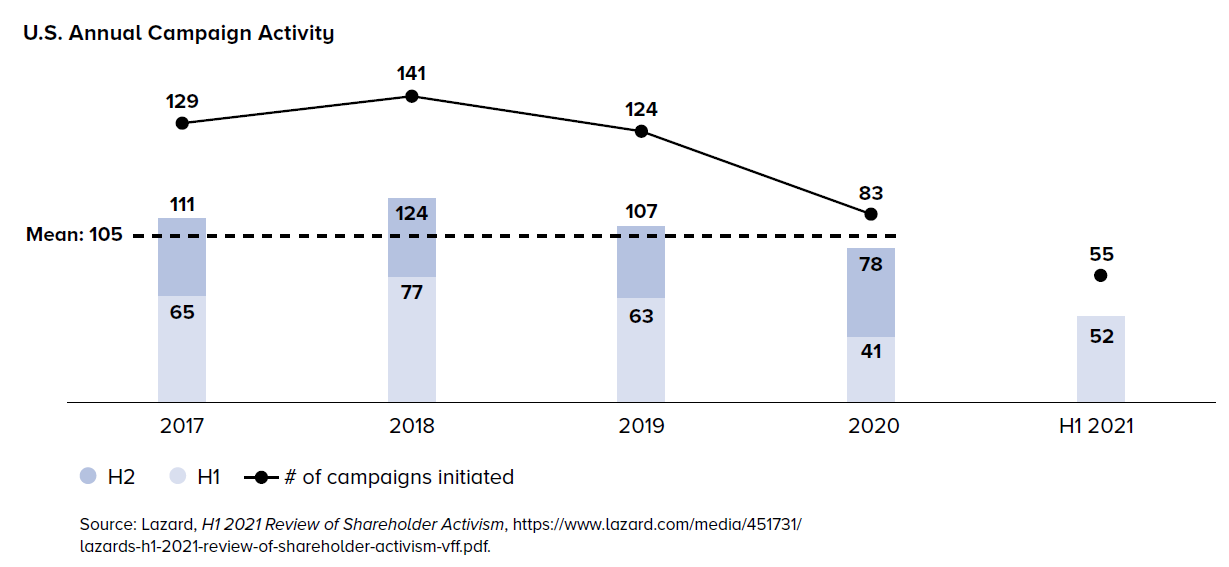

While shareholder activism declined sharply in the spring and summer of 2020, the overall number of campaigns was lower but did not result in a significant year-over-year decline. This was in large part due to the fact that the two annual proxy seasons book-ended the market turbulence of 2020, such that many of the activist campaigns were initiated either before COVID-19 in Q2 or after the economic recovery at the end of the year. The rebound of activism continued through the first half of 2021, with activist campaigns in the U.S. accelerating at a higher pace—large-cap United States companies experienced an approximately 30% increase in the number of activist campaigns in the first half of 2021 compared to 2020 (see chart below). Notwithstanding this renewed push, activism levels remain muted compared to the 2017–2020 averages (see chart below). Nevertheless, we expect the growing momentum to continue into the second half of 2021 and into 2022.

M&A-Related Activism Remains in Focus

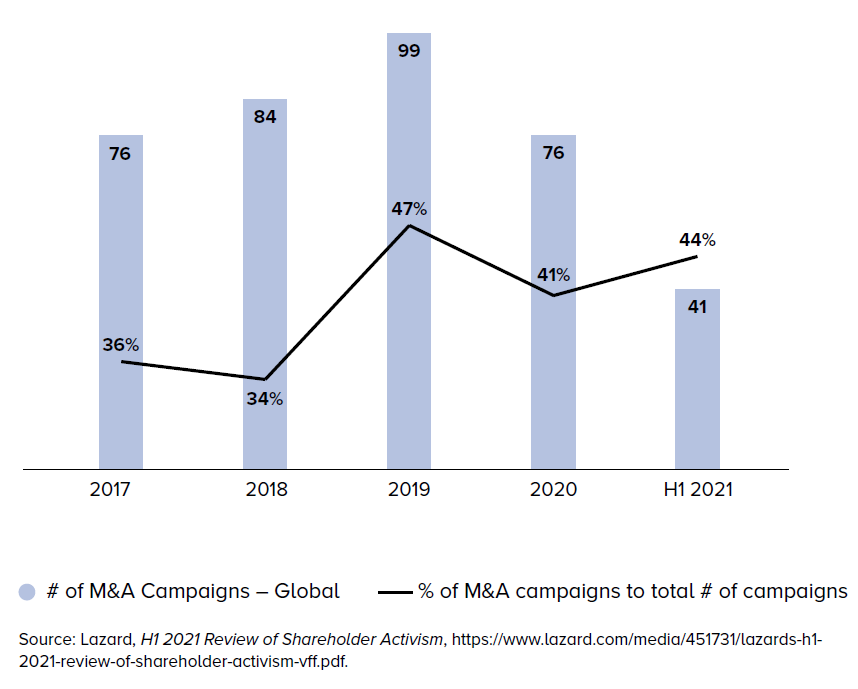

M&A-related activist campaigns remain the most common campaigns in 2020 and in the first half of 2021, constituting 41% and 44% of the total campaigns initiated at large-cap companies during such periods, respectively, consistent with levels of recent years.

ESG Activism Continues to Rise

ESG-themed or ESG-related campaigns are trending

Activists launched multiple ESG-themed campaigns in 2020 and early 2021, with environmental issues standing front and center. In 2020, London-based hedge fund BlueBell Capital Partners announced its “One Share ESG Campaign” whereby it buys one share of a company that it believes has questionable ESG practices, and later that year it targeted Belgian chemicals company Solvay to demand it cease discharging waste from its Tuscany plant into the sea. In early 2020, another London-based hedge fund, The Children’s Investment Fund (TCI), launched its “Say on Climate” campaign (modeled after the “Say on Pay” executive compensation initiative), which has resulted in more than 20 companies, including Unilever, Moody’s, Canadian National Railway, Rio Tinto, S&P Global and the Spanish airports operator Aena, committing to hold Say on Climate votes. [1] Perhaps the most notable ESG activist victory thus far was the recently formed ESG-focused activist fund Engine No. 1’s successful campaign to elect three directors to the board of ExxonMobil in a bid to push the company toward transitioning to a low-carbon economy. The campaign received significant institutional investor support, including from Vanguard, BlackRock, State Street, T. Rowe Price and CalPERS, as well as support from Institutional Shareholder Services (ISS) and Glass Lewis. Even shareholder activists that have historically not focused on ESG matters are now integrating ESG issues into their campaigns. After pushing for what was an unsuccessful sale of the utility company Evergy, activist firm Elliott settled its campaign when Evergy agreed to a five-year business plan that included the adoption of a sustainability transformation plan and a shift toward renewable energy. In its successful campaign to force the multinational insurer Prudential to separate its U.S. business and its Asia business, hedge fund Third Point argued that the divestment would save costs and reduce the company’s carbon footprint. While the activists pivoting to ESG is likely opportunistic rather than a shift away from maximizing shareholder returns, it does show that they believe that ESG may help draw support from large institutional investors, which have been more vocal about their willingness to support ESG-driven activist campaigns, and other stakeholders such as ISS and Glass Lewis.

Environmental and social (E&S) proposals gain more support [2]

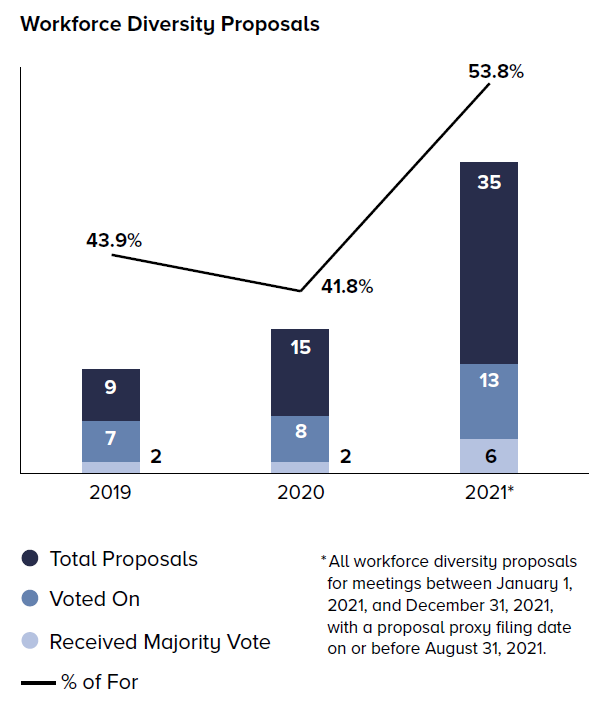

While the number of social and political proposals in 2021 remains comparable with prior years, they are garnering more support among shareholders. Nearly 20% of the social and political proposals voted on received majority shareholder support, up from approximately 10% in 2020 and 7% in 2019. All social and political proposals voted on received an average support of 34.4%, up from 27.7% in 2020 and 28.1% in 2019. Among the social proposals, those relating to racial equity reporting received a record number of submissions (eight submissions), and those related to workforce diversity increased dramatically (more than doubled the 2020 submissions and quadrupled the 2019 submissions). [3]

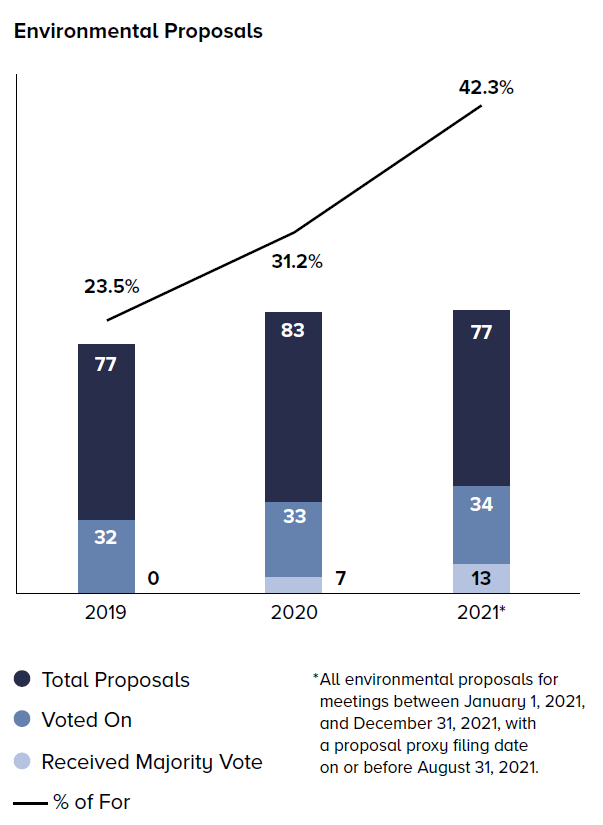

Environmental proposals are also receiving more support from shareholders in the 2021 proxy season. Approximately 38% of all environmental proposals that were voted on this year received majority shareholder support, compared to none in 2019 and about 21% in 2020. The average support for all environmental proposals voted on also increased (by more than 10% compared to 2020). [4]

We expect to see activists continuing to pivot to ESG issues in their campaigns and that companies that are both behind on ESG issues and financial underperformers will be more vulnerable to activist campaigns. We also expect shareholders to continue to engage on E&S issues inside and outside of the proxy ballot. It remains to be seen at what pace ESG-focused activist funds will grow or whether ESG issues will become a primary campaign objective given the perceived tension between the ESG-themed impact investing strategy and the conventional activist objectives of maximizing shareholder returns.

Convergence of Activists and Private Equity

The convergence of activist investing and private equity persisted throughout the COVID-19 pandemic:

Activists pursuing new pool of capital and engaging in acquisitions

Several activist funds, including Hudson Executive Capital, Pershing Square, Starboard Value and Elliott, found new avenues for raising capital during the SPAC frenzy of 2020–2021, and have deployed capital raised in SPAC IPOs to engage in heighted M&A activity. Activist investors are also finding inroads into new publicly listed companies by participating in PIPE investments associated with many of the de-SPAC transactions, alongside private equity firms (e.g., ValueAct’s investment in the EV maker Nikola and Inclusive Capital’s investment in AppHarvest, an agriculture technology company). Certain activists are also turning to what was once known as private equity turf—privately held companies—in an attempt to seek the lucrative gains enjoyed by private equity in these investments and gain access to additional information that can help inform other investment decisions.

Private equity deploying activist tactics

Private equity firms continue to make activist-like moves, including by amassing ownership stakes in public companies, engaging more actively with management and running proxy fights. KKR acquired a 10.7% stake in the restaurant and entertainment company Dave & Buster’s in early 2020 and signaled a desire to engage with the board or management and to seek board or management changes, or a possible transaction. KKR later secured a seat on Dave & Buster’s board. In September 2020, New Mountain Vantage Advisers (NMV), holding approximately 10.8% of the common stock of the IT services company Virtusa, launched a campaign against Virtusa calling for immediate board change at Virtusa to drive what it described as long-overdue corporate governance reform and management accountability. NMV and Virtusa reached an agreement in October in connection with NMV’s nominations for directors.

Activists and private equity teaming up

While activists and private equity investors have continued to borrow from each other’s toolboxes, they have also increasingly teamed up on strategic campaigns. Hedge fund Senator Investment Group joined Cannae Holdings in a buyout offer of the property data company CoreLogic, and Hudson Executive Capital joined private equity firm Apollo Global Management in a buyout offer for the ATM operator Cardtronics, while Elliott pursued a takeover of the public transportation and defense company Cubic with private equity firm Veritas Capital and worked with frequent ally Bluescape Resources against Evergy, the utility company.

The convergence of activists and private equity is the outcome of multiple factors: the intense competition for positive returns, both investment classes sharing similar sensibilities for undervalued companies (including a willingness to drive certain operational, financial and strategic efficiencies) and the record amounts of capital raised but undeployed on hand. While we expect some continued cooperation between activists and private equity, restrictions in private equity limited partnership agreements on hostile transactions and proxy fights and negative associations with activist activities may subdue cooperation on activist campaigns.

Poison Pills Surged in 2020 but Normalized in 2021

Market volatility in the early days of the COVID-19 pandemic provided activists with an opportunity to take advantage of the unprecedented drop in stock prices in March, which led to a significant uptick in the adoption of anti-takeover rights plans. About three times as many rights plans (79) were adopted in 2020 by companies listed in the United States compared to historical numbers (22 in 2018 and 23 in 2019), with 60% being adopted during March, April and May. As the markets normalized in the second half of 2020 and the risks related to opportunistic acquisitions and activist strategies declined, the rate of adoptions slowed and fell in line with prior years. [5] We expect the rate of rights plan adoptions to be consistent with historical (pre-COVID) low levels in the second half of 2021.

Endnotes

1See Say On Climate, https://sayonclimate.org/supporters.(go back)

2Note that some socially or environmentally focused campaigns occurred primarily outside of the proxy ballot. The campaign spearheaded by the New York City Comptroller’s Office seeking public disclosure of the S&P 100 companies’ Employment Information Report (EEO-1, which provides a demographic breakdown of an employer’s work force by race and gender) data and the non-profit shareholder advocacy group, As You Sow’s engagement with companies asking for net zero transition plans with shareholder voting both fall under this category.(go back)

3Source: Deal Point Data. Proposals are limited to Rule 14a-8 proposals for meetings during the relevant period and for 2021, with a proposal proxy filing date on or before August 31, 2021.(go back)

4Source: Deal Point Data. Proposals are limited to Rule 14a-8 proposals for meetings during the relevant period and for 2021, with a proposal proxy filing date on or before August 31, 2021.(go back)

5Source: Deal Point Data.(go back)