Print

PrintMatthew Behrens and Annie Anderson are associates at Shearman & Sterling LLP. This post is part of the 19th Annual Corporate Governance Survey publication prepared by Shearman & Sterling LLP, by Mr. Behrens, Ms. Anderson, Richard Alsop, Doreen Lilienfeld, Gillian Moldowan, and Lona Nallengara. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) and Will Corporations Deliver Value to All Stakeholders?, both by Lucian A. Bebchuk and Roberto Tallarita; For Whom Corporate Leaders Bargain by Lucian A. Bebchuk, Kobi Kastiel, and Roberto Tallarita (discussed on the Forum here); and Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy—A Reply to Professor Rock by Leo E. Strine, Jr. (discussed on the Forum here).

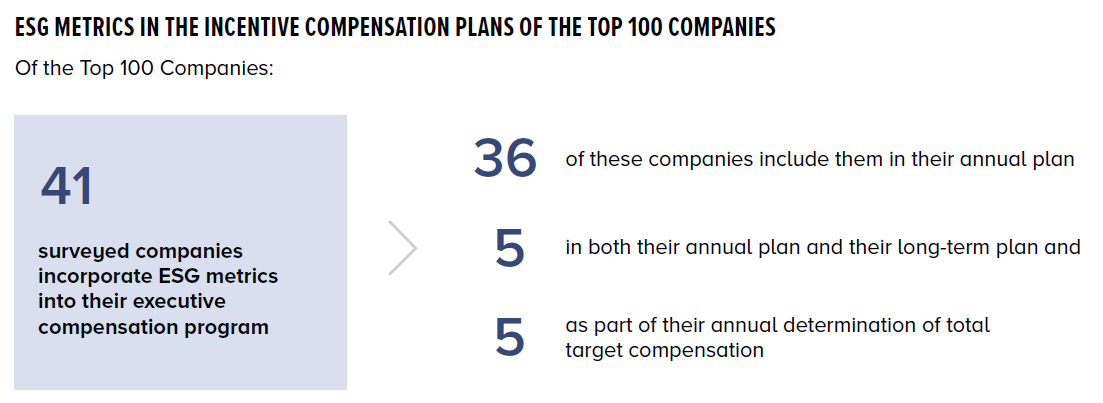

Although COVID-19 and its impact on business operations brought its own challenges to issuers’ incentive compensation programs, a review of 2020 proxies showed no slowdown in the incorporation of ESG metrics into plan design. Traditional incentive compensation metrics, namely quantitative shareholder return and financial and operational metrics, still dominate but, increasingly, qualitative “social” factors, such as diversity and pay equity, are playing a meaningful role in executives’ take-home incentive pay. In the Top 100 Companies, 15 have announced in their 2020 CD&As that incentive compensation for 2021 will include new ESG metrics. The move toward ESG metrics is both a response to stakeholder pressures and a growing recognition that these factors are important to long-term shareholder value.

This post discusses the forces leading companies to adopt ESG metrics, analyzes how those companies are incorporating ESG metrics into their incentive compensation programs and discusses the challenges of establishing meaningful metrics.

The Forces of Change

A number of forces have led to the increased use of ESG metrics in incentive compensation plans. These include:

1. Institutional Investor Focus on Sustainability

In January of 2020, Larry Fink, Chairman and CEO of BlackRock, noted in his letter to CEOs that failure to focus on the needs of a broad range of stakeholders will ultimately damage long-term profitability. In his 2021 letter, Mr. Fink reiterated this position and called for a single global standard with respect to sustainability disclosures. Survey data shows that asset managers agree that a focus on ESG brings financial benefits. According to the 2020 RBC Global Asset Management (RBC GAM) Responsible Investing Survey, 75% of institutional investors in Canada, Asia, the United States and the United Kingdom apply ESG principles to investment decisions, with a 26% increase in Asia. In addition, 43% of the respondents said they believe ESG-integrated portfolios are likely to perform best, which is a 14% increase from 2019. Notably, the United States lags behind its peers, as only 28% of U.S. institutional investors polled held this view.

2. Shifting Views of the Role of the Corporation

In August of 2019, more than 180 CEOs signed onto a Business Roundtable statement that, for the first time, expanded the view that corporations exist principally to serve their shareholders to say that corporations should commit to serving the interests of all stakeholders, including shareholders, customers, employees, suppliers and communities. The Business Roundtable’s position undoubtably reflects increasing public, investor and employee pressure on companies to focus not only on advancing profits, but to also contribute to solving societal problems such as income inequality and environmental sustainability. The incorporation of ESG into incentive compensation plans is a key measure that observers will use to track whether the signatories’ companies are honoring this new philosophy.

3. Regulatory Activities

In March of 2021, the SEC requested public input on climate change disclosure and tasked the staff with evaluating SEC disclosure rules related to climate change. The SEC received more than 550 unique comment letters in response, and three out of every four letters was in support of mandatory climate disclosure rules. SEC Chair Gary Gensler subsequently announced that the staff is developing a mandatory climate risk disclosure rule for the SEC’s consideration by the end of the year, emphasizing that investors are looking for “consistent, comparable, and decision-useful” disclosures in this regard. In addition, the removal of the “performance-based compensation” exemption from Section 162(m) of the tax code provides companies with greater latitude to use qualitative performance metrics and to implement a bonus “modifier,” which enables the company to increase the payable bonus as a result of a subjective determination, such as a commitment to the company’s ESG principles.

The Challenge of Metrics

Boards looking to incorporate ESG metrics into incentive compensation plans are faced with the dual challenge of choosing appropriate metrics and appropriately measuring success. Although there is a movement toward establishing a global set of standards for reporting ESG metrics—as is the case with financial reporting—there is an ongoing debate as to whether a global set of ESG standards is, in fact, beneficial. For example, in April of 2021, SEC Commissioner Hester Peirce argued that a “global reliance on a centrally determined set of metrics could undermine the very people-centered objectives of the ESG movement by displacing the insights of the people making and consuming products and services.” [1] Further, for any individual issuer, the chosen set of global standards required to be reported on may not align with the long-term business strategy of the issuer and, therefore, may not be appropriate as an incentive compensation metric.

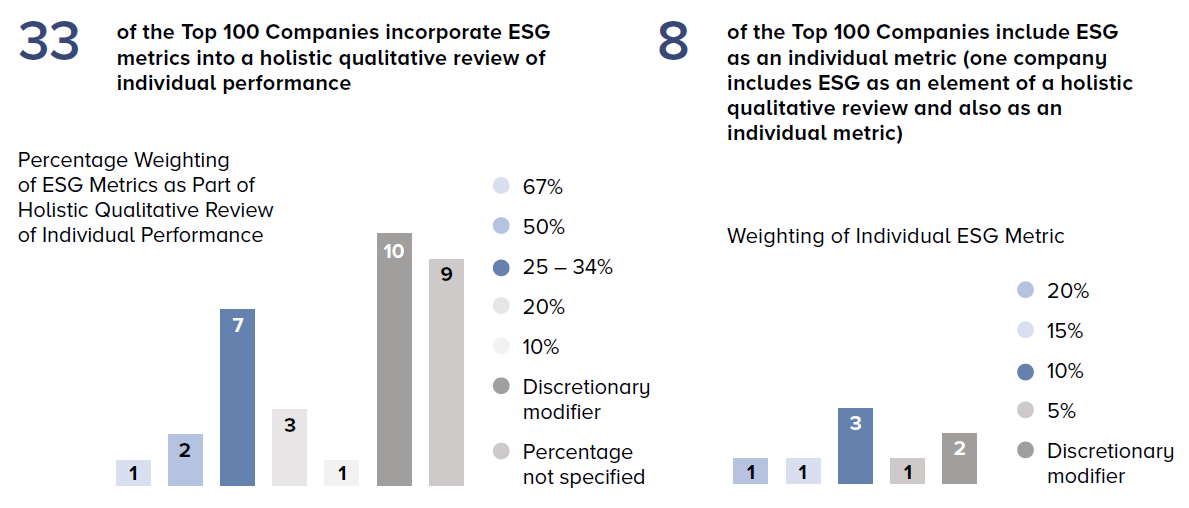

As issuers continue to grapple with how best to incorporate ESG metrics in their incentive compensation programs, most provide for a qualitative review and include the metrics as part of an overall review of individual performance. Regardless of how the ESG metrics are utilized, they should come coupled with transparent disclosure to investors as to how and why the metrics were chosen, weighted and evaluated.

Action Items for Incorporating ESG Metrics

The following is a list of action items for companies looking to incorporate ESG metrics into their incentive compensation programs:

1. Engage with Shareholders

As part of a company’s regular calendar on shareholder engagement, the company should discuss with key shareholders the inclusion of ESG metrics into its incentive compensation programs. Companies should seek to emphasize that these metrics are not divorced from the interests of shareholders but are, in fact, value drivers.

2. Identify the Appropriate Metrics

Consider a task force comprising different stakeholders within the organization that can appropriately determine ESG metrics that reflect the company’s strategy and key risks and promote value creation.

3. Ensure a Line of Sight between Executive Actions and Performance

Incentive compensation metrics are without value if employees do not have the ability within their job function to impact the desired outcome. For example, while improved safety may be an important goal for an organization, it is likely the controller has little ability to effect change in this regard and his or her attention should be directed toward other goals of the company.

4. Set Goals

With a lack of historical context by which to measure ESG progress, consider providing the compensation committee with discretion to determine how executives have performed with respect to the company’s ESG goals. Although companies may decide to measure success against targets set by third parties, such as SASB, these external targets may not be appropriate for every individual company. Also, determine whether goals should be annual or long-term. As shown in the Survey data, most ESG metrics are tied to annual incentive plans, reflecting the long-held belief that long-term goals should relate to financial and shareholder return metrics.

5. Review Your Executive Officer Scorecards

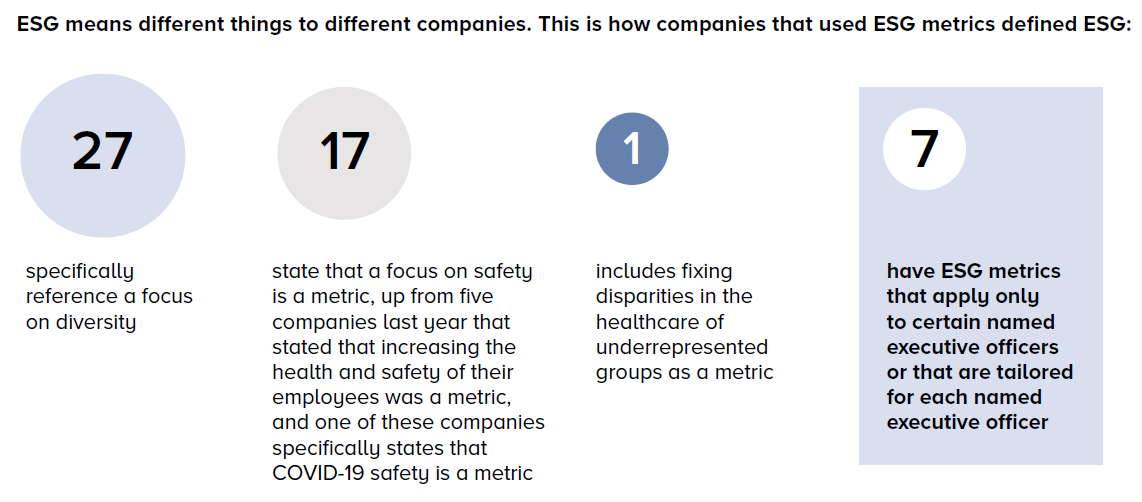

As discussed, unlike financial metrics, ESG performance cannot be boiled down to numbers on a spreadsheet and requires a subjective analysis. Therefore, when evaluating the overall performance of the company’s executive officers, the board should include relevant ESG metrics on its scorecards.

The DOL’s Rules on ESG Investing for ERISA Plans—The Pendulum Swings Again

In December 2020, the Department of Labor (DOL) published a final rule with respect to ESG investing in the ERISA context. Purporting to reflect the DOL’s long-standing position that ERISA fiduciaries may not sacrifice investment returns in order to promote social, environmental or other policy goals, the rule provided that ESG factors may be considered only to the extent they present material economic risks or opportunities. The rule was not without controversy, as evidenced by the over 8,000 comment letters sent to the DOL following the initial release of the proposed rule.

Reflecting the long-standing back and forth between Republican and Democrat administrations as to the role of ESG considerations in ERISA investing, the Biden administration announced it would not enforce the rule and, on October 13, 2021, the DOL promulgated a new proposed rule. The proposed rule addresses concerns that the previous rule put fiduciaries at risk if they considered ESG factors in their financial evaluation of plan investments. Therefore, the proposed rule eliminates the requirement that fiduciaries only consider “pecuniary factors” in making investment decisions and allows fiduciaries to consider any factor that is material to the risk-return analysis. Therefore, the proposal would allow fiduciaries to consider ESG factors, including climate change-related factors.

Endnotes

1See Hester Peirce, “Rethinking Global ESG Metrics,” Views—the Eurofi Magazine, page 208 (April 2021). (Also available at https://www.sec.gov/news/public-statement/rethinking-global-esg-metrics).(go back)