Print

PrintKei Okamura is Director of Japan Investment Stewardship at Neuberger Berman LLC. This post is based on his Neuberger Berman memorandum.

Issues of corporate governance, capital management and sustainability have been on the radar in Japan for the past decade, but soon the pace of change could accelerate. The difference is a revised Corporate Governance Code and the upcoming overhaul of the Tokyo Stock Exchange, which aim to reinforce the role of sound governance and capital efficiency in enhancing shareholder value and are expanding their scope to issues such as diversity and climate change. In this post, we assess the potential implications, and explain why companies’ ability to adapt to the new Code could be crucial to their success moving forward.

Introduction

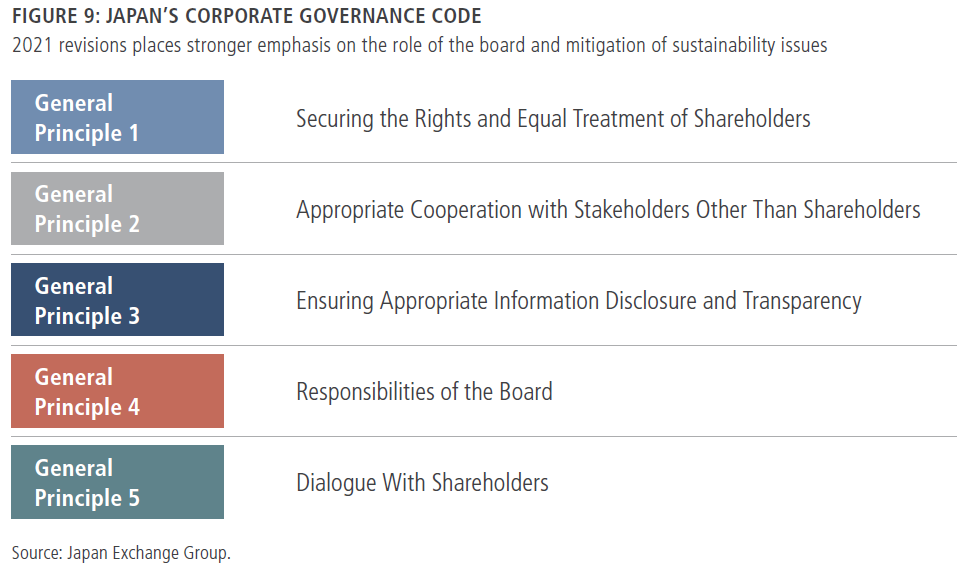

Over the next 12 to 24 months, Japanese companies will embark on a historic overhaul of the ways they address corporate governance, capital management and financially material environmental and social risks to seek long-term sustainable growth opportunities. These issues have been on the radar since the early 2010s, when former Prime Minister Shinzo Abe placed corporate governance reforms at the heart of the nation’s growth strategies, known as “Abenomics.” What is different this time around, however, is the Japan Corporate Governance Code, which was revised in June 2021 to place greater emphasis on the role that corporate boards and their committees should play in enhancing shareholder value. The scope of the Code was also expanded to include sustainability issues such as gender diversity and climate change. Further, the Code now includes an enforcement element that targets nearly 60% of the country’s 3,800 listed companies, which will have to adhere to the Code on a “comply or explain” basis to become members of the Tokyo Stock Exchange’s (TSE) coveted Prime section, which is expected to go online in April 2022. Concurrently, the government is reportedly considering an overhaul of existing greenhouse gas (GHG) emissions and climate change risk-related disclosure rules for companies.

We believe Japan is on the cusp of a new wave of deeper and more comprehensive reforms than those of “Abenomics.” The breadth of change may also be more pronounced among the small to midsize companies that previously were left behind in governance reforms. In our view, there will be winners and losers from these changes, while a bottom-up and active long-term approach to investing has the potential to help identify companies able to undergo fundamental reforms that could facilitate sustainable growth opportunities.

Time Is Running Out for Japan

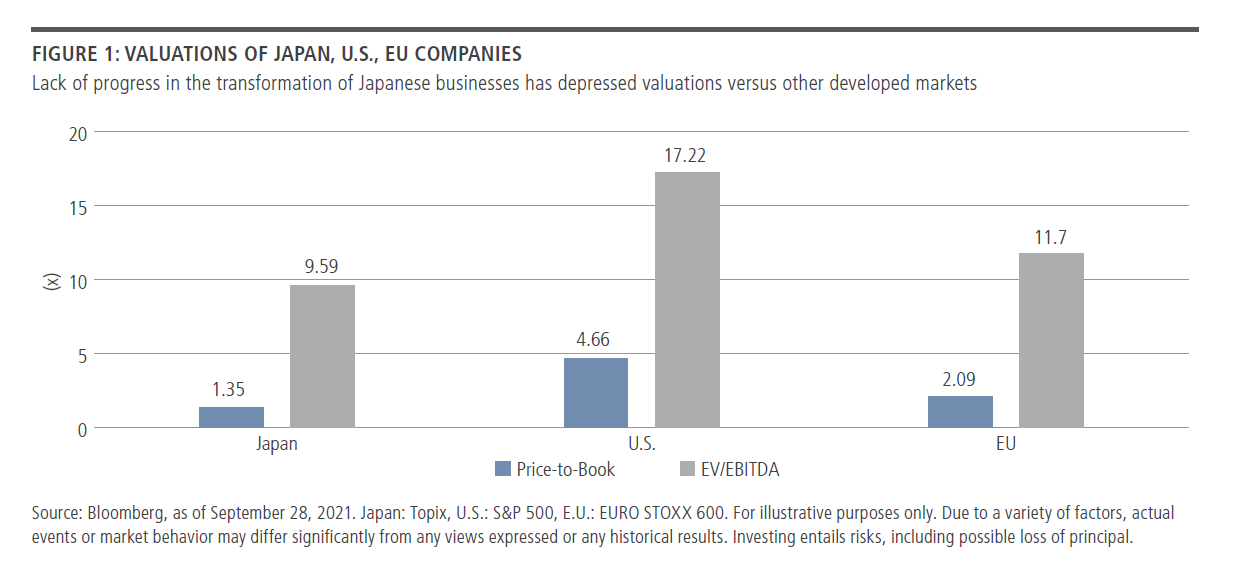

We believe it is critical for Japanese companies to address deeply rooted capital management, governance and sustainability issues, and that now may be an opportune time. The numbers speak for themselves. Since the bursting of the economic bubble in the early 1990s, the total return of Japan’s benchmark Topix Index has been a mere 79%. That compares to the EURO STOXX 600 Index’s 830% and the S&P 500 Index’s 2,025% during the same period. [1] Valuations tell a similar story, with the Topix price-to-book ratio (PBR) at 1.4 compared to the EURO STOXX 600 Index’s 2.1 and S&P 500 Index’s 4.7, [2] while other metrics like EV/EBVTIDA also support this view (see Figure 1).

We believe this disparity in valuation between Japan and other developed markets is due to a combination of the government’s slow progress in revitalizing the economy from the so-called “lost decades,” companies’ inability to address fundamental inefficiencies in their businesses, and the public’s struggle to wean itself from a deflationary mindset.

Today, with the COVID-19 pandemic, the accelerated pace of global digitalization appears to be widening the valuation gap further. In August 2021, the combined market capitalization of Google, Apple, Facebook and Amazon was some US$7.5 trillion, overtaking the US$6.8 trillion market value of all listed Japanese companies combined. [3] Further, the global shift in capital flows to sustainable investing, led by EU and U.S. investors, has also raised alarm as to whether ESG issues could lead to further underperformance. Japan

is a net importer of energy, and its reliance on fossil fuels has increased sharply due to the government’s revised energy policy since the 2011 Fukushima nuclear disasters. We believe the economy also remains skewed toward asset-heavy, carbon-intensive manufacturing, which makes up 21% of GDP versus Europe’s 14% and the U.S.’s 11%, [4] raising investor concern that Japan could be put at a disadvantage in a global sustainability framework based on the European taxonomy system.

Japan’s Smaller Companies Left Behind in Governance Reforms, Sustainability Transformation

Faced with a sense of crisis, then-Prime Minister Abe launched Abenomics and its “three arrows” in the 2020s, targeting monetary easing, fiscal stimulus and structural reforms. The third arrow included measures to strengthen corporate governance among Japanese companies in order to address inefficiencies, including the double codes of Stewardship (2014) and Corporate Governance (2015).

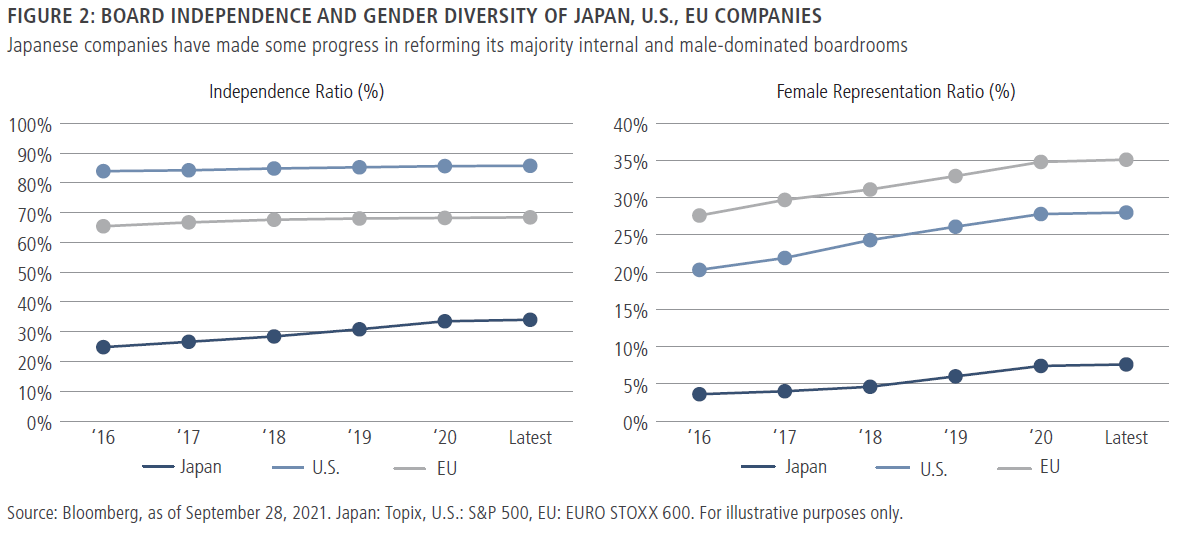

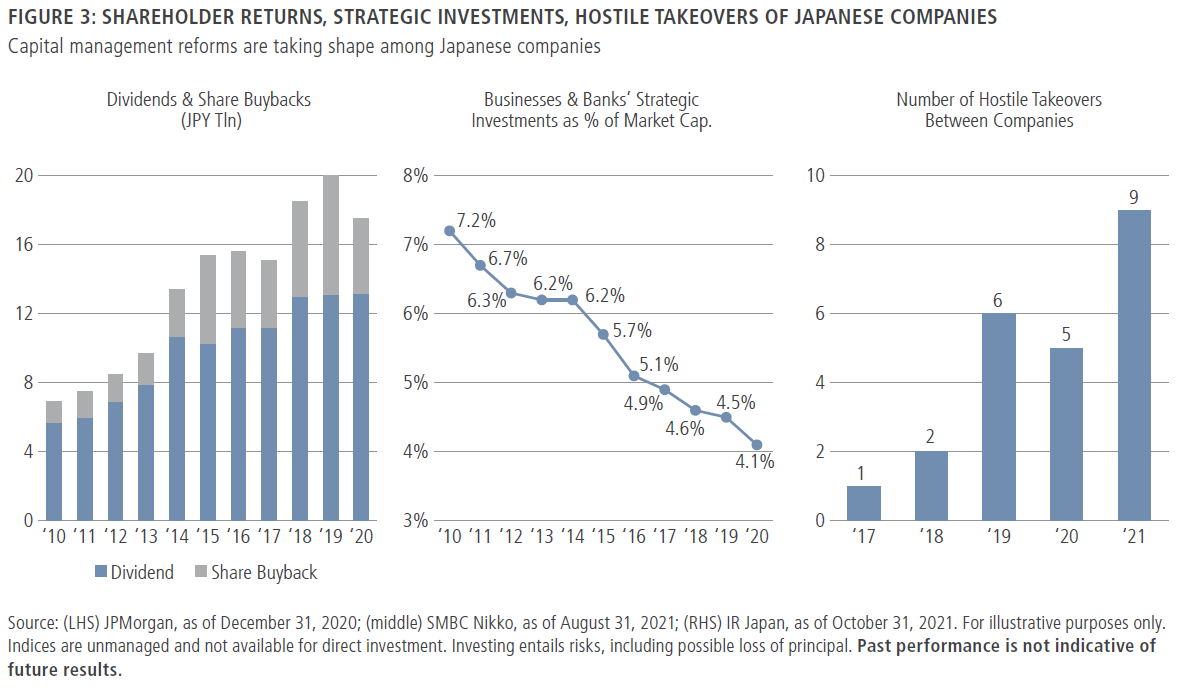

While the impact of the first two arrows has yet to be determined, we believe the third arrow has not completely missed its mark. Since 2016, the average board independence ratio of companies listed in the Topix Index has increased nine percentage points to 34.0% while the average female representation on boards has gained four percentage points to 7.6% (see Figure 2). [5] Although these ratios still lag those of equivalent indices in the U.S. and EU, we consider this to be notable progress for a market where many companies have historically been run by majority-internal and male-dominated boards. We believe this gradual shift to improve board independence and diversity, along with increased pressure from institutional investors, has contributed to corporate management’s early steps to address capital efficiency issues such as reducing surplus capital through higher shareholder returns, business restructurings targeting non-core assets, and the unwinding of cross-shareholdings (see Figure 3).

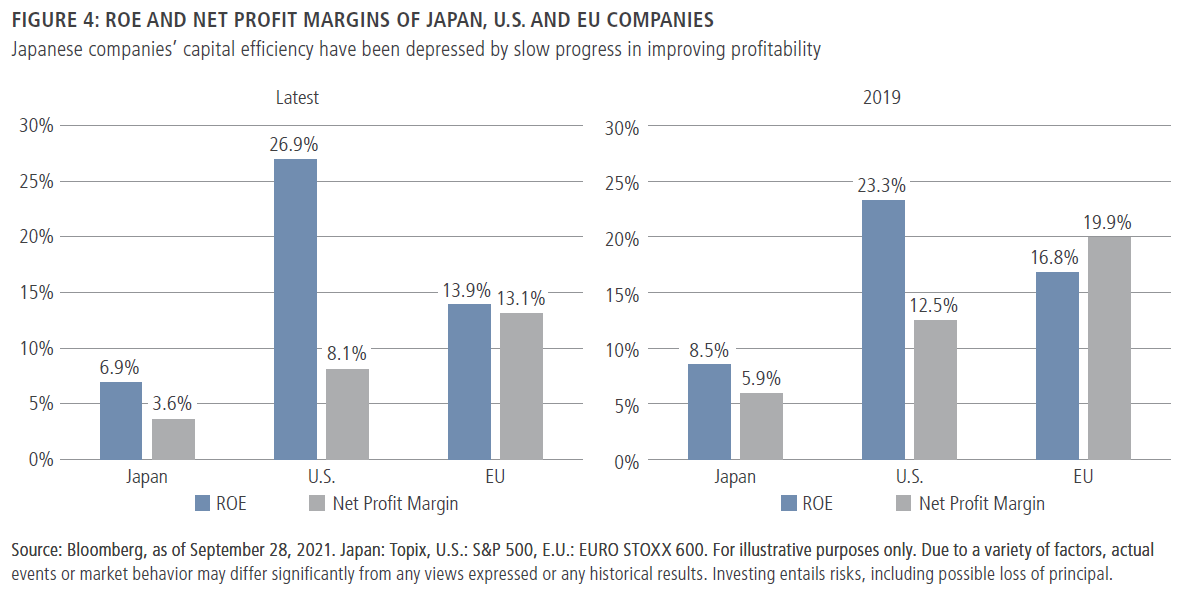

We believe the previous administration’s efforts have helped to raise awareness among Japanese companies of the importance of corporate governance and the role it can play to address capital management and sustainability issues. However, in our view, the awareness has not resulted in a fundamental shift in management decision-making on these topics. We see this in capital efficiency ratios like return on equity (ROE) and net profit margins, where Japan continues to lag developed market peers (see Figure 4) [6]—something we attribute to, in certain cases, overdiversified businesses resulting in a lack of focus, misallocation of resources, continuing uncompetitive products and bloated cost structures.

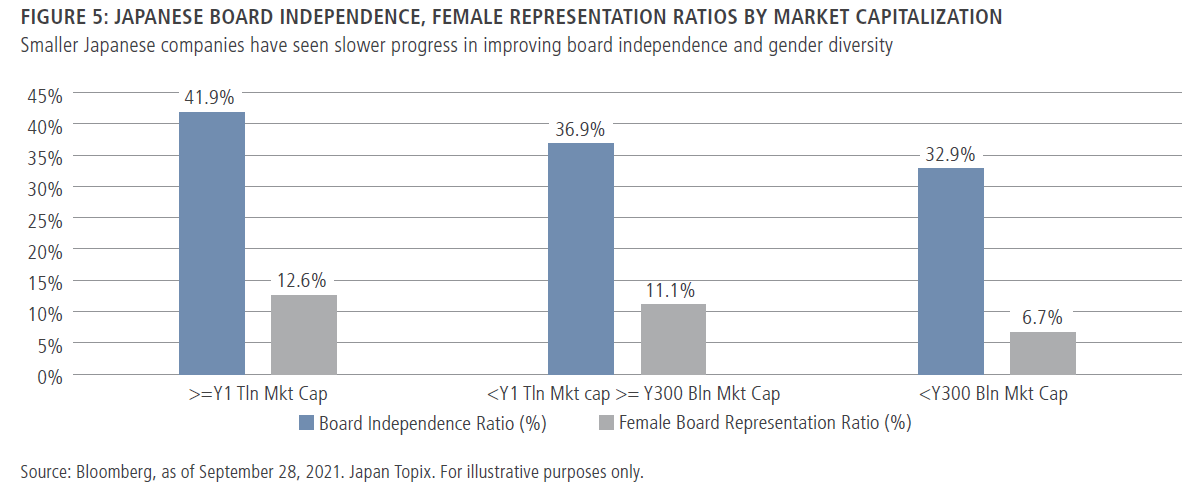

Further, many Japanese small to midsize businesses under one trillion yen in market cap have yet to implement corporate governance reforms or address financially material issues to their businesses. Since 2016, we have witnessed a small group of progressive companies in this cohort taking proactive measures to improve board independence and diversity, but the majority continue to lag bigger companies (see Figure 5). [7] Based on our conversations with corporate managements at small to midsize firms, a key reason is a perceived lack of qualified candidates for independent director and auditor roles, while the same rationale is cited for low gender representation in boardrooms. While many small to midsize companies do face challenges in accessing external talent, we believe some company managers have not embraced the importance of corporate governance and the role that it can play in fostering dynamic discussions within the boardroom to promote fundamental change.

We have seen Japanese companies take a more proactive stance in recent years to mitigate sustainability issues related to environment and social responsibility and improving related disclosures. According to the Government Pension Investment Fund’s (GPIF) annual survey of listed companies, the proportion of respondent firms that have voluntarily disclosed non-financial information including ESG topics rose nearly four percentage points to 78.5% from 2019 to 2020. [8]

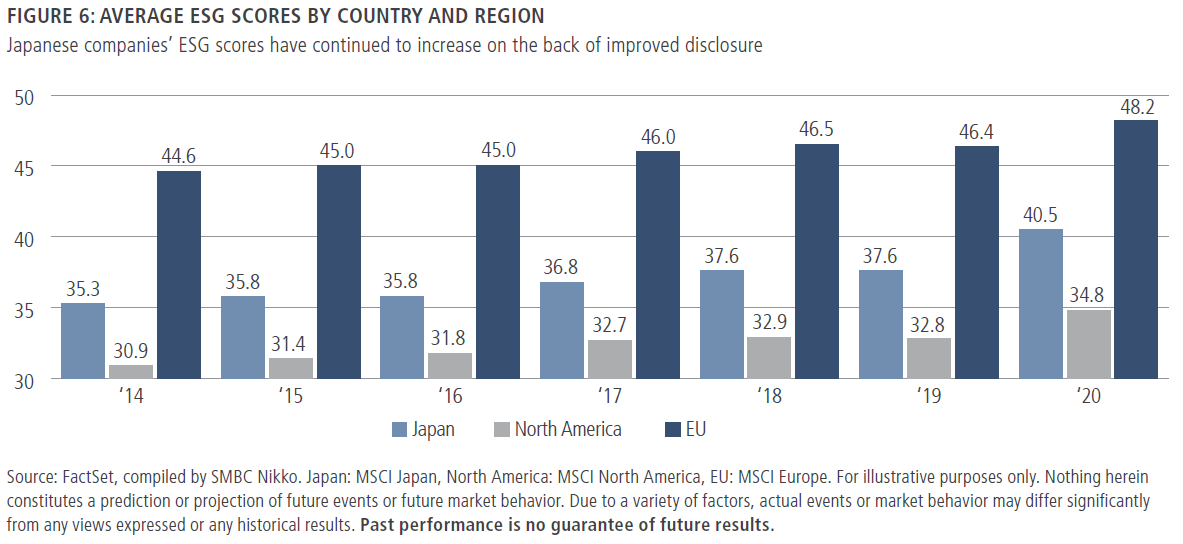

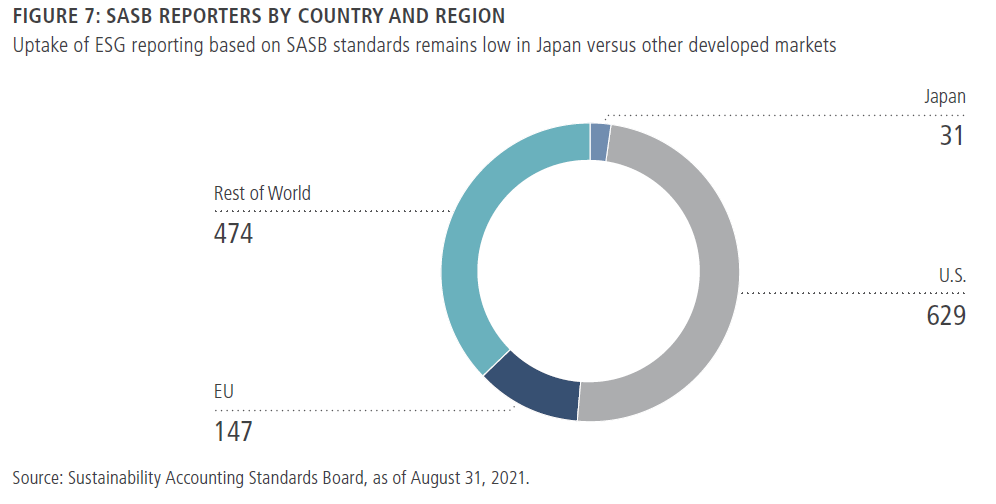

This improved disclosure may be one of the factors that contributed to the increase in some Japanese companies’ ESG scores in the last several years (see Figure 6). [9] However, based on our discussions with Japanese firms, we believe that many are still at the early stages of embracing the concept of sustainability at the management level and as part of a long-term growth strategy. A case in point is the relatively low uptake of key sustainability disclosure standards like the Sustainability Accounting Standards Board (SASB) and its framework of materiality, which we view as a critical tool to address ESG risks for long-term value creation. However, the number of Japanese companies that have adopted and reported based on SASB standards remains at 31 companies or 2.4% of all SASB reporters, compared to 49% and 12% for the U.S. and EU, respectively (see Figure 7). [10] For reference, the 31 Japanese firms represent 13% of the country’s listed companies by market value. [11]

Meanwhile, climate change has become a topic of growing interest among companies, especially after the 2020 announcement by the Japanese government of its intention to reduce GHG emissions to zero by 2050 to achieve “carbon neutrality.” [12] This has been a key driver of the expanding support for climate change disclosure related to the Taskforce on Climate-Change Related Financial Disclosure (TCFD) framework, with Japan seeing the highest number of TCFD supporters in the world at 475 institutions. [13]

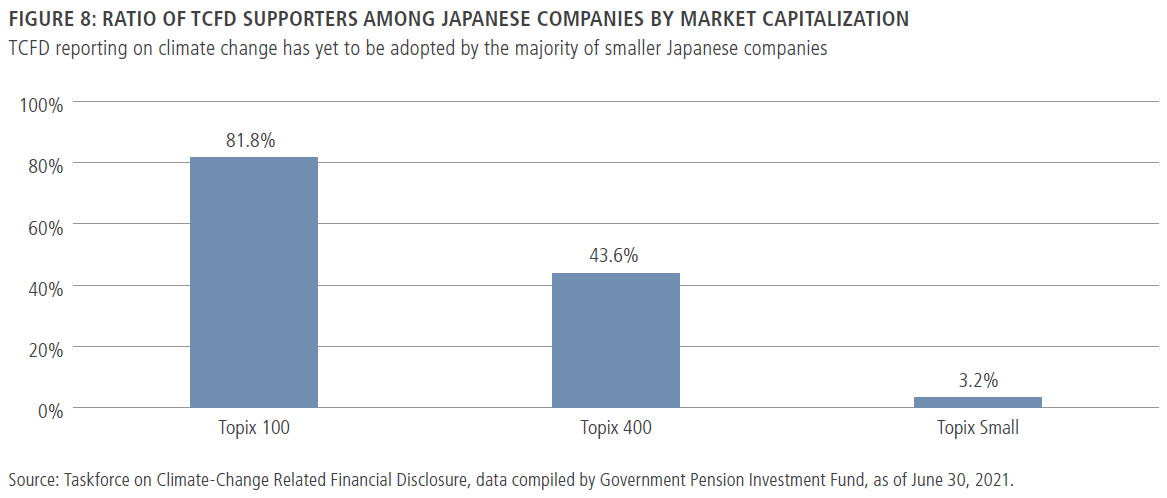

However, according to the GPIF, supporting public companies are generally larger, with less uptake in the small to mid-cap category (see Figure 8). In our meetings with such companies, often-cited hurdles to addressing climate change risks have included a lack of reliable data on emissions and the human and financial resources needed to undertake disclosure, especially in 2-degree scenario analyses. [14]

The Changes to Come in Japan

Japanese corporate governance has made progress over the last several years, but we believe one of the reasons this has not resulted in a rerating of the Japan equity market is that the changes have not addressed the fundamental issues of businesses. Based on our conversations with management, many companies still do not view enhancing board independence or diversity, improving shareholder returns or mitigating sustainability issues as requisites in seeking potential long-term sustainable growth. Instead, they see such changes as necessary to appease increasingly vocal stakeholders, raise ESG ratings and/or as an extension of their activities in corporate social responsibility. We believe this is partly because government-led reforms have lacked enforcement and incentives to instigate a fundamental shift in management mindset. Hence, we view Japan’s recent revision of its Corporate Governance Code as a potential gamechanger. The revised Code gives more clarity to the role boards should play in protecting minority shareholder rights and raising company value.

With the Code becoming a criterion (on a comply-or-explain basis) for companies to be included in the new TSE Prime market starting in April 2022, we believe corporate management will have an incentive to comply. Further, we believe companies will need to consider more carefully the impact of their reforms within the context of corporate value creation, as they will need to maintain a market value above certain thresholds to remain constituents of the Topix Index, which is slated to undergo a phased overhaul starting in 2022. Below, we highlight some of the key upcoming changes that investors should consider.

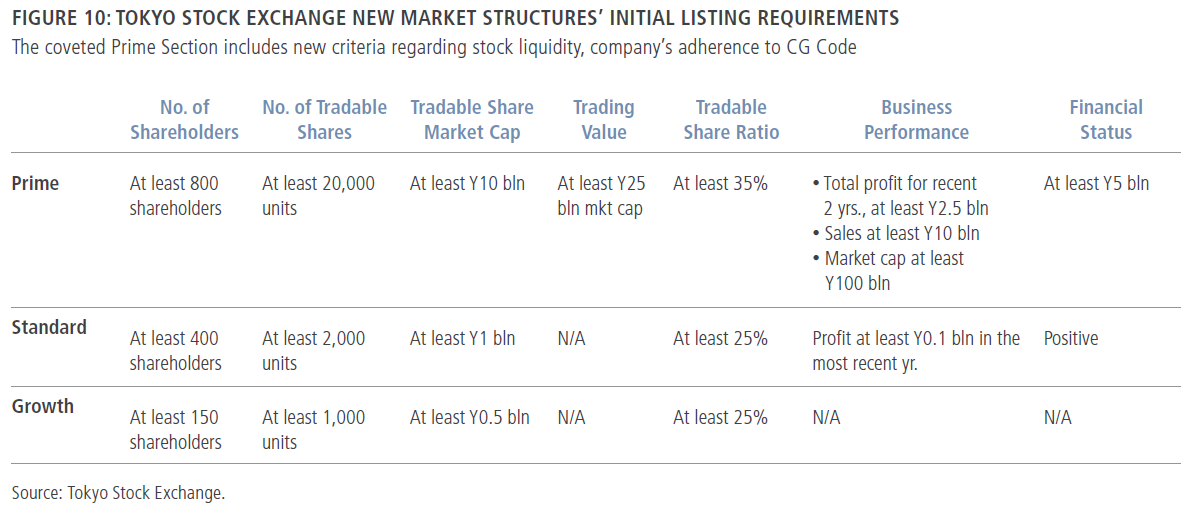

In our view, many investors outside of Japan do not yet fully appreciate the magnitude of the impending changes to the TSE market in 2022. This is undoubtedly the biggest shake-up of the Tokyo bourse since its establishment in 1847. Starting next April, the current sections of TSE First, TSE Second, Mothers and JASDAQ will be consolidated into Prime, Standard and Growth categories. The most coveted market segment will be Prime, which is equivalent to today’s TSE First; many companies see membership in this segment as a status symbol that helps to recruit top talent and maintain business relationships with clients and financial institutions. The more than 2,000 companies (roughly 60% of all listed companies in Japan) that make up today’s TSE First section will have to meet various criteria to be considered a member of the new segment. [15] There are two requirements for Prime market listing, related to stock liquidity and corporate governance, that we see as particularly noteworthy: a minimum ratio of tradable shares and adherence to the revised Code on a comply-or-explain basis. [16]

With regard to stock liquidity, companies seeking listing in the Prime section will need to maintain a ratio of tradable shares at or above 35% of the outstanding amount (25% each for the Standard and Growth sections). In addition, the TSE has redefined “tradable shares” to exclude stakes held by domestic banks, insurance companies and/or business entities. In other words, the uniquely Japanese practice of making strategic investments via cross-shareholdings—often representing a large portion of equity—will no longer be counted as “tradable shares” (see Figure 10). We believe these new requirements will encourage Japanese companies to rethink their capital alliances with clients, business partners and group companies that have often been criticized as leading to inefficient allocation of capital and resulted in coordinated proxy voting. Should this happen, we anticipate that corporate governance could be strengthened as management accountability increases and capital efficiency improves, given capital redeployment that is more focused on growth investments and/or higher total shareholder return.

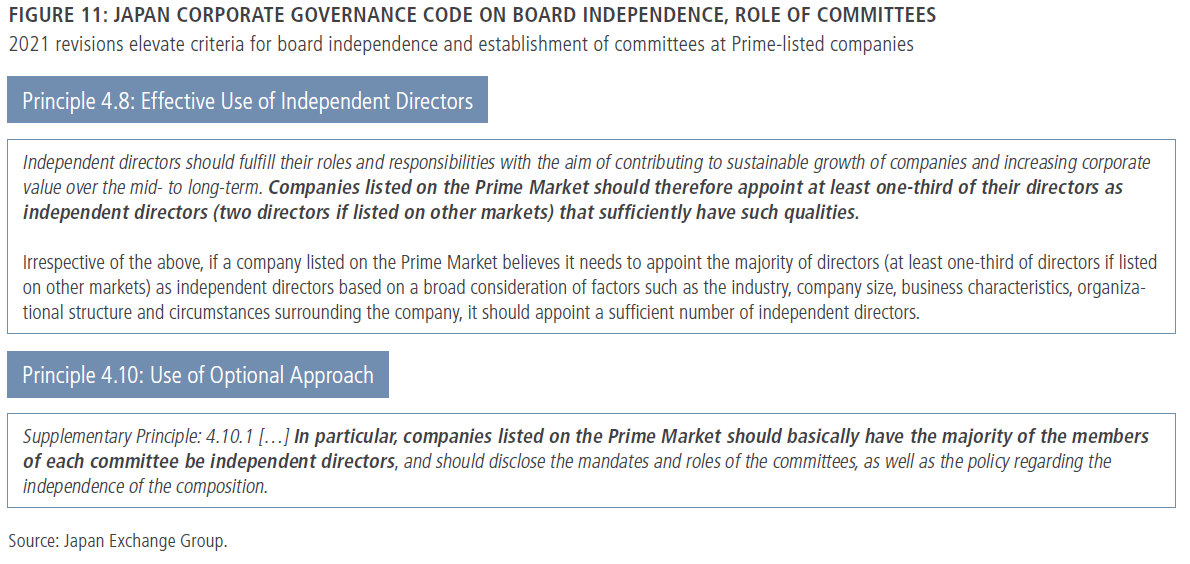

With regard to the revised Corporate Governance Code, we believe that three key amendments could play a crucial role in promoting fundamental change in the way Japanese companies embrace corporate governance. First, the revised Code sets quantitative guidelines for all Prime-listed companies to have at least one-third board independence and for listed subsidiaries with controlling owners to have a majority independent board and/or a special independent committee to oversee potential conflict of interest issues like takeover proposals (see Principle 4.8: Effective Use of Independent Directors in Figure 11). In addition, compensation and nomination committees are recommended to be majority-independent (see Supplementary Principle of Principle 4.10: Use of Optional Approach, also in Figure 11).

We believe having a clearer definition of independence is vital to fostering dynamic and objective boardroom discussions on management issues that concern the protection of minority shareholder rights and corporate value. We believe this will be particularly important in the coming years as corporate mergers and acquisitions (M&A) and takeover activities are expected to pick up as companies review capital alliances as part of financial management reforms.

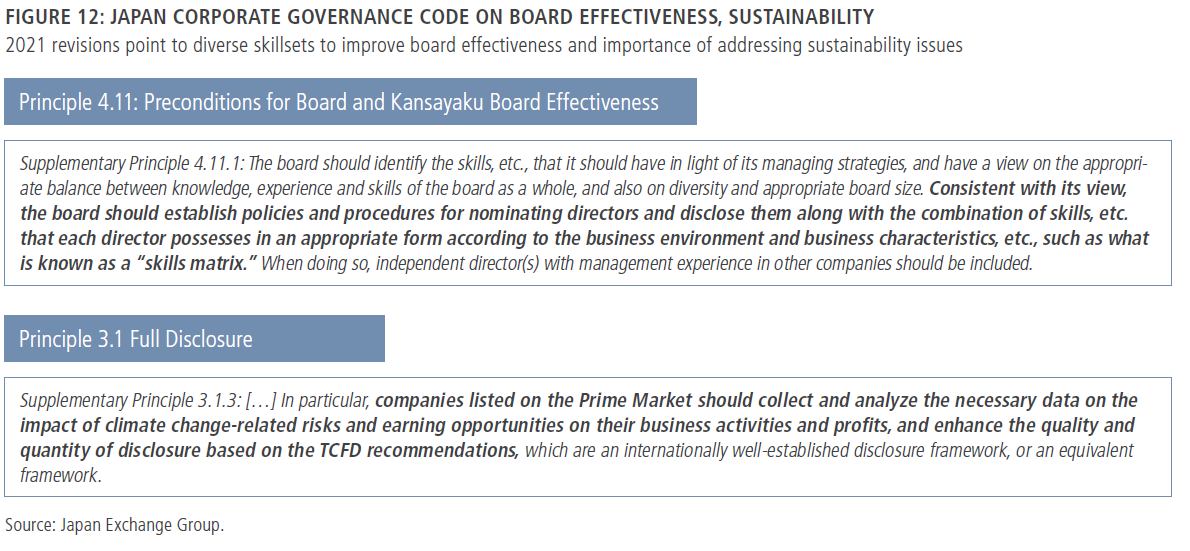

Second, to help reduce the risk of companies taking a box-ticking approach to meeting independence requirements by appointing affiliated external members to the boards with misaligned skills, the revised Code also recommends that the board identify what it sees as necessary skills and experience to effectively monitor management and to present the analysis in the form of a “skills matrix” (see Supplementary Principle of Principle 4.11: Preconditions for Board and Kansayaku Board Effectiveness in Figure 12).

We view the skills matrix as a key piece of disclosure that could provide valuable hints as to the strengths and weaknesses of the board and where certain expertise may be over- or underrepresented. Historically, Japanese boardrooms have typically been composed of salarymen turned executives, who have spent their entire careers at a company and therefore offer operational skill and know-how, but lack in hard management experience in key areas such as corporate finance, M&A, human capital management and, more recently, on issues such as sustainability and digital transformation. From that perspective, a skills matrix could be instrumental to encourage and direct the company to appoint experienced male and female executives in fields where the board lacks expertise.

Third, the revised Code places a stronger emphasis on the importance of integrating material environment and social responsibility issues into management decision-making. Previous editions of the Code also emphasized the importance of addressing sustainability issues, but in our view their wording lacked specificity and the enforcement element. In this revision, the Code includes detailed language that all companies should consider establishing a basic policy on mitigating sustainability issues and that Prime companies should address specific topics like climate change risks, based on the TCFD framework or an equivalent internationally recognized standard (see Supplementary Principle of Principle 3.1: Full Disclosure in Figure 12).

It’s also worth highlighting that the government is considering amending existing public disclosure rules to include climate change risks, as part of the mandatory disclosure requirements in annual securities filings starting in 2023. [17] Should this materialize, it would apply to not just Prime section companies, but all publicly listed firms in Japan. A preliminary survey of companies during the public consultation period for the new Code found that small to midsize companies saw climate change risk mitigation and TCFD disclosure as top issues to address in the Code, which suggests to us that their mindset on this topic may be gradually changing. [18]

Disclosure reform may also take place on the operational level with the Ministries of Trade and Environment reported to be preparing revisions to companies’ GHG emissions disclosure rules, also starting in 2023. [19] It’s relatively unknown outside of Japan that the country was one of the earlier adopters of mandated company disclosure on emissions, as part of the Act on Promotion of Global Warming Countermeasures, which was born out of the Kyoto Protocol. The Act covers key topics such as carbon dioxide, methane, hydrofluorocarbons (HFC) and sulfur hexafluorides (SF6). [20]

However, the Act was implemented in the mid-2000s and, over the years, its disclosure format has become out of sync with global ESG standards, for example, requiring just biannual reporting and parent company emissions sourcing. The Ministries are reported to be considering a change to disclosure on an annual basis, and including emissions by subsidiary and group companies. This could remove one of the key hurdles to obtaining reliable data, and facilitate the mitigation of climate change risks at the subsidiary level. It could also pave the way for more Japanese companies to pursue TCFD reporting, which could help long-term investors to assess company sustainability.

A Golden Opportunity

We believe the noted potential changes could help to push companies to embrace good corporate governance as part of a long-term strategy to raise corporate value. Naturally, we believe there will be winners and losers that emerge from such a transformation, as some managements will proactively pursue measures to seek sustainable growth potential while others will fail to keep up. As long-term active investors in Japan, we see the next 12 to 24 months as a golden opportunity to identify such differentiation.

We are also cognizant that many attractive firms, especially small- to midsize companies, may want to reform, but lack the know-how and resources to do so. Hence, we are taking a proactive approach to engaging corporate management and providing detailed overviews of what issues we believe are most pertinent to their business fundamentals. We are also suggesting practical ideas on how companies with limited human and financial resources can seek to mitigate these issues to access long-term growth opportunities. The engagements take place over the duration of our investment timeframe and are managed based on our “Milestone Framework,” which includes an objective and a set of key performance indicators (KPIs) to consider in the interim.

Through these discussions, we ask that companies integrate both capital management and sustainability issues as part of a long-term management strategy to seek sustainable growth potential. In doing so, we encourage them to set medium- to long-term plans along with realistic KPIs and to disclose their efforts on an annual basis based on internationally recognized disclosure frameworks. We highlight several examples from our engagement in the next complete publication.

The complete publication, including footnotes, is available here.

Endnotes

1Bloomberg. September 13, 1991 – September 13, 2021.(go back)

2Bloomberg, as of September 28, 2021.(go back)

3Nihon Keizai Shimbun, “GAFA overtakes Japanese companies on market valuations as stable earnings invite inflows,” August 27, 2021.(go back)

4The World Bank World Development Indicators, as of September 13, 2021.(go back)

5Bloomberg. Fiscal year 2016 – September 13, 2021.(go back)

6Bloomberg. Return on equity, net profit margin of Topix, S&P 500, EURO STOXX 600, as of September 28, 2021.(go back)

7Bloomberg, as of September 28, 2021. Percentage of independent directors and female directors on the boards of Topix constituents.(go back)

8Government Pension Investment Fund, Report of the 6th Survey of Listed Companies Regarding Institutional Investors’ Stewardship Activities, 2021, p. 16.(go back)

9FactSet, SMBC Nikko Securities, as of August 2021. Historical Japan ESG ratings of MSCI Japan constituents.(go back)

10Value Reporting Foundation, SASB Standards Reporters, August 2021.(go back)

11Tokyo Stock Exchange, as of September 20, 2021. Japanese SASB Reporters excludes NTT Docomo, which was consolidated by parent company NTT.(go back)

12Japan Ministry of Economy, Trade and Industry, Japan’s Roadmap to “Beyond-Zero” Carbon” Report, November 11, 2020.(go back)

13Nihon Keizai Shimbun, “Pros and cons of strengthening disclosure within the context of climate change and finance,” September 16, 2021.(go back)

14Government Pension Investment Fund, ESG Report 2020, p. 40.(go back)

15Tokyo Stock Exchange, Development of Listing Rules for Cash Equity Market Restructuring (second set of revisions), December 25, 2020), p. 8 – 12.(go back)

16Tokyo Stock Exchange, Japan’s Corporate Governance Code: Seeking Sustainable Corporate Growth and Increased Corporate Value over the Mid- to Long-Term, June 11, 2020.(go back)

17Nihon Keizai Shimbun, “FSA debates climate change disclosure requirements on US and EU moves,” September 2, 2021.(go back)

18Nishiyama, Kengo, “Preview of the 2021 June AGM season and overview of the revised Japan Corporate Governance Code,” Nomura Securities investor presentation, May 19, 2021.(go back)

19Nihon Keizai Shimbun, “Companies’ emissions disclosure period to be shortened to a year, to include supply chain and operating companies,” September 13, 2021.(go back)

20Japan Ministry of Environment, Japan’s Domestic Efforts to Follow up on the Kyoto Conference, April 28, 1998).(go back)