Print

PrintDavid L. Portilla, David J. Kappos, Minh Van Ngo, Sasha Rosenthal-Larrea, John D. Buretta and Christopher K. Fargo are partners at Cravath, Swaine & Moore LLP. This post is based on a Cravath memorandum by Mr. Portilla, Mr. Kappos, Mr. Ngo, Ms. Rosenthal-Larrea, Mr. Buretta, Mr. Fargo, and Arvind Ravichandran.

I. Introduction

When interest in blockchain began to accelerate a few years ago, the expectations surrounding its uses were lofty. Blockchain was touted as technology that could fix our supply chains, our healthcare system and even our democracy. Yet, when the experiments conducted on potential blockchain applications, including pilot programs conducted in the financial services and banking industry, fell short of these expectations, industry interest in blockchain use cases waned. In some cases, those interested in blockchain technology found that traditional, centralized databases could provide the same functionalities as blockchain at a lower cost.

However, with the recent shift in the U.S. government’s attitude towards blockchain and cryptoassets, now is an opportune time for the U.S. financial industry to revisit the more mature, developed technology, using blockchain to improve existing products and services and offer new, more cost-effective products and services. Blockchains, both public and private, can be implemented across a variety of use cases in the financial world, opening up new sectors of banking services that benefit both banks and customers by allowing faster, cheaper, more secure and more inclusive transactions.

With a large pool of talent and a culture of innovation, the United States holds an advantage in resources available to develop blockchain solutions and spearhead the early deployment of blockchain-based products in the financial services industry. Blockchain technologies can provide a boon to the United States—but only with a combination of regulatory and private sector support. As new competition emerges internationally, with China pushing forward its digital yuan, the need for policy action to secure the United States’ lead in cryptoasset innovation is critical. Through collaboration across the public and private sectors to promote a technologically progressive regulatory environment, the United States can affirm its leadership position in blockchain development for the financial services industry.

Furthermore, through collaboration between financial services companies and regulators—and the development of standardized solutions—the entire financial services sector should be able to reap the rewards of this next-generation technology. Standardization of industry solutions through the use of both public and private blockchains can eliminate friction in transactions, reduce back-end costs and labor hours and dramatically increase transaction speed and security. In turn, the financial services industry will be able to expand its offerings, create new profit centers and provide new levels of service for customers both existing and heretofore unreached.

This post is divided by the potential applications of blockchain we consider to be most significant to the banking industry, including blockchain-based currency, lending and clearance and settlement systems. For each application, we make a distinction between potential use cases for public, permissionless blockchains that are decentralized (such as cryptoassets) and private, permissioned blockchains controlled by one or more entities. While exciting, this new landscape lacks clarity in key legal areas and, in this post, we aim to explore where the potential lies and what legal questions need to be resolved.

II. Applications

A. Blockchain-Based Currency

Blockchain technology is rapidly changing the way assets are transferred, stored and accounted for. Public and private blockchain-based currencies are being developed and utilized by private individuals, companies and even nation-states. These developments are signaling the early stages of an entirely new financial industry and the entrepreneurial opportunities that come with it. As the market capitalization and institutional support for cryptoassets grows, banks that develop the infrastructure for cryptoasset banking services (including custody, payment processing and lending offerings) will be well positioned to serve customers participating in this new and exciting asset class.

As more individuals and entities participate in the cryptoasset market, the ability to provide services dealing in cryptoassets will only grow in significance. The inherent difficulty and novelty of holding cryptoassets will likely solicit greater interest in having a trusted intermediary provide custody services. Outside of simply safeguarding these assets, as different forms of cryptoassets take hold, banks and regulators should prepare for the offering of other cryptoasset-based financial offerings.

Decentralized Cryptoassets

Given its unique monetary properties, including built-in durability, scarcity, fungibility, portability and divisibility, Bitcoin is quickly growing as a new store-of-value asset—similar to real estate or gold. The market for Bitcoin among individual investors has been growing for years. Recently, however, corporations have started adding Bitcoin to their balance sheets, some arguing that Bitcoin will help protect shareholder value from the effects of aggressive monetary policy around the world.

MicroStrategy, a software and data analytics business, was among the first major companies to invest in Bitcoin and has been perhaps the most aggressive corporate purchaser of Bitcoin. After converting large portions of its cash treasury into Bitcoin in the summer of 2020 and a subsequent series of debt offerings to acquire more Bitcoin, MicroStrategy now holds approximately 122,478 Bitcoins on its balance sheet. [1] Technology corporations such as Square and Tesla have followed suit. Square, a mobile payments company founded by Jack Dorsey, bought $50 million worth of Bitcoin in 2020 and an additional $170 million worth of Bitcoin in 2021. [2] Dorsey and Square CFO Amrita Ahuja both cited Bitcoin’s potential as native currency of the internet as a reason for the company’s purchase. [3] Similarly, in January 2021, Tesla disclosed that it had acquired $1.5 billion in Bitcoin as a treasury management strategy. [4]

This unique use case may spur demand for an entirely new suite of banking services similar to those offered for traditional currencies. Holders of Bitcoin and other cryptoassets may ask for crypto-based financial offerings such as customized exposure products, custody and trading solutions, credit lines, Bitcoin prime brokerage services, compliance solutions and more.

As a starting point, banks could issue simple derivatives such as cryptoasset swaps. These products could leverage banks’ institutional role as a trusted counterparty, while also allowing clients to gain exposure to cryptoassets of this sort. Banks also could directly step in to custody clients’ cryptoasset holdings. Mainstream industry players are already entering the space. Fidelity National Information Services is creating a product together with NYDIG, a Bitcoin-focused subsidiary of Stone Ridge Asset Management, that will allow banks to provide Bitcoin custody services. [5] Hundreds of banks have reportedly signed up for the product. [6]

Centralized Cryptoassets

In addition to the services that commercial banks can provide for decentralized cryptoassets, banks can provide similar services, such as custody or payment services, for centralized, blockchain-based cryptoassets or currency-like instruments, including stablecoins and central bank digital currencies (“CBDCs”).

Stablecoins are cryptoassets designed to have their value pegged to an external reference asset, such as a fiat currency. These new forms of traditional currencies have been growing in prominence and credibility, with the two most popular stablecoins, Tether and USD Coin (both pegged to the United States dollar), recently passing $50 billion and $25 billion in market cap, respectively. [7] Due to their targeted price stability, stablecoins are often viewed as a less risky alternative to other cryptoassets. While stablecoins bring the benefits of blockchain technology with faster settlement and programmability, stablecoins are also often centralized, with the issuing company maintaining control over the ledger and holding the ability to oversee and cancel transactions. As with decentralized cryptoassets, stablecoins represent opportunities for financial institutions that build the requisite infrastructure to provide an array of banking services. In November 2021, the President’s Working Group on Financial Markets (“PWG”), [8] the Federal Deposit Insurance Corporation (“FDIC”) and the Office of the Comptroller of the Currency (“OCC”) issued recommendations for the regulation of stablecoins, focusing on arrangements that are pegged to a fiat-currency. [9] The report recommended that Congress “promptly” pass legislation requiring that stablecoin issuers be insured depository institutions and providing federal agencies with significant regulatory authority over custodial wallet providers and other key participants in stablecoin arrangements. In the absence of congressional action, the report recommended that the Financial Stability Oversight Council (the “FSOC”) pursue its authority to designate certain activities conducted within stablecoin arrangements as systemically important payment, clearing and settlement (“PCS”) activities.

CBDCs are another growing trend, as central banks research and pilot their own digital currencies. CBDCs are digital payment instruments issued by a country’s central bank, akin to physical currency, but in digital form. The Central Bank of the Bahamas was the first to launch a digital currency when it deployed its digital Sand Dollar in October 2020. [10] China is piloting its digital yuan, in development since 2014, in Beijing and other cities. [11] According to a January 2020 report by the Bank for International Settlements, of 66 central banks surveyed, 80% responded that they were engaged in some sort of work with CBDCs, with 40% of them stating that they have progressed from conceptual research to actual proofs-of-concept and experimentation. [12] More than 88% of current CBDC projects utilize blockchain as the underlying technology. [13] China has recently taken the lead in promoting the worldwide development of CBDCs by proposing a global set of rules to govern information flows between central banks and encourage interoperability between CBDCs from different jurisdictions. [14] International interoperability and standardization could increase the opportunities available to banks that maintain the infrastructure necessary to handle these cryptoassets.

It is not clear how the rapid development of CBDCs will affect the current structure of the banking system. The Bank for International Settlements (“BIS”), in a chapter of its Annual Economic Report 2021, highlighted the importance of private sector involvement in a retail CBDC architecture and proposed potential alternatives for how such architectures could be modeled. [15] In a single-tiered direct CBDC architecture, the central bank would fully operate the system, including all associated operational and consumer-facing tasks, such as account maintenance and customer service. In a hybrid or intermediated CBDC architecture, the system would remain two-tiered, with the private sector playing its role in the operational and consumer-facing sphere. These two-tiered architectures can be distinguished based on the records kept by the central bank. In the hybrid model, the central bank would record retail balances, providing a backstop to the payment system, while in the intermediated model, the central bank would only record wholesale balances of individual payment service providers. The People’s Bank of China is experimenting with the two-tiered hybrid CBDC architecture system. [16] BIS has endorsed the two-tier system, noting that the single-tier system may detract from the central bank’s role as a “relatively lean and focused public institution at the helm of economic policy”. [17] In the near term, the Federal Reserve Board (“FRB”) is expected to release a long-awaited white paper on the “future of money”, covering CBDCs, stablecoins and other cryptoassets.

Legal Considerations

While recent regulatory guidance has provided insight and opportunity for financial institutions wishing to provide cryptoasset services, significant regulatory uncertainty remains. Financial institutions will need to work to ensure they are compliant with a rapidly evolving regulatory landscape and will need to build the necessary infrastructure to manage their public and private blockchain-based assets, services and activities.

In November 2021, the OCC published a letter by its Chief Counsel clarifying earlier interpretive letters issued under former Acting Comptroller Brian Brooks. [18] In 2020 and early 2021, under former Acting Comptroller Brian Brooks, the OCC opened the door to and signaled support for the expansion of banking services relating to cryptoassets and stablecoins by issuing guidance allowing national banks and federal savings associations to provide custody services for cryptoassets, including the safekeeping of cryptographic keys, [19] determining that banks that otherwise comply with applicable laws and regulations and conduct adequate due diligence are authorized to hold stablecoin “reserves” as a service to bank customers, [20] and clarifying the authority of national banks and federal savings associations to use stablecoins to conduct bank-permissible functions and to validate, store and record customer transactions by participating in independent node verification networks. [21] The interpretation published in November clarified that the activities addressed in these interpretive letters are legally permissible for a bank to engage in, provided the bank can demonstrate, to the satisfaction of its supervisory office, that it has controls in place to conduct the activity in a safe and sound manner. It also addressed prior guidance [22] regarding the OCC’s authority to charter a national bank that limits its operations to those of a trust company and related activities, by reiterating that banks must continue to comply with their existing obligations under the OCC’s fiduciary activities regulation and clarifying that the OCC retains discretion in determining whether an activity is conducted in a fiduciary capacity for purposes of federal law. In recent years, states, including New York, Wyoming and South Dakota, have passed legislation providing regulatory clarity and opportunity under state law for financial institutions interested in entering the space. Texas announced a similar authorization for state-chartered banks in June 2021. [23]

In 2020, the Securities and Exchange Commission (“SEC”) released a staff statement encouraging stablecoin issuers to engage with the agency in structuring token offerings to ensure compliance with federal securities laws, and noting that SEC staff is prepared to provide confirmation on an ad hoc basis that it will not take enforcement action against particular market participants with respect to specific digital tokens. [24] Relevant federal securities law regulations include the SEC’s Custody Rule, which provides additional requirements for the custody of cryptoassets that are deemed securities. [25] One such requirement is yearly independent audits, a practice that may be burdensome for custodians reluctant to expose private, cryptographic keys to third parties. However, practices relating to Proof of Reserves are being developed as a means of proving existence and control of cryptoassets to third-party auditors and customers without granting access to private keys. [26]

The Basel Committee on Banking Supervision (“BCBS”) recently issued a public consultation paper providing a proposed framework for prudential treatment of a bank’s cryptoasset exposure. This framework includes a division of cryptoassets into three categories: Group 1a, Group 1b and Group 2, with different risk-based capital requirements. A cryptoasset must meet a list of requirements to qualify as a Group 1a or Group 1b cryptoasset, with Group 1a including tokenized traditional assets and Group 1b potentially including stablecoins. Both Group 1a and Group 1b assets would be subject to capital requirements based on the risk weight associated with the applicable class of traditional assets underlying the cryptoasset as set out in the existing BCBS framework, plus consideration for additional technology-related risks. [27] Group 2 captures all cryptoassets not in Group 1, including most decentralized cryptoassets like Bitcoin, and would be subject to a 1250% risk weight that would apply to the absolute value of the aggregate long and short positions to which the bank is exposed. [28] An asset’s risk weight percentage is used to determine a bank’s risk weighted exposure to the asset which, when multiplied by its capital requirement percentage, determines the amount of capital the bank must hold to cover such exposure. This 1250% risk weight would ensure that banks hold risk-based capital at least equivalent to the value of the Group 2 cryptoasset they hold. Furthermore, the report emphasizes that banks that take on cryptoasset exposure should be subject to supervisory review processes to ensure that the bank has adequately assessed the risks relevant to the handling of cryptoassets. While the report is a preliminary proposal and specifically notes that finalizing the framework will be an “iterative process”, [29] its relatively punitive approach suggests regulatory skepticism and perhaps only a preliminary understanding of cryptoasset markets.

Finally, banks should consider compliance with sanctions regimes, including those set forth by the Office of Foreign Assets Control (“OFAC”). OFAC administers economic sanctions programs and promulgates regulations prohibiting transactions between individuals or entities in the United States with certain foreign individuals, entities or governments. In October 2021, OFAC published guidance for the cryptoasset industry (“October Guidance”), encouraging members of the industry to take a risk-based approach to sanctions compliance based on their specific circumstances, including the type of business involved, the products and services offered and the geographic locations served. [30] In addition to recommending certain tools, such as geolocation and IP address blocking controls, the October Guidance provides examples of “red flags” that companies handling cryptoassets should be on watch for, including customers that provide inaccurate or incomplete customer information when opening an account or when solicited for such information. [31] Just a few days after publishing the October Guidance, Deputy Secretary of the Treasury Wally Adeyemo requested additional funding from Congress to combat national-security threats, including such threats relating to cryptocurrency markets. [32] In addition, banks should be cognizant of the fact that OFAC has added virtual currency addresses to its Specially Designated Nationals and Blocked Persons List (“SDN List”). [33] Given OFAC’s increased focus on the space, banks must take an intentional approach in setting up their sanctions compliance programs to ensure the relevant risks are considered and addressed.

However, remaining in compliance with OFAC regulations will likely also require consideration of certain issues related to cryptoasset mining. [34] For example, banks will have to grapple with the fact that some miners on the network could be located in sanctioned countries, such as North Korea. Since these miners contribute to adding new blocks to the blockchain and provide network security in return for Bitcoin block rewards, there may be a concern that broadcasting a transaction could be construed as transacting with the miners themselves. Relatedly, banks may need to consider whether a particular cryptoasset that a bank is servicing was involved in a transaction with sanctioned entities or those specifically included on the SDN List.

While OFAC has not provided guidance on whether or how to address these sanctions issues, Marathon Digital Holdings (“Marathon”), one of the largest North American Bitcoin mining companies, recently launched what it has deemed as the first sanctions-compliant Bitcoin mining pool. By utilizing software that draws information from the SDN List and other sources on the dark web, Marathon’s pool filters out certain transactions in an attempt to ensure that only OFAC-compliant transactions, those not involving known or suspected nefarious actors, are included on each block. [35] While Marathon recently backtracked on this mining process due to backlash from the crypto-community over censorship, the effort provides an example of how mining pools may implement compliance protocols in the future. By utilizing trusted mining pools located in specific locales, banks could ensure that their transaction fees are not rewarding sanctioned miners and, if required by more extreme future regulations, could eventually work towards only handling Bitcoins used by non-sanctioned individuals.

Banks should also carefully consider tax consequences associated with cryptoassets. Unfortunately, these consequences are subject to substantial uncertainty. Most jurisdictions, including the United States, treat cryptoassets as a form of property rather than as currency. [36] As a consequence, using cryptoassets as a medium of exchange typically requires payment of immediate tax on the gain inherent in the cryptoassets. Beyond this basic premise, a great deal remains unresolved. For example, the treatment of cryptoassets under the various mark-to-market taxation regimes banks are often subject to is unclear, as is the tax treatment of swaps and other financial instruments involving or relating to cryptoassets. [37] There is limited guidance on issues that are unique and necessary to the functioning of cryptoassets, such as hard forks, and this guidance is not always favorable or easy to apply. [38] Finally, there is uncertainty regarding the application of valued-added taxes, property taxes and bank taxes (such as potential capital taxes) to cryptoassets. [39] Although tax authorities will continue to clarify cryptoasset taxation, it is likely uncertainty will persist for a considerable time .

B. Blockchain and Lending

Blockchain-based lending can provide a secure way of offering loans to an inclusive pool of consumers and can lower costs for all parties. There are two principal manners of involving blockchain in the lending process. The first is to use blockchain-based products as collateral in lending (e.g., cryptoassets). The second is to develop and use blockchain solutions to streamline the lending process.

Crypto-Collateralized Lending

One of the fastest growing applications of blockchain fintech is in the crypto-collateralized lending space. A crypto-collateralized loan is exactly what it sounds like— a loan collateralized by cryptoassets. There are numerous platforms providing centralized (bank-to-borrower) or decentralized (peer-to-borrower) crypto-collateralized loans. [40] As collateral, publicly traded cryptoassets like Bitcoin offer a variety of benefits for lenders. Bitcoin holdings with respect to any borrower can be verified much like investment assets, and the value of such holdings is easily ascertainable based on market prices. In a credit event, the collateral can be cheaply liquidated. In contrast to physical collateral (like equipment or real property), lenders can track or control the use of the collateral, as each Bitcoin is uniquely identifiable and each transaction publicly available. Finally, with new advancements in banking regulations, banks can now hold custody of cryptoassets, [41] which substantially reduces the lender’s risk when collateralizing loans with such assets.

The attributes listed above for cryptoassets as collateral may not seem unique, but the opportunities provided to the financial industry certainly are. The new asset class has unlocked new markets of borrowers. First, lenders now have more transparency into collateral when lending across borders. Rather than attempting to determine value of collateral, such as real property, that only has localized value (and, perhaps, requires costly currency exchange as well), cryptoassets can be evaluated and liquidated uniformly across the globe at any time and any day of the year. This allows lenders to programmatically assess the value of collateral assets of a borrower in real time over the course of a loan. Additionally, it reduces the challenges of enforcing liens across borders, which can be challenging in many jurisdictions. If a lender negotiates to take custody of the collateral, such collateral transparency can be even more advantageous, as the costs and challenges of enforcing liens across borders are virtually eliminated. Lenders can now afford to loan to borrowers in markets that were previously unreachable due to foreclosure and valuation risks. That means increased access to capital for more individuals globally, particularly in underbanked areas, where local laws and localized assets often preclude opportunities for debt. Further, the accessibility of cryptoasset collateral benefits lenders and borrowers alike by reducing the need for costly credit checks of limited benefit.

A number of legal challenges exist for lenders of crypto-collateralized loans. The first and most prominent is the difficulty of perfecting an interest in cryptoassets. Currently, there is much debate over how cryptoassets such as Bitcoin fit into the Uniform Commercial Code, relied on in the United States for perfecting and prioritizing assets. Bitcoin can be said to be money, investment property, a commodity or even a general intangible. Each of these has different procedures for perfection, and choosing one or the other could risk a lender’s priority if the choice proves incorrect. Further, while holding custody of the collateral can ease concerns over perfecting an interest in such collateral, there is not uniform clarity across regulatory authorities as to banks that may hold custody of cryptoassets. A single, uniform approach to perfection of cryptoassets collateral and rules regarding bank custody of cryptoassets is essential to allowing more people more access to capital.

Private Blockchain Process Solutions

Private blockchains also offer opportunities for banks to make it easier for capital to flow from creditors to debtors. Private blockchains can pave the way for smoother access to capital through standardization of the lending process across the industry and the use of verified documentary records by all participants in a lending network. Unlike the widely publicized public blockchains such as Bitcoin, private blockchains allow participants more control over the rules of the blockchain, permit authorization of users before they are allowed to participate on the blockchain (i.e., permissioned blockchains) and can require identification for participants.

Private blockchains operate by restricting access to the network through certain permission controls. Specific access controls limit the participants to the blockchain, and therefore who can view information on the network, contribute to the network or have knowledge of the transactions that take place on the network. By limiting the participants to the network, private blockchains also allow for greater governance over the network as agreement to certain contractually binding terms can be a prerequisite to access.

Requirements imposed on lenders by Anti-Money Laundering (“AML”) and Bank Secrecy Act regulations require time and process that adds to the time necessary for funds to flow from creditors to debtors as lenders. Tax reporting and information collection requirements, such as U.S. FATCA and the OECD’s Common Reporting Standard, create similar frictions. [42] Private blockchain solutions can reduce the costs associated with these requirements and increase speed by allowing lenders to store debtor information, or an encrypted version of that information, on private blockchains, which can be refreshed and updated over the course of repeat interactions and shared amongst approved lenders.

While blockchains generally allow participants to store and create a permanent and verifiable record of information (ledgers) necessary to the lending process, private blockchains enhance the security of the network’s information through security protocols and access restrictions. Documents and records of transactional interactions stored on the blockchain, or accessible through it, can then be readily accessible to the pool of lender-participants approved to use the network, for instance a syndicate lending group, with more immediacy, and less risk of information asymmetry, than legacy processes allow.

Once data is stored on the blockchain, that data becomes tamper-proof and unchangeable, except in accordance with the network’s consensus rules. Thus, once debtor information relating to regulatory compliance demands is approved by the lender-participants for inclusion on a block, it becomes immutable and any future iterations of that information can be compared to an as-agreed accurate baseline that cannot have been altered without the blockchain participants’ agreement and recordation of such change. Therefore, any new data layered on a block can be more easily reviewed and confirmed as accurate by participants through comparison to a previously confirmed iteration of that information, in accordance with the relevant consensus requirements. This iterative trail of information on the blockchain, along with ease of comparability, streamlines data requests and reviews, and helps to combat fraud.

Outside of the banking context, developers are working on blockchain solutions to address consumer identity-verification and documentation issues. [43] However, banks have greatest access to customer information required through know-your-customer (“KYC”)- or AML-type processes involved in lending, meaning they are also very well positioned to take advantage of the opportunity that blockchain offers and develop the next generation of lending mechanisms. Furthermore, while the solutions coming to market revolve around public blockchains, new data regulations, such as General Data Protection Regulation in the United Kingdom and the California Consumer Privacy Act, present data protection issues that public blockchains have yet to solve. These data privacy laws provide users with greater rights over the management of their information, including rights to deletion and rectification of personal information, which could fundamentally contradict the immutable nature of information on public blockchains. [44] Private blockchains, on the other hand, offer the possibility of creating limited-access networks where consensus as to the rules and thus as to changes to the blockchain becomes more manageable. Banks, as established market participants, sit in an advantageous position to employ private blockchains to implement new lending solutions while ensuring compliance with data privacy regulations. Furthermore, banks have the capability to develop private blockchain solutions for lending to corporate clients for whom data privacy regulations are less stringent. Upon gaining expertise in the corporate lending market, banks can leverage this experience in the consumer credit market.

Because private blockchains, like their public counterparts, still require consensus agreement mechanisms, their implementation would also pave the way for information standardization. Lending approval processes currently operate as independent workstreams among all counterparties to a loan. In loan transactions involving a syndicate of lenders, data requests can often vary for the same or similar information. This not only increases the number of documentary requests sent to debtors and the amount of work required of debtors to provide the requested information, but also increases the cumulative effort on the part of lenders to retrieve and process such information. As information added to a blockchain first requires authentication by the parties to it, these solutions operate best in an environment where all parties request and are able to process the same information. Therefore, as private blockchains are developed in the lending space, advance agreement between the participants as to what information is required and how it is to be presented for addition to the chain can reduce effort duplication across institutions and reduce the demands on debtors and the lending system as a whole.

Private blockchains can also be used on the transactional side of lending as solutions in transferring funds, tracking disbursements and payments and monitoring compliance with covenants, especially when made interoperable with cryptoassets and stablecoins. The ledger characteristic of blockchains can be used by lending parties to track every interaction between lender and debtor. Future interactions with a debtor (i.e., new loans or new disbursements) can also be recorded on the blockchain to keep a running ledger of transactions with that party. In this manner, private blockchain solutions can enable loan counterparties to seamlessly track the ongoing status of an individual loan. As future interactions between debtor and lender on a private blockchain network can be recorded on the blockchain, complete information can be made available to prior lenders regarding that debtor’s current borrowing activities simultaneous to them engaging in new transactions. This continuous feed of transactional information increases transparency in the lending space while reducing reporting burdens on borrowers to notify lenders, under existing agreements, of new transactions.

C. Clearance and Settlement Systems

Blockchain networks are beginning to enable transactions—even complex, cross-border, multi-party transactions—to clear within seconds, 24 hours a day, with dramatically reduced fees. These developments have the potential to fundamentally reshape how people transfer money and property.

The costs associated with settlement are especially pronounced with international transactions, where average transaction fees for cross-border payments are over 10% with an average clearance period of two to three days. [45] In contrast, blockchain networks, with their enhanced settlement features, should provide the ability for users to transact instantly with final settlement at nearly zero cost. These features provide the potential to make previously unthinkable applications, such as real-time streaming of cross-border payments and instant settlement of financial products, commonplace in the near future.

Blockchain networks not only present a significant opportunity for financial service providers, but also represent a major step forward for financial inclusion and human rights. By dissolving the financial barriers between developed and developing nations and offering a low-cost network of frictionless international payments, blockchains have the potential to bring financial services to billions of people who would otherwise be left behind. A large percentage of international payments involve migrant workers who transfer remittances to low- and middle-income countries. Blockchain networks can provide relief to these individuals who need it most.

Public Blockchains

Public blockchains, such as Bitcoin, are quickly demonstrating their potential as future settlement layers for large transaction volumes. While blockchains were initially limited to only a few transactions per second, recent developments in Layer Two technologies, such as the Lightning Network, have increased the throughput of public blockchains by several orders of magnitude, with theoretical upper bounds of over 1,000,000 transactions per second. [46]

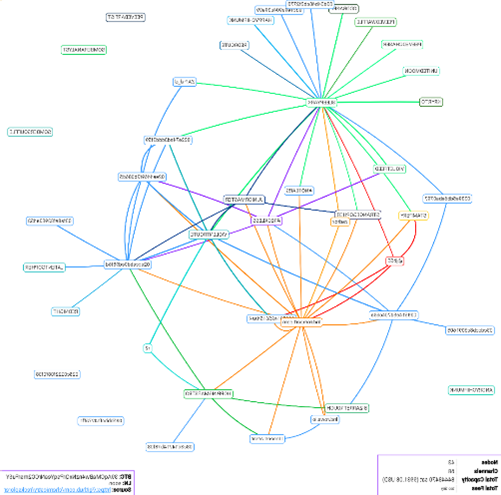

Growth of the Lightning Network 2018-2021

The Lightning Network, a network of payment channels built on the Bitcoin blockchain, allows users to create peer-to-peer payment channels anchored into the underlying blockchain, and then route payments over its secondary network layer. Using this secondary network, a user can send a payment for final settlement within seconds and at nearly zero cost while maintaining the same level of cryptographic assurance present at the base layer blockchain. [50] The topology of this payment channel network resembles that of the internet and could be the beginning of a new internet of money, where payments can be streamed in real time much like data packets are today.

Companies and developers are building state-of-the-art settlement platforms to take advantage of this new technology. For example, payment processors such as Strike and OpenNode offer payment and point-of-sale Bitcoin services. By using the Lightning Network as their backend infrastructure, these applications function similarly to PayPal’s Venmo and Square’s Cash App; however, users are able to transfer funds to any other Bitcoin wallet, regardless of the service provider. This level of interoperability is unprecedented for settlement systems and could spark a transition to open and interoperable financial protocols.

The Lightning Network’s Layer Two settlement technology has recently made headlines in Central America. In June 2021, El Salvador passed a bill designating Bitcoin as legal tender and later announced the creation of a new digital wallet named “Chivo” for its citizens. Chivo is a mobile application that will use the Lightning Network to send payments from one user to another instantly and at near zero cost anywhere in the world.

Private Blockchains

In contrast to permissionless, public blockchains, entities such as financial institutions and governments can also create blockchain-based networks aimed at facilitating asset transfers and information flow on a global scale.

One example of such a network is the recently debuted Liink by J.P. Morgan. [51] With more than 400 financial institutions from 78 jurisdictions having signed letters of intent to join the Liink system—of which approximately 100 are live today [52]—Liink provides a glimpse into how future private blockchains may operate.

Using a distributed ledger and public-private key cryptography, Liink enables “financial institutions and corporate users to make secure, peer-to-peer data transfers with greater speed and control”. [53] By facilitating information exchanges in near real time between a network of banks, Liink allows cross-border remittances to take place more efficiently. [54] True to blockchain’s primary objective of decentralization, Liink also enables participants to build applications on the network, with the potential to expand regional expertise into global influence. [55]

Other examples of private blockchains include Amazon Managed Blockchain and Elements-based sidechains (separate blockchains that are attached to their parent blockchain using a cryptographic two-way peg) such as Liquid. Specifically for financial entities, Amazon Managed Blockchain allows parties to trade and process related paperwork (i.e., ISDA agreements) in a matter of seconds without the need for a centralized authority, adding long overdue efficiency to a process that often takes days. [56] Liquid, a sidechain-based settlement network for traders and exchanges of Bitcoin, enables “faster, more confidential Bitcoin transactions and the issuance of cryptoassets” such as securities. [57] Liquid is operated by its members—large financial services entities that benefit from its use—without the need for a centralized figure. [58]

These types of networks present many advantages compared to today’s common siloed and centralized databases. First, they enable easier compliance with regulatory requirements, including sanctions regimes. Liink’s first application, “Resolve”, is focused on remedying sanctions exceptions that occur in cross-border transactions, reducing the operational tasks involved in verifying names and addresses “from weeks to minutes”. [59] Second, they enable easier validation of bank information prior to transmitting payments, lowering the costs associated with rejected transactions, particularly international ones. Liink’s feature, “Confirm”, allows users to validate account information prior to initiating a payment in near real-time. [60] In addition, “Format” helps to ensure that payment messages align with relevant country and currency requirements. [61]

Legal Considerations

While blockchain-based settlement technology continues to progress, recent developments also bring a new set of legal issues as traditional regulatory regimes are applied to this emerging field.

First, new settlement systems could conflict with status quo regulations relating to money service businesses and money transmission licenses. Under today’s regulatory regime, businesses responsible for sending or receiving money on behalf of a third party are required by the Financial Crimes Enforcement Network (“FinCEN”) and state authorities to register as money transmitters. [62] At the state level, different regimes vary, but are generally focused on consumer protection and ensuring the solvency of the transmitter who maintains custody of a customer’s funds. At the federal level, FinCEN is primarily concerned with surveilling a customer’s private information (KYC requirements) to prevent money laundering and terrorist financing.

For many cryptoasset businesses it is readily apparent how and why these rules apply. For example, cryptoasset exchanges are centralized businesses that regularly process customer transactions and hold funds on behalf of customers. As a result, American and even international exchanges (e.g., Binance) have recently instituted standard KYC and AML policies without significant difficulties. [63]

However, blockchain settlement innovation also brings a series of novel business and transaction structures that do not neatly fit under the traditional definition of a money transmitter. For example, Lightning Network routing nodes routinely route payments on behalf of a third party and even receive a fee in consideration for their work; however, the cryptographic structure of the network is such that routing nodes cannot know the sender or the recipient of the transactions they process. [64] Furthermore, routing nodes never take custody of a user’s funds. [65] Similarly, decentralized exchanges, such as Uniswap and PancakeSwap, allow users to trade cryptoassets without a centralized order book or a trusted third party to execute their trades. Instead, all trades are executed by a series of smart contracts found on a blockchain network such as Ethereum or Solana.

There are key tax considerations and opportunities here also, primarily related to tax reporting. In the first place, tax laws generally impose substantial reporting obligations on intermediaries such as banks. [66] These include the collection of customer information, and reporting as to transactions involving property held by the bank or for which the bank acted as a broker. It is conceivable the use of blockchain can substantially improve the efficiency of these operations, which have often been built up piecemeal on top of unrelated systems, by leveraging the technology inherent in the clearance system and by integrating these requirements into the technology at an earlier stage. In addition, governments continue to impose more significant and onerous reporting obligations tied to blockchain generally and cryptoassets specifically. One example is Section 80603 of the Infrastructure Investment and Jobs Act. This requires all “brokers” to collect annual activity information from users and report such information to the IRS. However, “broker” is broadly defined and could be interpreted to apply to many network participants such as miners, validators and developers who do not have access to the identity of cryptocurrency users, yet effectuate transfers for the network. [67] It will be critical for banks to ensure their ordinary operations comply with the existing rules as well as regulations and guidelines with respect to new rules, and the potential of a “ground-up” system built for compliance is likely to be significant.

These recent developments highlight the blockchain industry’s strides in the past decade and also demonstrate that authorities may have to reconsider their earlier positions. Addressing tensions surrounding cryptoasset settlement in the coming years will be crucial in determining whether the United States remains as a center for blockchain innovation.

III. Conclusion

With significant blockchain-based opportunity available to the financial services industry, the time is now for the industry and the governmental authorities to work together in facilitating widespread adoption of blockchain technology in a safe and sound manner and with robust consumer protections. While the wait-and-see approach generally taken in the past may have been necessary given how novel the technology was at the time, blockchain has since matured to the point where there is an urgent need for action. As other countries promote and develop blockchain use cases, especially in the financial services industry, private entities in the United States must continue to explore the benefits of blockchain technology and deploy it in practical marketplace solutions, and should be allowed to do so under a clearly delineated regulatory framework that does not preclude the advancement of this new technology.

Recent remarks from SEC Chair Gary Gensler, Federal Reserve Chairman Jerome Powell and other government officials, including officials at the U.S. Department of the Treasury and the OCC, and the report on stablecoins published by the PWG make clear that cryptoassets and blockchain are on the forefront of the minds of regulators concerned about financial stability, investor protection and market integrity. In November 2021, the federal banking agencies issued a brief statement outlining cryptoasset-related issues that the agencies will continue to address throughout 2022, including the safety and soundness expectations with respect to such activities. [68] Banks are well placed to address these concerns. With a history of acting as trusted intermediaries, banks can provide confidence and protection to customers and investors in the space.

Importantly, the benefits of blockchain implementation in the financial services industry will be shared by all stakeholders, including financial institutions themselves and the general public. With the potential to lower the costs associated with financial services, including through collaboration between financial institutions and through standardized processes across the industry, blockchain technology can provide broader and more uniform access to otherwise financially excluded individuals. By creating trust between third-party entities and facilitating information transfer through means that did not previously exist, blockchain can enable collaboration between financial institutions and strengthen the banking industry’s role as a trusted intermediary.

There is a historic opportunity for the banking industry to modernize dramatically by incorporating both public and private blockchains in banking services. Through a combination of appropriate governmental regulation and partnerships between the public and private sectors, the legal uncertainties prevalent in the space can be clarified and the banking industry in the United States can expand its use of blockchain technology to provide more efficient and secure products and services to new and existing customers. Now is the time to realize this opportunity in the United States.

Endnotes

1See Sheldon Reback, MicroStrategy Says It Bought 1,434 Bitcoins Since Nov. 29, CoinDesk (Dec. 9, 2021), https://www.coindesk.com/business/2021/12/09/microstrategy-says-it-bought-1434-bitcoins-since-nov-29/.(go back)

2See Nick Chong, Jack Dorsey’s Square Purchases $50 Million Worth of Bitcoin, Forbes (Oct. 8, 2020), https://www.forbes.com/sites/nickchong/2020/10/08/jack-dorseys-square-purchases-50-million-worth-of-bitcoin/?sh=282a2182386a; see also Kevin Helms, Square Adds $170 Million More in Bitcoin to Balance Sheet — Company Now Holds 5% of Total Cash Reserves in BTC, Bitcoin (Feb. 24, 2021), https://news.bitcoin.com/square-170-million-bitcoin-5-total-cash-reserves-btc/.(go back)

3See Chaim Gartenberg, Twitter CEO: Bitcoin will be the world’s ‘single currency’ in 10 years, The Verge (Mar. 21, 2018), https://www.theverge.com/2018/3/21/17147574/twitter-ceo-bitcoin-jack-dorsey-square-interview-currency-10-years; see also Square, Inc. Invests $50 Million in Bitcoin, Square (Oct. 8, 2021), https://squareup.com/us/en/press/2020-bitcoin-investment.(go back)

4See Arjun Kharpal, Tesla has made about $1 billion in profit on its bitcoin investment, analyst estimates, CNBC (February 21, 2021), https://www.cnbc.com/2021/02/22/tesla-has-made-1-billion-profit-on-its-bitcoin-investment-analyst.html.(go back)

5See Kim Snider, Bitcoin in Your Bank Account? FIS, NYDIG Partner to Enable Banks to Offer Their Customers the Ability to Buy, Sell and Hold Bitcoin, Business Wire (May 5, 2021, 8:00 AM), https://www.businesswire.com/news/home/20210505005025/en/Bitcoin-in-Your-Bank-Account-FIS-NYDIG-Partner-to-Enable-Banks-to-Offer-Their-Customers-the-Ability-to-Buy-Sell-and-Hold-Bitcoin.(go back)

6See Hugh Son, Bitcoin is coming to hundreds of U.S. banks this year, says crypto custody firm NYDIG, CNBC (May 5, 2021, 2:43 PM), https://www.cnbc.com/2021/05/05/bitcoin-is-coming-to-hundreds-of-us-banks-says-crypto-firm-nydig-.html.(go back)

7See Jamie Crawley, Tether Passes $50B Market Cap, Coin Desk (Aug. 24, 2021, 4:05 PM), https://www.coindesk.com/markets/2021/04/26/tether-passes-50b-market-cap/.(go back)

8The PWG is chaired by the Secretary of the Treasury and includes the Chairs of the FRB, SEC and Commodity Futures Trading Commission (“CFTC”).(go back)

9PWG, FDIC, and OCC, Report on Stablecoins, available at https://home.treasury.gov/system/files/136/StableCoinReport_Nov1_508.pdf.(go back)

10See Sebastian Sinclair, Central Bank of Bahamas Launches Landmark ‘Sand Dollar’ Digital Currency, Coin Desk (Aug. 24, 2021, 7:00 PM), https://www.coindesk.com/markets/2020/10/21/central-bank-of-bahamas-launches-landmark-sand-dollar-digital-currency/.(go back)

11See Arjun Kharpal, China to hand out $6.2 million in digital currency to Beijing residents as part of trial, CNBC (June 2, 2021, 12:20 AM), https://www.cnbc.com/2021/06/02/china-digital-currency-beijing-to-hand-out-6point2-million-in-trial.html.(go back)

12See Codruta Boar, Henry Holden & Amber Wadsworth, Impending arrival—a sequel to the survey on central bank digital currency, 107 BIS Papers, Bank for International Settlements (2020), https://www.bis.org/publ/bppdf/bispap107.pdf.(go back)

13PwC CBDC global index, PwC (1st ed. 2021), pwc-cbdc-global-index-1st-edition-april-2021.pdf.(go back)

14See Tom Wilson & Marc Jones, China proposes global rules for central bank digital currencies, Reuters (Mar. 25, 2021, 8:38 AM), https://www.reuters.com/article/us-cenbanks-digital-china-rules/china-proposes-global-rules-for-central-bank-digital-currencies-idUSKBN2BH2TA.(go back)

15See Bank for International Settlements, CBDCs: an opportunity for the monetary system, Annual Economic Report 2021 (June 29, 2021), available at https://www.bis.org/publ/arpdf/ar2021e3.pdf.(go back)

16Id. at 79.(go back)

17Id. at 78.(go back)

18OCC Interpretive Letter 1179 (Nov. 18, 2021).(go back)

19OCC Interpretive Letter 1170 (July 22, 2020).(go back)

20OCC Chief Counsel’s Interpretation on National Bank and Federal Savings Association Authority to Hold Stablecoin Reserves, available at https://www.coindesk.com/wp-content/uploads/2020/09/2020-125a.pdf (last visited September 29, 2020).(go back)

21OCC Interpretive Letter 1174 (Jan. 4, 2021).(go back)

22OCC Interpretive Letter 1176 (Jan. 11, 2021).(go back)

23See Cheyenne Ligon, Texas State Regulator Greenlights Banks to Custody Crypto, Coin Desk (Aug. 24, 2021, 3:34 PM), https://www.coindesk.com/texas-state-regulator-greenlights-banks-to-custody-crypto.(go back)

24See Public Statement from SEC FinHub Staff, SEC FinHub Staff Statement on OCC Interpretation, U.S. Securities and Exchange Commission (Sept 21, 2020), available at https://www.sec.gov/news/public-statement/sec-finhub-statement-occ-interpretation.(go back)

25Investment Advisors Act of 1940, 17 C.F.R. § 275.206(4)-2 (1940).(go back)

26See Sam Abbassi, et al., Proof of Reserves: The Practitioner’s Guide to an Emerging Standard for Increasing Trust and Transparency in Digital Asset Platform Services, Chamber of Digital Commerce (May 4, 2021), https://4actl02jlq5u2o7ouq1ymaad-wpengine.netdna-ssl.com/wp-content/uploads/2021/05/Proof-of-Reserves-.pdf.(go back)

27Consultative Document – Prudential treatment of cryptoasset exposures, Basel Committee on Banking Supervision—Bank for International Settlements, at 3 (June 2021), https://www.bis.org/bcbs/publ/d519.pdf.(go back)

28Id.(go back)

29Consultative Document – Prudential treatment of cryptoasset exposures, Basel Committee on Banking Supervision—Bank for International Settlements, at 1 (June 2021), https://www.bis.org/bcbs/publ/d519.pdf.(go back)

30See Office of Foreign Assets Control, Sanctions Compliance Guidance for the Virtual Currency Industry (Oct. 15, 2021), https://home.treasury.gov/system/files/126/virtual_currency_guidance_brochure.pdf.(go back)

31Id.(go back)

32Mengqi Sun & Ian Talley, Treasury Seeks More Money for Illicit-Finance Oversight, Including Crypto and Cybercrime, The Wall Street Journal (Oct. 19, 2021), https://www.wsj.com/articles/treasury-seeks-more-money-for-illicit-finance-oversight-including-crypto-and-cybercrime-11634692030.(go back)

33See Harry Clark, et al., Cryptocurrency and OFAC: Beware of the Sanctions Risks, JDSupra (Jan. 24, 2020), https://www.jdsupra.com/legalnews/cryptocurrency-and-ofac-beware-of-the-34002/.(go back)

34See Britt Mosman, et al., OFAC Sanctions Considerations for the Crypto Sector, Willkie Farr & Gallagher LLP at 6 (Aug. 17, 2021), https://www.willkie.com/-/media/files/publications/2021/08/ofacsanctionsconsiderationsforthecryptosector.pdf.(go back)

35See Marathon Digital Holdings to Launch the First North American-Based Bitcoin Mining Pool, Fully Compliant with U.S. Regulations, Globe News Wire (Mar. 30, 2021), https://www.globenewswire.com/news-release/2021/03/30/2201918/0/en/Marathon-Digital-Holdings-to-Launch-the-First-North-American-Based-Bitcoin-Mining-Pool-Fully-Compliant-with-U-S-Regulations.html.(go back)

36IRS Notice 2014-21, 2014-16 I.R.B. 938. Even this may develop further as countries begin to accept cryptoassets as legal tender. For example, El Salvador recently began to accept Bitcoin as legal tender. See Oscar Lopez and Ephrat Livni, In Global First, El Salvador Adopts Bitcoin as Currency, The New York Times (Sept. 7, 2021), https://www.nytimes.com/2021/09/07/world/americas/el-salvador-bitcoin.html?referringSource=articleShare.(go back)

37See, e.g., IRC §§ 475, 1256. For example, it is not clear whether cryptoassets are commodities or securities for tax purposes.(go back)

38See Rev. Rul. 2019-24; CCA 202114020; IRS, Frequently Asked Questions on Virtual Currency Transactions (June 4, 2021), https://www.irs.gov/individuals/international-taxpayers/frequently-asked-questions-on-virtual-currency-transactions.(go back)

39OECD, Taxing Virtual Currencies: An Overview of Tax Treatments and Emerging Tax Policy Issues 32-40 (2020).(go back)

40These services are currently predominantly offered by new players in the lending space that are solely focused on crypto-related product offerings (see, e.g., BlockFi, https://blockfi.com/crypto-loans/ (last visited Sept. 13, 2021); SebaBank Crypto-collateralized Lending, https://www.seba.swiss/trading-and-credit-solutions/credit (last visited Sept. 13, 2021)).(go back)

41Interpretive Letter 1170, supra note 16.(go back)

42See IRC §§ 1471-1474 (FATCA); OECD, Standard for Automatic Exchange of Financial Information in Tax Matters (2d ed. 2018), https://www.oecd.org/tax/exchange-of-tax-information/implementation-handbook-standard-for-automatic-exchange-of-financial-information-in-tax-matters.pdf (CRS).(go back)

43See, e.g., Civic Technologies, Inc. White Paper (2017), https://tokensale.civic.com/CivicTokenSaleWhitePaper.pdf.(go back)

44For a complete discussion of the problems posed by GDPR compliance in the blockchain context, see David Kappos, Shawn Muma and Rob Sumroy, The Right to be Forgotten Meets the Immutable: A Practical Guide to GDPR-Compliant Blockchain Solutions, Center for Global Enterprise, Cravath, Swaine & Moore LLP and Slaughter and May (2020).(go back)

45See Sam Klebanov, A Look at Blockchain in Cross-Border Payments, Payments Journal (Feb. 5, 2021), https://www.paymentsjournal.com/a-look-at-blockchain-in-cross-border-payments/.(go back)

46See Joseph Poon & Thaddeus Dryja, The Bitcoin Lightning Network: Scalable Off-Chain Instant Payments (2016), https://www.lopp.net/pdf/lightning-network-paper.pdf.(go back)

472018, source: https://github.com/chemicstry/recksplorer.(go back)

482019, source: https://www.reddit.com/r/Bitcoin/comments/8cv5hi/i_dont_know_guys_but_this_lightning_network_is/(go back)

492021, source: https://lightninglayer.map.(go back)

50See Joe Kendzicky, The Bitcoin Lightning Network: A Technical Primer, Medium (Jun. 5, 2018), https://medium.com/@jkendzicky16/the-bitcoin-lightning-network-a-technical-primer-d8e073f2a82f.(go back)

51JPMorgan Liink, https://www.jpmorgan.com/onyx/liink.htm (last visited Sept. 13, 2021).(go back)

52See JPMorgan Uses Liink Network To Help FIs Innovate Payments Economics, Pymnts (Mar. 30, 2021), https://www.pymnts.com/blockchain/2021/jpmorgan-uses-liink-network-to-help-fis-innovate-payments-economics/.(go back)

53JPMorgan Liink, supra note 47.(go back)

54Pymnts, supra note 48.(go back)

55See Ian Allison, JPMorgan Invites Banks and Fintechs to Build on Its Revamped Blockchain Network, NASDAQ (Oct. 28, 2020, 12:00 AM), https://www.nasdaq.com/articles/jpmorgan-invites-banks-and-fintechs-to-build-on-its-revamped-blockchain-network-2020-10-28.(go back)

56Amazon Managed Blockchain, https://aws.amazon.com/managed-blockchain/ (last visited Sept. 13, 2021).(go back)

57Blockstream, https://blockstream.com/liquid/ (last visited Sept. 13, 2021).(go back)

58Technical Overview, Blockstream (last visited Sept. 13, 2021), https://docs.blockstream.com/liquid/technical_overview.html.(go back)

59See Pymnts, supra note 48.(go back)

60See Allison, supra note 51.(go back)

61See India’s largest bank adopts JP Morgan’s payments blockchain Liink, Ledger Insights (Feb. 23, 2021), https://www.ledgerinsights.com/indias-largest-bank-adopts-jp-morgans-payments-blockchain-liink/.(go back)

62See Money Transmitter Licensing for U.S. Crypto Companies, Kelman Law (July 13, 2020), https://kelman.law/insights/money-transmitter-licensing-for-u-s-crypto-companies/.(go back)

63See Binance Expands Global KYC Requirements to Further User Protection, Binance (Aug. 19, 2021), https://www.binance.com/en/blog/421499824684902585/ecosystem/binance-expands-global-kyc-requirements-to-further-user-protection.(go back)

64Peter Van Valkenburg on Lightning & The Law, What Bitcoin Did (April 16, 2019), https://www.whatbitcoindid.com/podcast/peter-van-valkenburg-on-lightning-the-law.(go back)

65Id.(go back)

66See, e.g., IRC §§ 6045 (broker reporting), 6050W (reporting for payment processors).(go back)

67See Marcy Gordon, EXPLAINER: How cryptocurrency fits infrastructure bill, AP NEWS (Aug. 10, 2021), https://apnews.com/article/technology-joe-biden-business-bills-cryptocurrency-92628a41124230448f65fdeb89ffad7d.(go back)

68See, e.g., FRB, FDIC, OCC, Joint Statement on Crypto-Asset Policy Sprint Initiative and Next Steps (Nov. 23, 2021), available at https://www.federalreserve.gov/newsevents/pressreleases/files/bcreg20211123a1.pdf.(go back)