Print

PrintBob Moritz is Global Chairman at PricewaterhouseCoopers LLP. This post is based on PwC’s 25th annual CEO Survey.

As we near the two-year mark of the pandemic, the global economy has rebounded from the depths of mid-2020. The IMF projects [1] global GDP to grow 4.9% in 2022, a downtick from the 5.9% growth expected in 2021, but still formidable. The 4,446 CEOs from 89 countries and territories who responded to our 25th Annual Global CEO Survey display optimism about continued economic resilience.

Yet threats, uncertainties and tensions abound. The survey was in the field during the COP26 conference in Scotland, which convened world leaders to try to prevent the worst effects of climate change. PwC experts who attended were both impressed by executives’ commitment to rapid progress and aware that the captains of industry in Glasgow were a self-selected group that came prepared to take action. The question of how to bring others along looms large. Then, just two weeks after our survey closed, news of the Omicron variant reverberated around the world, raising fresh questions about the course of the pandemic and about society’s ability to continue the slow climb to normalcy.

Our survey findings reflect these and other tensions. For example, just 22% of survey respondents have made net-zero commitments (though the largest companies in our sample are further along). CEOs are most worried about the potential for a cyberattack or macroeconomic shock to undermine the achievement of their company’s financial goals—the same goals that most executive compensation packages are still tied to. And they are less concerned about challenges, like climate change and social inequality, that appear to pose smaller immediate threats to revenue.

But our survey also provides a glimpse of what is possible when we reimagine the status quo. A case in point: the power of trust. We found that highly trusted companies are more likely to have made net-zero commitments and to have tied their CEO’s compensation to nonfinancial outcomes, such as employee engagement scores and gender diversity in the workforce. Correlation is not causation, and we’ll continue to explore these results. But at first blush, they suggest a relationship between trust and the ability to drive change —a means of moving beyond short-term, “it’s the next leader’s problem” thinking.

It’s an apt finding to spotlight as we commemorate our 25th year documenting CEO sentiment toward and reactions to transformative trends. During the dot-com bubble in 1998, we talked to chief executives about technology, from their personal use of the internet to the future of e-commerce; in 2003, we tracked the rise of corporate governance and enterprise risk management in the wake of financial scandal. We’ve also surveyed CEOs in moments of crisis—in 2008, as the global financial system collapsed, and last year, as we approached the one-year mark of the pandemic—to gauge the impact on strategy and growth.

The challenges facing CEOs today are no less daunting. Increasingly, these leaders need to create sustained outcomes for multiple stakeholders whose interests are not always aligned. Yet the imperative to take decisive action has perhaps never been as strong. Business as usual isn’t mitigating the climate crisis or bridging the socioeconomic divide. The results of our 25th Annual Global CEO Survey lay these truths bare—and underscore the need for bold leadership to unite us as global citizens and problem solvers.

Near-term optimism

In aggregate, CEO optimism has remained stable, and high. When we surveyed chief executives in October and November of 2021, 77% said they expect global economic growth to improve during the year ahead, an uptick of one percentage point from our previous survey (conducted in January and February of 2021) and the highest figure on record since 2012, when we began asking CEOs how they felt about the economy’s potential.

Although it is unclear how the emergence of the Omicron variant will affect CEOs’ optimism, today’s headlines emphasise the asymmetrical nature of the world’s pandemic recovery [2] which our survey results also reflect. CEOs in Brazil, China, Germany and the United States report feeling less optimistic than they were a year ago that growth rates are poised to increase, whereas those in India, Japan and the UK are even more optimistic than they were early last year. These differences may simply reflect where CEOs see themselves in the economic cycle. China and the US, for example, rebounded ahead of the rest of the world and are now experiencing growing pains in the form of inflation, real estate bubbles and supply chain disruptions. Both countries are also confronting labour shortages. In China, shifting demographics and structural unemployment [3] are creating a growing gap; in the US, headlines about the ‘great resignation’ and early retirement [4] predominate.

More than half of CEOs also report high levels of confidence about their own prospects for revenue growth over the next 12 months. Most upbeat of all are CEOs of private equity firms (67% of whom are highly confident about their company’s growth) and technology firms (64%). Both sectors continue to benefit from large inflows of capital, thanks to the favourable financial conditions prevailing in most advanced economies. Among the CEOs expressing a more tepid outlook are those in the automotive (46%) and hospitality and leisure sectors (44%), which are grappling with semiconductor shortages [5] and the lingering effects of the pandemic on travel, respectively. It remains to be seen whether the pandemic trajectory will shift and present new constraints on some industries.

Sources of growth. Innovation fuels growth, and it’s often driven by small, nimble organisations. Over the past five and a half years, according to a new PwC study [6] of the global unicorn landscape, a total of 869 companies achieved the US$1bn valuation mark. Five innovation trends have emerged from this influx of funds, each of which is generating meaningful economic energy, should present opportunities for many larger companies, and may necessitate that established companies build or buy new capabilities. The five areas to watch are the platformisation of consumer financial services, the electric vehicle ecosystem and stored energy, the creation and expansion of the tech-enabled “metaverse,” the ongoing convergence of mobility and digital commerce, and the virtual evolution of health and wellness.

Threats to the top line

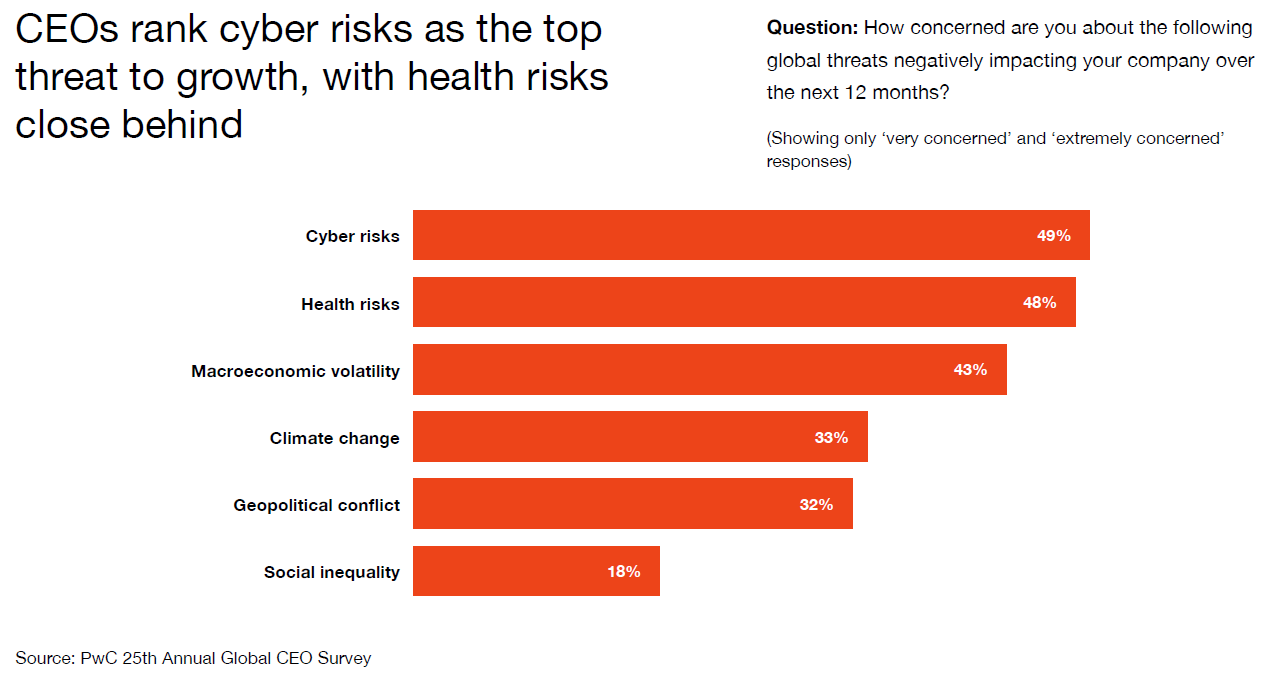

The threats that CEOs are most worried about and the impact they see those threats having on their business in the next 12 months reveal leaders under pressure to deliver top-line results.

Similar to last year, CEOs are most concerned about cyber risks (49%) and the global health situation (48%) as the pandemic lingers. Interestingly, CEOs in the manufacturing and consumer sectors displayed lower levels of concern about cyber risks (40% and 39%, respectively), despite those sectors’ high volume of cyber attacks. [7] Coming in a close third on the threat list for all CEOs is macroeconomic volatility, including fluctuations in GDP, unemployment and inflation.

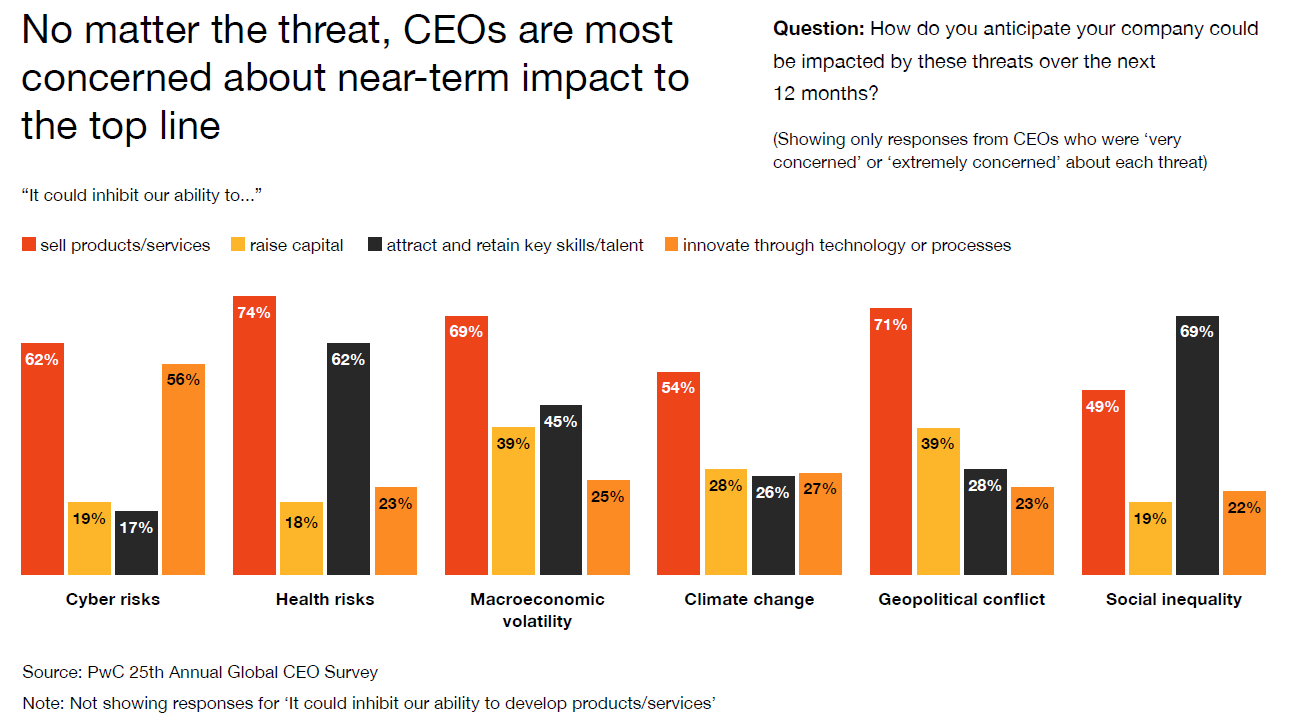

To understand what lies behind these views, we asked CEOs how they think each threat could inhibit their ability to achieve various business outcomes over the next 12 months. With the exception of social inequality, CEOs are most concerned about the potential of each threat to disrupt revenue. Thiraphong Chansiri, CEO of the Thailand-based global seafood company Thai Union Group, explains how inflation threatens sales: ‘Even if we can successfully pass on the costs, we expect that it might affect volume—that consumption may drop due to the high price.’

CEOs’ priorities may help explain the lower threat ranking given to social inequality, which is less likely to be tightly linked with sales and value creation over the 12 months we asked respondents to consider. Also low on the list of concerns is climate change; an exception here are CEOs of companies with revenues exceeding US$10bn, for whom it is the top threat. Other key findings: CEOs do not appear especially concerned about whether most of the threats analysed will inhibit their ability to raise capital. Concern over the ability to attract and retain talent is strongly linked in CEOs’ minds with health risks and social inequality. And many CEOs worry that cyber risks could inhibit innovation as well as sales. Leaders recognise the importance of these outcomes, but they may give them short shrift because of top-line pressures.

Cyber risks hit home. Juan Ricardo Ortega, [8] CEO of Grupo Energía Bogotá, Colombia’s largest natural gas transporter and second-largest energy transmitter, described a cyberattack against his company when his employees were working from home, despite the company’s purchase of protection equipment. ‘It happened while we were trying to implement our new defence system, and our staff was not fully trained yet,’ Ortega explains. ‘Fortunately, we managed to defend ourselves by shutting down the servers before the attackers accessed sensitive databases. In the end, we had an operational problem of only a few hours. But [it] was a wake-up call for us.’

Ortega is far from alone, according to PwC’s 2022 Global Digital Trust Insights Survey [9] of nearly 700 CEOs and 2,900 other C-suite executives. Yet despite myriad challenges, some organisations are starting to create a blueprint for the securable enterprise. They focus on establishing security and privacy as operational goals and business imperatives; hiring a chief information security officer; empowering this individual to create cross-functional teams; making cybersecurity part of other key decisions, such as acquisitions and product launches; and reducing complexity through steps such as vendor consolidation to minimise nodes of vulnerability.

Which outcomes matter?

The near-term value creation pressures that are driving CEOs’ most pressing concerns seem even more significant when we look at the outcomes CEOs are working toward—as articulated in their corporate strategies and reflected in their own compensation packages.

Most CEOs have goals related to customer satisfaction, employee engagement, and automation or digitisation included in their long-term strategy. These nonfinancial outcomes are intertwined with day-to-day business performance. Much less well-represented, in strategies and compensation, are targets related to greenhouse gas (GHG) emissions (13% of CEOs have these targets in their annual bonus or long-term incentive plan), workforce gender representation (11%) and racial and ethnic diversity (8%). The picture looks different in industries for which climate change presents a more direct, existential threat. For example, 30% of power and utilities CEOs have GHG emissions tied to their personal compensation, as do 27% of energy CEOs.

We also see a difference among CEOs of “high trust” companies. For the first time in our survey’s history, we asked CEOs about the nature of their engagement with customers across six dimensions of trust and aggregated those responses to create an index of perceived customer trust. It’s not yet clear which way the association runs or whether there is a mediating variable that explains the relationship. Still, these findings— which were normalised by industry and confirmed for independence from demographic characteristics such as the company location or size—seem important. For example, CEOs of companies ranking highest on our customer trust index are significantly more likely to have nonfinancial outcomes (such as customer satisfaction, employee engagement, and gender, race and ethnicity representation) tied to their compensation. In fact, the most highly trusted companies are 1.4 times more likely to have gender diversity targets in their chief

executive compensation plans.

Closing the say–do gap. Adding environmental, social and governance (ESG) metrics to executive pay packages can be a powerful way for a company to prove its commitment to these principles and to help elevate such metrics to the top of the CEO agenda. But as a recent PwC report makes clear, [10] pay follows strategy—it doesn’t drive it. ESG metrics need to be part of a company’s strategic priorities, which are then reinforced by incentives. In setting up this system, boards should factor in both internal targets, which the company uses to benchmark itself, and external targets, which are based on measures of stakeholder impact, and establish individual KPIs and scorecards. They’ll also need to determine whether it’s most appropriate to tie the metrics to the CEO’s long-term incentive plan or annual bonus.

The diverse paths to net zero

COP26 thrust the net-zero transition onto the global stage, adding to momentum that had already been building. For example, by March 2021, more than 2,150 businesses had signed on to the UN’s Race to Zero initiative [11], placing themselves, at minimum, at the starting line; as of December 2021, this number had grown to 4,475. But the reality is that achieving net zero (when a company reduces its greenhouse gas emissions to near zero and removes its remaining unavoidable emissions) will be exceedingly difficult for some companies and industries, and as a result there’s no single trajectory. We see this evidenced in our survey findings: just 22% of our respondents have made a net-zero commitment, which is consistent with research from the Energy and Climate Intelligence Unit and Oxford Net Zero. [12] An additional 29% of our survey respondents are working toward making a net-zero commitment.

When we take a closer look at the companies formally committed to decarbonisation, several interesting findings emerge. For one, the CEOs of companies that ranked highest on our customer trust index are significantly more likely to lead organisations that have made a net-zero commitment than the average company in our global sample.

Large companies are also highly represented: nearly two-thirds of those with revenues of US$25bn or more have made a net-zero commitment, compared to 10% of companies with revenues of less than US$100mn. And the public companies in our sample are more than twice as likely as the private companies to have made a net-zero commitment. These findings point to the oft-cited echo chamber phenomenon—the leaders of companies that understand the need to take dramatic action, which tend to be large in terms of both revenue and resources, are the most vocal and active.

At the sector level, among those that have made net-zero commitments, energy and power and utilities are the most highly represented. This reinforces the fact that high-emitting (and hard-to-abate) industries are often front and centre when it comes to climate action, placing them in the complex and critical role of being part of both the problem and its solution. Japan-based conglomerate Mitsubishi Corporation, which has a large energy business, is grappling with these issues head-on. ‘Japan is expected to cover about 40% of its energy demand with renewables,’ explains CEO Takehiko Kakiuchi. ‘Natural gas is vital for the remaining 60%, and while getting to a consensus around offsetting mechanisms is challenging, carbon-neutral LNG [liquefied natural gas] offers a promising solution.’ There are also questions about what will ultimately be both acceptable to other stakeholders and cost competitive. Nuclear power, the most economical option, is fraught. ‘In Japan, nuclear energy provides a veritable source of clean power, but innovative approaches to safety concerns are essential to overcome public opposition.’

Meanwhile, among CEOs of companies that have not made a commitment to achieve carbon neutrality—attained when a company offsets its greenhouse gas emissions to zero (for example, by purchasing voluntary carbon credits)—or a net-zero commitment, 57% indicate that they don’t think their company produces a meaningful amount of GHG emissions. CEOs from the technology (74%), business services (72%) and insurance (71%) sectors were most likely to place themselves in this category. Many of those companies may be focusing on their Scope 1 (direct) emissions and Scope 2 (indirect from the purchase of electricity, steam, heat or cooling) emissions, as opposed to Scope 3 emissions (those created through the use of their products and across the full value chain, including the contributions of suppliers and other partners). Scope 3 emissions are harder to quantify, and a large number of CEOs report that they lack both the ability to rigorously measure emissions and an established industry-wide approach for decarbonising—highlighting the need for reliable data and consistent processes.

Of the 24% of CEOs who are not confident that their company could fulfil a commitment, many represent sectors that contribute significantly to emissions, such as metals and mining, automotive, and real estate. In major cities, for example, the built environment can account for 70% of emissions. And as Christian Ulbrich, CEO of global real estate services company Jones Lang LaSalle, headquartered in the US, explains, ‘There is no easy solution for many buildings because of the way they are constructed—it is financially unattractive to try to decarbonise them.’ For building owners, this will only become increasingly problematic. ‘The speed with which financial institutions are declining to finance those buildings and investors and fund managers are deciding not to buy them is amazing. Soon we won’t be talking about the premium afforded by green buildings, but rather the discount for brown buildings. And we have far more brown buildings.’

Very few CEOs are avoiding commitments out of a belief that their stakeholders (internal and external) don’t care about climate change, or because they couldn’t afford to do it. That’s consistent with the perspective of CEOs who have made net-zero commitments: meeting customer expectations was the number two motivator identified by CEOs, behind only their overall desire to mitigate climate change risks. David Taylor, [13] chairman and former CEO of US-based consumer products company Procter & Gamble, is keenly aware of those rising expectations. ‘What has changed from, say, ten years ago is that the consumer now wants to know the values of the companies behind the brands they buy. That’s becoming increasingly important, especially for younger consumers,’ he says. ‘Moreover, what you need to do to be considered “good” at ESG has changed dramatically. Companies like ours need to have ambitious plans.’

Overcoming barriers to net zero. Separate PwC research on the economic realities of ESG [14] suggests that major investors are at least as frustrated as CEOs with the measurement, management and reporting challenges associated with decarbonisation. This survey of global asset managers found that a critical priority for leaders seeking to overcome these challenges is harnessing the full power of the C-suite. Unified senior leadership is necessary for environmental priorities to ‘cascade through the business,’ in the words of one analyst. It also contributes to breaking down silos between sustainability teams, risk teams, financial reporting teams and investor relations teams, all of whom must work together to drive progress.

Economic alignment

To better understand the context in which CEOs are seeking to address emissions, we investigated the alignment between climate commitments and their strategic priorities, personal incentives, corporate resources, industry trends and regulatory factors. The upshot: context matters, a lot, and many CEOs are stretching for progress under less than favourable conditions.

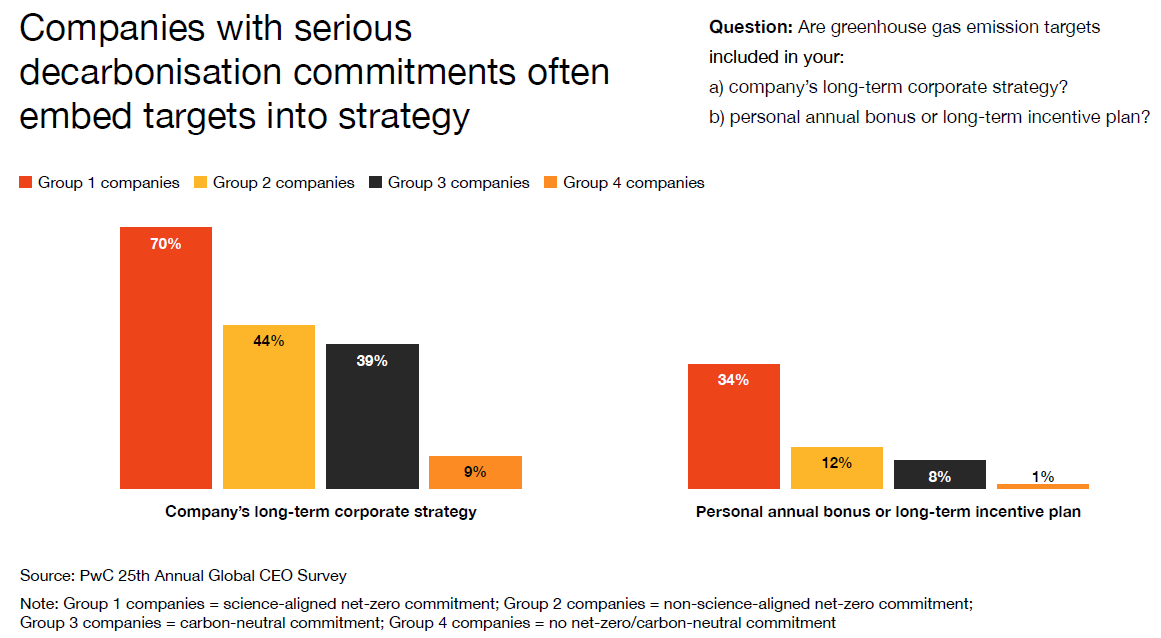

First, consider strategic and incentive alignment. We categorised companies into four groups, based on their decarbonisation commitments, from the most serious (Group 1, representing companies with science-aligned net-zero commitments or commitments-inprogress) to the least (Group 4, comprising companies that have not made a net-zero or carbon-neutral commitment to date). We found that the more significant the decarbonisation commitment, the more likely the company is to have emission targets in its corporate strategy. This is true for 70% of our Group 1 companies, but for only 44% of companies whose commitment is not science-aligned— and for only 9% of companies that have not made any type of commitment. This trend holds for incentives, too: 34% of companies that have made or are progressing toward science-aligned net-zero commitments have emissions tied to CEO compensation, compared to only 1% of companies with no commitment.

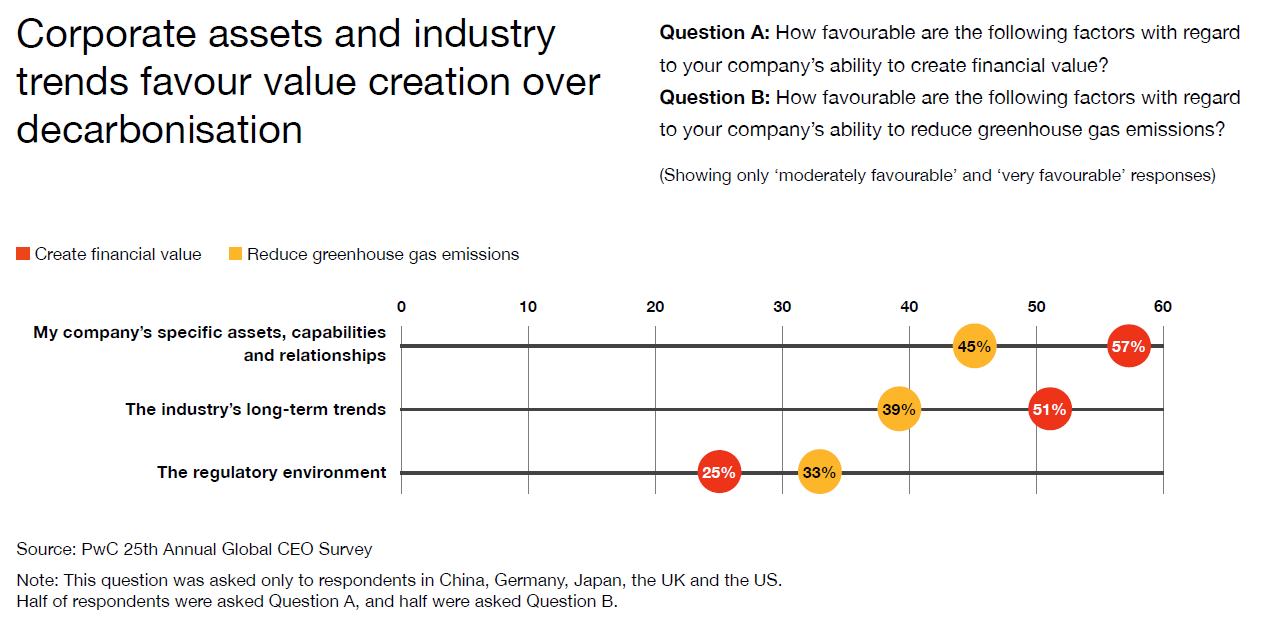

Next, consider the broader context for decision-making and action. CEOs report that their companies’ assets, capabilities and relationships, as well as the long-term trends in their industry, were considerably more favourable for creating financial value than for driving GHG reduction. This view is consistent with the priorities of investors, according to the above-mentioned PwC survey of global investors, only 19% of whom said they were prepared to take a hit on their returns exceeding one percentage point in the pursuit of ESG goals

CEOs acknowledge the need to navigate these complex financial realities. As Natascha Viljoen, [15] CEO of South Africa–based mining company Anglo American Platinum, explains it, ‘We have a responsibility to mine the mineral resources entrusted to us in a way that maximises the benefits to stakeholders and minimises the impact on the environment and host communities. We know that the mineral resources don’t belong to us; they belong to the people of the country. And then we have our shareholders’ money, which they entrust us with for returns.’

Despite the perception that corporate resources are more aligned with financial value creation than GHG reduction, the data suggests CEOs also believe those same assets and capabilities will do more than government regulation to address climate change. No doubt this reflects the challenges regulators have had in creating a coherent carbon reduction regime. CEOs such as Annikka Hurme, who leads Finland-based dairy and food company Valio, acknowledge both the opportunities and the potential obstacles governments can present. The company is setting up a joint venture to create biogas from cow manure for trucks on the road in Finland. ‘Right now,’ Hurme notes, ‘we are lobbying the government to create subsidies so that more businesses can convert their heavy vehicles from fossil diesel to biogas.’ At the same time, she is concerned about how policy changes could affect her company’s sustainability initiatives—‘that politicians at the EU and national level will make decisions that harm us, for example, by adding extra payments or new taxation that will prevent us from developing products in [a less-carbon-intensive] way.’

What if carbon carried a higher price? Establishing a meaningful regulatory framework—one that can truly move the needle in terms of decarbonisation—is fraught with challenges. But a new analysis by PwC and the World Economic Forum [16] starts to chip away at the complexity and offer a new way of thinking about regulation by assessing the economic impact of an international carbon price floor (ICPF). The study found that an ICPF could significantly reduce emissions—by as much as 12.3% by 2030—at an economic cost of less than 1% of global GDP. The costs avoided by reducing emissions would offset direct GDP loss. And the revenues generated from carbon pricing could be used to help decrease the impact on low-income countries. Carbon pricing is recognised as a highly efficient means of reducing emissions, but it will be politically complex, and its impact varies significantly by industry, geography and demography.

Breaking the cycle

The opportunity—and the challenge—is clear: progress on society’s toughest problems will be limited without bold action from CEOs stewarding critical corporate resources. At the same time, this year’s CEO Survey underscores just how full the “inboxes” of CEOs have become. Near-term financial imperatives remain mission critical, even as broader societal needs demand more mindshare. Against that backdrop, the following five priorities should help CEOs deliver the diverse range of sustained outcomes that stakeholders are

increasingly demanding:

- Resetting the conversation: Boards should be talking with their CEOs, and CEOs with their top teams, about their collective “inbox” problem. Enthusiasm about ESG won’t make near-term financial demands go away. Indeed, in a world of scarce time, attention and corporate resources, framing trade-offs realistically may be the only way to bring investors along and create a prudent strategic agenda, as opposed to a wish list.

- Recalibrating skills: Our survey results point to capability-building priorities related to cybersecurity, the cultivation of trust and the measurement and management of decarbonisation. In addition, the “inbox” problem holds implications for skill building and role modelling among top management and boards. When leaders are stretching to reimagine their organisation’s place in the world [17] and juggling an ever broader array of competing priorities, those who have a growth mindset and who demonstrate empathy and a willingness to embrace debate and dissent become more important than ever.

- Reappraising succession: The leadership needed to master today’s tenuous trade-offs is likely to come in all shapes and sizes, with external hires and emerging leaders from diverse talent pools critical to rounding out skill sets and resetting the conversation. Succession planning is an area where leaders and boards can challenge themselves immediately to start creating the future to which they aspire.

- Rethinking incentives: The strong association between incentives, net-zero commitments and other nonfinancial outcomes suggests it’s time for boards and management teams to take a hard look at the fit between the priorities they want their people to drive, the performance management systems they have in place and how they report their progress.

- Reimagining collaboration: Tackling society’s most urgent challenges won’t be an individual sport. It calls for an unprecedented level of cooperation among business leaders, government officials, policymakers, investors and nongovernmental organisations (NGOs). Each brings critical tools to the table and can support and enhance one another’s capabilities. Edelman’s pre-Glasgow Trust Barometer [18] found that no single type of institution is trusted when it comes to climate change action, but together they can create powerful momentum—in the form of regulation driving businesses to take aggressive action, NGOs boosting new government policies and so on.

Trust runs through many of these priorities, just as it runs through our survey results. To the extent that highly trusted companies are thinking and acting differently, and that those actions could help bridge the gap between society’s expectations and the system in which CEOs are operating, trust may be a meaningful enabler of change. And it’s only through change—bold, innovative and unbounded—that we can secure our collective future.

The complete publication, including footnotes, is available here.

Endnotes

1IMF, 2021. World Economic Outlook October 2021, https://www.imf.org/en/ Publications/WEO/Issues/2021/10/12/world-economic-outlook-october-2021(go back)

2Heather Swanston, Peter Greaves and Steven Fleming, 2021. “Navigating an asymmetrical recovery,” strategy+business, https://www.strategy-business.com/article/Navigating-an-asymmetrical-recovery(go back)

3Meng Ke and Yuke Li, 2021. “China needs 11.8m workers. Here’s how to close its labour gap,” World Economic Forum, https://www.weforum.org/agenda/2021/07/how-to-fix-china-labour-shortage(go back)

4Andrew Van Dam, 2021. “The latest twist in the ‘Great Resignation’: Retiring but delaying Social Security,” Washington Post, https://www.washingtonpost.com/business/2021/11/01/latest-twist-great-resignation-retiring-delaying-social-security(go back)

5Michael Wayland, 2021. “Chip shortage expected to cost auto industry $210 billion in revenue in 2021,” CNBC, https://www.cnbc.com/2021/09/23/chip-shortage-expected-to-cost-auto-industry-210-billion-in-2021.html(go back)

6Vicki Huff Eckert, 2022. “Living in a world of unicorns,” strategy+business, https://www.pwc.com/world-of-unicorns(go back)

7PwC, 2020. “Cyber threats 2020: Report on the global threat landscape,” https://www.pwc.co.uk/issues/cyber-security-services/insights/cyber-threats-2020-report-on-global-landscape.html(go back)

8Carlos Mario Lafaurie and Mariana Palau, 2021. “A Colombian energy company’s bold bet on sustainability,” strategy+business, https://www.strategy-business.com/article/A-Colombian-energy-companys-bold-bet-on-sustainability(go back)

9PwC, 2021. “2022 Global Digital Trust Insights Survey: The C-suite guide to simplifying for cyber readiness, today and tomorrow,” https://www.pwc.com/us/en/services/consulting/cybersecurity-risk-regulatory/library/global-digital-trust-insights.html(go back)

10Phillippa O’Connor, Lawrence Harris and Tom Gosling, 2021. “Linking executive pay to ESG goals,” strategy+business, https://www.pwc.com/gx/en/issues/esg/exec-pay-and-esg.html(go back)

11United Nations Climate Change, 2021. Race to Zero Campaign, https://racetozero.unfccc.int/join-the-race/(go back)

12Richard Black et al., 2021. “Taking stock: A global assessment of net zero targets,” Energy & Climate Intelligence Unit and Oxford Net Zero, https://ca1-eci.edcdn.com/reports/ECIU-Oxford_Taking_Stock.pdf(go back)

13Barbra Bukovac, 2021. “Procter & Gamble’s path to constructive disruption,” strategy+business, https://www.strategy-business.com/article/Procter-and-Gambles-path-to-constructive-disruption(go back)

14James Chalmers, Emma Cox and Nadja Picard, 2021. “The economic realities of ESG,” strategy+business, https://www.pwc.com/gx/en/services/audit-assurance/corporate-reporting/esg-investor-survey.html(go back)

15Michal Kotzé and Deborah Unger, 2021. “How Anglo American Platinum is reimagining the future of mining,” strategy+business, https://www.strategy-business.com/article/How-Anglo-American-Platinum-is-reimagining-the-future-of-mining(go back)

16World Economic Forum and PwC, 2021. “Increasing Climate Ambition: Analysis of an International Carbon Price Floor,” https://www.pwc.com/gx/en/services/sustainability/assets/economic-impact-of-a-carbon-price-floor.pdf(go back)

17Paul Leinwand and Mahadeva Matt Mani, 2021. “Seven imperatives for moving beyond digital,” strategy+business, https://www.pwc.com/gx/en/issues/transformation/leadership-in-the-digital-age.html(go back)

18Richard Edelman, 2021. “Business goes to Glasgow on the back foot,” Edelman, https://www.edelman.com/trust/2021-trust-barometer/business-goes-glasgow-back-foot(go back)