Print

PrintDan Konigsburg is Global Corporate Governance Leader, Aurelien Rocher is Senior Manager, and Jo Iwasaki is Corporate Governance Advisory Lead at Deloitte. This post is based on their Deloitte memorandum. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) and Will Corporations Deliver Value to All Stakeholders?, both by Lucian A. Bebchuk and Roberto Tallarita; For Whom Corporate Leaders Bargain by Lucian A. Bebchuk, Kobi Kastiel, and Roberto Tallarita (discussed on the Forum here); and Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy—A Reply to Professor Rock by Leo E. Strine, Jr. (discussed on the Forum here).

Climate change has emerged as a central and existential risk for organizations—and fertile and critical ground for innovation. Yet new Deloitte research shows that many audit committees, an essential bulwark in helping companies manage and respond to risks and opportunities, haven’t yet sufficiently placed climate change initiatives at the core of their agendas.

Among the more than 350 board audit committee members in 40 countries surveyed in Q4 2021 by the Deloitte Global Boardroom Program, nearly 60% say they don’t regularly discuss climate change during meetings. And nearly half say they lack the basic literacy in climate issues they need to make informed decisions. While results vary by region (see sidebar, “EMEA moving ahead”), more than two-thirds (70%) say they have yet to complete an assessment of how climate change will affect their company’s operations, supply chain, and customers.

Alarmingly, this report finds that “systemic threat barely features on audit committee meeting agendas, and there seems to be little appreciation of the impact climate change will have on the company’s business model and long-term strategy,” says Kerrie Waring, CEO) of the International Corporate Governance Network, which promotes global standards of corporate governance and investor stewardship (figure 1).

EMEA moving ahead

Deloitte Global’s survey of audit committee members shows that organizations in Europe, Middle East, and Africa (EMEA) are addressing gaps in climate governance and oversight better than organizations in the Americas and Asia-Pacific (AP) in many areas.

For example, 55% of EMEA audit committee respondents say their organization includes climate change on its agenda at least once a year, compared with just 34% in the Americas and 31% among AP companies. Moreover, 62% of respondents in EMEA describe some or all committee members as “climate literate,” versus 51% and 41% in the Americas and AP, respectively.

Perhaps not surprisingly, fewer than half of Americas and AP respondents say their committee has the information, capabilities, and mandate to fulfill its regulatory role on climate risks, compared with 58% of EMEA respondents.

Increasing urgency in a changing world

Amid the combined forces of the COVID-19 pandemic, climate change, and a heightened focus on racial injustice and economic inequality, companies are being called upon as never before not just to build shareholder value, but to participate in solving the world’s greatest challenges—and to be transparent and accountable in their endeavors.

“Investors are asking for accurate data to be able to assess companies’ risks and opportunities, emissions, and their climate impacts; regulators are seeking higher quality in ESG reporting to eradicate greenwashing and ‘social washing,’ and NGOs are increasingly pointing out shortcomings in this high-stakes and fast-moving area of company reporting,” says Veronica Poole, Deloitte Global IFRS and corporate reporting leader.

Sandra Boss, global head of Investment Stewardship at BlackRock, emphasized that “We ask that companies provide comprehensive disclosures on their long-term strategy, the milestones involved to deliver it, and the governance and operational processes that underpin their businesses.”

Businesses need to prepare for operational disruptions due to changing weather patterns and storms and focus on transitioning successfully to the low-carbon economy. “If a company understands that climate change is existential to the business, then this whole discussion is not simply an ‘add-on,’” says Robin Stalker, a Germany-based board audit committee member of Commerzbank AG, Hugo Boss Group, Schaeffler AG, and Schmitz Cargobull AG. “It is part and parcel of the whole strategy.”

Barriers to action

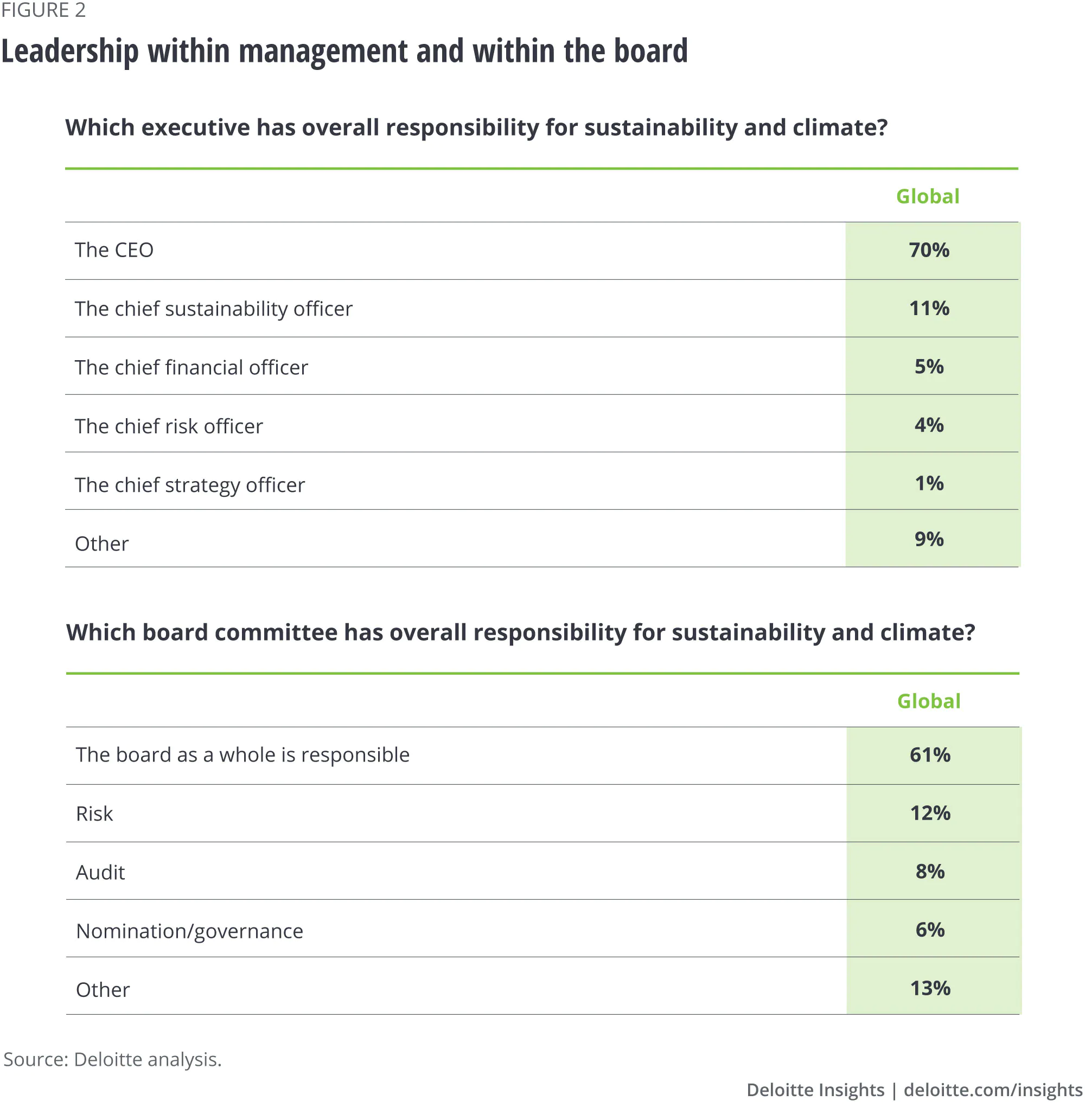

Many already recognize the urgency, with 42% of respondents wishing their organization’s climate response were swifter and more robust. And while the Deloitte Global’s survey focuses specifically on audit committees, 61% of respondents agree that responsibility for action rests not with any specific committee but with the entire board. And 70% say the CEO, rather than a chief sustainability officer or chief risk officer, should lead the way among executives (figure 2). All of which underscores the question: Why the delay?

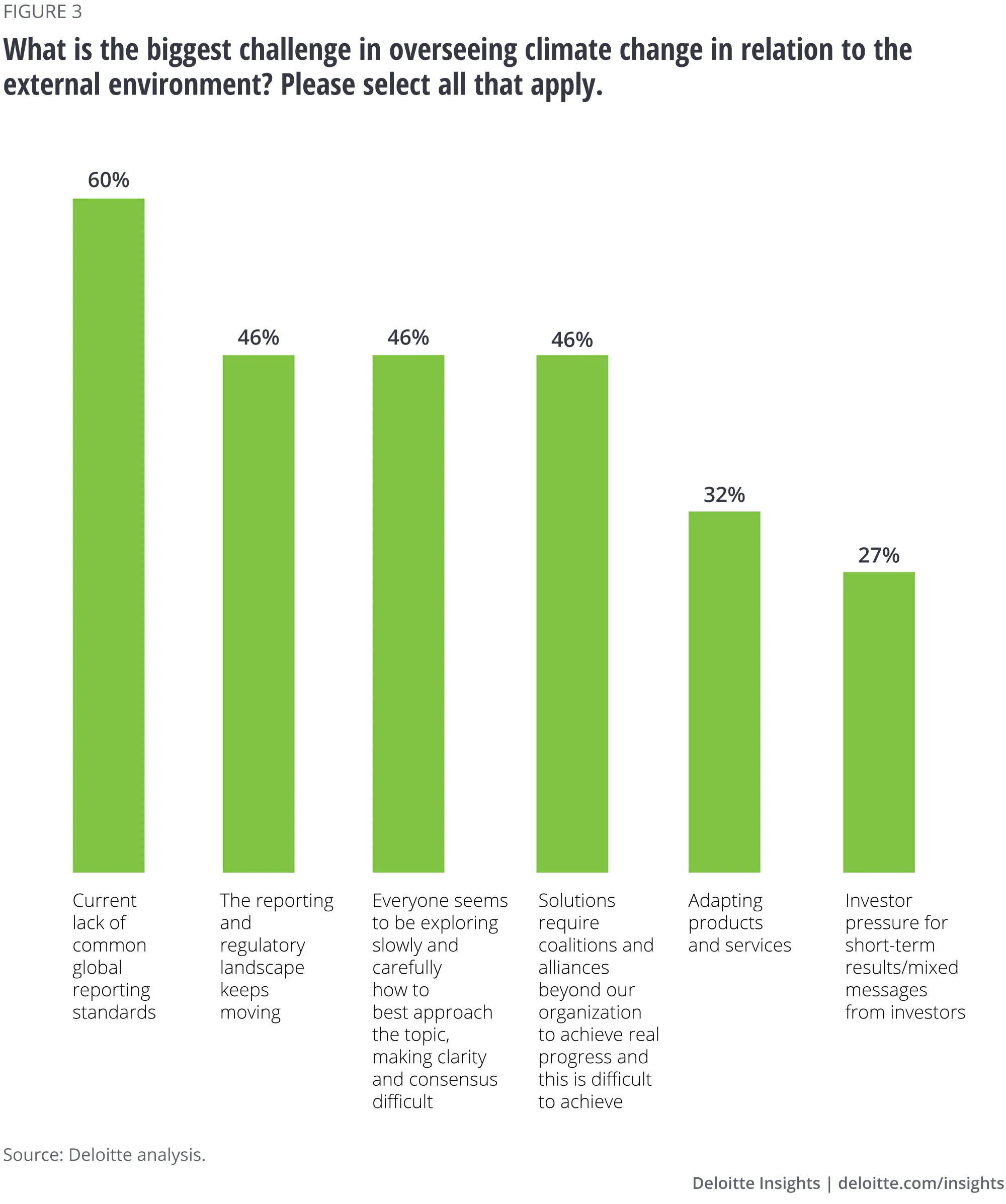

In some cases, inaction may feed a sense of complacency: Fifty-two percent of respondents say that even without completing a risk assessment, they believe climate change won’t materially affect the business. Respondents say the most formidable barrier they face is a lack of standards across geographies. About 60% believe the lack of global reporting standards makes it hard to compare their organization’s progress against meaningful external benchmarks. Fortunately, this is changing fast.

Other external barriers include an ever-shifting reporting and regulatory landscape, according to 46% of respondents. The same percentage of respondents attribute their own organization’s slow response to a more general lack of progress across industries, as all businesses seek the best approach. Such caution, they say, makes consensus difficult to attain. Still others (27%) cite conflicting messages from investors, who are simultaneously demanding long-term (and potentially expensive) climate change adjustments without sacrificing short-term financial results (figure 3).

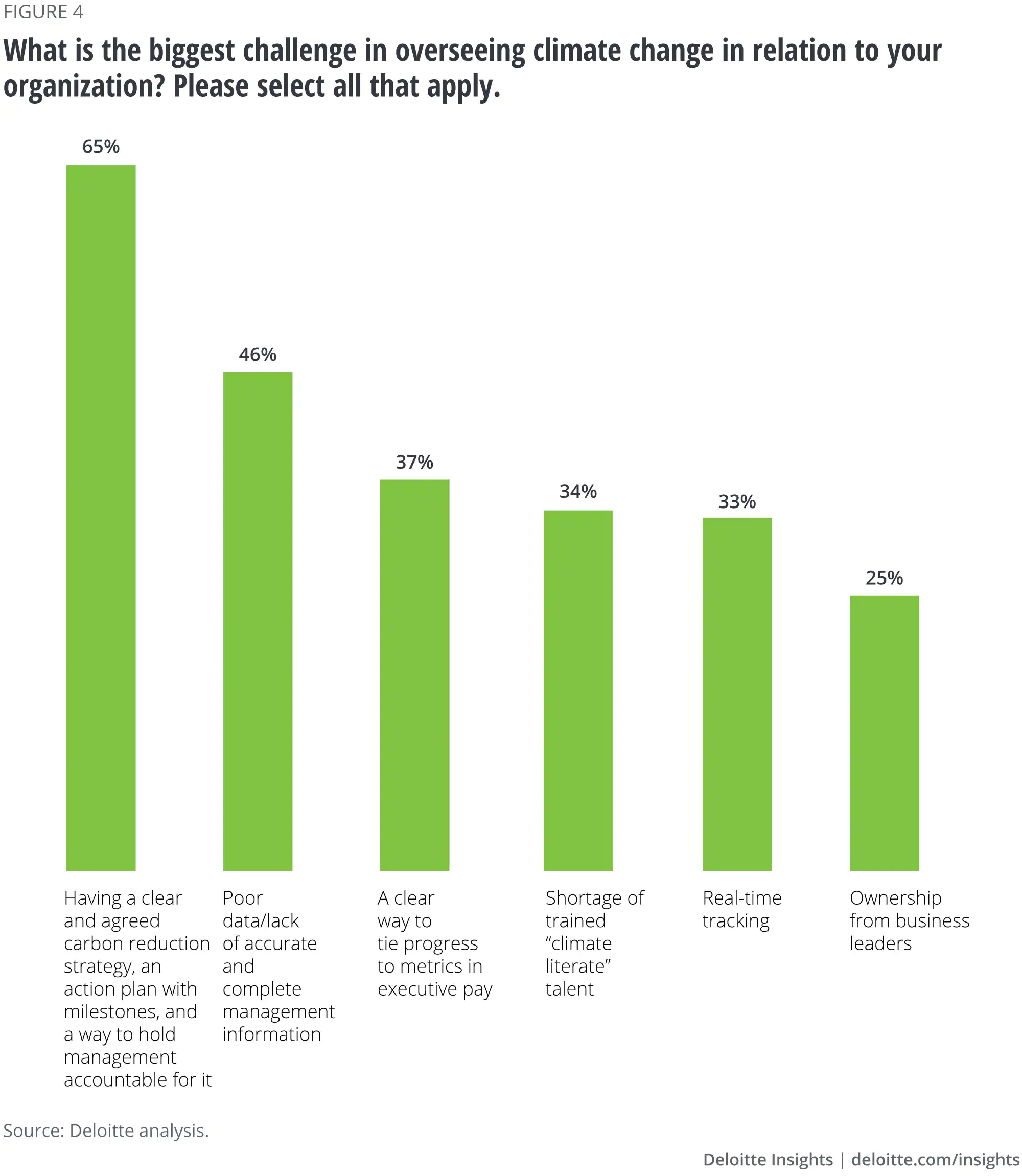

Internally, 65% of respondents say overseeing climate change initiatives is challenging because their organization lacks “a clear and agreed-upon carbon reduction strategy,” as well as “an action plan with milestones and a way to hold management accountable for it.”

One reason for the climate literacy challenge among boards and, more specifically, audit committee members, may be a paucity of information—an issue that’s being felt most acutely in the Americas. Fewer than half (46%) of respondents in Americas say the audit committee “has the information, capabilities, and mandate to fulfill its regulatory responsibilities in relation to climate risks and carbon reduction targets” (figure 4).

However real and credible these obstacles are, what’s manifestly clearer is that no board or audit committee can afford to use them as reasons for inaction or waiting to see how things unfold over time. Change isn’t coming; it’s already upon us.

Elements of a strategy

The specific elements of a company’s climate strategy will depend, of course, on its industry, products or services, geographical location, and other factors. Yet all such assessments rest on a few basics. “Fundamental to any strategy are the questions: Are we sustainable? Do we understand the risks? What does this mean for our business?” Stalker says.

The company’s climate strategy, as presented in the annual report, should offer specific details on commitments and strategies, rather than simply naming or listing them, Deloitte Global’s Poole recommends. That means, for example, being clear about how far down the value chain a company looks to identify climate-related risks and opportunities; specifying which categories of emissions are included in emissions targets and in the reported Scope 3 emissions; describing in what way climate commitments and strategies are incorporated into business plans; and how those plans have been reflected in the projections of cash flows that underpin numbers in financial statements.

Perhaps the greatest value that board members can add is insisting on measurable targets and milestones, Stalker says. “As good accountants, we know that what gets measured gets done.”

Board members can avoid accepting results at face value by pressure-testing assertions, advises Erik Thedéen, director general of Finansinspektionen Sweden and chair of the Task Force on Sustainable Finance at the International Organization of Securities Commissions (IOSCO). “If I sat in an audit committee and was presented with ESG numbers and metrics, I would be skeptical and ask questions about how were those metrics obtained? What alternative approaches were available?”

Opportunity to lead

Global sustainability reporting standards are now being developed by the IFRS Foundation’s International Sustainability Standards Board (ISSB), announced at COP26. But global reporting initiatives such as the Task Force on Climate-Related Financial Disclosures (TCFD) and the Sustainability Accounting Standards Board (SASB) are already helping companies embed climate issues into their businesses, and measure and report on progress and performance. The ISSB plans to issue new climate standards in 2022, which will reflect the TCFD recommendations. Those companies that have embraced TCFD should have a head start.

“We are greatly encouraged by the progress we have seen, as companies around the world are dramatically improving their sustainability disclosures and taking substantive action to adapt business models to mitigate climate risk and capitalize on new climate-related opportunities,” BlackRock’s Boss says.

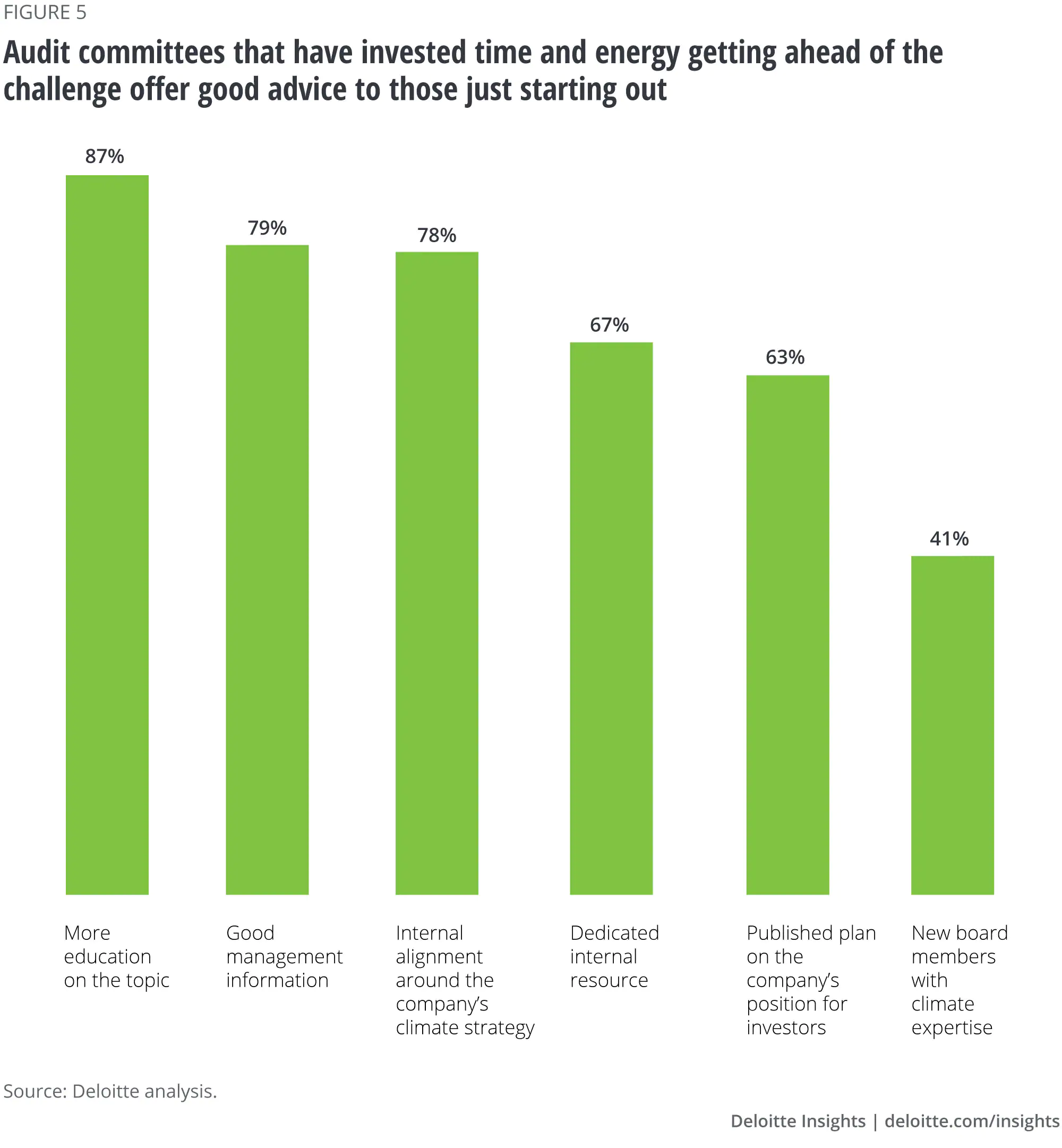

Companies that recognize the importance of acting now have the opportunity to help frame the conversation—rather than perpetually trying to keep up. In addition to pointing out barriers and challenges, the Deloitte Global’s survey reveals some best practices from respondents who say their committees, boards, and organizations are investing time and energy to stay ahead.

Among these respondents, the overwhelming majority (87%) say better education among board members is essential. Other recommendations include getting more robust information from management (79%), while 78% stress the importance of aligning internally around the company’s climate strategy (figure 5).

Establishing and following a climate strategy isn’t enough. Communication is also essential, with 63% recommending that companies publish their climate change plan for investors. Finally, 41 respondents suggest bringing on new members with specific climate expertise, which is easier said than done.

A call to action

The pace of change will only escalate in the years to come. Standards and measures used today will likely evolve, and audit committees, boards, and organizations as a whole must be willing to adapt and change in real time.

Yet the uncertainties can be no excuse for inaction. Companies need to jump in and act immediately. “We are all learning right now, and things are not perfect at the moment, on any board,” Stalker says, “but this is no excuse for not embarking on the journey.”