Print

PrintPeter Reali is Managing Director and Global Head of Stewardship, Jennifer Grzech is Director of Responsible Investing, and Anthony Garcia is Senior Director of Responsible Investing at Nuveen. This post is based on their Nuveen memorandum. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) and Will Corporations Deliver Value to All Stakeholders? both by Lucian A. Bebchuk and Roberto Tallarita; and For Whom Corporate Leaders Bargain (discussed on the Forum here) and Stakeholder Capitalism in the Time of COVID, both by Lucian Bebchuk, Kobi Kastiel, and Roberto Tallarita (discussed on the Forum here).

The momentum and support for environmental, social and governance (ESG) integration into the investment process has reached critical mass. Most companies now recognize the strategic need to have an ESG story, and some are even leveraging ESG leadership as a key differentiator from competitors.

Stakeholders may be looking for 2022 to represent the year that real-world impact is universally accepted as being in the long-term best interests of businesses. However, investors may disagree on how far the market is from that reality. Yet, it is becoming increasingly apparent to investors and stakeholders alike that there is market conflation of the inputs that go into corporate management of ESG risks and opportunities — such as reporting, policies and oversight — and the outputs of improvement on important environmental and social indicators — such as lower carbon emissions or greater pay equity among workers. For example, one interpretation of progress among the Climate Action 100+ universe of companies (i.e., the world’s largest corporate greenhouse gas emitters) is that nearly 85% have established oversight for climate risk. Another interpretation is that less than 3% of those companies have disclosed a quantifiable and trackable strategy in line with net zero emissions.

As stakeholders push for stronger stances and tangible outcomes, investors must navigate the shifting sands of financial materiality and the appropriateness of setting expectations for companies that may not yield results for years, if not decades. But with a recognition that the entire financial system will be significantly affected by long-term environmental and social (E&S) impacts comes a responsibility for investors to credibly address risks and opportunities today, rather than years in the future.

Figure 1: Reorienting E, S, and G along the lines of transparency, accountability and impact

One way to enhance credibility may be through a clearer categorization of ESG information and even proxy ballot items not just in terms of E, S or G, but in terms of the direct objectives or intentions they address.

| Category | Summary | Outcome Example |

|---|---|---|

| Transparency | Consistent, material disclosure that can inform investment analysis

Foundation for establishing ESG oversight, developing ESG commitments and assessing the results of company actions |

New or improved reporting on climate risk |

| Accountability | Policies, business strategies, oversight structures and incentives aimed at appropriately managing financially material ESG issues

ESG-related commitments with clear, relevant key performance indicators (KPIs) |

Set a science-based, net zero carbon commitment |

| Impact | Operational: The measurable results of company policies and practices

Products and services: The measurable results of company products and services for the environment and/or affected individuals and communities |

Emissions reduction achieved through intentional changes to business strategy |

Source: Nuveen

While there is no regulatory definition or market standard on what constitutes transparency, accountability and impact when it comes to ESG, such a framework forces investors to assess the meaning of existing ESG information and recalibrate expectations for what additional progress really looks like.

With the significant increase in ESG transparency over the last few years, investor engagements and shareholder proposals are increasingly focused on accountability and impact. In this maturing landscape, a recognition that reporting does not automatically generate impact has resulted in a greater focus on accountability as the bridge, with more calls for public commitments, strategies and even pay incentives related to E&S issues in particular.

While it may be too early for investors to coalesce around accountability expectations to drive significant vote dissent, the 2022 proxy season will likely see a continued evolution of more clearly articulated standards. If the precedent on board diversity is anything to go by, it is likely that boards will adapt and the market as a whole can move past transparency, toward accountability. We anticipate this to be an important turning point given where the tangible E&S outcomes of proxy voting currently stand.

The Divergence Between Shareholder Proposal Support and Election of Directors

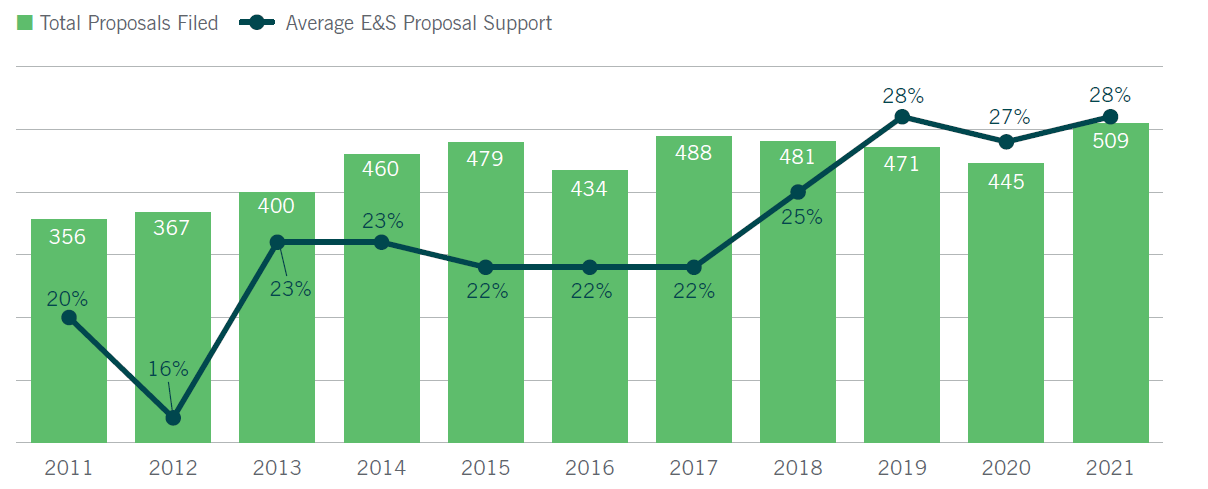

Since the first E&S-related shareholder proposal received majority support in 2016, each subsequent year has reset the high water mark for shareholder proposal support (4 in 2017, 8 in 2018, 12 in 2019, 21 in 2020, and 32 in 2021) and the trend is likely to continue accelerating in 2022 (Figure 2). Changes in the SEC’s position on the social policy significance of E&S issues will increase not only the quantity of shareholder proposals that appear on ballots, but also the specificity of what the proposal requests of the company. This has implications for the number of proposals making it through that focus on accountability and impact.

Investors seem to be applying greater scrutiny to boards of directors — indicated by a creeping number that received lower support (6.1% received less than 80% support in 2021 vs 5.3% in 2020). However, there also seems to be low correlation between investors’ stated ESG priorities and director election votes. Even for investors that appear favorably in both number of ESG shareholder proposals supported and number of directors voted against, the reasons for each set of votes are often unconnected.

Figure 2: Environmental and social shareholder proposals

Filed and average proposal support from 2011 – 2021

Source: ISS, 2021 Proxy Season Review on Shareholder Proposals

Many investors share anecdotal examples of E&S issues influencing a decision to vote against directors, but traditional governance issues like shareholder rights and director overboarding remain the predominant factors for directors receiving less than majority support from investors. While investors are not required to disclose any or all reasons behind a vote against a director, there is little evidence that a company’s failure to address E&S risks or be responsive to a shareholder proposal resulted in a director receiving less than majority support.

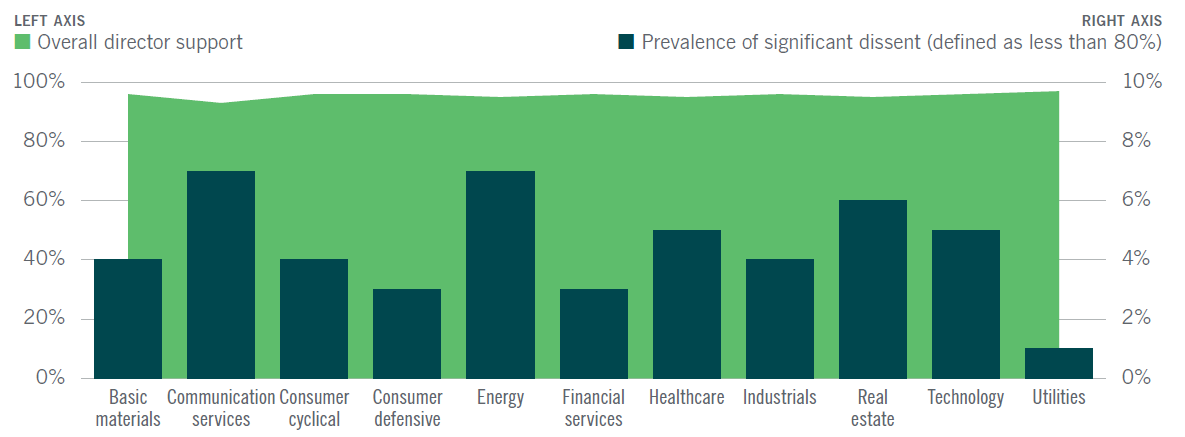

For director votes in the most carbon intensive sectors, there has been a generally high level of director support — around 95% support in 2021 — and little differentiation relative to other industries despite a heavy focus on climate change among the proponents of shareholder proposals. There is some incidence of industry carbon footprint correlating to lower director support. Coal companies had 86% overall support and 40% prevalence of significant dissent, but there are many governance issues at those companies which more likely drove dissent rather than environmental performance or escalation of environmentally-focused stewardship (Figure 3).

Figure 3: Director support levels by sector at 2021 annual meetings

Overall support levels and prevalence of significant dissent

Sources: ISS, 2021 Proxy Season Review on Director Elections & Governance and Proxy Insight Director Voting Data

One possible reason for continued board support, despite a lack of progress on low-carbon transition strategies and actual decarbonization, is that companies in carbon intensive industries are more likely to disclose climate-related information in line with investor expectations. The amount of information disclosed, in particular relative to industries where climate risk is less direct or well understood, could be holding back investor votes against directors at energy companies that are perceived to have met a higher standard of transparency on an absolute basis.

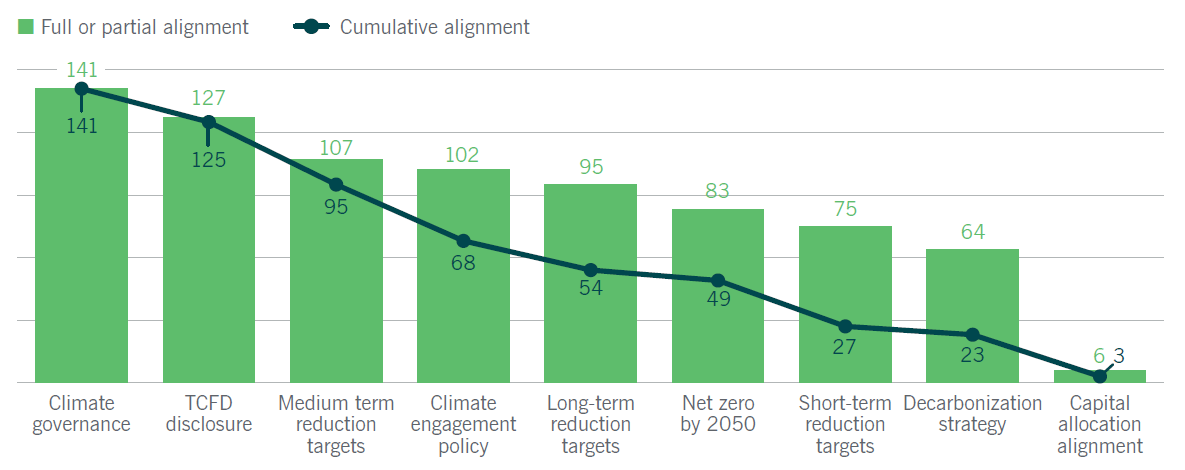

Yet, as investors raise the bar on climate expectations, the fact that over half of the Climate Action 100+ focus companies had stated a net zero by 2050 goal, but less than half have a clearly defined decarbonization strategy, could forecast a turning tide. In cumulative terms, only 2% of companies have at least partial alignment across all of the Climate Action 100+ key performance indicators (KPIs) (Figure 4).

The rise of net zero commitments from asset owners and asset managers suggests investors may be prepared to translate newly enhanced ESG transparency into investment decision-making, including voting against directors where companies’ carbon footprints are clearly misaligned with the investors’ strategies for achieving net zero. On the other hand, investors may be focused on engagement and understanding company strategy related to carbon reduction with 2025 or 2030 as the more appropriate dates to assess company performance against a low carbon strategy.

Assessing Shareholder Proposal Support Against Real-World Outcomes

The history of E&S proposals receiving majority support is limited, but the early evidence suggests that support does lead to company responsiveness and positive improvements — at least when measured by ESG ratings. Based on E&S shareholder proposals that received majority support from 2018 – 2020, the most common outcome is for the companies’ ESG ratings to improve on both an absolute and industry-relative basis. More than two thirds of companies (69%) have seen an improvement in MSCI ratings and almost 60% now have environmental or social ratings that are above the industry average. [1]

However, ESG ratings do not exclusively or even primarily measure the impact a company has on its stakeholders. Usually, the ESG ratings focus on transparency and whether the company faces any ESG-related controversies. The ESG ratings do not measure whether, or to what extent, policies adopted or KPIs reported lead to improvements for the stakeholders they are intended to address. In other words, despite the correlation between shareholder proposal support and ESG ratings improvements, the real-world outcome is less clear, or perhaps yet unrealized.

Figure 4: Climate action 100+ focus companies

Cumulative alignment with net-zero key performance indicators

Source: Climate Action 100+, Net Zero Company Benchmarks

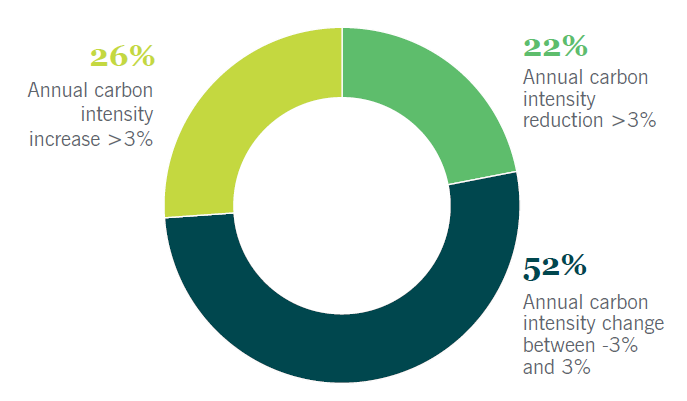

Looking at climate change, for example, companies may develop new reporting or make low-carbon- aligned commitments in the short-term to improve ESG ratings. But meaningful reduction in a company’s carbon footprint requires capital expenditures and changes to business operations that often require more time. Reviewing shareholder proposals for the past decade relative to an impact indicator such as carbon intensity shows a mixed picture. Analysis of shareholder proposals that have received significant support (30% or more) going back to 2011, shows that fewer than half (48%) of the vote outcomes translated to sustained reduction in carbon intensity from the year of the annual meeting to present. In terms of assessing real-world impact, only 22% of companies had an average annual reduction in carbon intensity of greater than 3%, which, if sustained over 10 years, would translate to a 25% reduction in emissions intensity. Given global decarbonization in 2021 was about 2.5%, these results generally align with business as usual (Figure 5).

Figure 5: Changes to carbon intensity at companies

Where climate-related shareholder proposal received >30% support

Source: Nuveen analysis of MSCI and Proxy Insight Data as of 31 December 2021. Carbon intensity is defined as total Scope 1 + 2 + 3 emissions/total company revenue. Annual change in carbon intensity uses the year a shareholder proposal received majority support as the company’s baseline year for emissions intensity. The cumulative year over year change from the baseline was averaged over the number of years since the vote to account for the different time periods.

Granted, in some cases shareholder proposals were filed at the same company in multiple years. ExxonMobil and Chevron Corporation alone account for 8% of the data sample. This may skew the results since companies that make improvements are less likely to require continued advocacy via additional shareholder resolutions. Nonetheless, this data points to a need for investors to be mindful that the support for shareholder proposals does not always create the outcome being sought in the proposal. It also raises the question of what should define the success of a shareholder proposal given the limits to their scope.

Focusing on Shareholder Proposals as Tool for Transparency and Accountability

Despite something of a lack of evidence for shareholder proposals catalyzing environmental or social impact, they have generated meaningful change. Earlier versions of climate-related shareholder proposals were often broad-based and transparency focused; e.g., seeking a sustainability report. This is in contrast to the current proposals requesting specific greenhouse gas (GHG) reduction targets or strategies to keep business operations aligned with net zero ambitions.

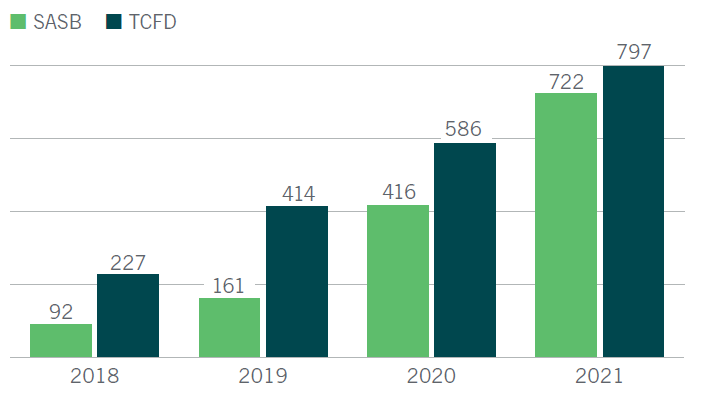

What the period of 2011 – 2018 does represent is the foundational work that stewardship advocacy has had on ESG transparency and creating a focus on material ESG disclosures that can drive assessments of company accountability. Since the publication of the Sustainability Accounting Standards Board’s (SASB) materiality map standards in 2018, there has been a significant uptick in the number of companies providing material ESG disclosure in line with the SASB and Task Force on Climate-Related Financial Disclosures (TCFD) frameworks (Figure 6).

Figure 6: Number of companies reporting in line with material ESG standards

S&P 1200 companies

Source: The Value Reporting Foundation, More Than Half of S&P Global 1200 Now Disclose Using SASB Standards, September 22, 2021

Looking at climate risk specifically, the quality of TCFD reporting is improving in terms of companies not only establishing aspirational targets or acknowledging climate as a material risk to the business, but also creating the infrastructure to manage climate risk. More than 52% of companies (a 14% improvement from 2018) now address climate risks and opportunities of the business and 13% (an 8% improvement from 2018) even address the resilience of the current climate strategy if market or social momentum spur a faster low carbon transition. [2]

The SEC’s new standards will allow for more shareholder proposals with specific expectations with regard to company strategy making it to ballots. For companies to continue to be responsive, they will have to more closely align with the accountability or impact expectations of the stakeholders and investors that supported the proposal. So long as investors hold companies to account for responsiveness to achieving impact in the same way they have for responsiveness to ESG reporting expectations, then real-world E&S outcomes may begin to manifest from shareholder proposals.

Escalating Unaddressed ESG Issues to Votes Against Directors

The proxy contest at ExxonMobil was seen as a watershed moment for investors’ conviction on developing a business strategy aligned with the low carbon transition. While carbon reduction cannot be expected over a six-month period, Exxon’s recently announced corporate strategy suggests business as usual, as the company will continue to invest 90% of capital expenditures into its legacy businesses.

Investors continue to advocate for more accountability via independent board leadership and more climate expertise in addition to target setting, and there have been some positive results in terms of influencing Exxon to make a net zero by 2050 commitment. However, the Exxon commitment excludes scope 3 emissions and raises questions about how far investors will be able to push the company.

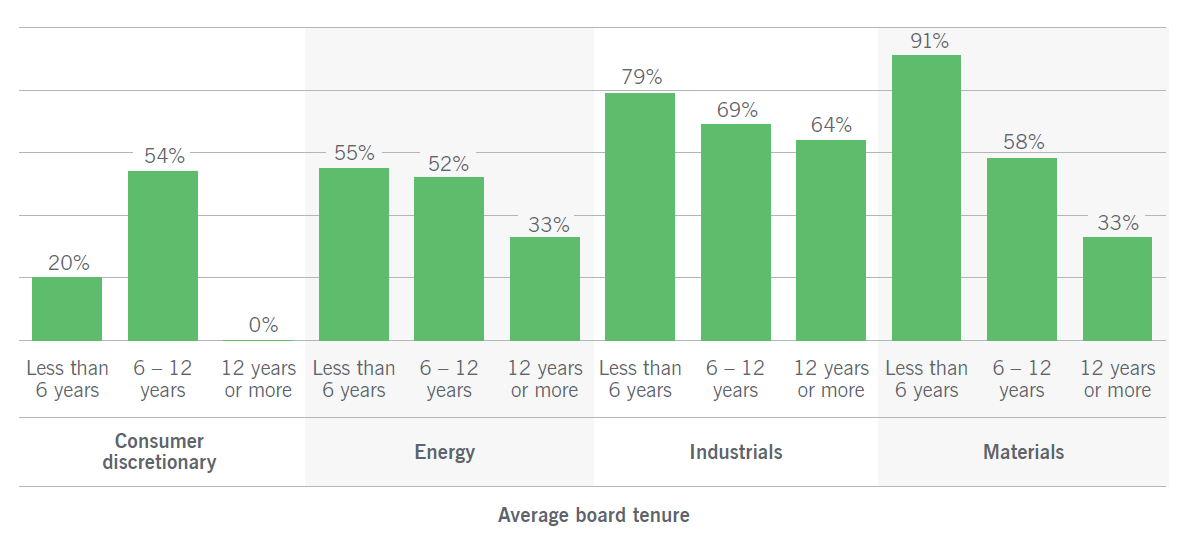

Analyzing the market more broadly though, board refreshment does exhibit greater correlation to positive outcomes on climate performance than shareholder proposal support. Over the past decade, companies with the lowest average board tenure were more likely to have reduced carbon intensity at a greater rate than industry peers. In addition, boards with the highest average tenure are more likely to lag industry peers in carbon intensity reduction (Figure 7).

Figure 7: Relative carbon intensity reduction among S&P 1500 companies (2011 – 2021)

% of companies with carbon intensity reduction > industry average

Source: Nuveen analysis of MSCI and ISS data 01 January 2011 – 31 December 2021.

Conclusion

Market participants often focus exclusively on transparency or impact in their company assessments. However, distinguishing and assessing company accountability, in terms of the ESG targets the company sets and the detailed plans it has to achieve those targets, is more likely to indicate which companies are making meaningful progress toward impact and which companies are using transparency to deflect stakeholder pressure.

Investors themselves must increasingly contend with their own transparency, accountability and impact when it comes to stakeholder expectations. This requires that ESG conviction extend beyond the shareholder proposal vote, if the investment thesis is truly that companies’ management of ESG issues affects sustainable, long-term value creation. In this context, votes against boards based on unmet E&S expectations may be the new frontier of active ownership.

Endnotes

1Source: Nuveen analysis of MSCI ratings as of 12/31/2021. The comparison was based on the MSCI ratings pillar most relevant to the shareholder proposal theme.(go back)

2The Task Force on Climate-related Financial Disclosures 2021 Status Report.(go back)