Print

PrintMaria Moats is the leader of PricewaterhouseCoopers LLP Governance Insights Center, Shawn Panson is the US Private Company Services Leader for PricewaterhouseCoopers LLP, and Carin Robinson is a Director at PricewaterhouseCoopers LLP. This post is based on their PwC memorandum. Related research from the Program on Corporate Governance includes Independent Directors and Controlling Shareholders by Lucian Bebchuk and Assaf Hamdani (discussed on the Forum here); Politics and Gender in the Executive Suite by Alma Cohen, Moshe Hazan, and David Weiss (discussed on the Forum here); Will Nasdaq’s Diversity Rules Harm Investors? by Jesse M. Fried (discussed on the Forum here); Duty and Diversity by Chris Brummer and Leo E. Strine, Jr. (discussed on the Forum here).

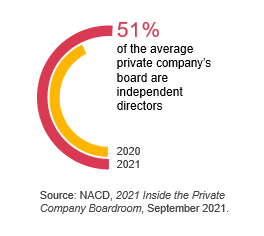

Good governance is not just for public companies. Private companies today are also looking for ways to improve their board’s effectiveness—in part, by changing their board composition. Where once private company boards were dominated by members of management and investors, independent directors now make up slightly over half (51%) of the average private company’s board (up from 43% in 2020) according to a recent survey.

Why the shift? Some companies are positioning themselves for the future. They could be preparing to go public or considering a generational transition in family ownership. Others simply see the incremental value that outside directors bring.

Companies that are reshaping their boards and introducing new faces outside of their familiar networks are gaining valuable insights. Private companies that do not have outside directors today are missing out on a valuable opportunity.

What is an “outside” director?

Outside of certain regulated entities, private companies are not generally required to have independent directors on their boards. So while public companies have a fairly clear standard of independence, private companies may define “outside” directors in different ways. Here, we use the term to mean a person who doesn’t have a significant relationship with the company aside from board service. That means that they are not an employee or consultant, and they are not a significant investor, customer, vendor, or counterparty to other contracts or arrangements.

Outside directors as a complement to the current board.

Private companies are looking to outside directors to make their boards better. Seventy-one percent (71%) of private company directors say their boards added independent directors as “a source of new ideas,” and more than half (55%) did so for the benefit of their experience running profitable businesses. Areas where outside directors can add tremendous value include:

- Perspectives, experience, networks. Outside directors can bring knowledge and experience in areas that inside directors do not possess. They can also bring fresh perspectives and leverage their networks to benefit the business.

- Objectivity and independence. Highly-qualified outside directors will challenge assumptions and bring an unbiased perspective that can be extremely valuable to those who are immersed in the company’s day-to-day.

- Governance and accountability. Having outside directors often means enhancing board practices and bringing discipline to governance processes. If board meetings and reporting about areas like strategy, projects, and financial results have become routine, having outside directors can improve the underlying processes and instill accountability.

- Credibility: Consumers, employees, investors, and other key stakeholders may perceive outside directors as a positive governance practice, bringing improved credibility to the company and its owners.

- Advising the CEO. Outside directors may be leading or have led their own companies, in which case the CEO may value feedback from executives who have been in his or her shoes.

- Planning/advising on exit strategies: Outside directors can help the entire board navigate important strategic transactions, such as an IPO, minimizing disruption related to the withdrawal of an investor, or other ownership changes.

Board committees

The number of standing board committees tends to increase with the addition of outside directors. As the percentage of private companies with outside directors rises, we note that the number of private companies with an audit committee also rose (from 79% to 88% in the last year). Outside directors should push private companies to consider an audit committee if one does not exist today.

Audit and compensation committees in particular (which are mandatory for public companies) benefit by leveraging truly independent perspectives, which only outside directors can bring. Outside directors often serve as chairs of these committees.

Diversifying with outside directors

With increasing pressure for public company boards to become more diverse, many private companies are examining their own board composition and identifying changes that should be made. Particularly for private companies that intend to go public, there is an urgency to establish a diverse board in line with jurisdictional standards applicable to public companies.

Ninety-three percent (93%) of directors say diversity brings unique perspectives to boardrooms, and 85% also say it improves board performance. So private company boards can benefit from more diversity—but often they need to look to outside directors to make enhancements, whether in terms of gender or racial diversity.

Recruiting outside directors with diverse backgrounds can be particularly helpful if the executive management team is not diverse. The board, to some degree, should resemble a company’s customers, employees, shareholders, and other key stakeholders. Many governance professionals believe that doing so can provide better insight into how these important constituencies think.

Finding the right outside director(s) for your board

There are many factors to consider when adding outside directors. Boards will want to take a systematic approach so that they have the right mix of skills, experience, and diversity of thought in the boardroom.

- Determine optimal board composition—Consider the company’s longer-term strategy and the skills or experience needed to support it. Through this exercise, identify other desirable attributes, such as director tenure, age, and diversity. Also consider the skills or experience needed for each of the board’s committees. For example, having someone with a financial background on the audit committee is critical.

- Assess current board composition—Evaluate the skills and attributes of each director, including any known departures or committee transitions, to get a holistic view of the current board and any gaps. Some companies use a board composition matrix to do this. See an example of one in our Board composition: The road to strategic refreshment and succession.

- Prioritize gaps to inform director search—Focus on the most important missing skills or experience to drive the search. Boards may not be able to fill every gap, so ensure that the priority of which needs to be filled first is clear.

- Launch a director search—Create a director profile to help with recruitment. It’s important to confirm the director profile with the entire board, but it’s also a great recruiting tool to share with outside candidates. Including your company’s mission and vision, details about the director role and expectations, and even compensation will help candidates evaluate if this is the right role for them before they sign on.

Recruiting outside directors: a how-to

- Identify candidates. This may mean looking at sources that are outside of the personal networks of current directors and members of management. Being deliberate about pursuing diverse or specialized candidates often means broadening the search. Director search firms, governance associations, and professional service firms can help.

- Conduct interviews. Candidates will likely be interviewed by members of the nominating and governance committee (if there is one), the board chair, and certain executives to evaluate the candidate and determine whether they would be a good cultural fit.

- Complete a background check. It’s important to know if there are any issues that would affect the prospective board member’s candidacy, as well as any relationships they may have with the company, investors, or management.

- Consider the candidate’s ability to commit. This includes time preparing for, traveling to, and attending meetings. Some candidates simply won’t have the time to do the job effectively.

- Understand the candidate’s decision-making process. Candidates will be performing their own due diligence on the company, to determine whether the board is a good fit for them. They may ask to meet other directors, visit business locations, review financial statements, and/or understand the company’s directors and officers (D&O) liability insurance. Since much of this information is confidential, companies often ask candidates to sign a non-disclosure agreement.

What’s holding private companies back adding outside directors to their boards.

It’s not unusual for shareholders or current board members to have concerns about adding outsiders. Though most private companies would say they encourage decision-making that embraces a range of views, they are also often nervous about losing connection to the company and its values. Common shareholder concerns and possible ways to address them include:

- Outside directors may slow down decision-making. Having outside directors may slow down the process, but the value they bring often outweighs this concern. Companies can consider this when deciding who to recruit, by focusing on director candidates that come from environments where speed matters. They can also make sure that outside directors are well informed, which may mean holding ad hoc meetings to get directors up to speed when a quick decision is needed.

- Outside directors may expect more formality. Outside directors may expect certain formalities—like meeting agendas and materials prepared in advance, and recording minutes. These activities take time. This investment typically pays off, and in some situations can come in handy. For example, if challenged, having copies of meeting materials and minutes can help demonstrate that there was appropriate board deliberation or oversight.

- Shareholders may feel like they are giving up control. Controlling shareholders still get the final say. A written shareholder agreement is an effective way for shareholders to give themselves veto rights on certain decisions in the event the board votes in a manner that shareholders are not happy with.

- Outsiders may have access to confidential information. Outside directors are expected to maintain confidentiality about the company’s operations and results. A common practice is to reinforce this expectation by having outside directors sign a non-disclosure agreement.

- It may be expensive to have outside directors. Governance usually costs more as boards formalize processes and add outside directors. However, companies can consider different ways to compensate outside directors (e.g., equity-like vehicles) if cash flow is a problem.

Some private companies prefer to give outside directors an advisory role.

Boards of private companies are not locked into specific roles. They are not bound by the SEC and stock exchange listing rules that set responsibilities for public company boards and committees. Shareholders may decide they don’t want the board involved in all areas.

Some private companies choose to bring outside directors onto their boards in an advisory capacity—either by bringing them on as advisors to the fiduciary board, or creating a separate advisory board. Advisors to the fiduciary board often join only certain portions of board meetings, and many times do not have voting rights. Advisory boards meet separately, but exist to provide the fiduciary board and management with insights and views on specific subjects. Creating an advisory board can be a comfortable first step for some private companies.

Conclusion

Top-performing private companies know that bringing on outside directors is essential to being at the forefront of leading governance practices. They bring diverse perspectives and can fill important skill gaps. They can lend added credibility to the company and help as it looks to growth or exit opportunities. And as discussed above, having outside directors can lead to other governance improvements that will benefit the company as it matures.

The complete publication is available here.