Print

PrintSubodh Mishra is Global Head of Communications at Institutional Shareholder Services. This post is based on an ISS ESG memorandum by Viola Lutz. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance by Lucian A. Bebchuk and Roberto Tallarita (discussed on the Forum here); For Whom Corporate Leaders Bargain by Lucian A. Bebchuk, Kobi Kastiel, and Roberto Tallarita (discussed on the Forum here); Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy – A Reply to Professor Rock by Leo Strine (discuss on the Forum here); and Stakeholder Capitalism in the Time of COVID, by Lucian Bebchuk, Kobi Kastiel, and Roberto Tallarita (discussed on the Forum here).

Key Takeaways

- Transparency is the foundation of a successful Net Zero transition. Given heightened concerns about what has been described as ”the climate emergency,” transparency about where actors stand on climate issues is crucial. Companies and financial institutions alike need to disclose medium-term action so it can be scrutinised, allowing for the identification of gaps that need to be tackled.

- Standards setters and regulators are driving transparency, from the Task Force on Climate-related Financial Disclosures (TCFD) to the US Securities and Exchange Commission (SEC) and the International Sustainability Standards Board (ISSB). The development of a comprehensive global baseline of sustainability disclosures could significantly promote transparency further.

- Active ownership via engagement and voting, together with litigation by shareholders and other stakeholders, are increasingly motivating enhanced disclosure. Shareholder proposals requesting disclosure of emissions reductions goals remained one of the top climate-related proposals in 2021.

- The market needs to become more transparent: 71% of companies in the STOXX USA 500 and 73% within the STOXX Europe 600 are disclosing all material Scope 1, 2 and 3 emissions and 23% (STOXX USA 500) and 47% (STOXX Europe 600), respectively, have an emission reduction target approved by the Science Based Targets initiative (SBTi). Larger companies are driving overall transparency performance, but there is pressure for the rest of the market to step up.

- Financial institutions are increasingly expected to report transparently on their climate change-related governance practices. This could involve climate competency within boards, explicit structures for climate oversight, and clear responsibilities for climate strategy and risk management, along with prioritising real economic impact over “virtual” emission reductions.

Introduction

Addressing climate change will require increased transparency. The low-carbon transition is a hugely complex undertaking. Knowing where different actors stand in transition efforts and what unresolved technological and organizational problems exist can help direct investments, research and development efforts, and rapid policy responses to climate change. This post examines the drivers of an increased focus on transparency around climate change, how regulatory action is shaping up, and the non-regulatory measures being taken by a variety of actors, such as litigation and active ownership strategies. The complete publication (available here) concludes with an investigation into what this means for the finance industry.

Shining a Light—Why the Focus on Transparency is Here to Stay

Concern about transparency on climate change-related issues is spreading through the finance industry. From Singapore to New York, from local to national levels, from the Task Force on Climate-related Financial Disclosures (TCFD) reporting for financial institutions to companies’ Net Zero pledges and target-setting frameworks, transparency on climate issues is a priority.

What is driving this unprecedented focus on climate transparency? Three factors stand out:

- It’s a climate emergency. With the stakes high, it is essential that the market understands where the world and companies stand.

- The road ahead is clear. What needs to happen in the medium-term is evident, and hence transparency on progress is being demanded.

- The long game still needs to be won. There are gaps that need to be filled in research and development and policy action if we are to reach Net Zero. Disclosure is essential if these gaps are to be identified and acted upon.

Increasing Requirements for Transparency

The UNFCC’s COP26 in Glasgow and the COP26 Private Finance Strategy promoted greater adoption of the TCFD, highlighting the importance of addressing climate disclosures. Investors and broader financial institutions were at the forefront of the conversations.

The world certainly seems to have listened, responding with a wave of climate-disclosure-related regulation. Institutions that do not voluntarily embrace transparency might be pushed regardless towards greater transparency, by litigation and active ownership.

The regulatory wave

Regulators across all markets are increasingly requiring companies, including financial institutions, to provide timely, comprehensive, and comparable climate-related risk (and sustainability) reporting. In some cases, the proposed requirements extend beyond public companies to the private sector and span companies’ subsidiaries and supply chains. Asset owners, asset managers and civil society organizations have advocated for greater transparency, and voluntary market-led initiatives like those of the TCFD and Sustainability Accounting Standards Board (SASB) have helped to improve transparency and climate-related risks disclosures. Meanwhile, research providers like ISS ESG continue to support investors with comprehensive data, analytics, and advisory services to help them understand, measure, and manage risks and opportunities to achieve their investment objectives.

Nevertheless, well-crafted and thoughtful legislation and regulation foster policy durability and generally lead to wider market adoption. Regulators in the EU, US, UK, and the APAC region are well on their way to developing climate-related reporting requirements. This paper does not seek to comprehensively address them all, but it is worth noting that while the approaches might differ, the underlying objective does not: regulators are seeking greater corporate transparency.

Regulatory sequencing can vary: for example, financial institutions in the EU must report on certain sustainability characteristics before their portfolio companies do. The materiality approach may vary as well, with some regulators focusing on enterprise value, meaning how climate change might impact a business’ financial performance, whereas other regulators opt for a broader double materiality approach, including the actual and potential impacts of an entity’s activities on the environment and the society.

Commonalities persist across the various regulatory drivers, however. For example, the concept of a “taxonomy” ranking the sustainability of different business activities has become a cornerstone of transparency initiatives across the globe. The EU’s Taxonomy, which initially focused on climate-change objectives and has now broadened to cover further environmental ones, was certainly the first mover, but we are observing a proliferation of regionally focused equivalents. They serve to form a common national understanding of what can be considered “green” or “sustainable.”

Such taxonomies are being increasingly complemented by mandatory or quasi-mandatory efforts targeting financial institutions. These disclosure efforts often take the perspective of climate-risk management and what an adequate approach to such risk by financial actors can and should look like.

Another recent regulatory initiative has been the requirement for government-supervised entities in the finance sector to conduct climate stress testing of their portfolios and loan books, as well as scenario analysis across various timeframes, usually with more incremental time intervals in the short-term, and long-term assessments up until 2050. Down the line, stress testing may start to influence monetary policy. We can also expect regulators to expand their regulatory and supervisory approach to climate-related financial risks to take into account systemic risks.

Moreover, in various jurisdictions regulators and standard setters have proposed or are implementing either voluntary or mandatory rules around the disclosure of climate risk. In France and the Netherlands, the finance sector is asked to assess and disclose the carbon footprint of its investments. In the UK, the Financial Conduct Authority (FCA) is developing a standard for the disclosure of Net Zero transition plans intended to apply to listed companies and financial institutions alike.

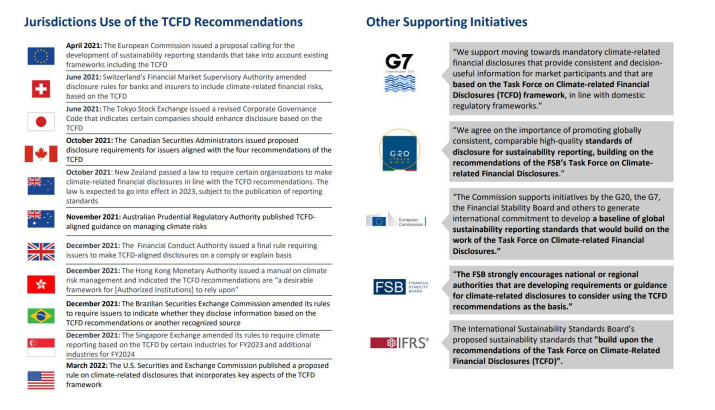

Figure 4: Organizations Expressing Support for the TCFD Recommendations

Source: TCFD

The Task Force on Climate-related Financial Disclosures (TCFD) appears repeatedly as a common backbone for various disclosure frameworks around the world. Given its broad take-up, what should one know about the TCFD?

The common choice: The TCFD

The first regulation legislating mandatory TCFD-aligned climate disclosures was introduced by New Zealand’s “Financial Sector (Climate-Related Disclosures and Other Matters) Amendment Bill,” in April 2021, which targeted most listed issuers, banks, insurers, and asset managers. The first reports are expected in FY2023. The UK introduced a phased implementation approach followed by reporting requirements increasing up until 2025.

In a context where more than 400 disclosure frameworks for corporates and 20 for investors exist, the objective of the TCFD is to create a harmonised standard for both corporate and investment climate disclosure which acknowledges that domestic and local regulatory frameworks may require different levels of compliance. And in 2021, it launched an update to its recommendations.

TCFD Core Recommendations are organized under four well-known pillars: Governance, Strategy, Risk Management, and Metrics & Targets. In its 2021 Recommendations update, the TCFD left the four underlying pillars intact and provided additional guidance on two of them (Strategy and Metrics & Targets) for all sectors, as well as supplementary guidance for the Finance Sector across three pillars.

What stands out about the updated 2021 Recommendations are increased demands for details related to climate risk and specifically actual financial impacts, and encouragement for Scope 3 emissions disclosure.

These features are similar to recently published considerations from the US Securities and Exchange Commission (SEC) that also refer to the TCFD as a source of inspiration.

The common talk: The SEC

In March 2022, the SEC proposed long-awaited rule changes to enhance and standardize climate-related disclosure of domestic and foreign registrants. The SEC’s objective is to provide “consistent, comparable, and reliable—and therefore decision-useful—information to investors to enable them to make informed judgments about the impact of climate-related risks on current and potential investments.” The SEC explains that “Climate-related risks can affect a company’s business and its financial performance and position in a number of ways… [improved disclosures] on the material climate-related risks public companies face would serve both investors and capital markets.”

The proposal, adopted on a 3:1 Commission vote, broadly aligns with the TCFD framework and the GHG Protocol, and requires companies to report on three areas:

- Oversight and governance of climate-related risks by the company’s board and management, including how oversight is exercised, and climate-related expertise.

- Carbon footprinting for Scopes 1, 2, and, for many, Scope 3 emissions, with Scope 3 required “if material or if the registrant has set a GHG emissions reduction target or goal that includes its Scope 3 emissions.” For large companies (accelerated filers), audit assurance and attestation is required for Scopes 1 and 2.

- Climate-related risks, including physical and transition risks, that are reasonably likely to have a material impact on a public company’s business, results of operations, or financial condition.

Assuming the SEC proceeds as scheduled, the implementation timeline will move US corporate reporting ahead of Europe’s Corporate Sustainability Reporting Directive (CSRD), resulting in multi-directional spillover of corporate disclosure across regions.

What many hope for: The ISSB

The formation of the International Sustainability Standards Board (ISSB) was announced in November 2021 at COP26, the United Nations’ global summit to address climate change. ISSB consolidates several different initiatives, notably the Climate Disclosure Standards Board (CDSB) and the Value Reporting Foundation, which in turn combines the Integrated Reporting Framework and SASB Standards.

ISSB is developing standards that aim to become a global baseline for sustainability disclosures with a focus on how to meet the information needs of financial actors. Likewise, companies can use it as a point of departure on what information on sustainability to provide to global capital markets.

ISSB aspires to provide a global baseline for different jurisdictions developing their own reporting requirements additional to the baseline. While reporting requirements would not end up being the same everywhere, the objective is to improve the availability of a key set of metrics across geographies.

In March 2022, the ISSB published two exposure drafts of IFRS sustainability disclosure standards, one covering general sustainability-related financial information requirements; and the other focusing on climate-related disclosures. The latter proposes reporting standards covering disclosure of material information related to physical and transition risk as well as climate-related opportunities, incorporating TCFD recommendations and SASB-derived metrics.

Push is coming to shove

While regulation continues to move ahead, many responsible investors are not willing to wait for the implementation timelines to kick in. They are already forcing the hand of companies by means of litigation and active ownership.

Litigation

Investors and civil society are looking for more transparency and they are not necessarily willing to wait for regulation to take hold. An example is how climate change litigation continues to grow in importance. The cumulative number of climate change-related cases has more than doubled globally since 2015. Just over 800 cases were filed between 1986 and 2014, while over 1,000 cases have been brought in the last six years. Litigation that is aligned with climate goals is on balance seeing success, according to the Global Climate Litigation Report 2020 Status Report from UNEP, and there has been a run of important wins in the last 12 months, such as the Milieudefensie v. Shell case.

A classification of the type of cases being brought forward identifies six different clusters (see Figure 5), with greater disclosure, closely linked to questions about greenwashing, being one of them.

Figure 5: Climate Litigation Categories

Source: Global Climate Litigation Report, 2020

What does this mean for corporate and financial market actors? An increasing number of claims focus on financial risks, fiduciary duties, and corporate due diligence, which directly affect not only fossil fuel and cement companies, but also banks, pension funds, asset managers, insurers, and major retailers, among others.

An example is McVeigh v Retail Employees Superannuation Pty Ltd, which concerns a member of a super fund known generally as “Rest,” who claimed the fund was in breach of Australia’s Corporations Act 2001 due to a failure to provide information on how Rest was managing climate change risks. Although resolved in an out-of-court settlement in 2020, the case has set a strong precedent for acknowledging the material risk climate change poses for institutional investors.

The road ahead may very likely see climate change litigation continue to grow. But this is not the only lever used to push for climate-related transparency. Active ownership is seeing a marked rise as well.

Active ownership

Climate-related shareholder proposals and voting items at companies’ annual general assemblies are gaining traction. A deep dive into the topic of climate change and voting is offered in a recent ISS publication. Three trends stand out: the number of shareholder proposals on environmental and social topics is increasing; all indicators point towards support for them being at an all-time high; and climate change concerns specifically are moving beyond shareholder proposals to be reflected in topics and voting decisions on other ballot items..

So, what are some of the specifics around these trends?

- In 2021 as in 2020, the majority of environmental and social-related shareholder proposals around the world were related to climate change and/or climate lobbying. More than half of the climate-related proposals were seen in the finance sector, the oil & gas sector, and the mining sector.

- Climate-related shareholder proposals were seen in 14 markets in 2021—Australia, Canada, Denmark, Finland, France, Japan, New Zealand, Norway, South Africa, Spain, Sweden, Switzerland, the United Kingdom, and the United States—compared to 12 markets in 2020. There were 88 climate-related shareholder proposals that were voted on in 2021 compared to 65 in 2020.

- Shareholder proposals requesting disclosure of emissions reductions goals remained one of the most common types of climate-related proposal in 2021. Globally, the average level of support received by these proposals was 42.1 percent in 2021, up from 29.2 percent in 2020. Shareholder proposals requesting “Say on Climate” votes received an average of 32.7 percent support in 2021.

The activity is—at least anecdotally—having an effect. One example is a recent account from the New York State Common Retirement Fund linked to climate actions taken by eight companies. The fund, one of the largest of its type in the US, put forward proposals at 10 companies related to climate change investment risk, in sectors as diverse as construction materials, manufacturing, natural gas, and food production.

According to the fund, agreements with eight companies were reached relating to areas ranging from target setting, to increased reporting of companies’ impact on the environment, to transparency on how the impact from the International Energy Agency’s Net Zero by 2050 scenario might play out.

Implications for the Finance Industry

With such a host of dynamics in play, where do companies stand on disclosure? And what might finance industry actors do to stay ahead of the curve?

Are companies prepared?

The short answer is “somewhat.” Disclosure has generally increased in recent years. The number of companies disclosing their Scope 1 and 2 emissions has seen a clear rise, most notably among larger companies. For example, 85% of companies in the S&P 500 but only 31% of companies in the Russell 3000 have disclosed Scope 1 and 2 emissions. Those figures are 70% and 21% for the two indices respectively when it comes to Scope 3 emissions.

This shows that even on Scope 1 and 2 emissions, one of the most fundamental metrics when it comes to climate change, greater disclosure is possible. Increased disclosure on climate target setting and climate risk assessments and management is also possible.

For example, only 21% of companies in the S&P 500 have disclosed a climate change target that has been approved by the Science Based Targets initiative (SBTi). Of emissions-intensive utility companies, which contribute more than a third of the Scope 1 and 2 emissions associated with the index, more than 60% are considered to be not currently aligned with Net Zero targets. Within the STOXX600, only one in every 16 emissions-intense materials companies has taken credible initial steps to align with Net Zero, and the same holds true for less than one-fifth of emissions-intense industrial companies.

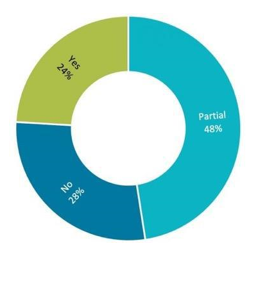

Even among the more than 160 companies that feature as the world’s largest emitters of greenhouse gases and are monitored by the investor initiative Climate Action 100+, only 24% have set climate targets for the period 2026-2035 that meet criteria such as compliance with a 1.5°C climate target (see Figure 6).

Figure 6: Comprehensiveness of the Net Zero goals (2026-2035) of Climate Action 100+ Companies

Source: ISS ESG

Based on such analysis, there is clearly much to do. Where are financial actors on the spectrum of action?

Are financial actors ready?

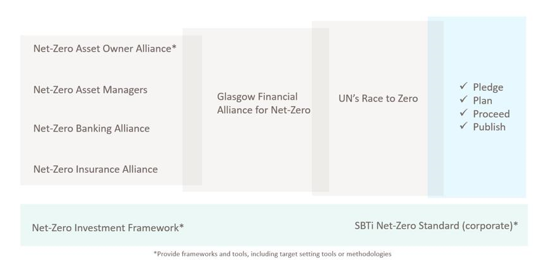

A rising tide of Net-Zero pledges and Net Zero action is gaining momentum in the financial world, too. The finance sector, often regarded as the blood supply for the economy, is uniquely positioned to be part of this shift and benefit from the opportunities offered by the transition to a low-carbon economy.

For investors, the journey starts with commitment. Many Net Zero initiatives have developed, encompassing all levels of society and industry: an overview of some of the key ones is provided in Figure 7. Especially notable are the Net-Zero Asset Owner Alliance and the Net-Zero Investment Framework, as they provide some of the most specific frameworks and guidance on how to set and implement such targets.

Figure 7: Overview of Net-Zero Initiatives

Source: ISS ESG

From a practical perspective, Net Zero requires accelerated decarbonization across sectors and countries while recognizing that this will happen at different rates. With such unprecedented transition opportunities, enormous investment is needed in climate solutions, with the International Monetary Fund (IMF) and the International Energy Agency (IEA) estimating that over $4 trillion average annual capital investment in clean energy will be required by the 2030s for the energy sector alone.

What remains to be seen is whether current efforts result in hitting the target but missing the goal. Transparency is not the objective in and of itself, decarbonizing the real economy is. To be effective, efforts to foster the right type of transparency would need to be combined with efforts to ensure that evasive movements do not obstruct the intended goal.

The right transparency

Metrics can obscure as much as they can elucidate. Asking for the right type of metrics will thus be key. GHG footprinting was once regarded as the solution to measuring finance’s impact on the climate. This method did not tell investors about the climate strategy of portfolio companies, however, or give details on their product portfolio. Now an investment GHG footprint is very reasonably advocated as more of a gauge of where a portfolio is headed with respect to the climate goals.

Another approach claims to be able to determine the specific global warming “temperature metric” that a company’s activities are aligned with, with some offering estimates to two decimal points. Given the uncertainty in both the forward-looking projections (no one can claim to know how the world ultimately develops and climate scenarios are continuously adjusted) and the input data (the same emissions budgets are associated with a range of warming potentials and company reporting still needs to improve), temperature scores are a classical example of a type of transparency that might harm as much as it helps. That being said, the development of easily communicable scores and metrics is important.

The conclusion: a metric that is helpful for certain use cases does not necessarily serve others. Transparency needs to focus on key raw data points for consumption in different use cases.

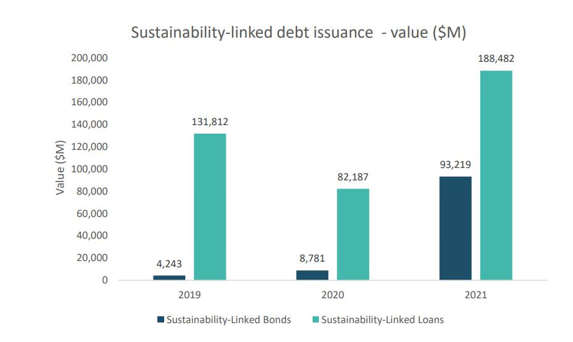

A focus on individual market segments might also obscure other relevant areas. Listed companies have received most of the attention, which is understandable: they are owned by the public, many of them belong to some of the largest companies in their sectors, and their economic importance continues to increase. But while sustainable bonds have been the focus of debate and scrutiny, a significant portion of sustainable financing in debt markets happens in the much less transparent lending market.

Figure 8: Issuance Values for Sustainability-linked Bonds and Loans

Source: Environmental Finance Data

Bringing transparency to the currently less scrutinized areas of finance, whether it be lending, real assets, or private equity, will therefore offer a significant expansion of visibility of climate risk for the investor.

Focusing on real world outcomes

Transparency will also play a key role in ensuring real world outcomes that arise from investor action on climate.

With scrutiny being dialed up in the public markets, there is a risk that emissions-intense assets are simply sold off to private actors. From a climate action perspective, it would be preferable if (for instance) companies that are reducing their exposure to fossil fuel extraction are not simply selling their ownership to other actors that might continue to produce fossil fuels, but instead retain ownership and phase out and ultimately end such production.

By the same token, Net Zero frameworks targeted at the finance industry need to stay laser focused on real world outcomes versus “virtual” emission reductions that result from simply reducing exposure to emissions-intense companies. The question on how best to achieve this is also reflected in the “divestment versus engagement” debate.

The fossil fuel divestment movement has played a critical role in raising investor awareness about climate risk, and while divestment is a useful tool for aligning a fund with stakeholder values, there is a risk that the underlying activities of the divested companies are not influenced. Engagement and stewardship activities are playing an increasingly important role.

This is reflected in different ways. One element to take note of is the focus on engagement in various climate initiatives as shown in Figure 9 below. In the UK, an All-Party Parliamentary Group on ESG has issued a report to policymakers with recommendations on standardizing and regulating ESG performance and disclosure. Recommendations include the development of frameworks for responsible divestment, on the grounds that divestment can reduce the ability of an investor to encourage improvements in an asset’s social and environmental performance. Similarly, Japan’s Government Pension Investment Fund (GPIF), managing $1.36 trillion in assets, and Norway’s $1 trillion Government Pension Fund Global have underscored the merits of engagement.

Figure 9: Finance Sector Climate Initiatives and Engagement

Source: ISS ESG

Who to pay attention to?

Investor action on climate change is on the one hand straightforward (shoot for Net Zero!) and on the other quite complex (as illustrated in the discussions above). Here are three ways that financial actors can stay on top of the game:

- Governance, governance, governance. Climate competency within boards, explicit structures for oversight, and clear responsibilities for climate strategy and risk management can promote a Net Zero goal.

- Prioritise real world outcomes over “virtual” emission reductions. Prioritising real world outcomes can contribute to a climate transition that avoids climate change’s systemic physical and transition risks.

- Again: Transparency. In the absence of an established transition pathway to Net Zero for a large number of corporations, investors may find transparency (including acknowledgment of the many unknowns) about what they can achieve to be useful.

The complete publication is available here.