Print

PrintMolly Stutzman is Analyst of Corporate Research, Laura Thornton is Junior Analyst, and Matthew Nestler is Senior Manager of Workplace Policies Research at JUST Capital. This post is based on their JUST Capital memorandum. Related research from the Program on Corporate Governance includes The Perils and Questionable Promise of ESG-Based Compensation by Lucian A. Bebchuk and Roberto Tallarita (discussed on the Forum here); and Paying for Long-Term Performance by Lucian A. Bebchuk and Jesse Fried (discussed on the Forum here).

Key Findings

Customers, employees, shareholders, and other stakeholders, are increasingly expecting companies to tackle environmental, social, and governance (ESG) issues. That includes the American public. In our 2021 survey of the People’s Priorities, “The board of directors holds executives accountable to the interests of its workers, customers, communities, and the environment, as well as shareholders,” emerged as the third-most important Issue to the public, representing over 10% of our Rankings model.

And, as pressure has increased, so have corporate disclosures showing board oversight of ESG efforts. Our analysis of three data points on board oversight of ESG issues, covered under the Shareholders and Governance stakeholder, has led to two key findings. First, disclosure on these data points is steadily increasing. Almost a fifth of companies in the Russell 1000 Index report all three ESG governance data points we measure in 2022—up from around a tenth in 2020. Second, the Oil & Gas, Utilities, Energy Equipment & Services, and Chemicals industries have a much larger percentage of companies disclosing on all three ESG governance data points than other industries.

Board Oversight of ESG from 2020-2022: Unpacking the Rise in Disclosure

As proxy season kicked off last month, Mastercard made headlines with a decision to link ESG goals with bonus calculations for employees at all levels. The company had previously tied these metrics to compensation for senior-level executives, incentivizing leaders to be accountable to all their stakeholders and not merely shareholders. And while this remains a growing trend as median CEO pay sees another record-setting year, this latest move marks a deeper degree of incorporating ESG into how the company operates. Mastercard’s shift also comes as corporate America faces challenges from investors over policies and practices related to climate change, racial equity, political contributions, and other ESG issues.

Shareholders have filed a record number of ESG proposals this proxy season, with U.S. companies facing over 500 resolutions on ESG issues. This increased momentum comes alongside a push from the U.S. Securities and Exchange Commission (SEC) to mandate climate-related disclosures, a move the majority of the American public (86%) JUST Capital recently polled support. In fact, our survey found that Americans overwhelmingly want greater transparency from companies on ESG metrics—and this holds true across the political spectrum as backlash against ESG grows more prominent.

These stakeholders are all signaling that corporate statements and commitments on ESG are no longer enough. They want to see how executives are translating their commitments around prioritizing ESG into how they govern their businesses. Corporate governance, the “G” of ESG, is a crucial driver of a company’s overall sustainability efforts. Since 2020, JUST Capital has tracked corporate performance in our Shareholders and Governance stakeholder on three issues:

- Prioritizing accountability to all stakeholders.

- Acting ethically at the leadership level.

- Generating returns for investors.

Russell 1000 companies are required to report many financial and governance data points to the SEC that underlie the above issues. However, JUST Capital tracks three data points, which are not mandated but help assess a company’s prioritization and oversight of ESG topics. These data points, which collectively make up the “board oversight of just issues” metric, are:

- If the company links ESG risks and performance to executive compensation.

- If the company includes ESG key performance indicators in compensation metrics.

- If the company’s board has a formal schedule to discuss environmental, social, and health and safety matters.

Disclosure on ESG governance data points is steadily increasing

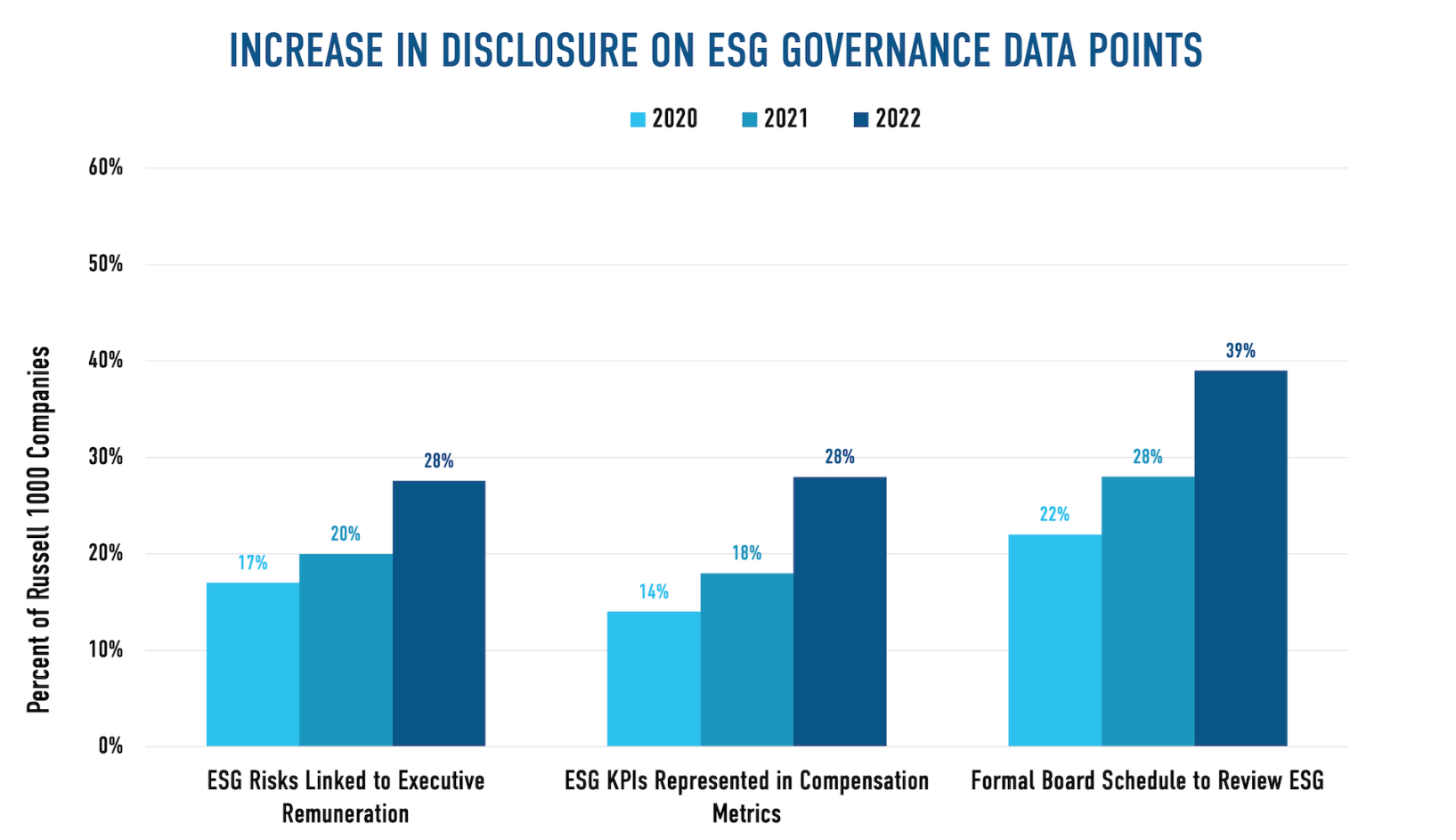

Figure 1. Year-over-year disclosure on data points. Analysis based on data from JUST Capital’s 2020, 2021 and 2022 Rankings.

From 2020-2022, companies in the Russell 1000 steadily increased their disclosures, with a more significant jump, about 10 percentage points, between 2021 and 2022 and slower growth between 2020 and 2021 (Figure 1). At present, boards are more likely to discuss and review progress on environment, social and health and safety topics (that is, they have a formal board schedule to review ESG) than to tie ESG metrics to compensation. This may signal the nascent place many companies are in their ESG and sustainability journeys and an implicit level of prioritization among companies in their planning and action on ESG issues.

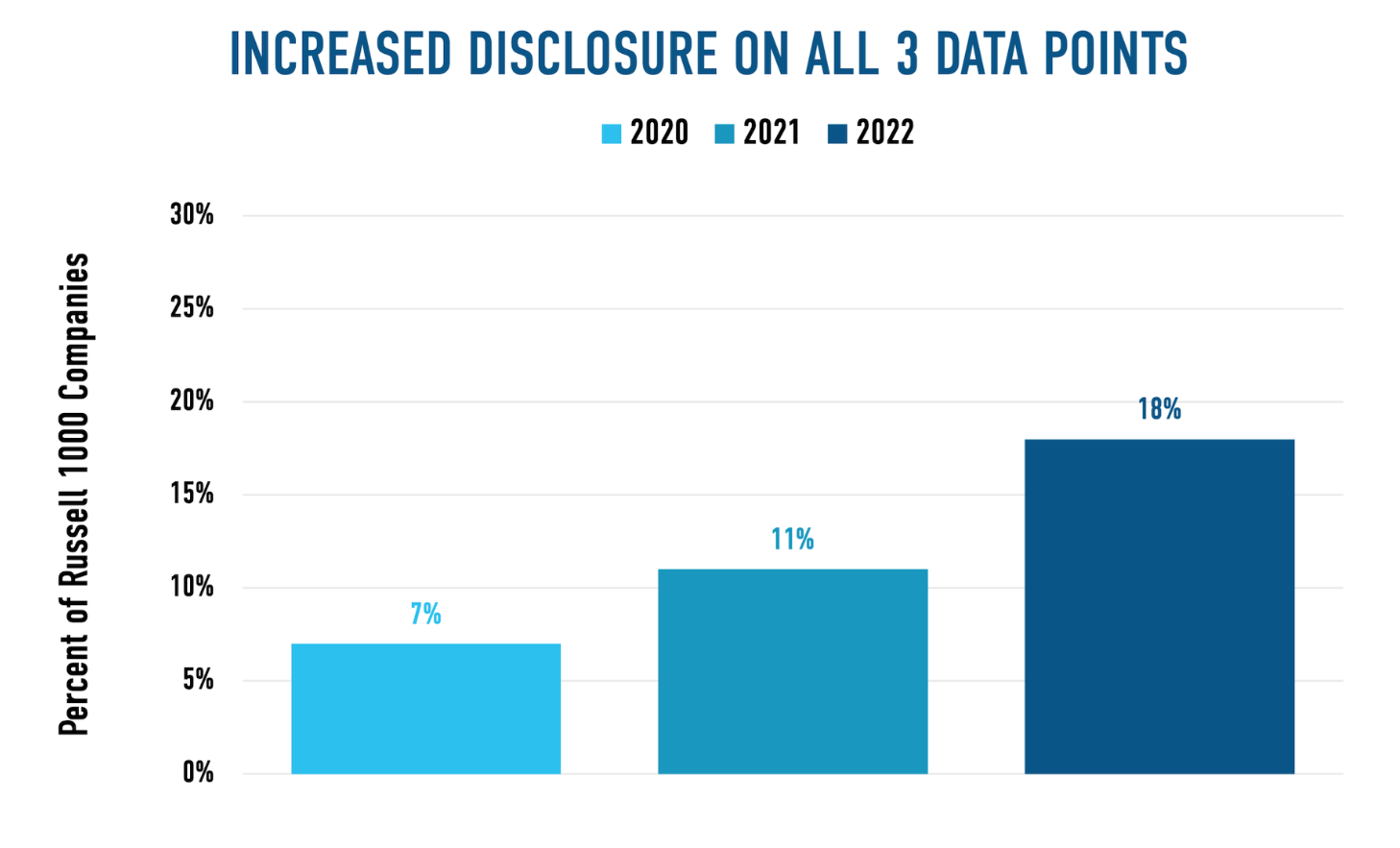

Figure 2. Percent of companies that disclose all three data points. Analysis based on data from JUST Capital’s 2020, 2021, and 2022 Rankings.

In addition to the rise in disclosure of each data point, the percentage of companies within the Russell 1000 that disclose on all three data points from 2020-2022 has also increased (Figure 2). Though these three ESG data points are related, as of 2022 fewer companies report on all three than on the lowest-disclosed data point (shown in Figure 1).

Oil & Gas, Utilities, Energy, and Chemicals industries have higher rates of disclosure

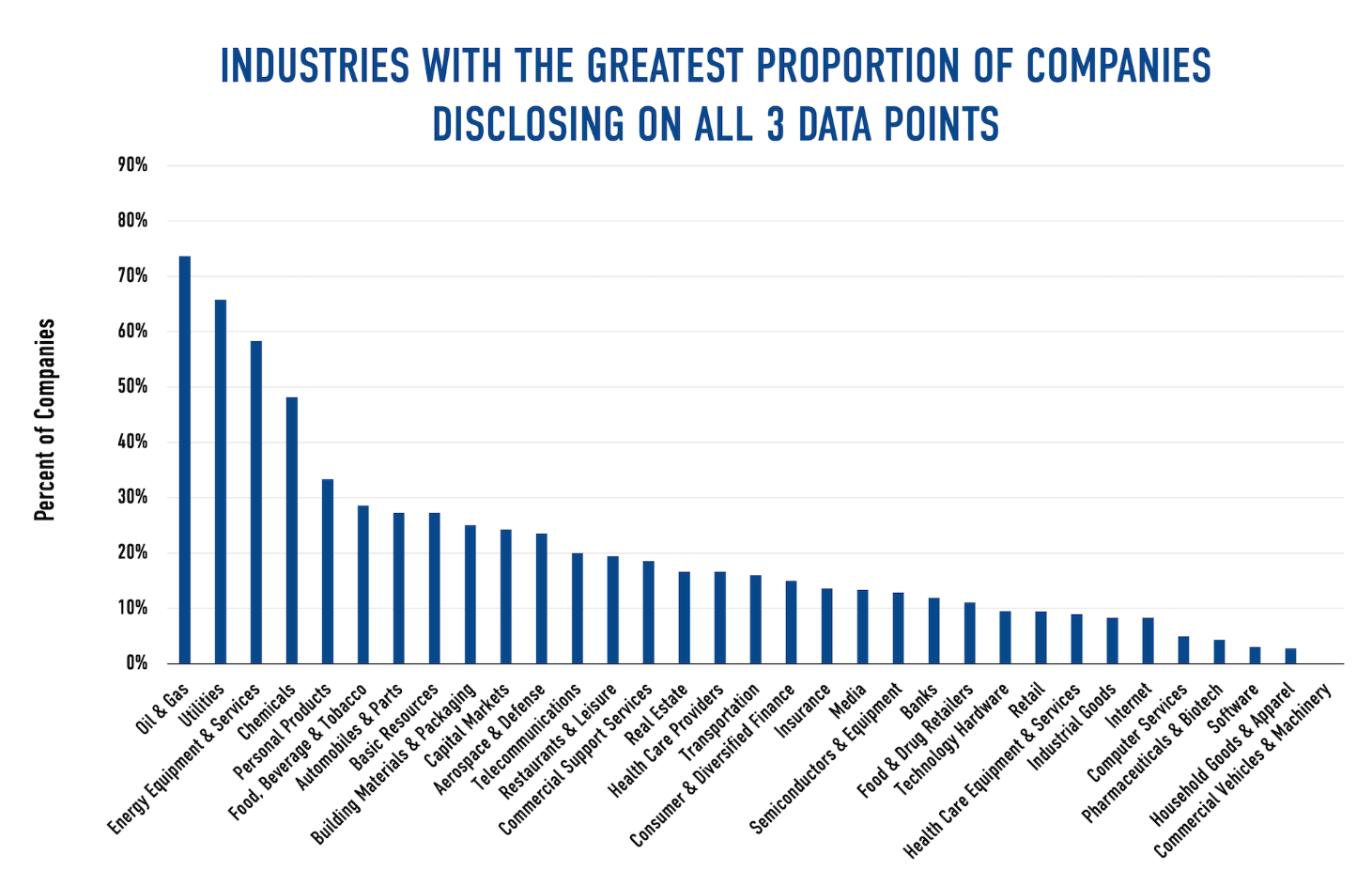

Figure 3. Industries with the largest percent of companies that disclose all three data points. Analysis based on data from JUST Capital’s 2022 rankings.

Our analysis found that the percentage of companies within each industry that disclose all three ESG data points ranges from 0-74%. The four industries with the greatest percentage of companies disclosing on all three are Oil and Gas (74%), Utilities (66%), Energy Equipment and Services (58%), and Chemicals (48%). Within these four industries, an average of 61% of companies disclose all three data points, compared with the remaining 29 industries, which average 15% of companies disclosing all three.

Companies in industries with business models that are environmentally intensive, and which often face public and private scrutiny, have notably higher levels of disclosure on these governance policies. Higher disclosure levels in these industries may be partly due to investor engagement on environmental issues. As climate change is increasingly recognized as a risk to long term financial performance, corporate boards face increasing pressure from asset managers and investors to review their companies’ impact on the environment and incentivize executives to make progress on sustainability targets by incorporating those goals into compensation plans.

At the beginning of this year, BlackRock, Vanguard, and State Street Global Advisors included guidance for board oversight of climate risks in their 2022 proxy season voting priorities. Climate Action 100+, the largest climate-related investor initiative, focuses on many companies in the Oil & Gas and Utilities sectors and engages with their boards and senior leadership to make progress on climate issues. Part of its disclosure framework includes climate governance, where companies are asked to report on their board’s oversight over climate change and the incorporation of climate change KPIs in determining compensation for executives.

As is the case with many ESG metrics, one of the main challenges to measuring transparency on ESG governance is a lack of standardization. The sustainability metrics companies link to compensation are somewhat vague and qualitative, making it challenging to assess if compensation incentives are effective drivers of performance. If boards want to incentivize progress on these issues, they must identify specific and measurable indicators as opposed to broader objectives. More specific, standardized, and quantitative performance targets for executives would allow investors and other stakeholders to better measure and determine the efficacy of these policies.

ESG issues like climate and diversity are in no way waning and stakeholders are going to continue to look to companies to show material accountability to their ESG commitments. Coming out of proxy season, JUST will continue to monitor how companies respond to this pressure—and whether that translates into greater board oversight and execution of ESG policies and practices.