Print

PrintJessica Ground is Global Head of ESG at the Capital Group. This post is based on her Capital Group memorandum.

Executive summary

ESG adoption is on the rise, fuelled by client demand and a desire to make an impact. As ESG momentum continues to gain steam, investors are refining and evolving their strategies. This can be seen in the implementation arena, where investors are moving away from basic screening methods towards more targeted and sophisticated strategies, including thematic and impact investing. Meanwhile, ESG integration remains the top implementation strategy — showing how investors are taking a holistic approach as they look to comprehensively embed ESG into the investment process.

This rigorous approach is also evident in the strong bias towards active strategies. Nearly two-thirds prefer active funds to integrate ESG. Investors therefore want managers to use active security selection to uncover ESG opportunities and active ownership to engage and influence investee companies.

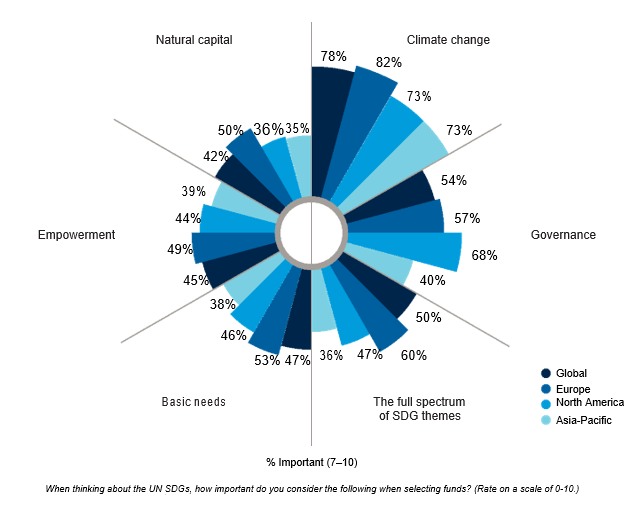

The increasing sophistication of ESG investors can also be seen in attitudes to the UN Sustainable Development Goals (SDGs). Almost a third say the ability to report on specific SDGs is one of the most important elements of fund sustainability reporting — nearly double last year’s percentage. And half say the ability to offer the full spectrum of SDG themes is important when selecting funds.

Crucially, as investors expand their ESG knowledge base, they increasingly recognise that companies with good sustainable credentials are more likely to outperform. Fewer investors this year point to sacrificing returns as an adoption hurdle. And more are now investing in ESG with the specific and sole remit of generating alpha. Furthermore, investors largely agree that investment returns and sustainable impact go hand in hand.

But as investors become more knowledgeable and familiar with ESG, they are becoming more cognisant of the challenges. Data challenges continue to be a critical issue that manifests throughout the investment process. Difficulties with the quality and accessibility of data and inconsistent ratings are hampering the ability of investors to adopt, incorporate and implement ESG.

These issues also present themselves to fixed income investors who identify a lack of standardisation across ESG bond ratings as the top barrier.

Such difficulties are compounded by the fact that investors face an information overload as they swim against a tidal wave of ESG data.

It is therefore essential that investors seek help from active managers who possess the specific tools, skill sets and resources to address these challenges. Using proprietary research and fundamental analysis, active managers can bypass the problems created by superficial scoring systems and a lack of consistent and reliable data.

The support of asset managers is paramount as the knowledge paradox plays out — the more investors know about ESG, the more they realize what they don’t know and the more help they need. Indeed, a third of investors say ongoing ESG education and training from their employer would help with ESG analysis and implementation. This skills gap presents an opportunity for asset managers to forge closer ties with investors through the provision of educational materials and resources.

ESG momentum

Growing adoption

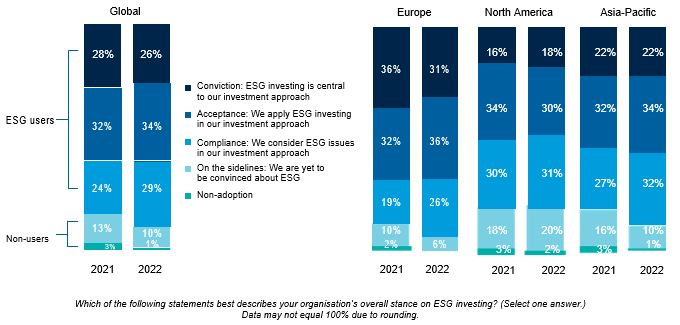

This year’s study shows continued momentum towards ESG. As with 2021, more than a quarter of global investors say ESG is central to their investment approach (26% vs. 28% in 2021). But a higher proportion this year describe their ESG stance as one of “acceptance” (34% vs. 32%) and “compliance” (29% vs. 24%).

Furthermore, the numbers of non-adopters (1% vs. 3%) and those “on the sidelines” (10% vs. 13%) have declined. Altogether, this brings the proportion of global ESG users to 89%—up from 84% in 2021.

Europe continues to lead the ESG charge. More European investors say ESG is central to their investment approach (31% vs. 18% North America, 22% Asia-Pacific). Europe also boasts the highest percentage of ESG users (93% vs. 79% North America, 88% Asia-Pacific). This reflects the more mature European ESG market and regulatory framework. The North America region, by contrast, has the least conviction in ESG and the lowest percentage of ESG users.

ESG adoption levels

“Sustainability and ESG are at the very heart of all our investment decisions,” says a portfolio manager at a UK pension fund.

Conviction in ESG is further underscored in the finding that just 13% of global investors agree ESG is a passing fad that will go out of fashion. This demonstrates how most investors view ESG as a permanent and pre-eminent part of the investment landscape.

“Sustainability and ESG are at the very heart of all our investment decisions,” says a portfolio manager at a UK pension fund. “It’s been a core principle ever since I joined my company.”

Strong conviction in ESG

Momentum drivers

“Client demand is a big factor. Clients are increasingly asking for investments in renewable energy and investments targeting Sustainable Development Goals,” says a portfolio manager at a German private bank.

The increasing ESG momentum is being fuelled by client demand and external pressures. More global investors this year say their approach to ESG is driven by client expectations and reputational concerns (42% vs. 37% in 2021).

“Client demand is a big factor. Clients are increasingly asking for investments in renewable energy and investments targeting Sustainable Development Goals,” says a portfolio manager at a German private bank. “ESG is also big in the media and that plays a large influence.”

A UK pension fund portfolio manager echoes the central role played by client demand:

“Investors are very specific in their needs, which is something that’s only really occurred in the last six to 12 months. Before that, it was us driving the process, but now it’s clients and investors who are asking for the products.”

The centrality of client needs

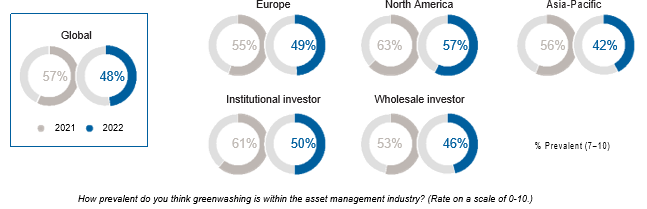

Another factor driving ESG momentum is reduced concern about greenwashing, giving investors more trust and confidence to invest sustainably. This year, less than half of global investors think greenwashing is prevalent within the asset management industry (48% vs. 57% in 2021). The perceived prevalence of greenwashing has dropped across all regions, but most markedly in Asia-Pacific (42% vs. 56% in 2021).

Perceived prevalence of greenwashing

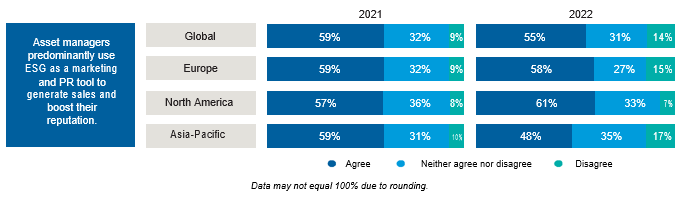

As a further ESG impetus, investors are also less sceptical about the motives of asset managers. Fewer this year think asset managers mainly use ESG as a marketing and PR tool to generate sales (55% vs. 59% in 2021). The falling trend is most apparent in the Asia-Pacific region (48% vs. 59% in 2021).

Views on asset manager motives

The climate change debate

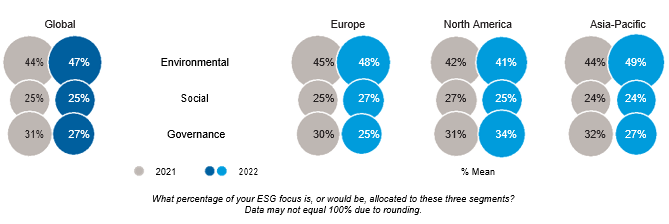

The continued dominance of the environmental element of ESG shows how climate change concerns are at the forefront of investor minds. Investors again allocate most of their focus to the E component of ESG, which has slightly increased its share from last year (47% vs. 44% in 2021). Global allocations to the S segment of ESG remain unchanged, while the focus on G has marginally decreased.

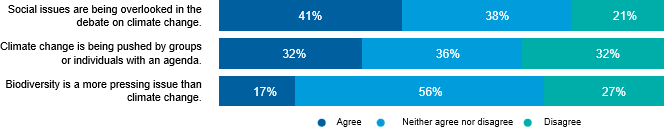

While climate change is clearly a top agenda item for ESG investors, a strong minority of investors think the focus on climate change is distracting from other issues. Four in 10 (41%) think social issues are being overlooked in the climate change debate. And climate change is still proving a politically charged issue for some. As with last year, about a third think climate change is being pushed by groups or individuals with an agenda (32% vs. 31% in 2021).

Views on climate change

Implementing ESG

Active strategies

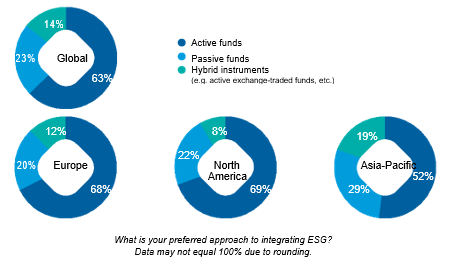

The strong bias towards active strategies when investing in ESG is again noticeable this year. Nearly two-thirds (63%) of global investors prefer active funds to integrate ESG. This demonstrates how investors want active managers to identify and manage ESG opportunities and risks through bottom-up security selection and fundamental analysis. It also shows how investors see active ownership as key to engaging with, and influencing the activities of, investee companies. Active funds are most popular among North American (69%) and European (68%) investors.

Integrating ESG

The allure of alternatives

“Since the end of last year we’ve been looking for alternative investments to attend to the problem of inflation, which has been relatively high in the euro area,” says a portfolio manager at a German private bank.

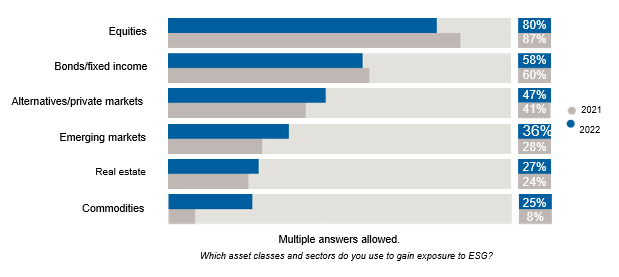

Equities (80%) and bonds (58%) remain the most popular asset classes to gain exposure to ESG among global investors. But this year, investors have increased their usage of alternatives (47% vs. 41% in 2021), real estate (27% vs. 24%) and particularly commodities (25% vs. 8%). This indicates stronger appetite for inflation-linked assets. While inflation has been rising since 2021 as economies emerge from the pandemic and struggle with supply-chain shortages, the crisis in Ukraine has exacerbated this trend.

“Since the end of last year we’ve been looking for alternative investments to attend to the problem of inflation, which has been relatively high in the euro area,” says a portfolio manager at a German private bank. “And events in Ukraine have made the situation worse, so it’s even more important now to have products that allow clients to protect their purchasing power.”

Emerging markets are also a more popular way to gain exposure to ESG (36% vs. 28% in 2021). This may indicate that some investors see developed-markets ESG as a crowded space and are searching for untapped, idiosyncratic opportunities further afield.

ESG asset classes

Integration seen as integral

“I think impact investing is another step on from ESG,” says a portfolio manager at a UK wealth management company.

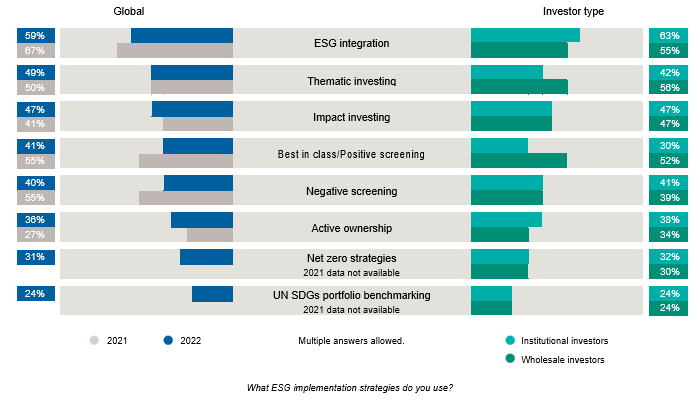

ESG integration, cited by almost six in 10 (59%) global investors, remains the most used implementation strategy. This illustrates how investors are taking a holistic approach as they look to comprehensively embed ESG into the investment process. Institutional investors are more likely to deploy ESG integration (63% vs. 55% wholesale).

The next most popular strategies are thematic investing (49%) and impact investing (47%). This marks a change from last year, when positive screening and negative screening were the second and third most popular implementation strategies respectively. Usage of these screening strategies has declined from over half of investors in 2021 to four in 10 this year.

These results show how investors are refining their approach as they move away from basic screening methods towards more targeted and sophisticated strategies.

“I think impact investing is another step on from ESG,” says a portfolio manager at a UK wealth management company. “Impact investing relies on a heavy emphasis on engagement and stewardship and also divestment.”

Elsewhere, about a third of global investors deploy net zero strategies (31%) and a quarter use UN Sustainable Development Goal (SDG) portfolio benchmarking (24%) when implementing ESG.

“Our organisation has a mandate to follow the SDGs, so we are incorporating that into our implementation strategy,” says an investment manager at a Canadian insurance company.

Implementing ESG

ESG challenges

Adoption barriers

Having examined the main adoption drivers, we now look at the hurdles preventing organizations from adopting or further adopting ESG. As with last year, a lack of robust data, cited by four in 10 investors, is seen as the greatest adoption barrier (40% vs. 49% in 2021).

“The big issue for us is we have regulations in all these different parts and we have to peg it to one framework,” says a senior portfolio manager at a German wealth management firm.

Worries about sacrificing returns is the second-biggest barrier. But far fewer investors cite the performance hurdle this year compared to 2021, when it was the joint-biggest barrier (35% vs. 49% in 2021). Performance worries present an even lower hurdle for wholesale investors (28%). Falling concerns about performance again align with the earlier finding that respondents see investment returns and sustainable impact as mutually beneficial.

Furthermore, investors seem less concerned about returns at the very time ESG investments, which tend to have a growth and quality bias, have had to contend with rising inflation and the rotation to value. This suggests investors are looking beyond short-term volatility and seeking to capture long-term structural ESG trends.

The third-biggest adoption barrier is concern over greenwashing, which has increased from 22% in 2021 to 30%. Investor views are therefore somewhat mixed on greenwashing. While fewer investors this year think greenwashing is prevalent and fewer think asset managers use ESG as a marketing and PR tool, more see it as an adoption barrier.

These top three ESG adoption barriers pose more of a challenge for investors in North America. A higher percentage flag concerns about a lack of robust ESG data (46%), sacrificing returns (49%) and greenwashing (37%) in North America than in other regions. This helps explain why North American investors have the least conviction in ESG and why the region has the lowest percentage of ESG users.

Biggest ESG adoption hurdles

Meanwhile, nearly three in 10 investors point to the challenge posed by a complex and confusing regulatory landscape (27% vs. 24% in 2021). This presents a higher adoption barrier for European investors (31%).

A senior portfolio manager at a German wealth management firm says a triple whammy of European rules, including the Sustainable Finance Disclosure Regulation (SFDR), taxonomy and Markets in Financial Instruments Directive, are creating a significant regulatory burden:

“The big issue for us is we have regulations in all these different parts and we have to peg it to one framework to handle. And that’s a real challenge as all these single regulations are different.”

Data difficulties

As we have seen, a lack of robust data is again regarded as the biggest adoption barrier. But data difficulties manifest throughout the investment process. Difficulties with the quality and robustness of data and inconsistent scores are hampering the ability of investors to adopt, incorporate and implement ESG.

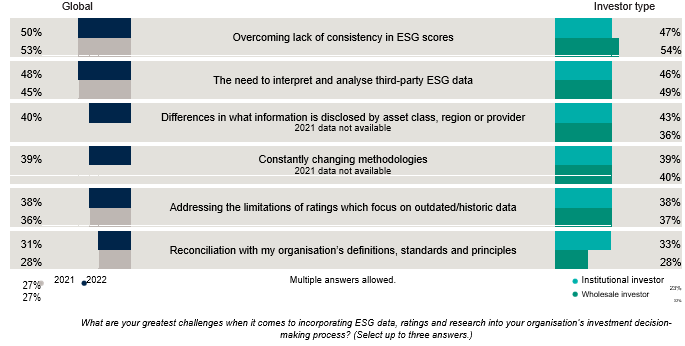

Overcoming the lack of consistency in ESG scores, cited by half (50%) of investors, remains the biggest headache when incorporating ESG data, ratings and research into the investment decision-making process. This is followed by the need to interpret and analyse third-party ESG data (48%) and differences in what information is disclosed by asset class, region or provider (40%).

Overcoming inconsistent ESG scores is more challenging for wholesale investors (54% vs. 47% institutional). Institutional investors, on the other hand, are more challenged by differences in information disclosed by asset class, region or provider (43% vs. 36% wholesale).

Challenges with incorporating ESG data

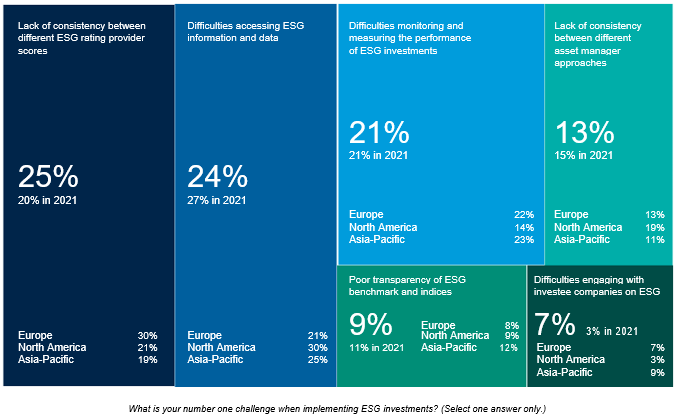

Consistency issues also loom large in the implementation stage. Global investors say their number one challenge when implementing ESG investments is lack of consistency between different ESG rating provider scores (25%). This marks a change from last year, when difficulties accessing ESG information and data were the main implementation challenge. This is now seen as the second-biggest challenge (24%), followed by difficulties monitoring and measuring the performance of ESG investments (21%).

Highest implementation hurdles

Concern about a lack of consistency between rating provider scores is more pronounced among European investors (30% vs. 21% North America, 19% Asia-Pacific). And difficulties accessing ESG information and data are more of a challenge for investors in North America (30% vs. 21% Europe, 25% Asia-Pacific).

Skewed scores

“ESG is a lot of things to a lot of people,” says the CIO at an Italian independent advisory firm. “I mean everyone looks at what is compatible with ESG from different angles and arrives at different conclusions.”

Inconsistent and inaccurate ESG scores result from a multitude of factors. These include backward-looking data that fails to adequately assess the future value of transitioners and identify tomorrow’s ESG leaders. The subjective nature of scoring systems also means there are varying views on the relative importance and material impact of different ESG factors in different sectors and countries.

“There is huge dispersion among the ratings of different third-party ESG providers,” says the CIO at an Italian independent advisory firm. “ESG is a lot of things to a lot of people. I mean everyone looks at what is compatible with ESG from different angles and arrives at different conclusions.”

These challenges with inconsistent, subjective-based ratings underscore the importance of active managers who can use fundamental analysis to identify a company’s intrinsic or true ESG value. By using proprietary research and rigorous security selection, active managers can bypass the problems created by superficial scoring systems and a lack of consistent and reliable data. This approach is especially useful when analysing companies with small market capitalisations, where active managers can deploy a labour-intensive process to sift through a large universe of smaller and less-researched companies.

Entrusting asset managers with the research and analysis function also relieves the burden on investors facing an information overload from a rising tide of ESG data.

A bond of sustainability

Issues over data, consistency and ratings also present themselves to fixed income ESG investors. Global investors identify a lack of standardisation across ESG bond ratings (58%) as the top barrier when investing in fixed income ESG funds. This is followed by concerns about the premium on green bonds (45%) and complexity of ESG bond fund covenants (43%).

Asia-Pacific investors are more likely to be held back by the so-called “greenium” when green bonds are issued at higher prices (54% vs. 33% North America, 43% Europe). Complexity of ESG bond fund covenants pose more of a challenge to Asia-Pacific (47%) and European (46%) investors compared to their North American (27%) counterparts.

As ESG bonds expand across different countries and industries, their sustainable objectives are broadening beyond the environmental sphere. This growth has been supported by new taxonomies and frameworks to improve transparency and disclosures.

But investing in ESG bonds can be a complex and arduous undertaking. The same company may issue a number of ESG bonds financing different projects and carrying different ratings. And while the absence of voting rights makes it harder for investors to influence the activities of issuing companies, engagement challenges render it more difficult to monitor use of proceeds. Such challenges make it imperative for ESG fixed income investors to use active managers who can deploy active engagement and rigorous risk management to break down these bond barriers.

Fixed income barriers

Data solutions

While data perhaps presents the biggest headache for investors, it can also offer the best remedy. Indeed, when investors are asked what would help with ESG analysis and implementation, the top three answers are all data related. Almost six in 10 (58%) say the standardisation of tools and data from different providers would help their organisation better analyse and implement ESG factors. This is followed by consistent data from asset managers (50%) and more automated analysis tools for ESG data (39%).

A significantly larger percentage of North American investors say the standardisation of provider tools and data would aid the analysis and implementation of ESG factors (70%). And compared to other regions, a slightly higher number of North American investors say consistent data from asset managers would help with ESG factor analysis (53%).

Interestingly, a third (33%) of investors say ongoing ESG education and training from their employer would help with ESG analysis and implementation. This finding shows that investors want to improve their ESG knowledge. It also hints at a skills shortage. This presents an opportunity for asset managers to forge closer ties with investors through the provision of educational materials and resources.

What investors need to better analyse and implement ESG

Role of asset managers

Helping with net zero

Asset managers and the products they design are the chief facilitators of ESG investing. But apart from building funds enabling investors to allocate money to good causes, investors also want asset managers to support them on other parts of their ESG journey.

“It’s important that we can show client investments are actually doing those things they set out to do,” says a portfolio manager at a US RIA. “So we want to use data such as carbon footprints that allow us to show how an investment actually aligns with their goals.”

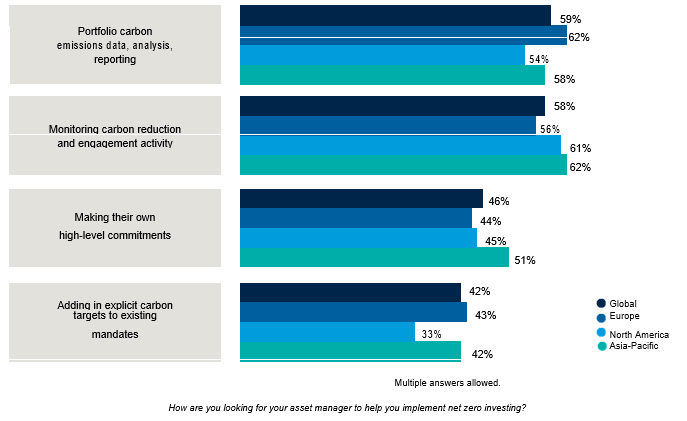

One important element of the ESG matrix where asset managers can provide additional value is support on net zero investing. And global investors say providing portfolio carbon emissions data, analysis and reporting (59%) is the best way asset managers can help them implement net zero investing. This is closely followed by monitoring carbon reduction and engagement activity (58%).

“I think, for investors, the documented numerical impact on specific metrics, such as carbon per dollar of revenue, is important,” says a portfolio manager at a Canadian pension fund. “It’s really all about having the right kind of disclosures to highlight the process and the outcomes of your ESG investments.”

A portfolio manager at a US RIA strikes a similar note: “It’s important that we can show client investments are actually doing those things they set out to do. So we want to use data such as carbon footprints that allow us to show how an investment actually aligns with their goals.”

The CIO of a family office in Singapore says, “Our core objective is investing into clean tech in Indonesia, so one of the key variables is the reduction in carbon emissions. We’re very big on climate change and clean energy.”

Aside from reporting and monitoring, investors also want asset managers to lead by example and demonstrate their own solid sustainable credentials. Nearly half (46%) say asset managers can help with net zero investing by making their own high-level commitments.

How asset managers can help with net zero

Fund sustainability reporting

Fund reporting is an essential part of the asset manager toolkit. Clear and transparent reporting can help investors deepen their ESG knowledge and commitment and ultimately drive more investment flows into sustainable causes.

As we saw earlier, greater transparency and consistency in ESG fund reporting is the prime factor encouraging investors to increase their ESG focus. In addition, as indicated on page 24, more than a third (35%) of global investors say more reporting from asset managers would help them analyse and implement ESG factors. This increases to four in 10 (39%) Asia-Pacific investors.

Detailed fund reporting is also seen as an effective antidote against greenwashing. The majority (52%) of investors say increasing the quality and transparency of fund literature is one of the best ways to tackle greenwashing, as shown on page 31.

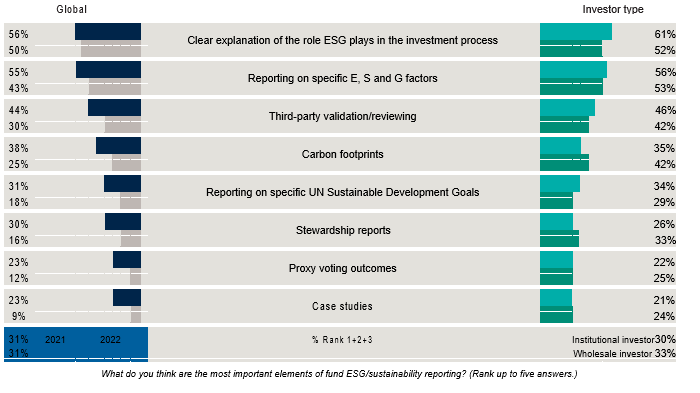

Given the importance attached to ESG reporting, it is essential that fund literature contains information that investors both want and need. Global investors say providing a clear explanation of the role ESG plays in the investment process is the most important element of fund sustainability reporting (56% vs. 50% in 2021). This is followed by reporting on specific E, S and G factors (55% vs. 43% in 2021) and third-party validation/reviewing (44% vs. 30% in 2021).

Most important elements of ESG reporting

These top three components of ESG fund reporting are unchanged from last year but have since grown in importance. Institutional investors attach even more weight to these top three compared to their wholesale counterparts.

The ability to report on specific United Nations Sustainable Development Goals (SDGs) is another area that has climbed up the priority list. Almost a third of investors think this is one of the most important elements of fund sustainability reporting — nearly double last year’s percentage (31% vs. 18%).

“The SDGs provide a clear, understandable and transferable framework for comparison,” says a portfolio manager at a UK wealth management company.

“The SDGs provide a clear, understandable and transferable framework for comparison,” says a portfolio manager at a UK wealth management company. “They are useful and easy for people to understand and I think they have real purpose.”

The SDGs also play a pivotal role in the fund selection process. Half (50%) of global investors say the ability to offer the full spectrum of SDG themes is an important consideration when selecting funds. Among European investors, this increases to six in 10 (60%).

SDGs and fund selection

Top asset manager qualities

Providing support on data challenges and net zero can help asset managers forge long-lasting partnerships with investors. But how do asset managers initially attract investors? And what do ESG investors look for in asset managers?

The ESG asset manager selection process can be a challenging undertaking. Firstly, investors are tasked with finding managers with authentic products that deliver in a climate where accusations of greenwashing are never far away. Secondly, the selection process is encumbered by the fact that almost all asset managers now offer sustainable products as ESG becomes ingrained into investment culture.

“ESG is a popular and growing area of investment and it’s easy for someone just to put a veneer of credibility over it,” says the CIO of an Australian wealth manager.

Investors again point to a proven track record in the ESG space as the attribute that inspires most trust and confidence in a manager. But this year a slightly smaller proportion point to this characteristic (48% vs. 52% in 2021).

The second-most prized attribute is a manager’s ability to demonstrate solid sustainable credentials and “walk the ESG walk” (40% vs. 39% in 2021). This underlines the importance of managers showing authenticity and leading by example. It links with the earlier finding about how asset managers can help with net zero investing by making their own high-level commitments.

“I think there needs to be some sort of guiding philosophy standing behind the fund manager which convinces investors that they’re genuine in their endeavours to invest in this sector rather than it just being the fashion of the day,” says the CIO of an Australian wealth manager. “ESG is a popular and growing area of investment and it’s easy for someone just to put a veneer of credibility over it.”

The third-ranked attribute most inspiring trust and confidence is the ability to integrate ESG considerations into all investments (36% vs. 39% in 2021). Investors therefore want asset managers that holistically embed ESG into their investment process and business DNA. This sits at the very core of Capital Group’s approach to ESG.

Asset manager ESG attributes

Regulation and greenwashing

Stamping out greenwashing

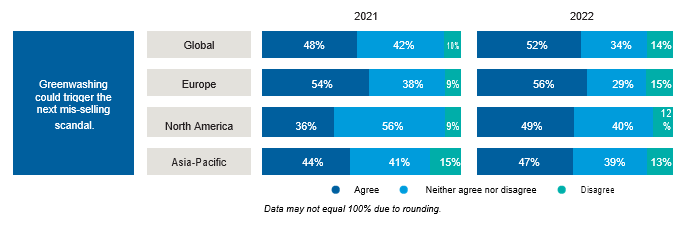

While global investors think greenwashing is now less pervasive, they consider it a bigger adoption barrier than last year. They are also slightly more worried about its potential to trigger a mis-selling* scandal (52% vs. 48% in 2021). Concern over a mis-selling scandal has increased most sharply among North American respondents (49% vs. 36% in 2021).

*When a product or service is deliberately misrepresented or a customer is misled about its suitability

As the ESG megatrend continues to gain steam and become more mainstream, regulation is playing an ever-increasing role in assuaging investor concern over greenwashing.

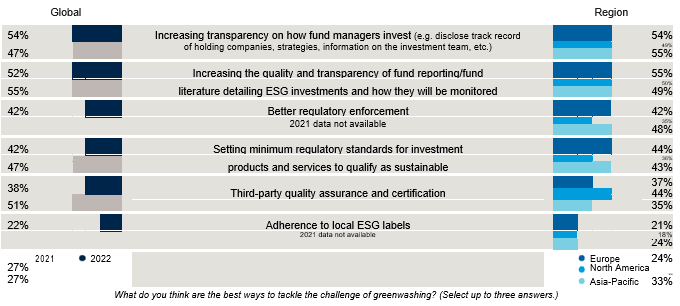

More than four in 10 (42%) investors think better regulatory enforcement is one of the best ways to tackle greenwashing, with this figure rising to 48% of Asia-Pacific investors. The same percentage of global investors (42%) think setting minimum regulatory standards for investment products and services would help tackle greenwashing.

But while regulatory firepower is helping in the fight against greenwashing, investors think fund managers are best placed to tackle the issue. Global investors point to increasing the transparency on how fund managers invest as the most effective way of combating greenwashing (54% vs. 47% in 2021). This is closely followed by increasing the quality and transparency of fund reporting in terms of detailing ESG investments and how they will be monitored (52% vs. 55% in 2021).

Fears about mis-selling scandal

Tackling greenwashing

Regulatory priorities

“The central problem with the whole ESG sector is there are no universal guidelines or benchmarks or standards,” says the CIO of an Australian wealth manager.

Aside from helping to stamp out greenwashing, investors are also looking to regulators to provide common standards and definitions. When asked what the ESG regulatory framework should prioritize in their respective countries, the highest proportion cite the need to harmonize global standards, taxonomies, and metrics (45%). This indicates that investors are struggling to untangle an increasingly complex and disjointed web of global regulations issued by different entities.

“The central problem with the whole ESG sector is there are no universal guidelines or benchmarks or standards,” says the CIO of an Australian wealth manager. “One of the key weaknesses is that it’s hard to come up with common definitions about what actually constitutes ESG investing.”

What should ESG regulations prioritise?

Developing guidelines for material, comparable ESG reporting for investors (44%) is considered the next most-pressing regulatory priority, followed by providing guidelines for consistent, objective, quantified disclosure of ESG-related risk factors (42%). The emphasis on guidelines suggests investors want regulators to provide a helping hand rather than issue a prescriptive set of rules.

“Our clients want an independent, reputable set of guidelines to inform their investment decision-making and help meet ethical objectives,” adds the CIO of an Australian wealth manager.

Regional priorities

Notably, a higher proportion of North Americans cite the need to harmonise global standards (51%), develop guidelines for ESG reporting (53%) and provide disclosure of ESG risk factors (53%). North Americans have the least conviction in ESG and encounter the highest adoption barriers. This suggests they have a greater need for regulations that can both alleviate their ESG concerns and help overcome adoption barriers. And in line with their fiduciary focus, they want client investments to operate in a safe and secure regulatory framework.

Looking at the top regulatory priorities for each region, European investors prioritise harmonising global standards (48%). North Americans prioritise guidelines for disclosure of ESG risk factors (53%), while Asia-Pacific investors see developing guidelines for ESG reporting as most important (44%).

The complete publication is available here.