Print

PrintMaia Gez, Era Anagnosti, and Taylor Pullins are partners at White & Case LLP. This post is based on a White & Case memorandum by Ms. Gez, Ms. Anagnosti, Mr. Pullins, Colin Diamond, Scott Levi, and Melinda Anderson.

The regulatory landscape for ESG disclosure by U.S. public companies faces potentially dramatic changes, with the Securities and Exchange Commission (“SEC”) proposing rules that would mandate comprehensive climate change disclosures and integrate key aspects of sustainability reporting with annual reports. [1] Against this backdrop, White & Case surveyed the SEC filings of 50 companies in the Fortune 100 to assess the latest trends in ESG disclosure.

Survey of ESG Disclosure—2020 to 2022

For its fourth annual survey of ESG disclosure in SEC filings, [2] the White & Case Public Company Advisory Group reviewed the annual meeting proxy statements and annual reports of 50 companies in the Fortune 100. [3] In these 100 SEC filings, we focused on 12 categories [4] of ESG disclosure in annual reports and proxy statements filed with the SEC in 2020, 2021 and 2022. The key trends and takeaways from our survey are discussed below.

Climate-Related Disclosure Takes the Spotlight in 2022

In the fall of 2021, ahead of Form 10-K filings, the SEC issued a sample comment letter on climate disclosure [5] and also issued bespoke comment letters to a number of companies questioning their materiality assessments with respect to climate disclosure. Climate-related disclosure significantly increased in both Form 10-K and proxy statement filings of the surveyed companies, with many companies including such disclosure for the first time in 2022. Our survey focused on the ways climate disclosure changed year-over-year among the surveyed companies.

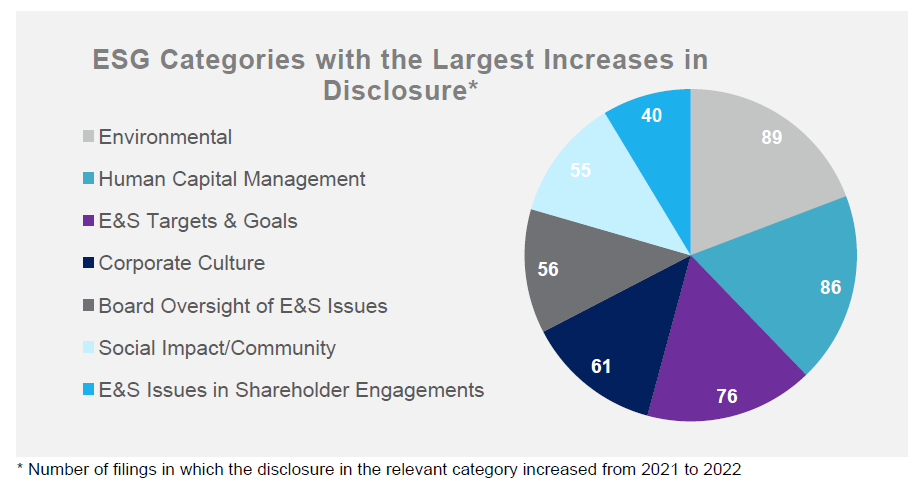

The Seven ESG Topics on the Rise in 2022

1. Environmental Matters

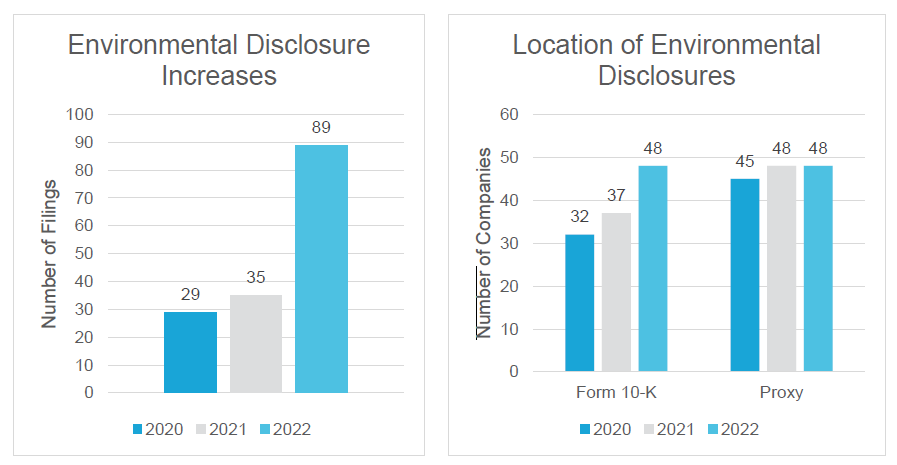

Overall for 2022, the largest increase in categories of ESG disclosure was with respect to environmental matters (up from third on the list in 2021) which covered a range of environmental topics, including investments in sustainability, recycling and renewable energy use. As shown in the chart below, 89 of the 2022 filings surveyed increased their environmental disclosure, compared to 35 of the 2021 filings and 29 of the 2020 filings.

Moreover, every company surveyed (all 50 companies) included environmental disclosure in their 2022 filings. Of the 96 filings that included environmental disclosure in 2022:

- Forty-eight companies (or 96%) included it in their Form 10-K (up from 37 in 2021 and 32 in 2020) and 48 companies (or 96%) in their proxy statement (the same number as in 2021 and up from 45 in 2020).

- Thirty-seven filings (or 37%) included historical quantitative metrics (13 Form 10-Ks and 24 proxy statements), such as information on greenhouse gas (“GHG”) emissions reductions and renewable energy use.

Although the number of proxy statements that contained environmental disclosure has remained fairly constant, environmental disclosures in Form 10-Ks have increased significantly over the past two years. The fact that every company surveyed included environmental disclosures either in their Form 10-K or in their proxy statement, and that so many companies that already had robust environmental disclosure increased that disclosure in 2022, illustrates the significant focus on environmental issues in 2022.

Examples of new environmental disclosures included the following: [6]

Investments in Environmental Sustainability, for example: “Operate Sustainably. We have a long-standing and substantial commitment to sustainable business operations, from the products and services we offer to our customers; to our store construction, maintenance and operations; to our supply chain and packaging initiatives; to our ethical sourcing program. As we strive to operate sustainably, we have focused on protecting the climate, reducing our environmental impact, and sourcing responsibly, and we have set specific, measurable goals to drive progress in these areas.”

Renewable Energy, for example: “The Climate Pledge is [the Company’s] commitment to be net-zero carbon by 2040, and we are on a path to powering our operations with 100% renewable energy by 2025. As the world’s largest corporate buyer of renewable energy, [the Company] announced dozens of new renewable energy projects in 2021 and now has 274 projects globally. The Climate Pledge has been signed by [the Company] and over 300 other companies that commit to the same goals…Pledge signatories in total generate over $3.5 trillion in global annual revenues and have more than 8 million employees across 51 industries in 29 countries.”

Climate Change Evaluation, for example: “As part of our commitment to being good stewards of the environment, we are working to understand, quantify, and reduce our impact on climate change. We understand that climate change poses risk and presents opportunities for our business to address such impacts in several ways. We recently undertook several actions to raise understanding about climate change and potential risks to our business, including…[e]valuating potential enterprise risks associated with climate change [and] [d]isclosing our baseline scope 1 and scope 2 [GHG] emissions, which we assessed in 2021 for calendar years 2019 and 2020. We are currently focused on calculating our scope 3 GHG emissions, and in conjunction with our Value Creation Plan, we are assessing energy usage and reduction opportunities and determining decarbonization goals.”

Spotlight on Climate-Related Disclosure

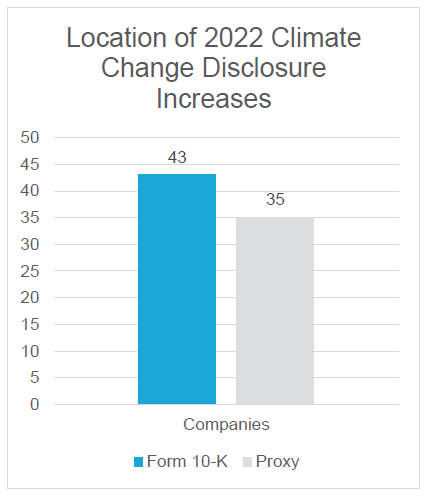

- Overall, 43 of the surveyed companies (or 86%) increased their climate-related disclosure in their 2022 Form 10-Ks, and 35 companies (or 70%) increased this disclosure in their 2022 proxy statements. Seven companies (or 14%) addressed climate-related disclosure in their Form 10-K for the first time in 2022, and six companies (or 12%) addressed climate-related disclosure in their proxy statements for the first time in 2022.

- Four of the surveyed companies received comments from the SEC in 2021 on climate-related disclosure. Two of the four companies agreed to additional risk factor and/or Management Discussion and Analysis (“MD&A”) disclosure. Many other surveyed companies included additional Form 10-K disclosure that appeared, based on content, to be directly influenced by the SEC’s sample comment letter.

- Fifteen companies added entirely new risk factors devoted to climate-related impacts (including physical impacts of climate change, transition risks to a low-carbon economy, compliance costs related to new and disparate regulations, and reputational risks), and 14 companies increased references to climate-related impacts in their existing risk factors.

- For the surveyed companies, references to climate-related impacts increased by seven mentions on average and five companies added new sections discussing ESG, sustainability and climate change in their MD&A. Only two companies did not mention climate-related impacts in their 2022 Form 10-Ks and seven did not do so in their 2022 proxy statements.

The increase in climate-related risk factors is particularly notable. For example:

“Climate Change Could Have a Negative Impact on [the Company’s] Results of Operations and Financial Condition.… Climate change presents both immediate and long-term risks to [the Company] and [our] customers and clients, with the risks expected to increase over time. Climate risks can arise from both physical risks (those risks related to the physical effects of climate change) and transition risks (risks related to regulatory and legal technological, market and reputational changes from a transition to a low-carbon economy)…”

2. Human Capital Management (HCM)

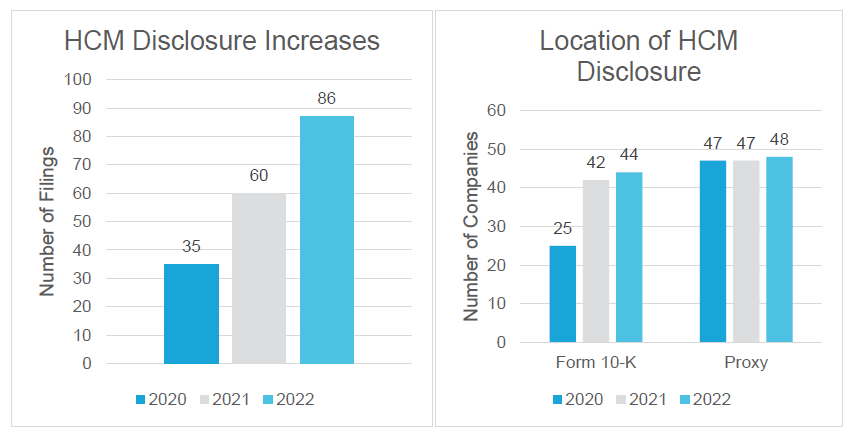

In 2022, the second largest increase in ESG disclosures came in human capital management (“HCM”), down from first place in the prior three years.

As expected due to the SEC rule changes mandating human capital disclosure in the Form 10-K, [7] every company surveyed included some form of HCM disclosure in their Form 10-K, and nearly all surveyed companies (96%) also included HCM disclosure in their annual meeting proxy statement. Eighty-six of the 2022 filings surveyed presented an increase in this type of disclosure from 2021 (up from 60 in 2021 and 35 in 2020), with 41 of these increases coming in the 10-K and 45 of these increases in the proxy statement. Increased disclosure included topics such as employee health and safety, talent management and development, employee engagement and pay equity.

Within HCM disclosures, we also found a significant number of quantitative disclosures in both 2021 and 2022. In 2022, of the 98 filings that included disclosure on HCM, 54 included current or historical quantitative metrics. These metrics included information on: (1) the percentage of employees who are women or people of color; (2) information on corporate initiatives to improve gender and ethnic diversity in their workforce; and (3) information on employee turnover and retention rates.

The below graphics represent the disclosure increases and the excerpts provide representative examples of the additional HCM disclosure:

Examples of new disclosures included the following:

On Employee Engagement, for example: Associate engagement is the emotional commitment associates have to [the Company]. It is vital to our culture and to our success. We create an engaging workplace by continuously listening to and acting on associate feedback. We provide several pulse check surveys…that help us determine how emotionally connected those associates are to our customers, the Company, their jobs, fellow associates, and leaders. In addition, our annual Voice of the Associate survey…serves as our primary means of gauging associates’ level of engagement within their roles. We use the feedback from these surveys to help improve the overall associate experience …We also maintain a digital associate engagement platform that links associates with common interests and fuels connections to co-workers and Company leaders.”

On Talent Retention, for example: “In 2021…our Employee Engagement Index, an overall measure of employee satisfaction with the Corporation, was 88%. Our turnover among employees was 12% in 2021 and 7% in 2020. Our pre-pandemic levels of turnover in 2019 and 2018 were 11% and 12%. Additionally, [we] provide[] a variety of resources to help employees grow in their current roles and build new skills, including resources to help employees find new opportunities, re-skill and seek leadership positions…In 2021, more than 26,000 employees found new roles within the Corporation.”

On Pay Equity, for example: Since 2019, we have achieved gender pay equity globally and we continue to maintain race/ethnicity pay equity in the US. We achieve pay equity by closing the gap in average pay between employees of different genders or race/ethnicity in the same or similar roles after accounting for legitimate business factors that can explain differences, such as location, time at grade level, and tenure.”

On Employee Wellness and Flexible Working, for example: “Our offices and sites once again closed Company wide for one day in May 2021 to allow colleagues to recharge In 2021, in recognition of the new way of working, we initiated [ Flex, a hybrid model that empowers our office based employees to find the right productivity and balance of in person and remote work.”

Focus on Diversity, Equity and Inclusion (“DEI”)

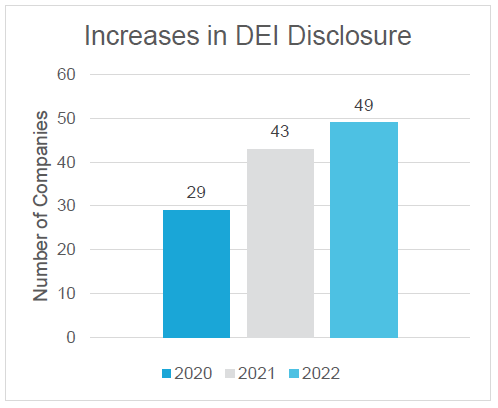

In 2022, all but one of the companies surveyed (49 out of 50) included disclosure on diversity or related initiatives at the company, up from 43 in 2021 and 29 in 2020.

In 2022, most companies surveyed (44 out of 50) included this in both their Form 10-K and their proxy statement, although the disclosures in the proxy statements were generally more robust and detailed.

On Employee Diversity, Equity and Inclusion, for example: Diversity, Equity, and Inclusion (DEI): Building a world where progress, equitable outcomes, diversity, and inclusion can be realities is at the heart of what we do—from how we build our products to how we build our workforce. We have deepened our efforts to drive meaningful change but we know there is more to be done. We have a responsibility to continue scaling our DEI initiatives, to ensure a workforce that is more representative of our users, a workplace that creates a sense of belonging for everyone, and to increase pathways to tech in the communities we call home…In 2020, we implemented a series of industry-leading principles and improvements that incorporated input from both employees and stockholders, including the creation of a new DEI Advisory Council, which comprises internal senior executives and external DEI experts. We have also heightened our focus on promoting racial equity, including announcing in 2020 a series of racial equity commitments. We shared an update on our progress in 2021 and continue working to translate those efforts into lasting, meaningful change.”

EEO-1 Data References. In 2022, 36 companies (or 72%) included EEO-1 data or referenced the provision of such data in a separate report, up from 16 (or 32%) in 2021. Thirty-two companies made this disclosure only in their proxy statement, two only in their Form 10-K and six included the disclosure in both filings. The prevalence of this disclosure was largely the result of renewed investor pressure and focus on these disclosures. For example, BlackRock called on companies to disclose their EEO-1 survey responses and, starting in 2022, State Street adopted a policy to vote “against” the compensation committee chairs at companies that do not disclose their EEO-1 survey responses.

Representative examples of these disclosures include the following:

“We released our 2021 [DEI] Report, in which we provide workforce diversity data, (including our EEO-1 data) and explain how we are working to drive progress through our pillars of action: public policy, workforce diversity, community engagement and supplier diversity.”

“As part of our Health for Humanity Report publication in June 2021, we publicly disclosed our U.S. Federal Employer Information Report EEO-1, and we annually publish the You Belong: Diversity, Equity & Inclusion Impact Review (DEI Impact Review), which examines how the Company’s global DEI strategy has been a key driver of innovation and business outcomes since our founding over 130 years ago.”

3. E&S Goals and Targets

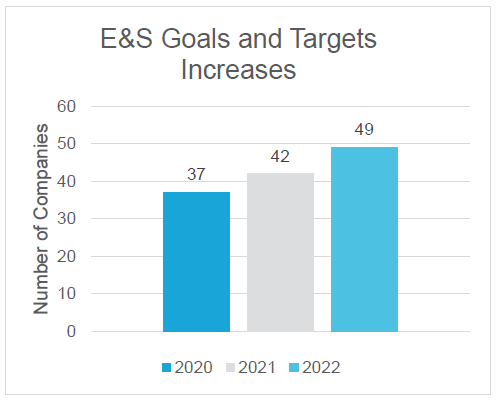

For the first time in White & Case’s annual survey, E&S Goals and Targets made the top seven categories, rising to the third spot with the largest increase in disclosure. This reflects the heightened focus by investors on companies setting specific targets with respect to environmental and social priorities.

Seventy-six of the filings surveyed (or 76%) increased their disclosure related to E&S goals and targets. In total, all but one of the surveyed companies (49 out of 50) included some form of E&S goal or target. Of these, 32 companies included the disclosure in their Form 10-K and 48 companies included it in their proxy statement. Of the 49 companies that included E&S goals and targets, seven companies included them for the first time in their 2022 disclosures.

E&S goals and targets cover a range of topics including long term goals to reach net zero, and shorter term goals to reduce GHG emissions by specified amounts. [8]

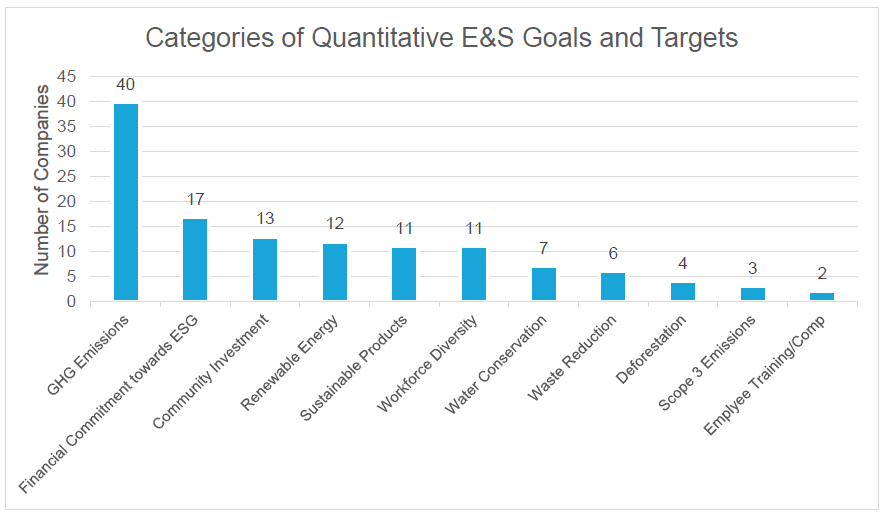

Quantitative E&S Goals and Targets. Notably, in addition to including qualitative goals and targets, a significant number of companies included quantitative metrics in their E&S goals and targets. Forty-four companies (or 88%) included some form of quantitative metric in their E&S goals and targets disclosure—18 in their Form 10-K (up from 11 in 2021) and 42 in their proxy (up from 26 in 2021). This demonstrates a growing trend of companies that are disclosing quantifiable goals in their SEC filings, and not just in sustainability reports or website disclosures, which can be measured and tracked by investors.

Specifically:

- GHG Emissions: Forty of the surveyed companies disclosed at least one specific goal relating to GHG emissions reduction on a given timeline. Twenty-three companies disclosed a specific net zero goal, ten companies disclosed a carbon neutral goal, 18 companies disclosed other specific emission reduction goals, and one company disclosed a goal to be carbon negative. Several companies disclosed a combination of emissions goals.

- Financial Commitment Towards ESG: Seventeen of the surveyed companies set forward-looking quantitative goals to commit a specified amount of funds over a specific timeline towards ESG initiatives, such as diversity funds, sustainable energy, climate action and local community support.

- Community Investment: Thirteen of the surveyed companies set goals to support local communities through a specific number of volunteer hours committed, meals donated or people educated.

- Renewable Energy: Nine of the surveyed companies set a quantitative goal to meet their energy needs with 100% renewable energy by a given timeline and four companies set a goal to source a specific percentage or amount of renewable energy by a given timeline. Four companies set other quantitative renewable energy or energy conservation goals, such as achieving green certification for a certain percentage of their buildings or producing a certain amount of clean energy.

Examples of new disclosures included the following:

GHG Reductions Goals, for example: “The Company’s environmental goals, collectively called “Strive 35”—an ambitious plan to, by 2035, reduce from a 2019 baseline absolute Scope 1 and 2 [GHG] emissions by 25 percent, reduce absolute Scope 3 emissions by 25 percent, reduce energy intensity by 15 percent, reduce water intensity by 10 percent, and achieve a 90 percent landfill diversion rate—are part of an aggressive plan to continue to reduce the [our] environmental footprint…In 2021, [we] added 5-year interim targets to ensure the Company stays on track to meet its 2035 goals. By 2025, the Company aims to reduce absolute GHG emissions by 1.5%, reduce energy intensity and water intensity by 6% and 5%, respectively, and achieve 87% of its waste diverted from landfill.”

Carbon Negative Goals, for example: “In January 2020, we announced a bold commitment and detailed plan to be carbon negative by 2030, and to remove from the environment by 2050 all the carbon we have emitted since our founding in 1975.”

Financial Commitments, for example: “In April 2021, we committed $1 trillion to sustainable finance by 2030, which builds on the work we outlined in our updated Sustainable Progress Strategy. This commitment includes extending our prior five-year, $250 billion environmental finance goal to $500 billion by 2030 through which we will finance and facilitate an array of climate solutions such as renewable energy, energy efficiency, sustainable transportation and circular economy and $500 billion in social finance including affordable housing, diversity and equity, economic inclusion, food security and healthcare.”

Employee Diversity Goals, for example: “We set the following goals to change our workforce representation by 2030: (i) globally, increase representation of women at the manager level and above to 48% (up from 40%); (ii) in the United States, increase representation of African American and Black employees at the manager level and above to 11% (up from 5%); and (iii) in the United States, increase representation of all other ethnically diverse groups at the manager level and above to 23% (up from 17%). To achieve these goals, we will focus on attracting, developing, and retaining diverse talent, from entry-level to senior leadership positions.”

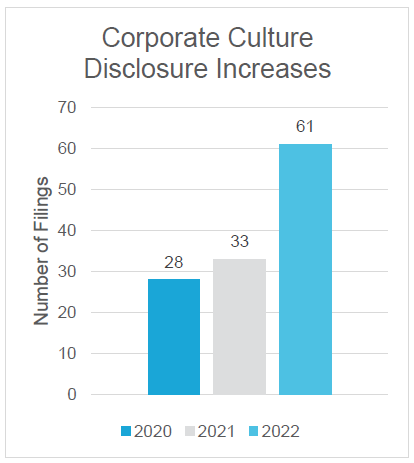

4. Corporate Culture

Sixty-one of the 2022 filings surveyed increased their disclosure on corporate culture, compared to 33 of the 2021 filings surveyed and 28 of the 2020 filings surveyed.

Overall, 47 of the companies surveyed included disclosure on corporate culture in their 2022 filings, compared to 44 companies in 2021 and 43 companies in 2020.

Examples of new disclosures included the following:

Core Values, for example: “The [Company] has a strong commitment to ethics and integrity, and we are a values- and culture-centric business. Our commitment to our core values drives our approach to human capital management. Our culture is based on our servant leadership philosophy represented by the inverted pyramid, which puts primary importance on our customers and our associates by positioning them at the top, with senior management at the base in a support role. We bring our culture to life through our core values, which serve as the foundation of our business and the guiding principles behind the decisions we make every day.”

Importance of Board in Shaping Culture, for example: “Our Board and its committees play a key role in establishing and maintaining our culture, setting the “tone at the top” and holding management accountable for its maintenance of high ethical standards and effective policies and practices to protect our reputation, assets, and business.”

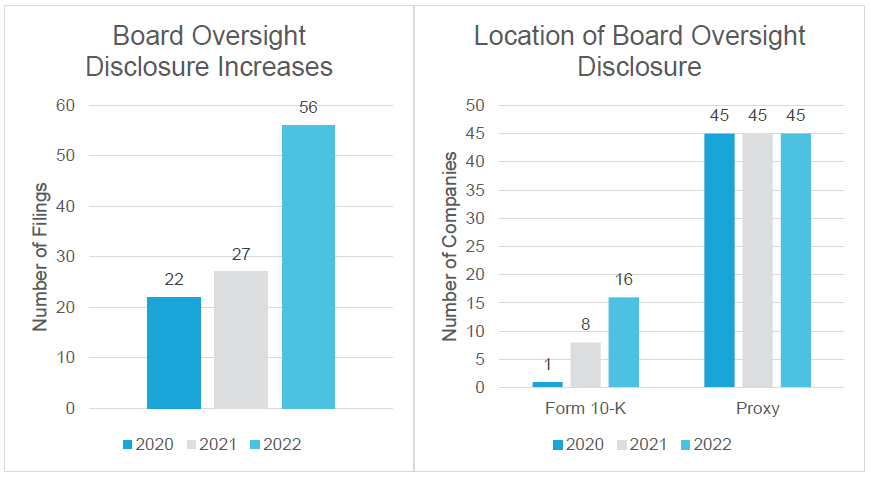

5. Board Oversight of Environmental and Social Issues

Fifty-six of the filings surveyed increased their disclosure related to board oversight of E&S issues in 2022, compared to 27 filings in 2021 and 22 filings in 2020. Overall, 47 companies included disclosure on board oversight of E&S issues in their 2022 filings.

Notably, there has been an increasing trend of companies including this disclosure in their Form 10-Ks as well as their proxy statements. In 2022, 16 companies included this disclosure in their Form 10-Ks, up from eight in 2021 and one in 2020. Board oversight disclosures generally appeared in the business section of the surveyed companies’ Form 10-Ks.

Examples of new disclosures include the following:

ESG Committee or Function Reporting to the Board, for example: “Our sustainability efforts are overseen by our Board of Directors, in particular a dedicated Sustainability and Corporate Responsibility Committee, and led by our Chief Sustainability Officer… The Sustainability and Corporate Responsibility Committee actively oversees our objectives, goals, strategies, and activities relating to sustainability and corporate responsibility matters and assists the Board in ensuring that we operate as a sustainable organization and responsible corporate citizen in order to enhance shareholder value and protect [our] reputation.”

Governance Committee Oversight of E&S, for example: “The [NGC] is responsible for overseeing management of risks related to our environmental, sustainability, and corporate social responsibility practices, including risks related to our operations and our supply chain.”

Board Oversight of HCM, in Form 10-K business section, for example: “As we execute on the Company’s strategy in the coming years, our focus on organizational performance and talent will remain front and center. We will continue to monitor various factors across our human capital priorities, including as a part of our business operating reviews during the year and with oversight by our Board of Directors and the Board’s Management Development and Compensation Committee.”

Specialized Board Committee Oversight of E&S Issues, in Form 10-K business section, for example: “Our Board of Directors and Board committees provide important oversight on certain human capital matters, including items discussed at the Executive People Forum. The Compensation, Talent and Culture Committee maintains responsibility to review, discuss, and set strategic direction for various people-related business strategies, including: compensation and benefit programs; leadership succession planning; culture; [DEI]; and talent development programs. The Sustainability, Innovation and Policy Committee is responsible for discussing and advising management on maintaining and improving sustainability strategies, the implementation of which creates value consistent with the long-term preservation and enhancement of shareholder value and social wellbeing, including human rights, working conditions, and responsible sourcing.”

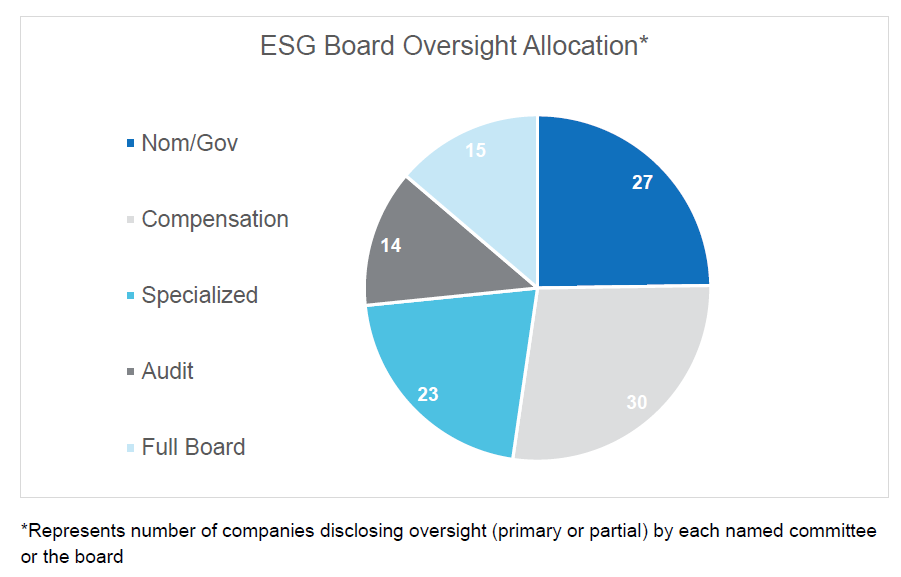

Committee(s) with Oversight over ESG Matters.

Of the 50 surveyed companies:

- Thirty companies (or 60%) disclosed that their Nominating and Corporate Governance Committee (“NGC”) oversaw some or all ESG Matters, up from 12 in 2021 (a 150% increase). Of these 30 companies: three disclosed that ESG matters were solely or primarily overseen by the NGC, while the other 27 companies disclosed that both the NCG and another committee had oversight over ESG matters.

- Twenty-seven companies disclosed that their Compensation Committee (“CC”) oversaw some or all ESG Matters; of these 27 companies, three disclosed that ESG matters were solely or primarily overseen by the CC, while the other 24 companies disclosed that there was shared ESG oversight between both the CC and another committee.

- Twenty-three companies disclosed that at least some ESG matters were overseen by a more specialized committee or committees, such as a dedicated Sustainability Committee or a Public Responsibility Committee.

- Fourteen companies disclosed that the audit committee had oversight over some ESG issues, such as risks and exposures associated with civil and human rights and sustainability, identifying ESG investment criteria and providing assurance of ESG disclosures. Additionally, ten companies disclosed that the full board shared E&S oversight responsibilities with another committee.

It is interesting to note that 34 companies disclosed that they allocated responsibility for oversight of ESG issues to more than one committee (up from 21 in 2021), with six companies disclosing that they allocate responsibility to four committees and five companies disclosing allocation of ESG oversight to five committees. This increase in allocation of ESG oversight to more than one committee reflects the increasing role boards have in providing oversight of ESG issues and allows committees to narrow and deepen their focus on different facets of these issues. For example, many companies disclosed that ESG issues were divided between committees that focused on human capital and social/public policy issues and those that focused on environmental and sustainability issues.

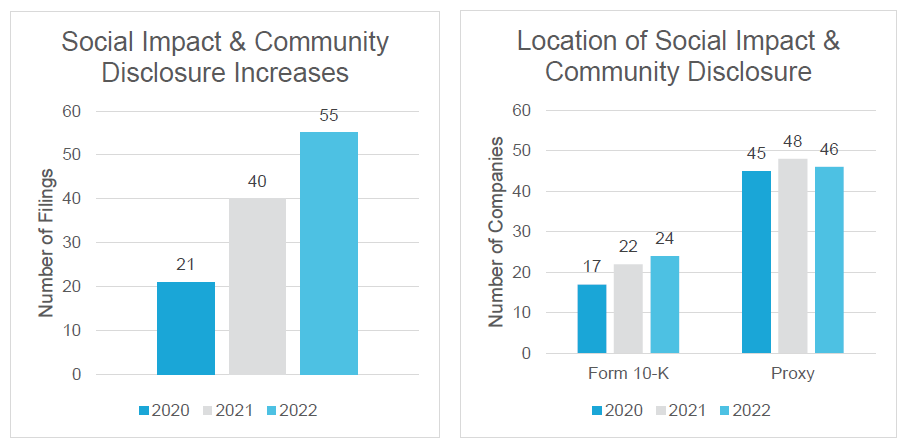

6. Social Impact and Community

The social impact and community category of ESG disclosure moved down from second to sixth on our list of increased ESG disclosure. Specifically, 55 of the 2022 filings surveyed (or 55%), including 16 Form 10-Ks, increased their disclosure related to social impact and community relations, compared to 40 in 2021 (or 40%) and 21 in 2020 (or 21%).

Examples of new disclosures included the following:

Community Development and Engagement, for example: “We are committed to creating value for our communities through economic development, philanthropy, volunteerism and advocacy, and by operating our business in a socially and environmentally responsible way. The communities in which our assets are located and where our employees live are critical stakeholders. We consistently and regularly engage with our local communities and seek their feedback. Our refining operations have community advisory councils or panels that include both Company representatives and community members…Our pipeline business units have year-round community awareness, education and listening panels to stay connected with those involved with and living near our extensive pipeline network.”

Access to Technology, for example: “Access to affordable and reliable internet service is critical for work, learning and commerce—and for staying digitally connected to family, friends, news and information. Using our platform to address the digital divide is strategically important to [the Company], as it helps drive social change while expanding our network reach and deepening valuable collaboration with communities, authorities and NGOs…In 2021, [the Company] announced a commitment to invest $2 billion over the next 3 years to help address the digital divide…As part of our $2 billion digital divide commitment, we introduced [] Connected Learning, a multi-year initiative led by our CSR organization to help stem the tide of learning loss, further narrow the homework gap and empower today’s learners…Through the end of 2022, we’re launching more than 20 [] Connected Learning Centers in under-resourced neighborhoods facing barriers to connectivity—providing access to high-speed internet and computing devices, as well as opportunities for tutoring and mentorship through our employee-driven [Company] volunteerism initiative.”

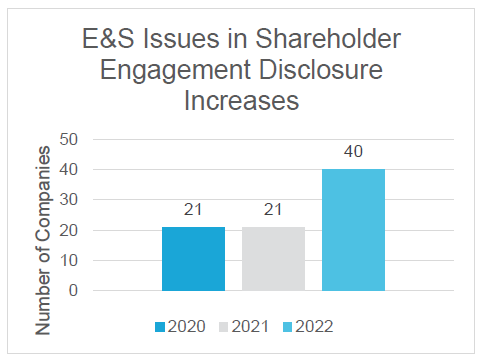

7. E&S Issues in Shareholder Engagements

Forty companies increased their disclosure related to ESG issues included in their shareholder engagements in their 2022 proxy statements, up from 21 in both 2021 and 2020. Overall, 48 companies disclosed that ESG issues were included in their shareholder engagements in their 2022 proxy statements, up from 45 in 2021 and 40 in 2020.

Examples of new disclosures included the following:

Responsiveness to Shareholder Feedback (in 21 of the 45 filings). For example: “Our Board believes that solicitation and consideration of shareholder feedback is critical to driving long-term growth and creating shareholder value. Our shareholder engagement program is a robust, year-round process encompassing meetings held throughout the year with shareholders during which we encourage ongoing, meaningful dialogue about the issues they find most important…Our Board reviews our annual meeting results, ongoing shareholder feedback and corporate governance and compensation trends to help drive and develop our shareholder engagement priorities…We respond to shareholder feedback by enhancing our policies, practices and disclosures informed by ongoing dialogue with our shareholders and communicate important updates and enhancements made during the fiscal year in our proxy statement.”

Mention of Specific E&S Issues Discussed, for example: “Recent Board discussions have addressed shareholder feedback on a variety of topics, including Board refreshment, shareholder proposals, executive compensation, sustainability and human capital management and political advocacy, often resulting in changes to our policies and practices as well as guiding the focus of future discussions in the boardroom…We also fulfilled our commitment to publish our first Sustainability Report and publicly disclosed our workplace diversity data, including our consolidated EEO-1 report. Recognizing the continued importance of transparency on political advocacy, we strengthened our website disclosures to provide additional detail regarding the Board and Governance & Public Policy Committee’s enhanced oversight role, information on our direct lobbying activities, and our political contributions guidelines and political action committee processes and oversight.”

Reporting Frameworks: SASB, TCFD and Others

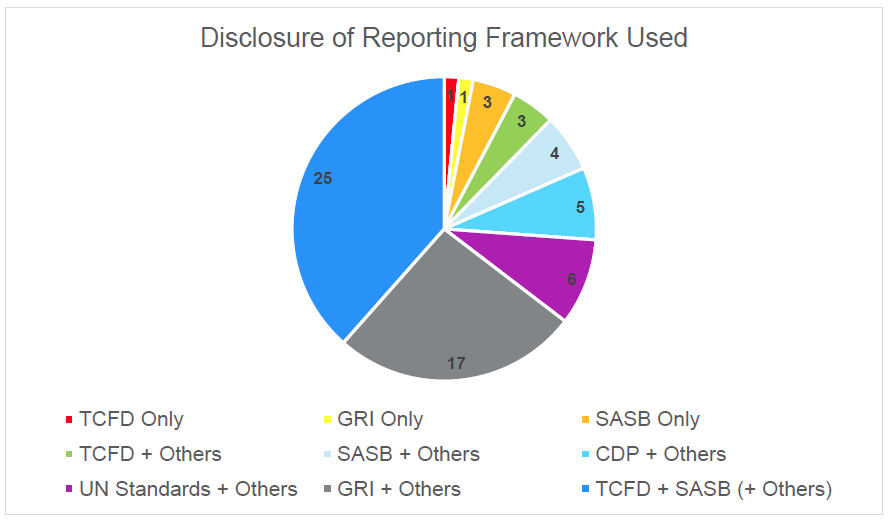

The 2022 SEC filings revealed a continuing trend of more companies disclosing the use of reporting frameworks. In 2022, 38 of the surveyed companies disclosed in their SEC filings that their sustainability reports posted on their website follow or align with specific reporting frameworks, a significant increase from 26 in 2021, 11 in 2020 and just one company in 2019.

In general, companies are trending towards disclosing the use of more than one framework. In 2022, five companies reported using only one framework, whereas 33 companies reported using at least two or more frameworks (compared to 16 companies using two or more frameworks in 2021). In 2022, of the 38 surveyed companies that disclosed their use of frameworks:

- Twenty-five surveyed companies disclosed that they align their sustainability reporting with both Sustainability Accounting Standards Board (“SASB”) standards and Task Force on Climate-related Financial Disclosures (“TCFD”) frameworks (compared to 13 in 2021).

- Eight companies only referenced SASB standards or SASB plus another non-TCFD standard (compared to 5 in 2021) and four companies only referenced TCFD or TCFD plus another non-SASB standard (compared to eight in 2021).

- Eighteen of the 38 companies in 2022 disclosed that they aligned with Global Reporting Initiative (“GRI”) standards (compared to six in 2021), with one company exclusively using the GRI standards.

- Companies also disclosed that they use other reporting frameworks such as CDP (formerly known as The Climate Disclosure Project) (five companies), the UN Guiding Principles Reporting Framework (two companies), the UN Sustainable Development Goals (three companies) and the UN Global Compact (one company).

Companies continue to make these disclosures referencing the reporting frameworks that they use primarily in their proxy statements. In 2022, only one company disclosed its reporting frameworks solely in its Form 10-K, whereas six companies made this disclosure in both their Form 10-K and proxy statements, and 31 companies made this disclosure exclusively in their proxy statement.

The significant increase in disclosure regarding use of these reporting frameworks echoes the calls from the investor community, including BlackRock, [9] which has asked the public companies it invests in to (i) “disclose the identification, assessment, management, and oversight of sustainability-related risks in accordance with the four pillars of TCFD,” and (ii) “publish investor-relevant, industry-specific, material metrics and rigorous targets, aligned with SASB or comparable sustainability reporting standards.” [10]

Examples of new disclosures included the following:

Disclosed following TCFD, for example: “In our most recent Task Force for Climate Change-related Financial Disclosure (TCFD)-aligned report issued in October 2021, we described our GHG intensity targets for oil, gas, flaring, and methane for 2028.”

Disclosed following more than one standard, for example: “[The Company] participates in the CDP’s climate, forestry and water security questionnaires to benchmark and quantify our environmental practices, to provide transparency on our progress and assist in the reduction of our contributions to climate change. We continue to align our sustainability reporting with the appropriate [SASB] standards for our industry, the [GRI] and the UN Sustainable Development Goals (“SDGs”). We also published our first [TCFD] report in 2021 to assess our climate-related risks and opportunities and better understand the potential impacts on our value chain.”

Disclosed following more than one standard, for example: “We are committed to transparency around our carbon footprint and climate risk and use the framework developed by the TCFD to inform our disclosure on climate governance, strategy, risk management, and metrics and targets…Our Corporate Responsibility Report also includes a mapping of our disclosure to the TCFD, the [SASB] framework, and our CDP Climate Change Survey, all of which are available on our website.”

Three Key Take-Aways

Given these disclosure trends and influences, when contemplating any ESG disclosure in connection with SEC filings, public reporting companies should consider the following key takeaways:

1. ESG: What’s In and What’s Out of SEC Filings

Based on our survey, the top ESG topics for 2022 SEC filings were:

- Environmental disclosure, with a focus on climate change, which moved up from third to first in 2022;

- Human capital management, with a focus on diversity and inclusion; and

- E&S targets and goals, which made the top seven list for the first time since our survey began in 2019.

These top categories for increase reflect the key areas of corporate, SEC and investor focus this year for the surveyed companies. [11]

2. A Renewed Focus on ESG for Form 10-Ks

Even ahead of the SEC’s adoption of any new climate rules, in-house teams should take note of the growing trend of providing ESG disclosure in annual reports on Form 10-Ks. The results of our survey demonstrate a re-focus and movement towards the Form 10-K for enhanced ESG disclosures. For example, 15 of the surveyed companies added entirely new risk factors devoted to climate change impacts, and more broadly, environmental disclosures in Form 10-Ks have increased significantly over the past two years while remaining fairly constant in proxy statements.

This increase in Form 10-K disclosure, particularly on the environment, came on the heels of the September 2021 sample letter on climate disclosure. As a result of this growing trend, companies should zero in on their (1) materiality assessments for climate change, (2) their approach towards differentiating their Form 10-K from sustainability reports, and (3) enhancing their controls on ESG disclosure. More specifically:

- Confirm Your Materiality Assessments. In terms of the materiality assessments, companies should continue to consider the SEC’s 2010 climate change disclosure guidance12 and the recent comment letters from Corp Fin on companies’ climate disclosure. SEC comments to date on climate disclosure initially asked questions focusing on a company’s materiality analysis and then requested additional details on the company’s determination that disclosure of climate change matters was not necessary because the climate change matters were not material. In some cases, the follow-up comments requested that companies provide quantitative information to support their materiality determinations.

- Differentiate ESG for Your Form 10-K and Sustainability Report. With respect to sustainability reporting, it is important to note the growing SEC scrutiny of the divide between the content of SEC filings and sustainability reports. One of the SEC sample comments asked companies to advise the SEC of “what consideration” a company “gave to providing the same type of climate-related disclosure in your SEC filings as you provided in your CSR report.” Although companies have largely continued to provide the vast majority of their ESG disclosure on corporate websites in sustainability reports, as opposed to their Form 10-Ks, the rationale for this divide is being called into question by both the SEC comments and proposed rule changes on climate.

- Enhance Your Controls on ESG. Following from these two points, it is crucial to confirm whether (a) any ESG disclosures (whether they be on website sustainability reports, or communicated to investors, underwriters or banks) may be material and therefore required to be included in a Form 10-K, and (b) sufficient controls are in place to ensure their accuracy and enable the information to be covered by Sarbanes Oxley certifications signed by CEOs and CFOs and filed with the SEC.

3. Focus on Next Steps in Light of ESG Trends and Proposed SEC Disclosure Rules on Climate

As the deadline passes for comments on the SEC’s rule proposal on climate change disclosure, the SEC will determine the fate of ESG disclosures in SEC filings, particularly the Form 10-K. In the meantime, companies will need to:

- First, prepare to update your company’s ESG disclosure on a holistic basis for future reports—across your sustainability report, proxy statement and your Form 10-K—as if the new SEC rules will not yet be in effect next year. Companies should begin considering their ESG disclosure on particular topics (for example, human capital and climate) on a holistic basis across all of their disclosure documents to ensure consistency, appropriate vetting of the accuracy of the disclosures and consistent messaging to investors.

- Second, carefully scrutinize any proposed expansion of your ESG disclosures at this time and make sure they undergo a comprehensive legal review. It is crucial that companies take a hard look at any new proposed ESG disclosures at this time and conduct a thorough legal assessment of the implications of making any such new disclosures. In particular, a company should consider in detail how the proposed rules (if adopted as proposed) would impact any such new disclosure, particularly as it relates to new E&S targets or goals and transition plans.

- Third, take steps to prepare for the proposed SEC climate rules now as if they will be adopted substantially as proposed. Companies should establish a working group (including legal, financial reporting, sustainability, IR and communications) and begin their assessment of what steps would need to be taken in order to comply with the new climate change disclosure requirements if the proposed rules are adopted substantially as proposed. This includes creating a plan to tackle those elements of the proposed rules that will be the most challenging for companies to comply with and require the most lead time to implement.

- Last but not least….remember the key word here: Controls, controls and more effective controls. Regardless of whether companies include enhanced ESG disclosure in their next Form 10-Ks, in light of the enhanced SEC scrutiny and trends on the horizon, companies should treat this disclosure as if it were subject to their disclosure controls and procedures under the Sarbanes-Oxley Act. This means establishing the same rigor of controls for such disclosure, such as completing a sub-certification process and disclosure committee oversight to appropriately vet and confirm the accuracy of required disclosures.

Endnotes

1For more information, see our alert “SEC Proposes Long-Awaited Climate Change Disclosure Rules.”(go back)

2The 2018-2019 White & Case LLP Survey is available here and the 2019-2020 White & Case LLP Survey is available here.(go back)

3The companies in this survey consist of the following: Alphabet Inc., Amazon.com, Inc., AmerisourceBergen Corporation, Anthem, Inc., Apple Inc., Archer-Daniels-Midland Company, AT&T Inc., Bank of America Corporation, Berkshire Hathaway Inc., The Boeing Company, Cardinal Health, Inc., Centene Corporation, Chevron Corporation, Citigroup Inc., Comcast Corporation, Costco Wholesale Corporation, CVS Health Corporation, Dell Technologies Inc., DuPont de Nemours, Inc., Exxon Mobil Corporation, FedEx Corporation, Ford Motor Company, General Electric Company, General Motors Company, The Home Depot, Inc., International Business Machines Corporation, Intel Corporation, Johnson & Johnson, JPMorgan Chase & Co., The Kroger Co., Lowe’s Companies, Inc., Marathon Petroleum Corporation, McKesson Corporation, MetLife, Inc., Microsoft Corporation, PepsiCo, Inc., Phillips 66, The Procter & Gamble Company, Prudential Financial, Inc., Raytheon Technologies Corporation, Sysco Corporation, Target Corporation, UnitedHealth Group Incorporated, United Parcel Service, Inc., Valero Energy Corporation, Verizon Communications Inc., Walgreens Boots Alliance, Inc., Walmart Inc., The Walt Disney Company and Wells Fargo & Company.(go back)

4The 12 categories of E&S disclosure in this survey are the following: (1) Board Oversight of E&S Issues; (2) Corporate Culture; (3) Ethical Business Practices; (4) Human Capital Management; (5) Environmental Matters; (6) Social Impact and Community; (7) Political Contribution Disclosure; (8) Supply Chain Management; ; (9) E&S Qualifications of Directors; (10) E&S Issues in Shareholder Engagement; (11) E&S Goals; and (12) References to Sustainability Reporting Frameworks, including SASB and/or TCFD.(go back)

5For more information, see our alert “SEC Issues Sample Comment Letter as it Ramps up Scrutiny of Climate Disclosures.”(go back)

6Public company ESG disclosures vary significantly for a variety of reasons, and the disclosure examples included in this article are representative of the subjects covered within each applicable category. The examples of disclosure in this memorandum are from the following companies (listed in order of appearance): The Home Depot, Inc., 2021 Form 10-K; Amazon.com, Inc., 2022 proxy statement; Centene Corporation, 2022 proxy statement; Citigroup Inc., 2021 Form 10-K; The Home Depot, Inc., 2021 Form 10-K; Bank of America Corporation, 2021 Form 10-K; Intel Corporation, 2021 Form 10-K; Johnson & Johnson, 2022 proxy statement; Comcast Corporation, 2022 proxy statement; Alphabet Inc., 2022 proxy statement; Raytheon Technologies Corporation, 2022 proxy statement; Johnson & Johnson, 2022 proxy statement; Archer-Daniels-Midland Company, 2021 Form 10-K; Microsoft Corporation, 2022 proxy statement; Citigroup Inc., 2022 proxy statement; Cardinal Health, Inc., 2022 proxy statement; The Home Depot, Inc., 2021 Form 10-K; Bank of America Corporation, 2022 proxy statement; Archer-Daniels-Midland Company, 2022 proxy statement; Amazon.com, Inc., 2022 proxy statement; General Electric Company, 2021 Form 10-K; Ford Motor Company, 2021 Form 10-K; Phillips 66, 2022 proxy statement; AT&T Inc., 2022 proxy statement; McKesson Corporation, 2022 proxy statement; The Boeing Company, 2022 proxy statement; Chevron Corporation, 2022 proxy statement; Lowe’s Companies, Inc., 2022 proxy statement; Intel Corporation, 2022 proxy statement.(go back)

7For more information, see our alert “SEC Adopts Amendments to Modernize Disclosures and Adds Human Capital Resources as a Disclosure Topic: Key Action Items and Considerations for U.S. Public Companies.”(go back)

8The more complete list of E&S goals and targets topics included: reducing GHG emissions; reducing energy consumption; reducing environmental footprint; increasing the use of renewable energy; improving energy efficiency; reducing waste and/or increasing re-use and recycling; increasing the use of recyclable or sustainable materials in products or packaging and/or introducing more sustainable products or packaging; reducing water usage; having more responsible supply chains; advancing workplace diversity, and recruiting and retaining a diverse workforce; expanding opportunities for diverse individuals; increasing diversity at leadership levels; increasing promotion for underrepresented individuals; cultivating and promoting an inclusive culture; developing talent; and delivering social impacts to support communities and improving community well-being.(go back)

9Available here. For more information, see our alert “Blackrock Calls for Enhanced Sustainability Disclosure and Accountability for Directors.”(go back)

10Similarly, Vanguard “suggest[s] that companies adhere to reporting structures such as the Value Reporting Foundation (formed by the merger of the [SASB] and the International Integrated Reporting Council), the [TCFD], or other broadly accepted industry-specific frameworks” (see Global investment stewardship principles) and State Street has asked companies to provide disclosure aligned with the four pillars of the TCFD framework (see Guidance on Climate-related Disclosures).(go back)

11Although some categories decreased in prominence or did not make the list (e.g. social impact and community and supply chain management), this does not necessarily reflect the relative level of disclosure on such topics, as companies may have already had robust disclosures on these topics and therefore did not increase those disclosures year over year.(go back)