Print

PrintTodd Sirras is a Managing Director; Austin Vanbastelaer is a Senior Consultant and Justin Beck is a Consultant at Semler Brossy. This post is based on a Semler Brossy memorandum by Mr. Sirras, Mr. Vanbastelaer, Mr. Beck, Alexandria Agee, Sarah Hartman, and Kyle McCarthy.

Related research from the Program on Corporate Governance includes The Perils and Questionable Promise of ESG-Based Compensation (discussed on the Forum here) and The Illusory Promise of Stakeholder Governance (discussed on the Forum here) both by Lucian A. Bebchuk and Roberto Tallarita; and Does Enlightened Shareholder Value add Value (discuss on the Forum here) and Stakeholder Capitalism in the Time of COVID (discussed on the Forum here) both by Lucian A. Bebchuk, Kobi Kastiel and Roberto Tallarita.

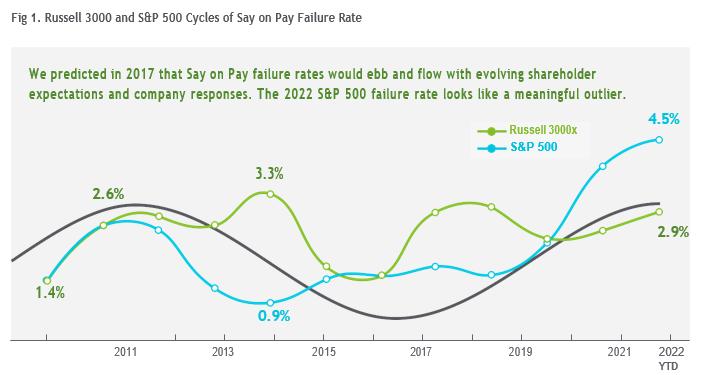

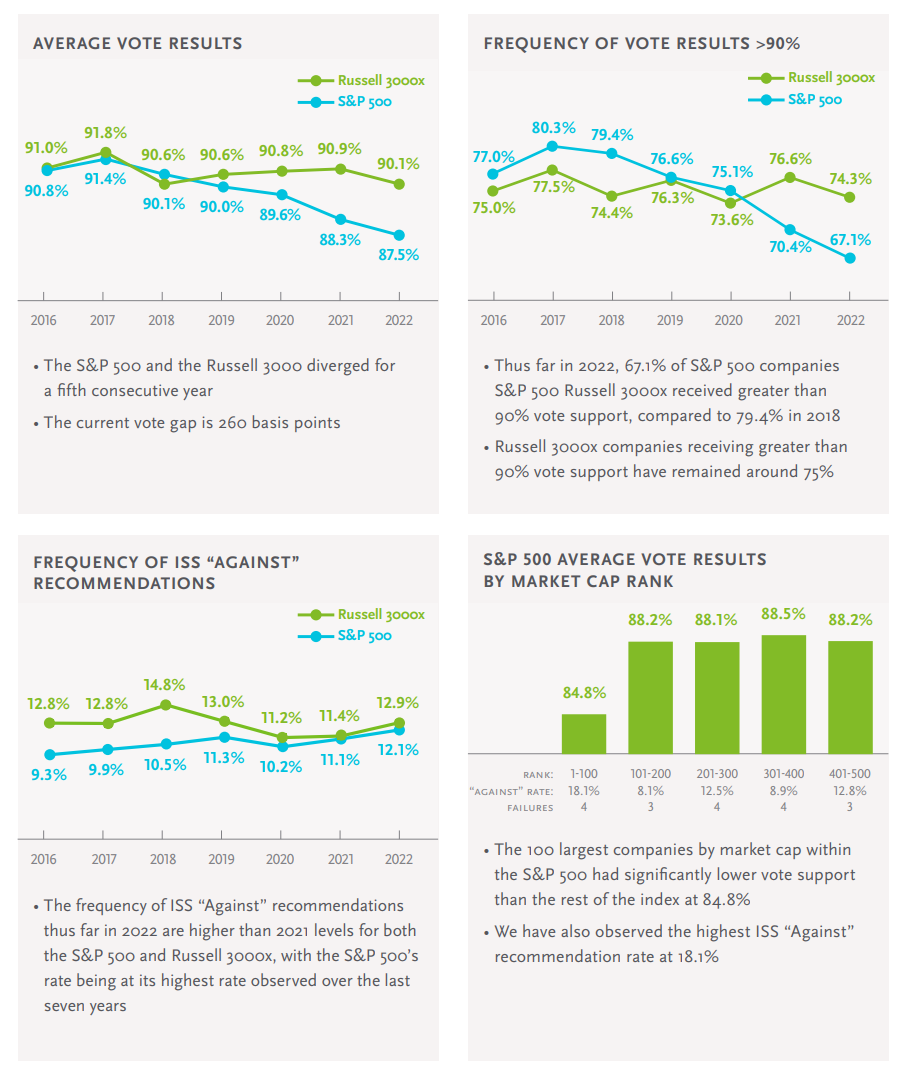

Large companies are receiving lower shareholder support for Say on Pay proposals than ever before. Average Say on Pay vote support for S&P 500 companies declined for a fifth consecutive year in 2022. Meanwhile, the average vote for Russell 3000 companies not in the S&P 500 (“R3000x”) stayed constant over the same five-year period. The 2.6 percentage point gap between average vote support in the S&P 500 (87.5%) and the R3000x (90.1%) in 2022 is the widest since Say on Pay voting began in 2011.

Importantly, this observation is driven by lower support more broadly across the index rather than just a materially higher failure rate or a few isolated cases that drag the average down. A third of S&P 500 companies received lower than 90% support thus far in 2022, compared to an average of 24% over the prior five years.

Vote results between the two indices have diverged due to a fractured governance landscape and differentiated expectations for “good” governance at large- and small-cap companies. Institutional investors and proxy advisors are signaling increased expectations through policy expansion. Their company evaluations now consider a broader set of financial metrics beyond total shareholder return, and their stewardship priorities now focus heavily on environmental, social, and governance (ESG) topics. These are often introduced and applied most firmly to large companies. In some cases, investors have added proxy voting policies on ESG topics that apply only to companies in the S&P 500.

This evolving landscape makes it more difficult to anticipate an individual shareholder’s vote, which creates ambiguous expectations for large-cap companies, given the number of diverse institutional investors that hold stakes in the largest US companies. A combination of the pandemic, dynamic sociopolitical environment, and common large non-annual CEO awards in the tech and IPO space have impacted how investors interpret the appropriateness of CEO pay magnitude relative to performance and the broader stakeholder experience.

Say on Pay History

Vote results in the first several years of Say on Pay voting reflected a lack of standardization. Investor policies on Say on Pay voting were being developed, tested, and refined. At the same time, companies had yet to gain experience in communicating the rationale behind their pay levels and designs with something riskier than an investor call at stake. As such, this first period of Say on Pay voting from 2012 to 2015 was marked by a cycle of relatively high failure rates among Russell 3000 companies that trended downward as companies adapted to investor expectations.

Say on Pay voting again is in a zone where governance expectations are evolving and companies have not fully adjusted, but the outcomes are manifesting differently this time. Over the last few years, we have seen localized volatility predominantly within the S&P 500, especially the largest constituents in the index. The difference in average vote support for S&P 500 companies and Russell 3000x companies increased each year from 2019 to 2021. In 2022, Say on Pay support is down for companies of all sizes, and the wide gap between the two indices remains.

We hypothesized in 2017 in our paper, “Cycles of Say on Pay”, that this dynamic of chaos coming to order and then back to chaos will produce failure rate statistics that rise and fall like a wave over time. This generally has been accurate for the Russell 3000x. The S&P 500 has followed a similar pattern, but the spike in failures in 2022 is an outlier that breaks the trend.

An expectation that 2023 failure rates may fall is suggested by the history but not certain. It is unclear how current and future changes to investor policies and company responses will impact upcoming years of this voting cycle. Will the failure rate shift back down and continue the wave pattern? Will an even higher number of large cap companies start to fail Say on Pay each year? Or will the S&P 500 failure rate trend back down to historical levels while average support remains lower-than-historical? Are ESG topics a fundamental shift that companies will have to catch up to?

Investors are expanding ESG-related policies that impact proxy voting decisions

For now, the degree to which ESG and other non-traditional pay topics directly influence institutional investor voting on Say on Pay is unclear.

Adjacent to the Say on Pay proposal, BlackRock and State Street released guidance in 2021 that states they will vote “Against” a company’s Compensation or Governance Committee Chair for shortcomings on certain ESG topics such as providing EEO-1 disclosure, maintaining a diverse Board, and disclosure on the company’s climate change risks. Parts of State Street’s policies specifically apply to S&P 500 companies.

Both investors have expanded upon their guidelines in subsequent years. It is safe to say that there is a trend toward more robust and prescriptive ESG policies from large institutional investors. However, we are in a stage of “chaotic progression” and have not yet reached a period of “new order.”

For example, investors are starting to combine ESG considerations with the executive pay focus of the Say on Pay proposal. Alliance Bernstein already outlined its expectation that companies integrate ESG as a performance metric in executive compensation. Will other investors codify similar expectations into their voting guidelines, such that “all forces work together”? Will investors air grievances with companies in Say on Pay voting versus another forum such as director election results?

Investors and proxy advisors appear to have developed higher expectations for the largest companies

Expanded investor expectations around relative pay, performance, and recently, good governance is only half the story. The second half is that institutional investors and proxy advisors appear more critical of large-cap S&P 500 companies than their smaller counterparts in the Russell 3000x. Similarly, media attention on executive pay often focuses on the highest paid CEO lists, predominately large company CEOs who received larger-than-typical pay packages or special awards.

We previously discussed this trend in our paper, “Are 2021 Say on Pay Changes Here to Stay”. Investors expect that large-cap companies, in particular, provide strong disclosure and proactively engage with shareholders on controversial pay actions. This development initially manifested when average Say on Pay support for the S&P 500 started to diverge downward from the Russell 3000x in 2019 and 2020. The voting trend accelerated in 2021 and begged the question of whether investors’ voting more critically towards S&P 500 companies was here to stay. Vote results to date in 2022 indicate the answer is yes: the gap between S&P 500 and Russell 3000 average Say on Pay support is the largest since voting began in 2011, and the S&P 500 failure rate jumped 160 basis points above the Russell 3000x failure rate.

We reviewed proxy advisor reports from the last two years to support our commentary on this topic. Our research found that proxy advisors tend to evaluate large- and small-cap companies differently. In particular, they reviewed large-cap companies more critically when CEO pay was high due to a special award, despite strong performance under the advisors’ quantitative pay-and-performance tests. For example, Apple received an “Against” recommendation from ISS due to the CEO’s large compensation package, despite performing in the top quartile relative to its peers. Large-cap companies have also received more visible criticism from larger shareholders and proxy advisors in recent years after adjusting incentive program structures or outcomes for one-time events (e.g., litigation expenses and executive retirement payouts). Given the already high magnitude of pay for some senior executives at large-cap companies, these adjustments can result in significant accounting expenses or divergences in adjusted financial outcomes relative to their GAAP counterparts.

Four significant trends in the data

Say on Pay vote trends have persisted throughout a period of economic volatility

The pandemic and stock market volatility in 2020 added a layer of unpredictability to Say on Pay voting in 2021, particularly for large-cap companies, as the S&P 500’s year-end failure rate ended 140 basis points higher than the Russell 3000x’s. Shareholders voted critically on 2021 Say on Pay proposals from companies that granted special retention awards or changed target performance goals to offset the economic shock in the prior year.

These actions were partly responsible for 56% and 32% of Say on Pay failures, respectively, in 2021. The S&P 500 failure rate spiked in 2021 and the average vote results declined by 130 basis points from the prior year.

That said, these responsive actions by companies were mostly isolated to a short period in the middle of 2020. Few companies adjusted pay programs due to the pandemic in 2021. Despite the lack of adjustments, the S&P 500 failure rate continued to increase in 2022, and the S&P 500 average vote result continued its downward trajectory.

The economy experienced some aftershocks from the pandemic in 2021, but fiscal and monetary policy actions supported a bull market that led to record-level equity valuations in late 2021. Additionally, an evolving hybrid work environment created a highly competitive and mobile talent market. That combination led many companies to grant lucrative equity awards to recruit or retain talent, contributing to a 12% median increase in CEO pay among S&P 500 companies from 2020 to 2021. This landscape has changed drastically since. The stock market declined sharply during the first half of 2022, and growing concerns about inflation have challenged executive incentive plans. Now, many companies are in a vulnerable position, and responsive pay actions could lead to adverse shareholder reactions.

Future Implications

- Companies may feel compelled to address retention concerns caused by underwater equity grants from earlier in the year if the stock market remains near the current level. It is unlikely that shareholders will vote in favor of Say on Pay proposals for companies that grant special awards to the named executive officers in response to this volatility. Say on Pay voting in 2021 reminded us that investors and proxy advisors will be critical of special awards, even in a black swan scenario like the pandemic. Retention actions should focus on levels below the EVPs. Companies that take action for named executive officers should be prepared to disclose strong rationale and engage with shareholders, as they may begin questioning the integrity of pay-and-performance if adjustments are always made during challenging times.

- Boards should stay educated on how ESG expectations and proxy voting implications evolve and ensure their companies at least meet the minimum expectations. Large investors have communicated ESG priorities and started to crystallize them into prescriptive guidelines. The most common approach now is to vote against Committee Chairs at large-cap companies where there are deficits on certain ESG topics. A subset of investors has asked that companies include ESG as a part of executives’ incentive-based pay. Going forward, it’s likely only a matter of time until ESG topics become a stronger consideration within the purview of Say on Pay voting.

- Larger companies and their investors will continue to set the precedent of what is acceptable. The onus will be on large-cap companies to react and adjust first to the evolving investor and proxy advisor guidelines. We predict that S&P 500 Say on Pay results will continue their downward trajectory in future years due to evaluations of likely special retention actions, potential new ESG requirements, and a broader focus on pay equity.