Print

PrintLindsey Stewart is Director of Investment Stewardship Research at Morningstar, Inc. This post is based on his Morningstar memorandum.

Related research from the Program on Corporate Governance includes The Agency Problems of Institutional Investors (discussed on the Forum here) by Lucian Bebchuk, Alma Cohen, and Scott Hirst; Index Funds and the Future of Corporate Governance: Theory, Evidence, and Policy (discussed on the forum here) and The Specter of the Giant Three (discussed on the Forum here), both by Lucian Bebchuk and Scott Hirst; and The Limits of Portfolio Primacy (discussed on the Forum here) by Roberto Tallarita.

Executive Summary

Active ownership—also called “investment stewardship”—has taken on ever greater significance as environmental, social, and governance themes feature more prominently in investing. This has been prompted by the search for solutions to address systemic issues like climate change and rising inequality.

At shareholder meetings, it has become common for environmental and social issues in particular to feature in both management and shareholder resolutions, with the latter rapidly increasing in number this year. Asset managers are responding by making their voting policies on E&S themes more detailed and specific. This is a positive development for investors as it gives them better sight of asset managers’ stances on key issues and helps them select the managers best aligned with their own E&S objectives as well as financial ones.

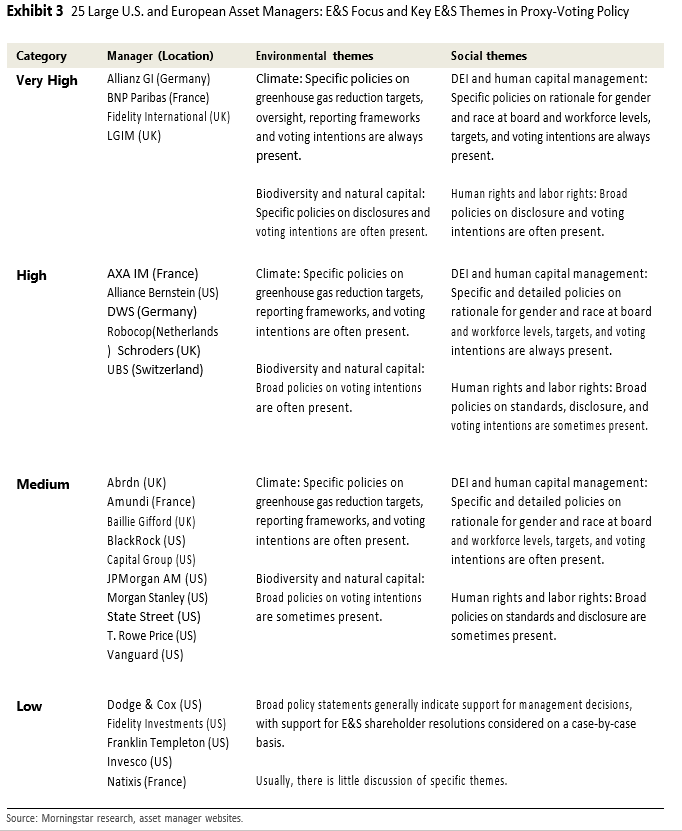

In this report, we dissect the current voting policies of 25 large asset managers—12 in the United States and 13 in Europe—and analyze the key E&S themes they cover. We also discuss the positions these managers take on E&S issues and the level of detail they provide in their policies, grouping them in four categories based on their level of focus on E&S themes, from Very High to Low.

Key Takeaways

- The number of shareholder resolutions on E&S themes, as well as the level of support for many of them, has increased significantly in 2022.

- Asset managers are adding more clarity to their policies on the features of E&S proposals that they will and will not support. This can help investors make informed choices about manager selection.

- Nine of the 13 European asset managers analyzed in this study have a high or very high E&S focus in their proxy-voting policies, while 11 of the 12 U.S. asset managers have a medium or low focus.

- Allianz GI, BNP Paribas, Fidelity International, and LGIM have the highest levels of focus on E&S issues in their proxy-voting policies. The “big three” index managers—BlackRock, State Street, and Vanguard all have a medium E&S focus.

- Among the environmental issues covered, climate, unsurprisingly, is the most common, but biodiversity and other connected topics, such as deforestation and water use, are gaining prominence.

- Among social issues, diversity, equity, and inclusion, or DEI, is the most common topic, covering issues from the board level to the general workforce. Broader human capital management issues, human rights, and labor rights are often also covered.

About Active Ownership

According to the Principles for Responsible Investment—to which the 25 asset managers examined in this study are signatories—active ownership is: “the use of influence by institutional investors to maximize overall long-term value including the value of common economic, social and environmental assets, on which returns and clients’ and beneficiaries’ interests depend.” [1]

Active ownership—also called “investment stewardship”—includes proxy voting, engagement, filing shareholder resolutions, and other forms of influence that investors can use as financial stakeholders. These can be used in combination as complementary strategies to manage investment risk, create and identify investment opportunities, and strengthen the resilience of capital markets.

A key feature of any active ownership strategy is the asset manager’s proxy-voting policy, which sets principles for the way in which asset managers vote on behalf of their clients at shareholder meetings. These policies are becoming important factors in distinguishing asset managers’ approaches to climate change and net-zero transition, gender and racial equality, and other key E&S themes. We take the view that investment stewardship should be guided by an overarching vision and strategy for change and that all of its components—engagements, voting, and other efforts—should be outcome-oriented.

Proxy-Voting Policies

Proxy-voting policies are typically written by specialist stewardship and corporate governance teams at each asset manager who work alongside senior management to develop policies that best fit the manager’s investment objectives. These policies are usually updated annually but may be revised more often, particularly if a response to a major ESG issue is needed. Proxy-voting policies are primarily governance-focused—historically written to set clear voting expectations for asset managers in areas such as:

- Board composition, independence, and effectiveness

- Management and board remuneration

- Shareholder rights, M&A, and capital issuance

- Financial reporting, audit, and internal controls

While proxy-voting policies continue to focus on addressing governance themes, increasingly they also include guidance on how investors intend to vote on environmental and social proposals, in areas such as:

- Climate change

- Biodiversity and natural capital

- Diversity, equity, and inclusion and human capital management

- Human rights and labor rights

Key Trends

Recent votes on climate policy at company shareholder meetings in North America and Europe have thrown into sharp focus the importance of shareholders using their votes to drive positive outcomes on ESG issues alongside shareholder value.

This is particularly true in the energy and banking sectors regarding climate, amid increasingly urgent warnings from the scientific community that companies need to take urgent action to bring down greenhouse gas emissions to prevent global warming from exceeding 1.5 degrees Celsius above preindustrial levels. The proxy contest between Engine No. 1 and oil majors Exxon Mobil XOM and Chevron CVX on climate action and governance in 2021 is perhaps the most notable event in this area. Shareholders are also increasingly taking an interest in how banks—such as Wells Fargo WFC, Citigroup C, and Bank of America BAC in the U.S., and Barclays BCLYF and HSBC HSBC in the United Kingdom—will ensure net-zero ambitions are reflected in their lending portfolios.

However, other key environmental and social issues—including biodiversity and natural capital, DEI, and human and labor rights—are gaining prominence in shareholder votes. Much of this increase is attributable to the SEC’s revised guidance [2] addressing “significant social policy issues,” which broadened the definition of permissible shareholder resolutions.

The number of shareholder resolutions on E&S themes has grown rapidly in the most recent proxy year, [3] as has the number of such resolutions with significant shareholder support.

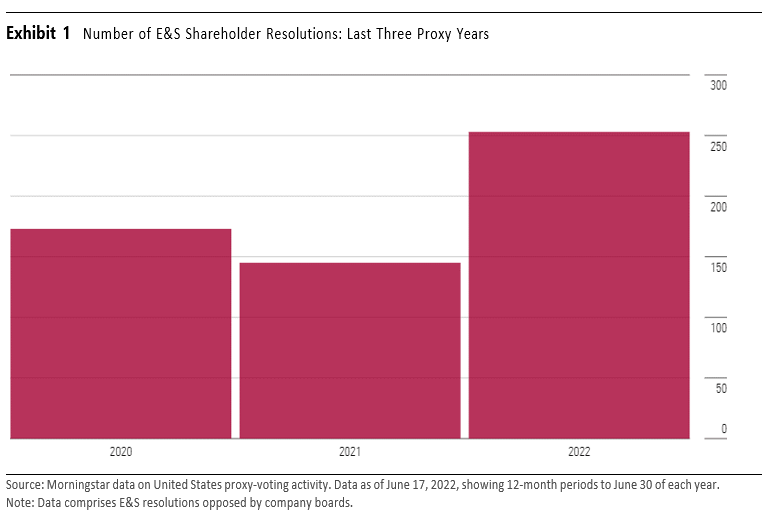

According to Morningstar’s data on U.S. proxy voting, the number of E&S shareholder resolutions in the United States that were opposed by company boards increased from 145 in the 2021 proxy year to over 250 this year (see Exhibit 1).

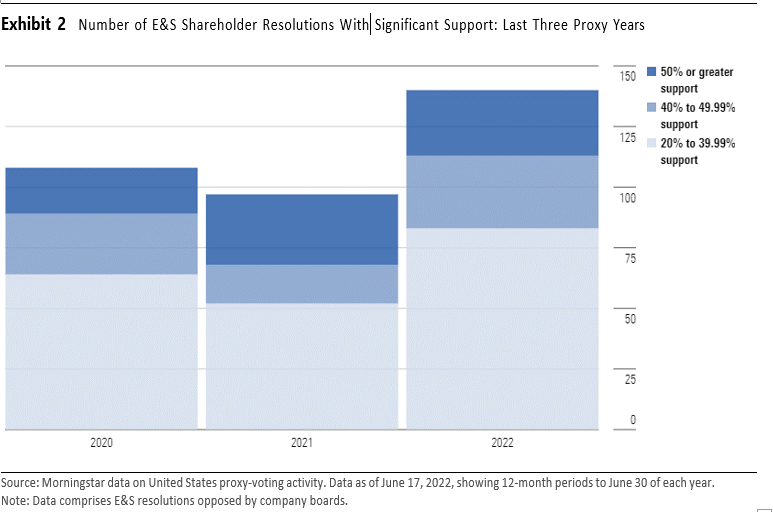

Out of those 2022 proxy-year resolutions, 140 gained the support of more than 20% of shareholders. Fifty seven gained more than 40% support, and 27 actually gained majority shareholder support (see Exhibit 2).

Many asset managers have responded to this trend by providing more detailed and specific policies on what E&S proposals they would support. This leads to more predictable voting outcomes for asset managers, which in turn can help investors make informed choices about which managers’ active ownership approach best reflects their own E&S priorities.

This paper analyzes the level of focus on these E&S themes in the current proxy-voting policies of 25 asset managers. These managers, including 12 based in the United States and 13 based in Europe, are a representative selection of the largest equity fund managers that Morningstar has previously assessed for the ESG Commitment Level rating. The 12 U.S. asset managers make up three fourths of the USD 54 trillion of assets under management represented in our analysis.

Analysis of Focus on E&S Themes

We analyzed the current proxy-voting policies of the 25 asset managers selected for this study. We assessed their overall active ownership philosophies and approaches to shareholder resolutions on E&S themes. We also evaluated each manager’s level of focus on key E&S themes—including climate, biodiversity and natural capital, DEI and human capital management, and human rights and labor rights—considering whether policies on these themes are present and sufficiently specific to give predictable voting outcomes at shareholder meetings.

We then ranked managers and grouped them in four categories based on their level of focus on E&S themes, from Very High to Low. Our findings are summarized in Exhibit 3 below.

Nine of the 13 European managers in our analysis have a High or Very High focus on E&S themes in their proxy-voting policies. Managers with a High or Very High E&S focus tend to include detailed and specific policies on several aspects of climate policy and often cover other environmental themes such as biodiversity, natural capital, deforestation, and water usage. They also outline in detail their rationale, targets, and voting intentions for DEI and human capital management issues—advocating for greater female and racial/ethnic representation on boards—and often also have detailed policies for human rights and labor rights.

Conversely, most of the large U.S.-based asset managers—including BlackRock, Fidelity, State Street, and Vanguard—have a Medium or Low focus on E&S themes in their proxy-voting policies.

AllianceBernstein, with a High E&S focus, is an exception. Managers with a Medium E&S focus often outline their expectations and voting intentions for climate matters, but in less detail than managers with a High or Very High E&S focus. Additionally, it is much rarer to find specific policies for biodiversity issues within this group. Finally, managers with a Medium E&S focus usually have detailed policies on DEI issues—also advocating for greater female and racial/ethnic representation on boards—but offer less detail on human rights and labor rights issues.

Meanwhile, managers with a Low E&S focus tend not to have detailed E&S policies—they often indicate that operational matters are left to management discretion with case-by-case consideration of support for shareholder resolutions on E&S issues.

The 25 asset managers in our selection represent USD 54 trillion of AUM, [4] of which USD 40 trillion (75%) is represented by the 12 U.S. asset managers. The “big three” index asset managers—BlackRock, Vanguard, and State Street—account for USD 23 trillion of AUM; all three have a Medium E&S focus. Managers with a High or Very High E&S focus (shown in dark green on the chart below) account for USD 9 trillion of AUM. All except one—AllianceBernstein—are based in Europe.

This apparent transatlantic divide can be attributed to several factors.

- Market culture: U.S. asset managers have long taken a strict shareholder value approach to their dealings with company boards and management in part due to the narrow definition of fiduciary duty in the U.S., which requires that managers focus on maximizing financial returns for the client. This contrasts with the European view that fiduciary responsibility encompasses a broader range of issues, including the impact of companies on the environment and society at large. U.S. managers have only recently espoused a more stakeholder-conscious stance on E&S issues.

- Regulation: European regulations implemented in recent years, such as the Sustainable Finance Disclosure Regulation and the Non-Financial Reporting Directive, have driven companies and asset managers to make fuller disclosures and set more-complete strategies for tackling key E&S issues.

- Stewardship codes: The use of best practice codes for investment stewardship started in the United Kingdom in 2010 and has become a key element of asset manager selection in Europe. This, in turn, has prompted greater focus by European asset managers on E&S policy and engagement in a way that has not so far manifested in the United States.

Summary of Findings

We examined the 25 asset managers’ proxy-voting policies from a variety of angles. Their overall approach to active ownership and consideration of shareholder resolutions reveals much about their level of focus on E&S themes.

Among environmental issues covered by voting policies, climate, unsurprisingly, is the most common, but biodiversity and other connected topics, such as deforestation and water use, are gaining prominence.

Among social issues, diversity, equity and inclusion—from board level to the wider workforce—is the most common topic. Broader human capital management issues, human rights, and labor rights are often also covered.

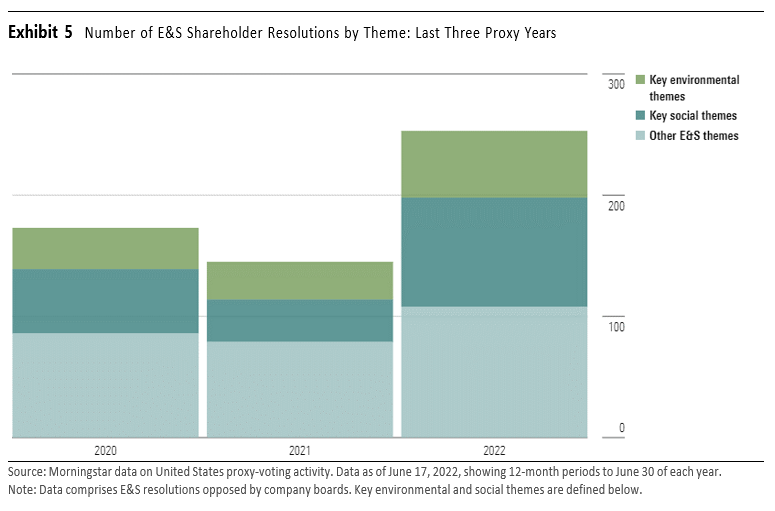

We refer to these issues as key environmental and social themes in this report, not just because they appear more frequently in asset managers’ proxy-voting policies but also because the number of shareholder resolutions on these themes has increased rapidly this year (see Exhibit 5). According to Morningstar data, in the 2022 proxy year, the number of shareholder resolutions on climate and environment issues has almost doubled to 55; the comparable number for DEI, human capital, and human rights and labor rights issues has more than doubled to 90.

The summary of our findings, below, covers the 25 asset managers’ approaches to:

- Active ownership philosophy

- E&S shareholder resolutions

- Key environmental themes: climate; biodiversity, and natural capital

- Key social themes: DEI and human capital management; human rights and labor rights

We have examined each of these areas in detail on the following pages, along with wording examples taken from the managers’ policies, which can be found on each company’s stewardship web page.

Examples of policy wording from each of the managers can be found in Appendix 1. Links to the asset managers’ policies and disclosures can be found in Appendix 2.

Active Ownership Philosophy

The wording in the 25 asset managers’ proxy-voting policies—about their overall approach to ESG, sustainability, and active ownership—gives a strong indication of their level of E&S focus.

While all of them state their aim of maximizing shareholder wealth, they tend to use different language when describing their approaches to E&S themes affecting broader stakeholder groups. We have identified three types of overall active ownership philosophies in the policies we have analyzed.

Asset managers that we have described as having a High or Very High E&S focus tend to write stakeholder-inclusive and stakeholder-conscious policies.

Asset managers with a Medium E&S focus tend to use stakeholder-conscious language, occasionally using stakeholder-inclusive policies for key issues like climate and DEI. Asset managers with a Low E&S focus often emphasize their strict shareholder-value approach.

E&S Shareholder Resolutions

A broad cross-section of investors, from individuals to large public pension funds, participates in the proxy process by filing shareholder resolutions, which have become a key area of focus in recent years. Shareholder-resolution policies covering governance themes like shareholder rights, board composition and independence, and management pay have long been commonplace. However, the increasing focus on E&S issues such as climate change and racial equity have prompted many asset managers to expand their policies on these themes.

Asset managers across the spectrum indicate that they consider E&S shareholder resolutions on their individual merits and that they are generally supportive of shareholder resolutions that seek to improve disclosure or company conduct in important areas. Yet our analysis reveals some key areas of difference between managers.

Several of the managers—mostly those with High and Very High E&S focus and a few with a Medium E&S focus—go further than this, providing considerable detail on the attributes of shareholder resolutions they are inclined to support and often covering several distinct E&S themes in depth. Most managers with a Low E&S focus tend to give little detail other than to say they support shareholder resolutions that are positive for shareholder value and that they decide case-by-case.

A few managers also highlight additional considerations of shareholder resolutions they are not inclined to support—they often object to “highly prescriptive” or “poorly framed” proposals, or to proposals covering issues that are already being addressed by the company.

BlackRock generated news headlines in May when it announced it was “likely to support proportionately fewer [shareholder resolutions] this proxy season than in 2021” due to an increase in the number of proposals perceived as inappropriately prescriptive. [5] The data for the 2022 proxy year suggest this trend covers more than just one asset manager (see Exhibit 7).

This year, the number of E&S shareholder resolutions with a very low level of shareholder support (5% or less) has increased to 13% of the total—that is, 33 resolutions—up from around 5% in the two previous proxy years.

Key Environmental Themes

Climate

Climate is the environmental theme that receives the greatest amount of attention from asset managers. Those with a High or Very High E&S focus tend to do most or all of the following.

- Request that companies disclose their targets for greenhouse gas emissions reduction (often referring to the goals of the 2015 Paris Agreement).

- Request alignment of climate-related disclosures with internationally recognized frameworks—for example, the Taskforce on Climate-Related Financial Disclosures, the Science Based Targets initiative, and others.

- Request alignment of their public policy advocacy activities (for example, political lobbying or membership of trade associations) with their stated climate objectives.

- Emphasize their expectation that climate matters are subject to board-level oversight by identified directors.

- Request a “Say on Climate” vote allowing shareholders to opine on the company’s climate strategy.

- State clearly what escalations will be applied to companies falling short of their expectations, including:

- voting intentions (for example, against specific directors, all directors, or the annual report and accounts); and/or

- partial or full divestment.

Managers with a Medium E&S focus often refer to their expectations regarding greenhouse gas reduction targets and disclosure frameworks but refer less frequently to the other issues mentioned above; voting intentions tend to be less clear. Managers with a Low E&S focus tend not to include specific expectations and voting intentions on climate matters, usually deferring to management discretion.

Biodiversity and Natural Capital

Policies in this area tend to be less specific than for climate. However, asset managers with a High or Very High E&S focus—and, less frequently, some with a Medium E&S focus—tend to:

- Request commitments from companies to reduce negative impacts on biodiversity and natural capital and provide greater disclosure.

- Request specific disclosures and actions regarding deforestation, water pollution, and water usage in areas of high water-supply stress.

- Be usually less specific on their voting intentions regarding biodiversity and natural capital compared with climate.

Key Social Themes

DEI and Human Capital Management

Alongside public focus on gender and racial inclusion, increased regulation in the U.S. and the U.K. has prompted many asset managers to raise their expectations of companies regarding practice and reporting on DEI issues. This is the only area where we have observed managers across the full spectrum of E&S policy focus—from Low to Very High—to have outlined specific policies and voting intentions.

- Managers of all kinds highlight their rationale that evidence shows that diversity of gender, race, ethnicity, and other characteristics at board-level improves business-decision-making and helps minimize risk.

- Managers with High or Very High E&S focus—and several of those with Medium E&S focus—tend to expect:

- at least around one third of the boards of large-cap companies in developed markets to be composed of women; and

- a minimum participation of racially or ethnically diverse individuals on boards in line with local norms.

- Less stringent expectations are often set for smaller companies or those in other markets, but further development in these areas over time is often expected.

- Several managers—again, usually those with High or Very High E&S focus but also a few with Medium E&S focus—outline their intentions to vote against director appointments where these targets are not met.

Additionally, several managers—usually those with High or Very High E&S focus—outline their expectations for DEI and human capital management along similar principles, addressing the matter from a business performance perspective. Clearly defined voting intentions in these areas are rarer, although some managers outline the circumstances of their potential support for shareholder resolutions.

Human Rights and Labor Rights

Human rights and labor rights voting policies tend to be published by managers with a High or Very High E&S focus—a few managers with Medium E&S focus also do so.

Several managers mention their expectation that companies manage human rights and labor rights risks in line with principles outlined by the United Nations; however, it is uncommon to find specific voting intentions or escalations in these policies.

A few managers mention that they would vote against individual directors if companies were unresponsive to engagement on human rights and labor rights. Some also outline the nature of shareholder resolutions on these themes that they would be willing to support.

The complete publication, including Appendix, is available here.

Endnotes

1Principles for Responsible Investment website(go back)

2Shareholder Proposals: Staff Legal Bulletin 14L (CF)(go back)

3A proxy year starts on July 1 and ends on June 30 to accommodate the fact that most shareholder meetings occur between March and(go back)

4AUM as of 31 December 2021. (A previous version of this paper showed AUM for Allianz Group instead of Allianz GI only. This has been corrected in the commentary and in Exhibit 4 )(go back)

5BlackRock, May 2022: 2022 climate-related shareholder proposals more prescriptive than 2021(go back)