Print

PrintJohn Borneman is Managing Director, and Jennifer Teefey and Matthew Mazzoni are Senior Associates at Semler Brossy Consulting Group LLC. This post is based on a Semler Brossy memorandum by Mr. Borneman, Ms. Teefey, Mr. Mazzoni, Mira Yoo, and Jay Veale.

Related research from the Program on Corporate Governance includes Paying for Long-Term Performance (discussed on the Forum here) by Lucian Bebchuk and Jesse Fried; and The Perils and Questionable Promise of ESG-Based Compensation (discussed on the Forum here) by Lucian A. Bebchuk and Roberto Tallarita.

There has been a rapid increase in the adoption of ESG metrics for executive incentive plans across the S&P 500 over the past several years. This has largely been driven by continued shareholder focus on human capital management (HCM) and environmental issues. By adding these ESG metrics to incentive plans, Companies are signaling a heightened sense of commitment to their stated ESG goals.

Key Takeaways

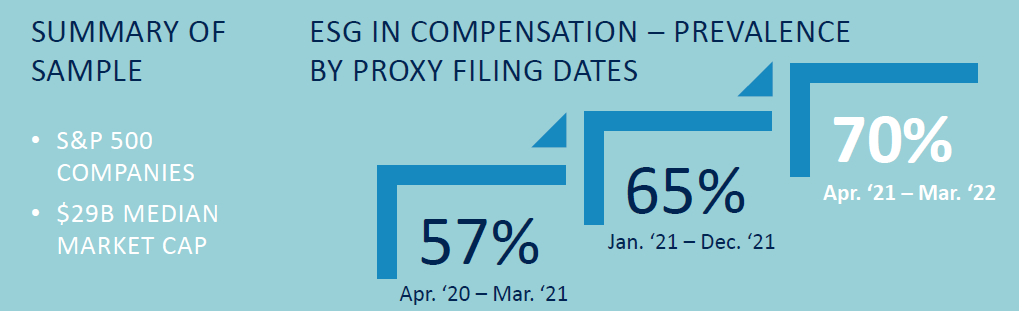

This year, there was a nearly 23% increase in the proportion of S&P 500 companies applying ESG metrics in incentive plans, at 70% prevalence compared to 57% prevalence a year ago. Diversity & Inclusion (D&I) and Carbon Footprint metrics had the largest year over year increases.

- Investors are strongly focused on HCM and environmental topics as the most important ESG issues. In this year’s data, we have specifically analyzed the prevalence of metrics within these two categories

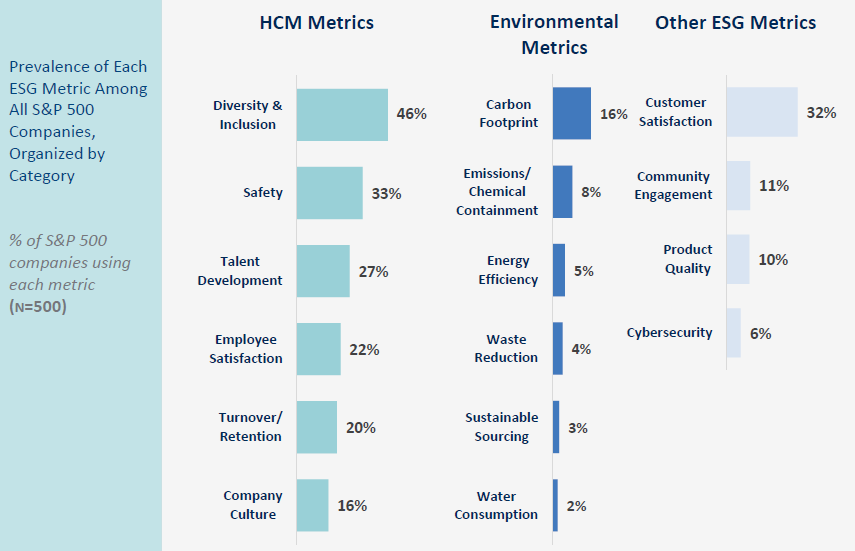

- Although D&I continues to lead as the most prevalent metric (46%), companies appear to be taking a holistic approach to HCM in incentives by using other HCM metrics along with D&I

- Environmental metrics remain uncommon in incentive plans. However, prevalence is increasing, with Carbon Footprint emerging as the environmental measure of choice

Methodology and S&P 500 Dataset

Semler Brossy has published an annual report series to track the growth of ESG metrics in incentive plans for the past two years. This post examines prevalence of ESG metrics across S&P 500 companies in the past year (proxies filed from April 2021 to March 2022). Future reports will assess differences in ESG prevalence by industry.

Structure of ESG in Incentive Plans

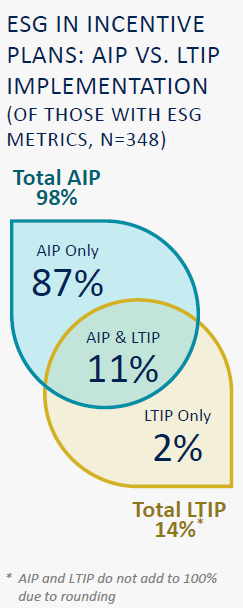

Of the S&P 500 companies with ESG metrics in incentive plans (348 of the 500), nearly all (98%) incorporate metrics into their annual incentive plans (AIP). Conversely, ESG metrics in long term incentive plans (LTIP) are still relatively uncommon (14% of the same group) but growing in prevalence. We expect that this dichotomy is primarily because this is a new area of measurement for incentive plans and companies are still learning what works and what doesn’t. Equity incentives also have more accounting complexity, and for ESG metrics, many companies shy away from the type of formulaic goals needed to ensure fixed accounting.

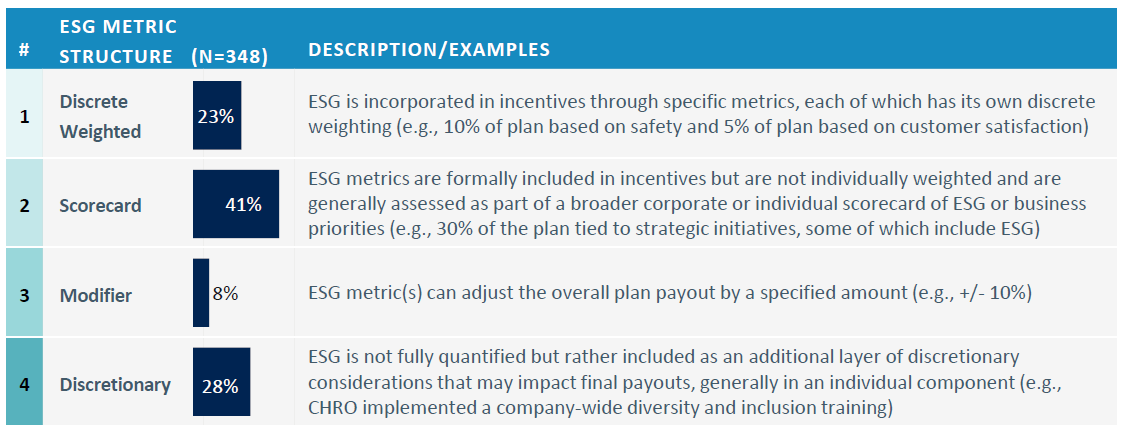

The most prevalent structure is to include ESG metrics as part of a scorecard (41%). A scorecard approach allows companies to designate a certain percentage of an incentive plan to a group of two or more metrics, which may include strategic or operational goals in addition to ESG. The scorecard provides Committees more discretion to assess performance and to update goals and priorities each year without adjusting the fundamental incentive plan design.

Discrete, weighted metrics, where each metric has a specific goal and a designated weighting, are often the most impactful design elements in incentive plans. This structure is used by 23% of S&P 500 companies with ESG metrics in incentives and is primarily used for metrics that are operationally focused, as opposed to sustainability oriented. We expect that this trend is driven by the longer experience with these metrics and relative ease of goal setting.

Metric Categories

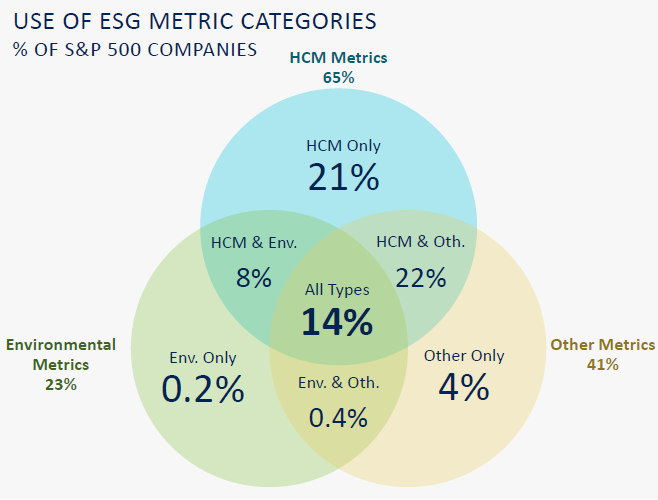

As we’ve historically discussed, ESG covers a broad spectrum of both operational and sustainability issues. Increasingly, investors are focused primarily on social and environmental sustainability measures. We’ve grouped the primary ESG measures into three categories to align with how investors and companies generally view ESG dimensions: Human Capital Management (HCM), Environmental, and Other ESG.

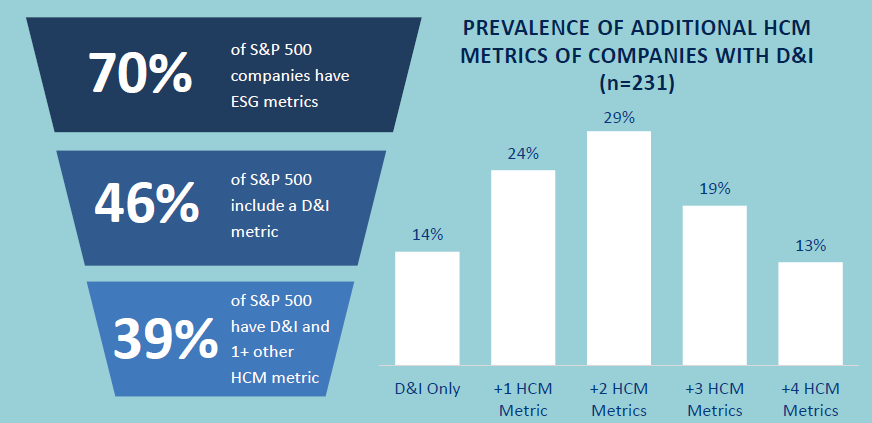

We found that 70% of the S&P 500 included ESG metrics in either their annual or long term incentive plan this year. Moreover, nearly half (45%) of S&P 500 companies include metrics from two or more ESG categories in their incentive design plans.

Also of note, 65% of S&P 500 companies have adopted HCM metrics, which demonstrates that nearly all companies that have included ESG metrics have specifically included HCM metrics.

Metric Prevalence

| HCM 65% |

Overall, HCM is the most prominent category of metrics, with 65% of the S&P 500 incorporating these considerations into incentive plans. This aligns with broader market talent related challenges that many companies are experiencing, including the highly competitive market for talent. |

|---|---|

| Env. 23% |

Consistent with prior years, environmental metrics are the least prevalent ESG category considered in only 23% of S&P 500 compensation plans; however, this is a 64% increase from 14% of S&P 500 companies last year. |

| Other 41% |

Other ESG metrics consist of operational, consumer focused, and broader social measures and represents the second most prominent category, with 41% of the S&P 500 implementing these measures. |

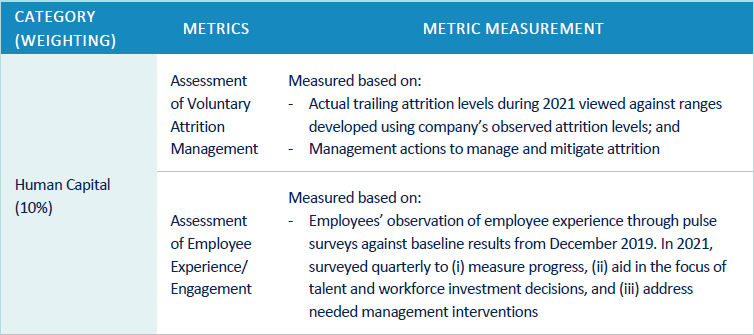

Human Capital Management Metrics

HCM is the most prominent category of ESG metrics, with 65% of the S&P 500 considering these metrics in executive incentive plans. All HCM metric categories increase substantially in prevalence year over year. We expect that this increase is driven by stakeholder focus on talent related issues, intense competition for talent, and the growing knowledge of how to measure and assess HCM performance.

Consistent with last year, D&I is both the most prevalent metric within HCM and overall ESG, and the metric that experienced the second highest year over year increase in prevalence (behind Carbon Footprint). D&I is considered in incentive plans at 46% of all S&P 500 companies, which represents a 64% increase when compared to last year’s 28% prevalence.

Although D&I is the most common metric, our findings show that companies generally take a more holistic approach to assessing HCM achievements. The exhibit below shows that nearly half of the S&P 500 include a D&I measure in their incentive plans. Of those companies, 86% also include at least one other HCM metric, and over half have at least two additional HCM metrics in their incentive plan designs.

Environmental Metrics

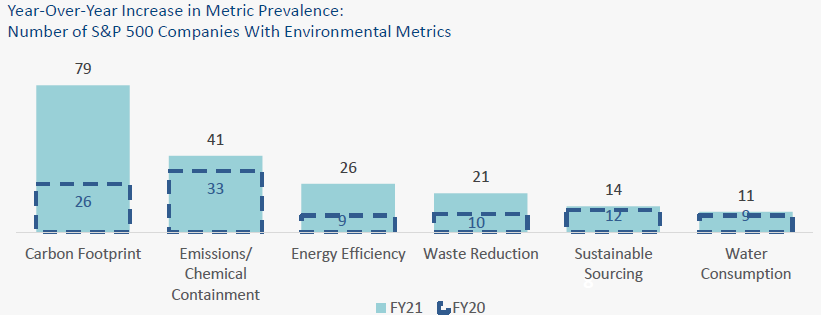

Although environmental metrics are the least prevalent grouping of ESG metrics in incentives, their prevalence has increased 64% year over year, from 14% to 23%. Carbon footprint metrics have been a key driver of this increase and have emerged as the environmental metric of choice for S&P 500 companies. Carbon footprint metrics experienced an over 300% year over year increase in prevalence, from 5% to 16% prevalence across the S&P 500. This was the largest increase among all ESG metrics year over year.

As major institutional investors continue to advocate for companies to consider risks and opportunities associated with climate change, we expect that pressure to add environmental measures will increase. Moreover, with two thirds of S&P 500 companies having set greenhouse gas emissions reduction targets, [1] we believe that carbon footprint metrics will continue to lead prevalence among environmental measures. Additionally, recent SEC guidance on expanded climate related disclosures may further accelerate this trend.

We hypothesize that challenges associated with goal setting and measuring achievements in a timely manner have historically deterred many companies from incorporating environmental measures into incentive design plans. We expect that as more companies are disclosing information around how they consider environmental measures in compensation, they are setting the standard and paving a path for more companies to follow suit.

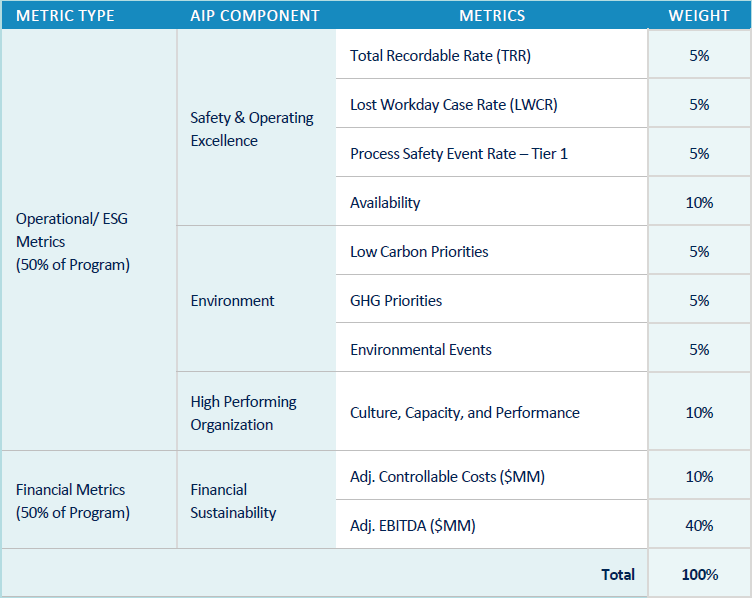

Case Study: Phillips 66

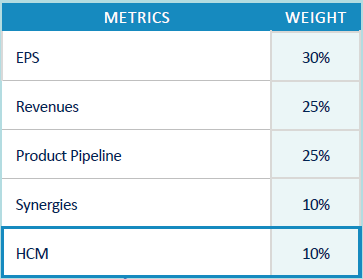

As a petroleum Company, Phillips focuses on its impact on stakeholders through its commitment to its corporate values of safety, environment, diversity, and social responsibility. These values are reinforced in Phillips’ annual incentive program which is tied to environmental metrics, including low carbon priorities, and HCM metrics focused on employee safety and culture. Phillips weights operational sustainability objectives, which include ESG and HCM metrics, at 50% of the annual incentive plan, with the remaining 50% dedicated to financial goals (Controllable Costs and EBITDA).

Case Study: Bristol Myers Squibb Co.

Bristol Myers Squibb Co. is a pharmaceutical giant that places a strong emphasis on retaining and developing critical talent to ensure that its leadership is exemplifying its “BMS Values” of accountability, inclusion, innovation, integrity, passion, and urgency. This is supported through their incorporation of human capital management goals worth 10% of their annual incentive plan based on maintaining high retention and employee engagement levels. These metrics have been maintained at the same weighting in the plan since their inception in 2020. Looking forward into 2022, the annual incentive plan will evolve to incorporate a 10% ESG scorecard in lieu of the HCM goals that will be “aligned to [Bristol Myers Squibb’s] commitments on sustainability and social

impact.”

Case Study: Xylem Inc.

As an industrial company focused on water technology, Xylem places a strong emphasis on ESG in its business as exemplified by its inclusion in both its AIP and LTIP. Xylem incorporates ESG in its annual incentive program as part of the individual objectives worth 25% of the program, which include goals on customer success, diversity and inclusion, company culture, talent development, community engagement and sustainability (the remaining 75% of the AIP is weighted evenly between organic revenue, adj. operating income, and free cash flow conversion metrics).

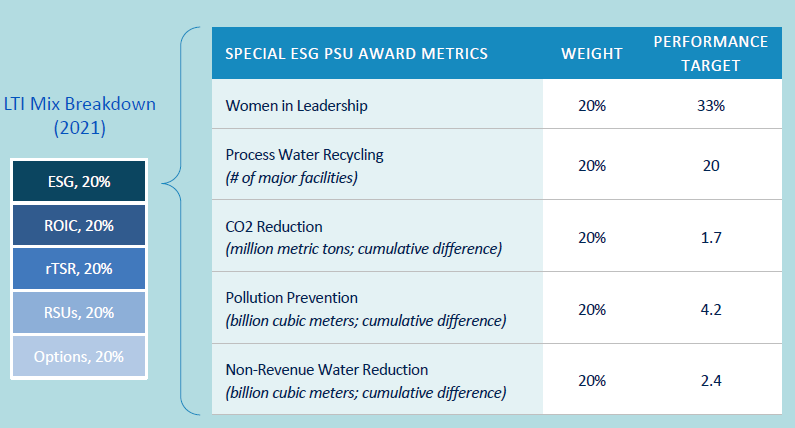

Separately, Xylem offered a special PSU award to its executive team in 2021 focused 100% on key ESG priorities. This award has a 4 year performance period to promote long term achievement against key ESG goals and is valued approximately at 10% to 15% of total compensation for all NEOs. Additionally, the award represents a 25% incremental increase on top of prior years’ target equity grants for the NEOs and is worth 20% of the overall 2021 LTI mix for each NEO.

Endnotes

1Refinitiv Research: https://www.refinitiv.com/perspectives/future-of-investing-trading/are-sp-500-companies-prioritizing-environmental-sustainability/(go back)