Print

PrintMatteo Tonello is Managing Director of ESG Research at The Conference Board, Inc. This post is based on a Conference Board memorandum by Merel Spierings, in partnership with ESG data analytics firm ESGAUGE and in collaboration with Debevoise & Plimpton, the KPMG Board Leadership Center (BLC), Russell Reynolds Associates, and the John L. Weinberg Center for Corporate Governance at the University of Delaware.

As US corporations seek to increase diversity of backgrounds, skills, and professional experience on their boards, they face a central hurdle: limited board turnover that creates few openings for new directors. Indeed, the percentage of newly elected directors in the S&P 500 has remained flat over the past several years. To overcome that hurdle, boards can (temporarily) increase their size—which they are doing modestly. [1] Additionally, they can adopt and implement board refreshment policies and practices that foster an appropriate level of turnover within the current ranks of the board.

Regardless of their approach to board refreshment, companies should expect continued investor scrutiny in this area. Indeed, while institutional investors may defer to the board on whether to adopt mandatory retirement policies, many are keeping a close eye on average board tenure and the balance of tenures among directors and will generally vote against directors who serve on too many boards.

This post provides insights about board refreshment policies and practices, as well as director evaluations at S&P 500 and Russell 3000 companies. Our findings are based on data pulled on July 7, 2022, from our live, interactive online dashboard powered by ESGAUGE as well as a Chatham House Rule discussion with leading in-house corporate governance professionals held in April 2022. Please visit the live dashboard for the most current figures. [2]

Insights for What’s Ahead

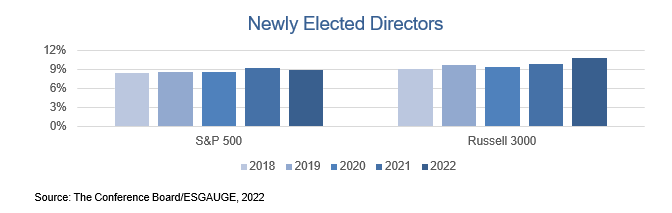

- Companies, especially in the S&P 500, are going to face challenges in increasing the diversity of backgrounds, skills, and professional experience on their boards if they continue to elect new directors at the current rate. In the S&P 500, the percentage of newly elected directors has held steady at 9 percent since 2018. By comparison, in the Russell 3000, it has increased from 9 percent in 2018 to 11 percent as of July 2022. To accelerate the diversification of their board, many companies may want to consider adopting a comprehensive approach, which may include adjusting the size of the board, board refreshment, and director succession.

- Companies should consider a variety of board refreshment tools to enhance demographic diversity and add relevant skills and experience to the board. To promote refreshment, boards can institute policies that (1) require board turnover (e.g., mandatory retirement age and term limits), (2) trigger a discussion of turnover (e.g., limit the number of public boards on which a director may sit or require directors to resign upon a change in their primary professional occupation), and (3) reinforce a culture of board refreshment, which may be the most important step that boards can take. A culture in which it’s fully acceptable for directors to rotate off a board before they are required to do so can be created not only by establishing guidelines on average board tenure, but also through setting initial expectations for director tenure through the director recruitment and onboarding process, as well as having candid discussions during the annual board evaluation and director nomination processes about how the current mix of directors matches the company’s needs. Such processes reinforce the message that no stigma is associated with rotating off a board before one is required to leave.

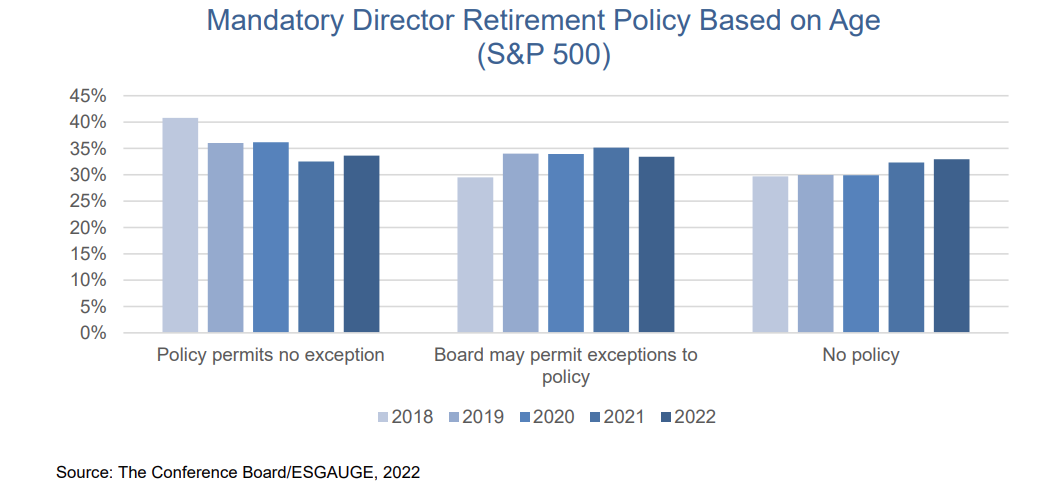

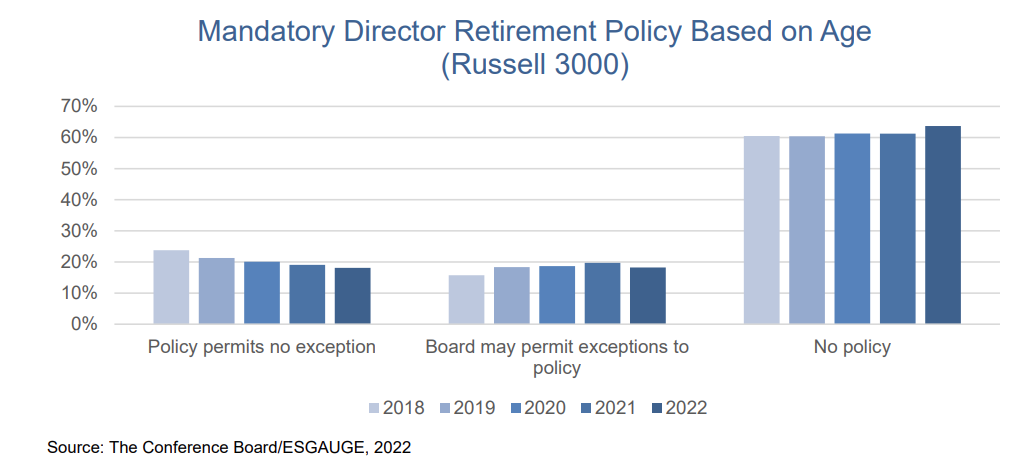

- Companies are moving away from policies that mandate turnover, as these force directors to leave based on tenure or age even when they are still valuable and strong contributors. Very few companies have term limits: as of July 2022, only 6 percent of S&P 500 companies and 4 percent of Russell 3000 companies disclosed a mandatory retirement policy based on tenure. (The most common term limits are either 12 or 15 years.) While mandatory retirement age policies are still common, companies have started to move away from them: in the S&P 500, the share of companies with such a policy declined from 70 percent in 2018 to 67 percent as of July 2022, and from 40 to 36 percent in the Russell 3000. Moreover, companies are increasingly permitting exceptions to the retirement age policy: the share of S&P 500 companies whose policy permits no exception declined from 41 percent in 2018 to 34 percent as of July 2022, and from 24 to 18 percent in the Russell 3000. They are also raising the retirement age: the share of S&P 500 companies with a retirement age of 75 rose from 39 percent in 2018 to 49 percent as of July 2022, and from 42 to 52 percent in the Russell 3000. While mandatory retirement policies can be criticized as arbitrary, allowing exceptions to those retirement policies can not only be viewed as favoritism but also impede board turnover.

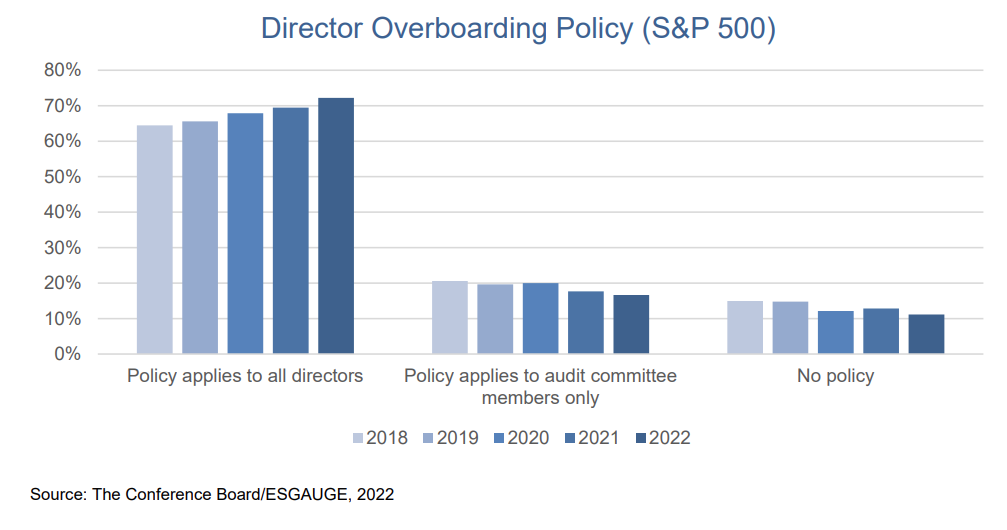

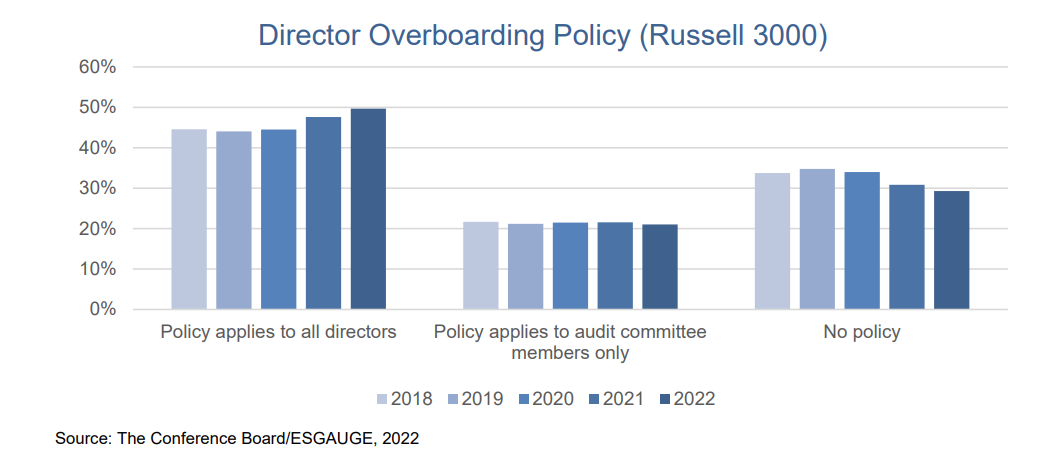

- While companies have considerable flexibility in their approach to board refreshment, expect continued investor attention to this topic. While major institutional investors usually defer to the board’s determination in setting mandatory retirement age or establishing term limits, they are keeping a close eye on board tenure and may oppose or withhold votes from boards that seem to have an insufficient combination of short-, medium, and long-tenured directors. [3] Further, BlackRock, State Street, and many other investors will generally vote against independent directors who serve on more than four public boards, which is why companies are increasingly limiting the number of other public company directorships their board members can accept. The share of companies in the S&P 500 with an overboarding policy applicable to all directors grew from 64 percent in 2018 to 72 percent as of July 2022 in the S&P 500, and from 45 to 50 percent in the Russell 3000. Indeed, director overboarding policies are a relatively evenhanded way of ensuring that directors are not overcommitted in this era of increasing workload, and they can prompt a thoughtful discussion between companies and their board members as to whether the director should step down from a particular board.

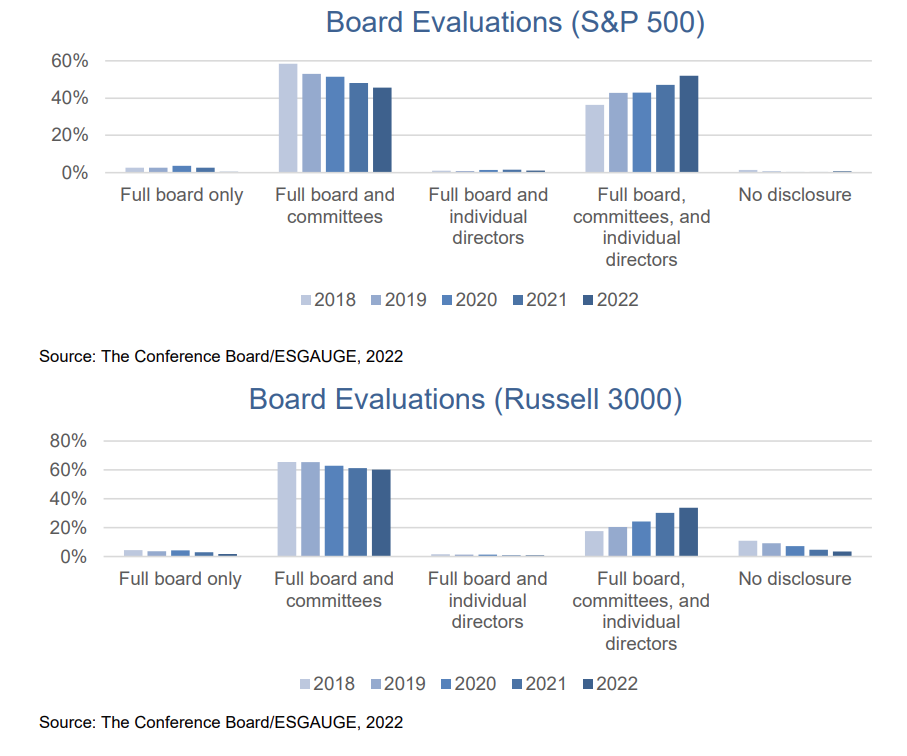

- Periodic individual director evaluations—which are growing in popularity along with companies’ use of independent facilitators for board evaluations— can promote board diversity and refreshment. In the S&P 500, conducting a combination of full board, committee, and individual director evaluations has become the most common practice (52 percent of companies reported conducting this combination of evaluations as of July 2022 compared to 37 percent in 2018). As our discussion with in-house corporate governance professionals revealed, individual director evaluations and/or the use of independent facilitators allow companies to have fruitful discussions about many challenging topics, including the skills and expertise needed on the board in the current environment, and in fact can lead to changes in board composition. Companies have found that they do not need to evaluate individual directors or use outside facilitators every year; indeed, these reviews can be more effective and less disruptive if conducted every two or three years.

Board Refreshment

Election of New Directors

- The aggregate rate at which new directors are elected at larger companies has remained virtually unchanged in recent years, potentially leading to challenges in increasing the diversity of backgrounds, skills, and professional experience. In the S&P 500, the share of newly elected directors has held steady at 9 percent since 2018. By comparison, in the Russell 3000, the share of new directors has increased from 9 percent in 2018 to 11 percent as of July 2022. [4]

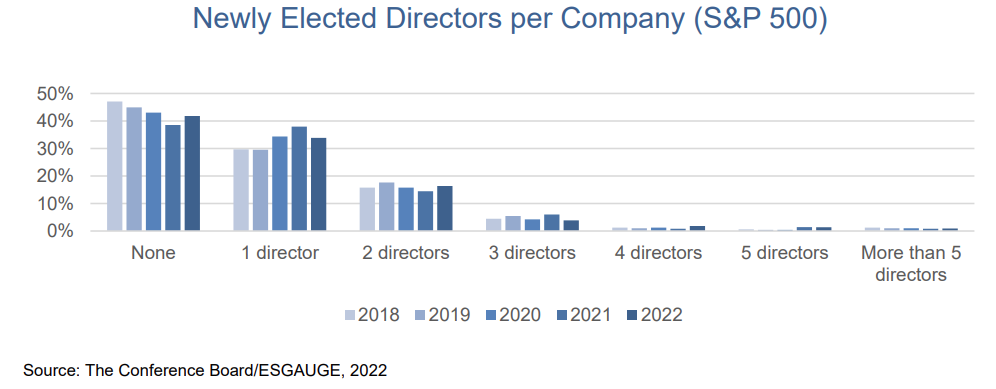

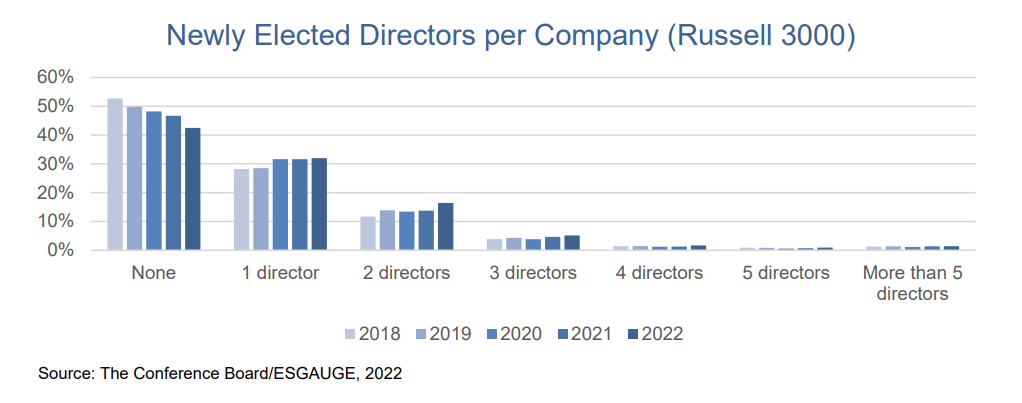

- While the aggregate rate of turnover has remained relatively flat, the percentage of companies adding at least one new director has grown in recent years—an increase that has been more pronounced at smaller companies. Both in the S&P 500 and the Russell 3000, 58 percent of companies added one or more new directors in 2022—an increase of 5 percentage points since 2018 in the S&P 500 and 11 percentage points in the Russell 3000.

Mandatory Retirement Based on Age

- The share of companies with a mandatory director retirement policy based on age is in decline. In the S&P 500, the share of companies with such a policy decreased from 70 percent in 2018 to 67 percent as of July 2022. The absence of a retirement policy based on age is even more pronounced in the Russell 3000, where only 36 percent of companies disclosed having such a policy as of July 2022 (compared to 40 percent in 2018). Moreover, existing retirement policies based on age are becoming less strict: the percentage of S&P 500 companies whose policy permits no exception declined from 41 percent in 2018 to 34 percent as of July 2022 (and from 24 to 18 percent in the Russell 3000).

- There is a direct relationship between company size and the adoption of the strictest type of retirement policy based on age, with larger companies more likely to have a policy that permits no exception and smaller companies more likely to have no policy at all. As of July 2022, a majority of companies (54 percent) with annual revenues of $50 billion and over disclosed a mandatory retirement policy based on age that permits no exception. [5] This percentage decreases gradually to only 3 percent for the smallest firms with annual revenues under $100 million. Conversely, 95 percent of the smallest firms disclosed no policy compared to 19 percent of the largest firms.

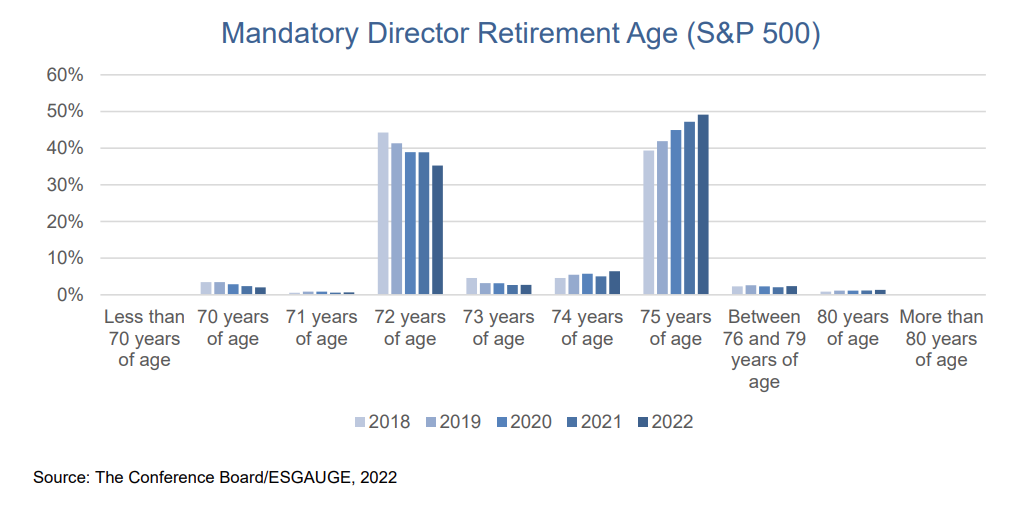

- The vast majority of companies with a mandatory retirement policy set the retirement age at either 72 or 75. While the share of companies that expect directors to resign at 72 is declining, the percentage that set the age at 75 is rising. As of July 2022, 84 percent of S&P companies and 81 percent of Russell 3000 firms with a retirement policy set the retirement age at either 72 or 75. But the share of S&P 500 companies with a retirement age of 72 decreased from 44 percent in 2018 to 35 percent as of July 2022, and the share with a retirement age of 75 rose commensurately from 39 to 49 percent in the same period. A similar pattern can be seen in the Russell 3000.

- Despite companies moving away from mandatory retirement policies based on age and the trend toward increasing the mandatory retirement age at companies that have such a policy, the average director age has not changed in recent years. It remained steady at 63 years in the S&P 500 and 62 years in the Russell 3000.

Mandatory Retirement Based on Tenure

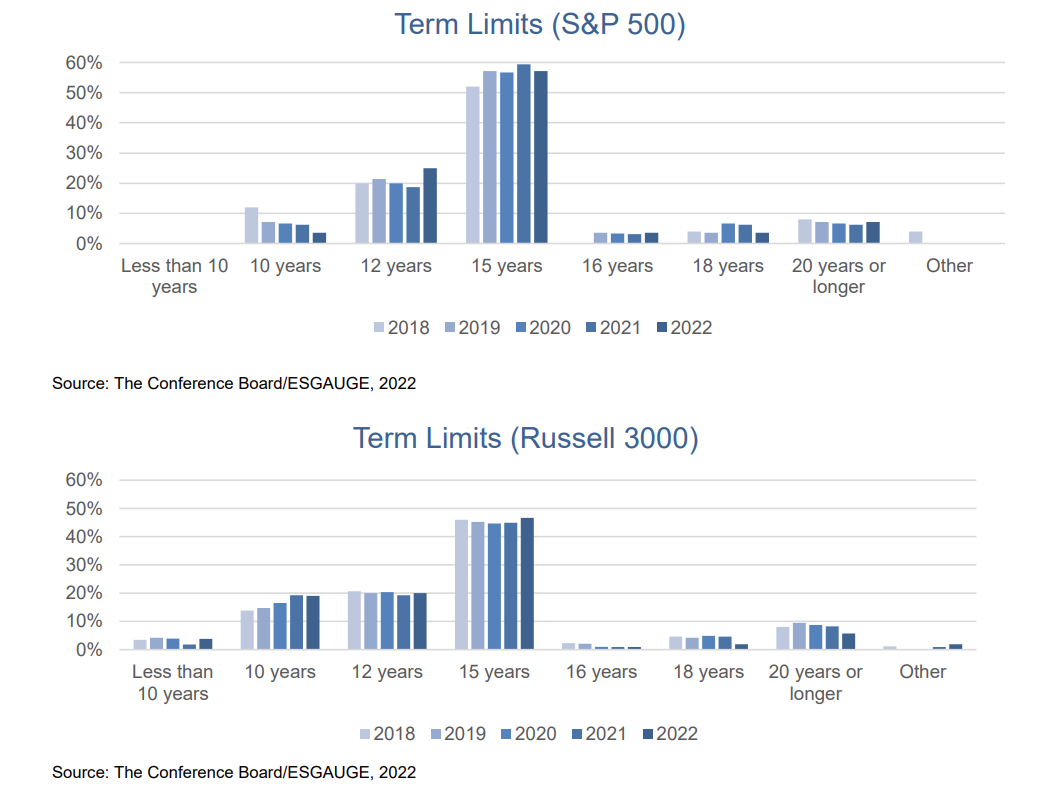

- Establishing term limits, or mandatory retirement policies based on tenure, continues to remain an uncommon practice as companies prefer to have the flexibility to retain valuable board members. Indeed, long-serving directors can be especially strong contributors to board discussions: directors whose service predates that of the CEO have particularly useful institutional memory and may be even more willing to challenge management because the current CEO was not involved in their selection as a board member. In both the S&P 500 and Russell 3000, the percentage of companies with a retirement policy based on tenure remained virtually unchanged, from 5 percent in 2018 to 6 percent as of July 2022 in the S&P 500, and from 3 to 4 percent in the Russell 3000.

- The largest firms are most likely to adopt director term limits; the smallest firms least likely. As of July 2022, 12 percent of the largest companies, with annual revenues of $50 billion and over, disclosed a policy that sets a maximum tenure. Conversely, only 1 percent of the smallest companies, with annual revenues under $100 million, have such a policy.

- The most prevalent term limit for companies that have a mandatory retirement policy based on tenure is 15 years, followed by 12 years. As of July 2022, 57 percent of S&P 500 companies with such a policy require board members to step down after 15 years of service, and 25 percent set the term limit at 12 years. By comparison, 47 percent of Russell 3000 companies set the term limit at 15 years and 20 percent at 12 years. Moreover, while the share of companies with a term limit of 10 years decreased considerably in the S&P 500 (from 12 percent in 2018 to 4 percent in 2022), it rose in the Russell 3000 (from 14 to 19 percent).

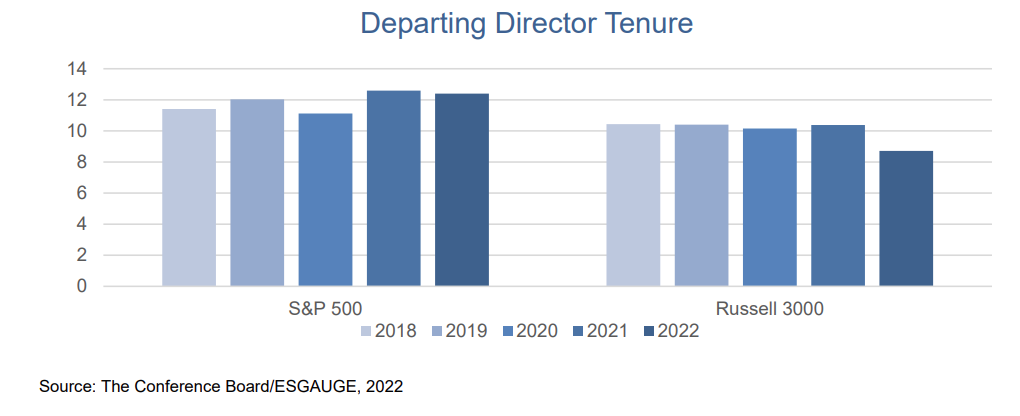

- In recent years, the average departing director tenure has increased slightly at larger companies and decreased at smaller companies. In the S&P 500, the average departing director tenure has fluctuated but overall rose from 11 years in 2018 to 12 years as of July 2022; it decreased from 10 to 9 years in the Russell 3000. This suggests that larger companies especially prefer to retain valuable board members, regardless of their tenure.

Director Overboarding

- Companies are increasingly limiting the number of other public company directorships their board members can hold—a result of growing investor concerns regarding director time commitments. In the S&P 500, the share of companies with an overboarding policy applicable to all directors grew from 64 percent in 2018 to 72 percent as of July 2022, and from 45 to 50 percent in the Russell 3000.

- There is a direct relationship between company size and the adoption of a director overboarding policy, with larger companies more likely to have a policy that applies to all directors, and smaller companies more likely to have no policy at all. As of July 2022, 73 percent of companies with annual revenues of $50 billion and over disclosed a director overboarding policy that applies to all directors. This share declines steadily to 20 percent for the smallest companies with annual revenues under $100 million. On the other hand, 68 percent of the smallest companies reported having no policy, versus 12 percent of the largest companies.

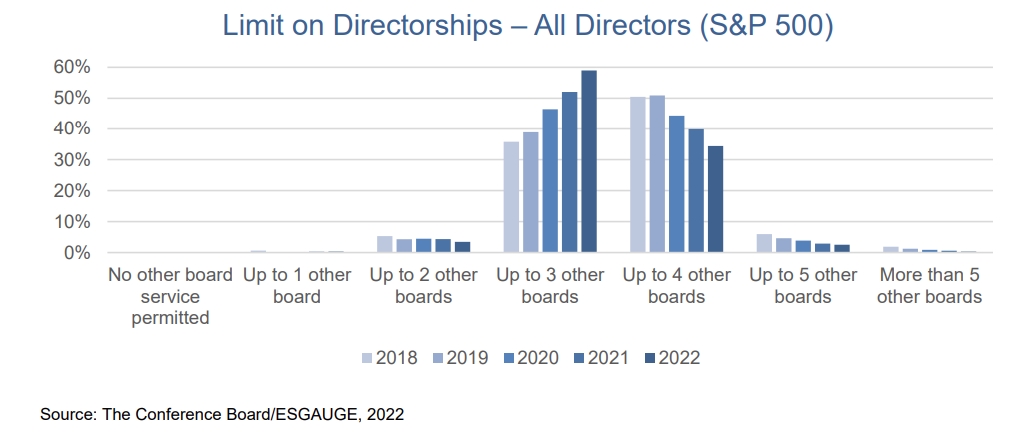

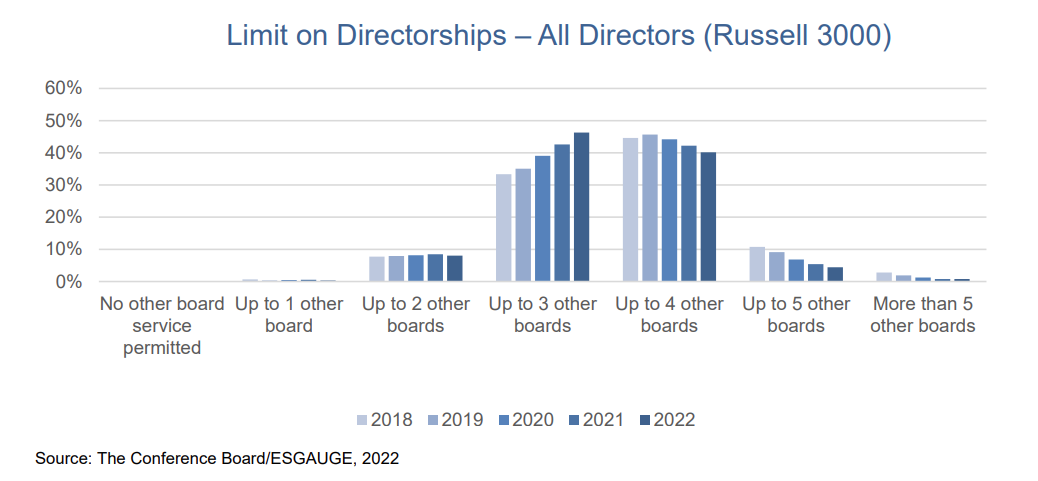

- When an overboarding policy for all directors exists, it most often sets a limit of three or four additional board seats. [6] As of July 2022, 59 percent of S&P 500 companies and 46 percent of Russell 3000 firms with an overboarding policy restricted additional board services to three seats, and 34 percent of S&P 500 and 40 percent of Russell 3000 companies set the limit at four. While the share of companies with a limit of three board seats rose in both indexes in recent years (by 23 percentage points since 2018 in the S&P 500 and 13 percentage points in the Russell 3000), it declined for a limit of four board seats (by 17 percentage points since 2018 in the S&P 500 and 5 percentage points in the Russell 3000).

- Although the number of directors that serve on more than one board has grown in recent years, most directors only sit on one additional board—and larger-company directors are more likely to serve on additional boards than their smaller-company counterparts. In the S&P 500, the share of directors who serve on at least one other board grew from 58 percent in 2018 to 66 percent as of July 2022, and from 42 to 48 percent in the Russell 3000. In both indexes, directors are most likely to hold one other board seat: 34 percent of S&P 500 and 26 percent of Russell 3000 directors. Additionally, 30 percent of S&P 500 and 21 percent of Russell 3000 directors sit on two or three additional boards. It is rare for directors to hold four or more board seats: only 1 percent of S&P 500 and 2 percent of Russell 3000 directors do so.

Board Evaluations

- Almost all companies disclose conducting some form of annual board evaluation (which, for NYSE companies, is mandated by listing standards)—and the combination of full board, committee, and individual director evaluations is growing in popularity. As of July 2022, 99 percent of S&P 500 and 97 percent of Russell 3000 companies disclosed carrying out board evaluations. In the S&P 500, conducting full board, committee, and individual director evaluations has become the most common practice (52 percent of companies reported this combination as of 2022 compared to 37 percent in 2018). [7] Indeed, in the S&P 500, the practice of conducting only board and committee evaluations has declined from 58 percent in 2018 to 46 percent as of 2022. Although the Russell 3000 has seen a similar pattern, with a rise in full board, committee, and individual evaluations (from 18 percent in 2018 to 34 percent as of July 2022), 60 percent of Russell 3000 companies continue to conduct only full board and committee evaluations.

- The practice of conducting full board, committee, and individual director evaluations increases with company size, rising from 27 percent for the smallest companies with annual revenues under $100 million to 52 percent for the largest firms with annual revenues of $50 billion and over. Full board and committee (without individual) evaluations, on the other hand, are most common among the smallest companies (65 percent versus 46 percent at the largest companies).

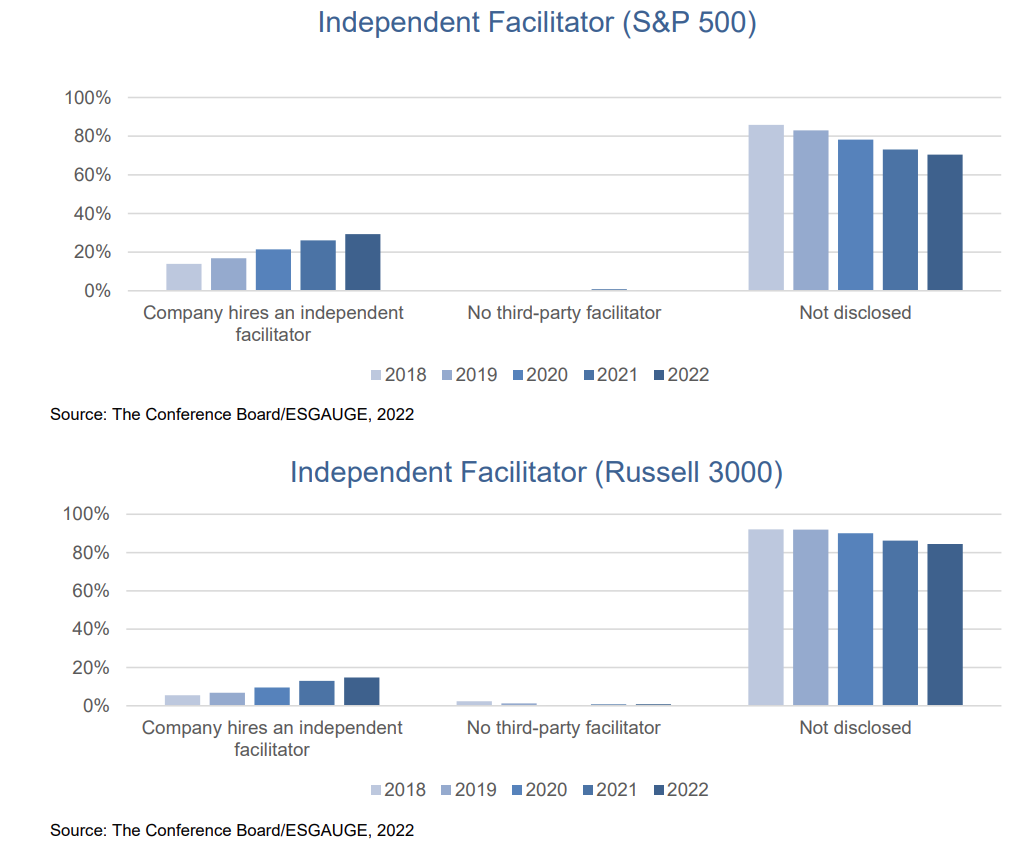

- Companies are increasingly disclosing their use of an independent facilitator for board evaluations—and larger companies are more likely to disclose hiring an independent facilitator than their smaller counterparts. As of July 2022, 29 percent of S&P 500 companies and 15 percent of Russell 3000 firms disclosed hiring an independent facilitator for board evaluations versus 14 percent of S&P 500 and 6 percent of Russell 3000 companies in 2018. In 2022, 42 percent of the largest companies, with annual revenues of $50 billion and over, disclosed their use of an independent facilitator, but only 5 percent of the smallest companies with annual revenues of under $100 million did so.

Conclusion

Companies have a variety of board refreshment tools at their disposal to increase diversity of backgrounds, skills, and professional experience on their boards. The tools that focus on triggering discussions of turnover or reinforcing a culture of board refreshment may be particularly valuable. These include overboarding policies, policies requiring directors to submit their resignation upon a change in their primary professional occupation, guidelines on average board tenure, individual director evaluations as part of the annual board self-evaluation process, and informal discussions that set an expectation that directors do not need to serve until they are required to leave, but rather should consider whether their contributions are still relevant to the needs of the company. Unlike policies that mandate turnover, such as term limits and retirement policies, these more flexible tools can lead to a more thoughtful process in proactively aligning board composition with the company’s strategic needs.

Endnotes

1Merel Spierings, Board Composition: Diversity, Experience, and Effectiveness, The Conference Board, May 2022.(go back)

2The Conference Board, in collaboration with ESG data analytics firm ESGAUGE, is keeping track of disclosures made by US public companies with respect to their board composition, director demographics, and governance practices. Our live, interactive online dashboard allows you to access and visualize practices and trends from 2016 to date by market index, business sector, and company size. The dashboard is organized in six parts: 1) board organization; 2) board leadership; 3) board composition; 4) new directors; 5) director election and removal; and 6) other board policies. While the data relied on for the conclusions presented in this post were pulled from the database on July 7, 2022, they reflect practices in place as of the most recent SEC filing or corporate documents relevant for each data point (including 2022 proxy statements, Forms 8-K and 10-K, committee charters, etc.).(go back)

3See BlackRock’s Proxy Voting Guidelines for US Securities; State Street Global Advisors’ Proxy Voting and Engagement Guidelines; and Vanguard’s Proxy Voting Policy for US Portfolio Companies.(go back)

4Throughout this post, the data for 2022 were pulled from our database on July 7 and include information for approximately 440 (or 88 percent of) S&P 500 companies and 2,600 (or 87 percent of) Russell 3000 companies.(go back)

5Company-size data in this post apply to manufacturing and nonfinancial services companies.(go back)

6In this context, “all directors” refers to independent, non-executive directors. More stringent limits generally apply to directors who are also a public company CEO or executive officer.(go back)

7There are different ways of assessing individual director performance, including through self-assessments, peer evaluations, and/or with the use of an independent facilitator.(go back)