Print

PrintHillary H. Holmes is partner and Justine Robinson is an associate at Gibson, Dunn & Crutcher LLP. This post is based on a Gibson Dunn memorandum by Ms. Holmes, Ms. Robinson, Tull Florey, Brian Lane, Jim Moloney, and Peter Wardle.

Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) by Lucian A. Bebchuk and Roberto Tallarita; For Whom Corporate Leaders Bargain (discussed on the Forum here) and Stakeholder Capitalism in the Time of COVID (discussed on the Forum here), both by Lucian Bebchuk, Kobi Kastiel, and Roberto Tallarita; and Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy—A Reply to Professor Rock (discussed on the Forum here) by Leo E. Strine, Jr.

Gibson Dunn has surveyed the comment letters submitted by public and private energy companies and related industry associations regarding the proposed rules by the Securities and Exchange Commission (the “SEC” or “Commission”) on climate change disclosure requirements for U.S. public companies and foreign private issuers (the “Proposed Rules”). [1]

Based on our review of these comment letters, we have seen general support for transparent and consistent climate-related disclosures, along with a concern that the Proposed Rules do not reconcile with the SEC’s stated objective “to advance the Commission’s mission to protect investors, maintain fair, orderly and efficient markets, and facilitate capital formation, not to address climate-related issues more generally.” [2] Overarching themes included (i) general support for the Commission’s decision to base the Proposed Rules on the Task Force on Climate-Related Financial Disclosures (“TCFD”) framework and Greenhouse Gas Protocol (“GHG Protocol”), (ii) concern with deviation from the long-standing materiality threshold, (iii) concern that the Proposed Rules would overload investors with immaterial, uncomparable, or unreliable data, and (iv) questions as to whether the Proposed Rules would cause an unintended chilling effect on companies to set internal emissions reduction targets or other climate-related goals to avoid additional liability risks in disclosing such goals. The proposed disclosure requirements receiving the most comments from energy industry companies relate to (i) the Greenhouse Gas (“GHG”) emissions reporting (particularly Scope 3 emissions) and (ii) the amendments to financial statement disclosure in Regulation S-X (particularly the 1% materiality threshold). In addition to these higher-level observations, this post also provides a more granular review of the energy industry’s comments on specific provisions of the Proposed Rules.

I. Background on the Proposed Rules

The proposed climate change reporting framework laid out in the 500+ page Proposed Rules is extensive and detailed, with disclosure requirements that are mostly prescriptive rather than principles-based. Rather than creating a new stand-alone reporting form, the Commission proposed amending Regulation S-K and Regulation S-X to create a climate change reporting framework within existing registration statements and reports under the Securities Act of 1933 (the “Securities Act”) and the Securities Exchange Act of 1934 (the “Exchange Act”).

The Proposed Rules would amend (i) Regulation S-K to require a new, separately captioned “Climate-Related Disclosure” section in applicable SEC filings, which would cover a range of climate-related information, and (ii) Regulation S-X to require certain climate-related financial statement metrics and related disclosures in a separate footnote to companies’ annual audited financial statements. While brief summaries of certain of the proposed disclosure requirements are provided in this post, for a more detailed description of the Proposed Rules, we encourage you to read our prior alert, “Summary of and Considerations Regarding the SEC’s Proposed Rules on Climate Change Disclosure (link),” and view our webcast, “Understanding the SEC Rule Proposal on Climate Change Disclosure (link).”

II. Comment Letter Highlights

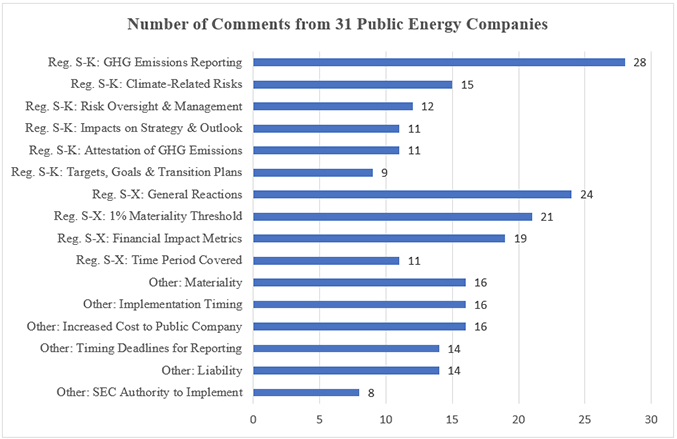

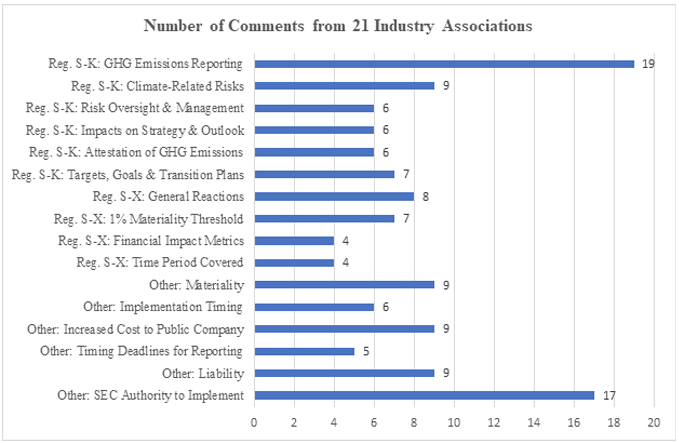

To contribute to our understanding of the general reaction of the energy industry to the Proposed Rules, we conducted a survey of what we believe are all comment letters submitted to the SEC through June 17, 2022 (the deadline for comment submissions) by public and private energy and energy services companies and related industry associations. Of the 62 comment letters we reviewed, 31 such comment letters were submitted by U.S. public reporting companies, 10 such comment letters were submitted by non-reporting companies, and the remaining 21 comment letters were submitted by industry associations. The following charts highlight the frequency of comments by the 31 public reporting companies and the 21 industry associations on a particular requirement in the Proposed Rules. The specific comments are described more fully in the sections following the chart. We note that not all comment letters addressed each particular requirement, and we did not assume that the absence of a comment on a proposed requirement by any company or association suggests approval of such proposed disclosure requirement.

III. Reactions to Proposed Reg. S-K Amendments

We summarize below the most frequent comments on the following proposed Reg. S-K disclosure requirements:

- GHG Emissions Reporting

- Climate-related risks

- Climate-related risk oversight & management

- Climate-related impacts on strategy, business model & outlook

- Attestation of GHG Emissions

- Targets, Goals & Transition Plans

A. GHG Emissions Reporting

Proposed Item 1504 of Reg. S-K would require companies to disclose Scope 1, Scope 2 and, in some cases, Scope 3 “GHG emissions … for [their] most recently completed fiscal year, and for the historical fiscal years included in [their] consolidated financial statements in the filing, to the extent such historical GHG emissions data is reasonably available.” The Commission based the GHG emissions disclosure requirements in the Proposed Rules on the GHG Protocol, which is a leading accounting and reporting standard for GHG emissions.

With respect to Scope 3 emissions, all reporting companies (other than smaller reporting companies) would be required to disclosure Scope 3 emissions, only if material or if the company has set a GHG emissions reduction target or goal that includes its Scope 3 emissions. The Proposed Rules presume that Scope 3 emissions are likely to be material for “oil and gas product manufacturers.”

The Proposed Rules include a limited safe harbor from liability for Scope 3 disclosures, providing that such disclosures will not be deemed fraudulent, “unless it is shown that such statement was made or reaffirmed without a reasonable basis or was disclosed other than in good faith.”

90% of public company letters and 90% of industry association letters commented on the GHG emissions reporting requirements, with particular focus on (i) the disclosure requirements in the Proposed Rule as compared to existing GHG emissions reporting requirements of the Environmental Protection Agency (“EPA”), (ii) the materiality of GHG emissions as defined, particularly with respect to Scope 3 emissions, and (iii) safe harbors for GHG emissions disclosure.

Sample Comments on GHG Emissions Reporting:

- “We . . . suggest that the SEC work with the EPA to ensure its standards for Scopes 1 and 2 GHG emissions are sound and consistent. The Proposal acknowledges that the EPA already requires, and makes available to the public, reporting of certain GHG emissions, and we believe the EPA is best positioned to regulate emissions reporting from a scientific standpoint.”

- “The SEC should not require GHG intensity disclosures for registrants that are not primarily involved in production activities, as such disclosures could lead to confusion and inaccurately suggest to investors that such data is comparable. Alternatively, the disclosure requirements should provide flexibility to account for differences in underlying business operations, including allowing midstream companies to report GHG intensity on a reasonable and supportable normalized basis of their choosing, or perhaps on a standardized basis developed and adopted by the industry over time (e.g., GHG intensity based on a ratio of emissions relative to throughput).”

- “[T]he Proposal would require registrants to report GHG emissions data for certain entities, such as joint ventures, over which they have no operational control. . . . For those [joint ventures] that we do not operate, there is a potential barrier for [us] to obtain required GHG data, as a joint venture partner may (i) not have the necessary information, (ii) be unwilling to provide it, or (iii) calculate it using methodologies or assumptions that conflict with those used by [us]. This will increase the liability for registrants if they are unable to obtain or cannot verify the accuracy of information that is not within their control. The SEC should allow registrants to report GHG emissions on an operated basis (vs. on an equity ownership basis), meaning the registrant would report emissions from assets operated by either the registrant or entities under its direct control.”

- “[T]here is an absence of materiality qualifiers applicable to the disclosure of Scope 1 and Scope 2 GHG emissions and, for Scope 3 GHG emissions, the materiality qualifier is ill-defined and somewhat esoteric. Gross emissions data should not be overemphasized, and the [EPA’s Greenhouse Gas Reporting Program (“GHGRP”)] and [California’s Regulation for the Mandatory Reporting of Greenhouse Gas Emissions (“MRR”)] have well-defined and understood reporting thresholds. . . . [R]egistrants who are subject to the GHGRP or MRR [should be allowed] to report GHG emissions in their SEC filings in a manner consistent with those programs.”

- “Adopting standards that correspond to the GHG Protocol would provide investors with comparable disclosures to those which companies have made historically and to those made by companies not subject to the Commission’s reporting requirements. However, the standards in the Rule Proposal differ significantly from those in the GHG Protocol. For example, the Rule Proposal requires companies to set organizational boundaries for GHG emissions disclosure using the same scope of entities and holdings as those included in their consolidated financial statements. Conversely, the GHG Protocol allows for an equity share or control boundary. This difference in boundaries could lead to companies reporting significantly different emissions than they have historically. Deviating from the GHG Protocol would only serve to confuse investors with differences from companies’ previous GHG emissions disclosure and unnecessarily increase compliance costs as companies would need to recalculate their emissions disclosure both historically and going forward. We urge the Commission to revise the emission standards in the Rule Proposal to match those of the GHG Protocol.”

Sample Comments on Scope 3 Emissions:

- “[T]he materiality of Scope 3 emissions must be evaluated on a case-by-case, registrant-by-registrant basis and does not lend itself to across-the-board presumptions of materiality, such as the Proposal implies for ‘oil and gas product manufacturers’. As a strictly exploration and production company, we are not ‘product manufacturers’ but this vague definition creates more uncertainty and underscores the need for Scope 3 materiality to be assessed at a specific registrant level, not by prescriptive assertions within proposed rulemaking.”

- “While midstream companies . . . are not generally oil and gas manufacturers, we are concerned with the risk that this presumption creates. . . . In addition, there is currently no standard or guidance for the midstream sector to define, measure or report on Scope 3 emissions. If pipeline companies are required to report emissions attributable to upstream, downstream and end-use activities that are not within our control and are highly uncertain and unreliable, this would result in significant double or multiple counting of emissions across companies.”

- “[R]equiring Scope 3 reporting, which includes all ‘upstream’ and ‘downstream’ emissions, . . . would be incredibly cost prohibitive, even with delayed compliance and ‘good faith’ safe harbor protections, and would limit innovation from companies in our supplier base. . . . Because [we have] thousands of vendors and customers, the variability in terms of their use of different methodologies, assumptions and speculation is self-evident. It would be difficult for us to attest even that the information was made on a ‘reasonable’ basis, since we will not be able to obtain sufficient access to the information required to generate Scope 3 emissions reports.”

- “Scope 3 disclosure—upstream and downstream—will remain a challenge for many companies during the next few years, until clear methodologies and estimation tools are put in place for each of the 15 categories defined by the GHG Protocol. Providing accurate and faithful estimates will be subject to a large magnitude of uncertainty. [The company] therefore suggests to allow Scope 3 disclosure with a 5 to 10% uncertainty range.”

- “Scope 3 emissions methodology double-counts emissions overall, since ‘the scope 3 emissions for one organization are the scope 1 and 2 emissions of another organization.’ Reporting across all 15 categories of Scope 3 emissions will also count the same emissions multiple times by the same party or by different parties in the value chain from initial production to ultimate sale and use of a product. . . . [T]he Proposal as currently written will likely end up enshrining the current, flawed approach as a feature of regulation, with advancement in reporting methodologies contingent on future SEC rulemaking.”

Sample Comments on Safe Harbors for GHG Emissions:

- “At a minimum, the Proposed Rule should include Scope 1 and Scope 2 reporting (the latter of which registrants will necessarily need to rely on other entities to provide), as well as any discussion of scenario analysis, within the safe harbor presently proposed for Scope 3 GHG emissions.”

- “Considering the nascent nature of the GHG reporting contemplated by the Proposal compared to traditional SEC reporting requirements, [the company] urges the Commission to provide stronger safe harbor protection from liability for all scopes of GHG emissions disclosures.”

- “[W]hile we support the disclosure of Scopes 1 and 2 GHG emissions, to the extent the SEC concludes this information should be included in SEC reports, the data should be furnished, not filed, because these metrics are subject to a significant degree of technical estimation and numerous assumptions.”

B. Climate-Related Risks

Proposed Item 1502 of Reg. S-K would require companies to describe “climate-related risks reasonably likely to have a material impact on the registrant, including on its business or consolidated financial statements, which may manifest over the short, medium, and long term.” Based on the definition of “climate-related risks” in the Proposed Rules, companies would need to consider not only the direct impact of climate change on their financial statements and business, but also the indirect impacts on their “value chains.” These “climate-related risks” would be categorized as either a “physical risk” (i.e., related to physical impacts of climate change) or “transition risk” (i.e., related to the transition to a lower-carbon economy).

48% of public company letters and 43% of industry association letters expressed concern about the climate-related risk disclosure requirements, with particular focus on the definitions of “physical risk” and “transition risk,” the assessment of risks over longer time horizons, and the practicality of assessing risks for a registrant’s value chain.

Sample Comments:

- “Risks, to the extent they are material, are currently disclosed in the Risk Factors section of our periodic reports and registration statements filed with the Commission. We believe certain aspects of the Proposal’s climate-related risk disclosures that require prospective disclosures will create compliance challenges and lead to volumes of information immaterial to investors. For example, the requirement to disclose risks over the near-, medium- and long-term presents a particularly tricky challenge given the complexity of modeling scenarios and making materiality determinations over extended periods of time, and such assessments may only serve to obscure material near-term risks.”

- “Assessing risk of a registrant’s value chain . . . . is especially onerous for a midstream infrastructure company . . . who provides federally regulated transportation services for shippers without necessarily knowing where the product being shipped originated or where it will go or how it will be used once it leaves the pipeline. Even if [a midstream infrastructure company] could reliably identify companies in its value chain and the myriad of climate-related risks they may face, [such company] does not possess special inside information that would allow it to assess the climate-related risk of its value chain for purposes of assessing materiality.”

- “[The] expansive definition of climate-related risks including the impacts on our value chains will require us to expend significant resources to assess and measure potential exposure from an endless list of parties outside of our own operations over which we have no control.”

- “We request that the Commission remove the requirement to assess physical risks related to the entities with which a registrant does business, apply a materiality threshold to the assessment of direct physical risks, and provide additional clarification on the definitions of physical climate risks (g., ‘water stress,’ ‘wildfire prone,’) on issues such as frequency and severity to ensure the scope of the analysis required under the Proposed Rule is clear. To the extent that the Commission determines that separate disclosures on physical risks as applied to a registrant’s supply chain will be required, it should create a new definition for ‘supply chain risks.’ Disclosures made pursuant to this new definition should then be limited to the extent that such risks are material and identifiable and should be clarified so as not to require registrants to incur costs associated with collecting data from third parties if the information is not readily available.”

- “[I]f the Proposed Rules are passed in their current form, it would be the first time that the Commission has required risk disclosures to be specified over prescribed time frames; this would be a significant departure from past practice. . . . The Proposed Rules do not provide a specific range of years to define short-, medium- and long-term time horizons. Instead, the Commission provides flexibility for registrants to select the time horizons and to describe how they define them. As such, the time horizons selected will vary widely across companies, resulting in information that is not comparable or consistent for investors.”

- “The detail required in this proposed disclosure—including, for example, requirements for disclosure of specific locations of properties at physical risk (with location defined as a ZIP code or other similar postal code)—would result in disclosure of extensive information that we do not believe would be decision-useful to investor. At the same time, this level of detail could result in unintended negative consequences, including security concerns, competitive harm and conflicts with contractual obligations for a company.”

C. Climate-Related Risk Oversight & Management

Proposed Item 1501 of Reg. S-K would require companies to describe “the [board’s] oversight of climate-related risks” and “management’s role in assessing and managing climate-related risks.” With respect to the board’s role, disclosure would be required as to whether any directors have “expertise in climate-related risks.” In addition, proposed Item 1503 of Reg S-K would require companies to describe, if applicable, “any process the registrant has for identifying, assessing, and managing climate-related risks.”

39% of public company letters and 29% of industry association letters commented on board and management oversight of climate-related risks, with particular focus on the requirement for a “climate expert” on the board, such board member’s liability as a “climate expert” and the impact such requirement would have on the director selection process.

Sample Comments:

- “Elevating particular facets of candidate experience above others, by compelling specific disclosure on those topics, creates a value-laden one-size-fits-all disclosure framework that ignores these important differences between companies and their board needs. Over the long term, this will likely impede the ability of boards and their nominating/governance committees to exercise appropriate judgment in candidate selection based on what they view as the most critical attributes needed for their particular businesses (versus feeling compelled to check certain boxes specified by the Commission).”

- “While the disclosure requirements around board and management climate-related expertise and decision-making are dressed up as mere disclosure requirements, the aim and practical effect are clear: By requiring extensive annual disclosures on one particular topic, the Commission is necessarily highlighting it above other issues relevant to good governance and effective operations and ensuring that all public companies will pay particular attention to climate-related issues.”

- “[T]here is little incentive for an individual to join a board of directors as a designated expert if there is potential for increased liability, including liability under Section 11 of the Securities Act. While we would urge the Commission to delete this disclosure requirement, if nonetheless adopted, the Proposed Rule should provide a safe harbor clarifying that such an expert designation would not impose any duties, obligations, or liability that is greater than the duties, obligations, and liability imposed on such person as a member of the board of directors in the absence of such designation or identification, similar to the safe harbor proposed in the Commission’s cybersecurity proposal.”

- “We have serious concerns that the Proposed Rule will remove or impair the company’s flexibility to select (or maintain) the right board members for the job, potentially elevating climate-related expertise over other business considerations in order to comply with the Proposed Rule. The board of a company is responsible for overseeing all aspects of the business, and the Proposed Rule—focused on climate as it is—ensures the overemphasis on one particular aspect of operations, thereby skewing the focus of boards.”

- “We do not believe that an in-depth discussion on climate-related expertise is necessary for investors to be able to understand how the board manages oversight of climate-related risks. However, to the extent that the Commission would require disclosure of such information, we recommend that the proxy disclosure rules be revised to require disclosure about any climate-related experience or expertise of board members.”

- “The Commission should provide additional guidance as to whether a director’s expertise in climate-related risks can be demonstrated through Board education or whether such expertise must be demonstrated by prior professional experience, as it does with respect to the Audit Committee Financial Expert designation.”

D. Climate-Related Impacts on Strategy, Business Model & Outlook

Proposed Item 1502 of Reg. S-K would also require companies to describe “the actual and potential impacts of any [identified] climate-related risks … on the registrant’s strategy, business model, and outlook.” Pursuant to this requirement, companies that use scenario analysis would be required to disclose the specific scenarios considered along with parameters, assumptions, analytical choices and projected financial impacts under each scenario. In addition, for companies that have set an internal price on carbon (i.e., an estimate of the cost of carbon emissions for planning purposes), the proposed rules would require detailed disclosure on such carbon pricing.

35% of public company letters and 29% of industry association letters commented on the disclosure requirements for climate-related strategies, business models and outlooks, with particular focus on the unique and competitive nature of a registrant’s climate strategy, as well as the fact that scenario analyses are based on assumptions and forecasts that may change over time.

Sample Comments:

- “Certain disclosures required under the Proposal such as internal carbon price and scenario analyses constitute competitive differentiators, the disclosure of which could cause competitive harm. Effective scenario analysis requires business plans and forecasts to assess the company’s exposure to climate-related risks and plan for transition scenarios. Disclosing this information would divulge sensitive information to the public and competitors. We therefore request the Commission consider providing additional safeguards or exclusions for information that a company deems to be competitively sensitive.”

- “Unless the SEC provides a detailed framework mandating specific scenarios and a common set of assumptions, this disclosure will inevitably result in a lack of comparability between issuers. Furthermore, it is important to note that these exercises utilize “scenarios,” which reflect potential outcomes over the long term, but these scenarios are not forecasts, and no representation is being made as to the accuracy of the underlying assumptions or the likelihood or occurrence. Including this information in financial reports as required under the Proposed Rule may afford them an undue sense of accuracy.”

- “While scenario analysis is a helpful tool, required disclosure of each scenario that a company simulates could result in the disclosure of commercially and strategically sensitive information, to the detriment of that company and its investors, which could penalize and disincentivize companies from taking prudent steps to manage risk through robust and varied scenario analyses. Moreover, disclosure of each scenario that a company simulates could result in disclosure of significant amounts of immaterial information that may only be of interest to competitors, not investors. Furthermore, because a company simulates a range of scenarios that could include those that management believes would have a remote likelihood of occurring, the Commission should not mandate disclosure of all scenario analyses, including input parameters, that a company performs.”

- “We believe that the Commission should specify that a registrant is not required to disclose internal carbon prices in any circumstances.”

- “We believe that registrants should be required to disclose information about an internal carbon price. Indeed, an internal carbon price is a multifaceted tool that can support companies in assessing climate-related risks and opportunities in the transition to a low-carbon economy. . . . However, there are different approaches both in the definition and application of an internal carbon price. . . . For this reason, we recommend not to mandate a particular carbon pricing methodology.”

E. Attestation of GHG Emissions

Proposed Item 1505 of Reg. S-K would require large accelerated filers and accelerated filers to obtain an attestation report from a GHG emissions attestation provider covering disclosure of Scope 1 and Scope 2 emissions.

35% of public company letters and 29% of industry association letters commented on the attestation requirement for Scope 1 and Scope 2 emissions, with particular focus on the expense and lack of availability of assurance providers.

Sample Comments:

- “The attestation requirements will further add to the complexity and cost of compliance. The assurance obligation significantly adds to the time burden by effectively requiring the work to be ‘done again’ (even if just by reviewing the original work) in order for a third-party to provide such assurance. This would be difficult enough for limited assurance, but could become nearly impossible when looking for reasonable assurance. Given the rapidly evolving nature of emissions monitoring and climate data analysis, the methodologies for analyzing this information is still in relatively frequent flux, and achieving reasonable assurance on the time frame in the Proposed Rules may well be impossible; and, if not impossible, prohibitively costly.”

- “One challenge that we potentially see with assurance requirements specifically could be availability and cost-effectiveness of qualified independent resources to perform limited reasonable assurance reviews on an annual basis. The supply of available, qualified auditors will be especially limited early on, and the high demand could mean companies are unable to secure and/or afford these resources until further development in this field takes place, which could take several years.”

- “[T]he SEC should phase in attestation requirements to allow for a sufficient market of GHG attestation provides to develop, and once phased in, require only limited assurance attestation.”

- “The Commission must provide clear guidelines for the accounting and attestation of emissions before reporting companies can be expected to provide results that are verifiable under attestation standards. Current guidelines, including those in the GHG Protocol and GRI, allow degrees of flexibility in interpretations that would be difficult to audit for lack of clear subject matter criteria. . . . The Commission has identified this flexibility as a concern in the Proposed Rule, but we do not believe that it has provided sufficient information to resolve these concerns.”

F. Targets, Goals & Transition Plans

Proposed Item 1506 of Reg. S-K would require detailed disclosures if a company has “set any targets or goals related to the reduction of GHG emissions, or any other climate-related target or goal (e.g., regarding energy usage, water usage, conservation or ecosystem restoration, or revenues from low-carbon products) such as actual or anticipated regulatory requirements, market constraints, or other goals established by a climate-related treaty, law, regulation, policy, or organization.” In addition, registrants would be required to disclose any use of carbon offsets or Renewable Energy Credits (RECs).

29% of public company letters and 33% of industry association letters commented on the disclosure requirements related to climate-related targets, goals and transition plans, with particular focus on the comparability of such disclosure across registrants and the chilling effect such disclosure may have on a registrant’s implementing goals or transition plans.

Sample Comments:

- “A registrant should control the timing and extent to which it communicates with investors and other stakeholders about any ‘transition plan’ that it may have adopted. The Proposed Rule may compel companies to disclose potentially sensitive and competitive information earlier than is appropriate. . . . Requiring this disclosure also will likely to have a chilling effect on the progress of goals and sustainability initiatives at companies that are at the early stages of addressing the transition to a low carbon economy.”

- “There are no standard methodologies for developing climate-related goals and targets, transition plans, or internal carbon prices. Accordingly, this information would not be comparable across companies and would not be decision-useful to investors.”

- “We . . . believe registrants should disclose plans and progress toward meeting material short-term targets and goals only, (i.e., those set within the next five (5) years) where it is possible to make definitive plans. . . . Plans and progress toward meeting long-term targets and goals are inherently less certain and are very likely to evolve over time as circumstances and technologies improve, and we have a number of options to meet these objectives, but have not yet committed to one path. Therefore, we believe that detailed disclosures on medium- and long-term goals and targets would not be material to investors and could potentially be misleading.”

- “The Proposal’s requirement to provide detailed disclosures applicable to all climate-related targets and goals that a company has set may have the unintended consequence of significantly limiting a company’s willingness to set new internal and external targets and goals to advance its environmental performance. . . . An alternative that could further the SEC’s goals and not result in these potential negative consequences would be to limit the disclosure requirements related to targets and goals to a company’s material climate-related targets and goals.”

- “[T]he Proposal’s requirement for detailed disclosure regarding a company’s use of carbon offsets would result in public disclosure of commercially sensitive, yet likely immaterial information, such as highly negotiated prices associated with different offset-generating projects. To promote comparability of useful information, an alternative to the current provision in the Proposal could require, to the extent material, disclosure of carbon offsets and renewable energy credits inventory volume and annual retirement volume at a summarized level in the same disclosure as GHG emissions and for the same time period. This summarized version of the information would effectively convey comparable information while avoiding competitive harm concerns.”

IV. Reactions to Proposed Reg. S-X Amendments

The Proposed Rules would amend Reg. S-X to require certain climate-related financial information (specifically, financial impact metrics, expenditure/cost metrics and financial estimates and assumptions) and related disclosures in a separate footnote to companies’ annual audited financial statements.

77% of public company letters and 38% of industry association letters commented on the proposed amendments to Reg. S-X, with particular focus on the 1% materiality threshold and the proposed definitions around the required financial metrics. Several commenters requested the Commission forego the amendments to Reg. S-X in their entirety.

Sample Comments:

- “[The company] requests that the Commission withdraw its proposed amendments to Regulation S-X. Alternatively, [the company] requests that the Commission bifurcate its rulemaking, deferring the proposed amendments to Regulation S-X until it is better positioned to issue a supplemental notice of proposed rulemaking that provides improved guideposts for assessing potential climate-related financial impacts.”

- “At the outset, the premise that climate-related disclosures should be linked to the parameters of a company’s consolidated financial statements is unprecedented and conflicts with existing emissions reporting regimes used by [the company] and others in [the] industry. . . . [I]mposing disclosure requirements that partially overlap others already in place adds to the burdens on companies in preparing required information. At a minimum, registrants should have the flexibility to determine the appropriate parameters for evaluating climate-related information in preparing any required disclosure in order to conform with that company’s operations and other reporting obligations. This would better promote the Commission’s goal of generating reliable disclosure by companies.”

- “[W]e believe the inclusion of information about climate events and transition plans through a principles-based framework focused on information most material to investors would align with the recently adopted amendments to modernize, simplify, and enhance certain financial disclosure requirements in Regulation S-K. We recommend that relevant financial impact metrics be included in the Form 10-K in some combination of Item 1 Business, Item 7 MD&A and/or the proposed Item 6 Climate-Related Disclosure under the provisions of Regulation S-K rather than within Item 8 Financial Statements under the provisions of Regulation S-X.”

We summarize below the most frequent comments on the following proposed Reg. S-X amendments:

- Materiality threshold of 1%

- Financial impact and expenditure/cost metrics; financial estimates and assumptions

- Time period covered

A. Materiality Threshold of 1%

The financial metrics under proposed Rules 14-01 and 14-02 of Reg. S-X would require quantified disclosure if the absolute value of all climate-related impacts or expenditures/costs, as applicable, with respect to a corresponding financial statement line item represents at least 1% of that line item.

68% of public company letters and 33% of industry association letters commented on the 1% materiality threshold for the proposed financial metrics, with particular focus on how such a low threshold would likely result in great cost to the registrant and an overload of immaterial information to investors.

Sample Comments:

- “One percent has never been, and is not, an appropriate threshold when quantitatively evaluating materiality for a financial statement line item; additionally, any individual line item may not be material for a given company. Applying a one percent threshold to every financial statement line item would require companies to collect data at a threshold much lower than one percent to demonstrate completeness and evaluate whether the threshold is met. This exercise would lead to excessive costs in collecting a substantial amount of data that is immaterial to investors. Furthermore, there is no other financial statement disclosure requirement under Regulation S-X that requires any similar disclosure for any other specific type of risk.”

- “The 1% threshold is . . . significantly below the ‘initial step’/rule of thumb of 5% used by some registrants/auditors in assessing materiality. While the SEC Staff openly acknowledges that a purely quantitative threshold is not conclusive, setting the threshold at 1% is very low by any normative standard and by the SEC’s own logic in Staff Accounting Bulletin: No. 99 (‘SAB No. 99’), and not dispositive for purposes of a registrant’s materiality determination.”

- “The 1% line-item threshold applicable to the impacts of severe weather or climate transition plan efforts (together, “climate-related impacts”) would not provide investors with consistently decision-useful information. . . . [W]hile materiality includes both qualitative and quantitative assessments, we believe it would be unusual for a climate-related impact to be qualitatively material yet have a quantitative value comprising just 1% of a line item. Indeed, this is even more likely to be the case since the 1% threshold is to be met by aggregating the absolute values of individual climate-related impacts. As a result, this footnote disclosure is unlikely to inform a reasonable shareholder’s investment or voting decision, and would only serve to increase compliance costs.”

- “Public companies will need to conduct extensive and costly assessments of potential impacts to determine if they trigger the reporting threshold and revise controls on their financial reporting systems to account for the unprecedented 1% reporting threshold. Thus, notwithstanding if a registrant has to disclose such information, it will still need to engage in data calculation and subsequent calculations to determine whether it falls below the threshold for materiality.”

- “[T]he materiality threshold of 1% of an individual line item is significantly lower than other thresholds in Regulation S-X implying that this information is more sensitive than any other measure of financial performance in the financial statements. Since the amount in which to apply this threshold is based on an aggregate number on an absolute basis, processes and controls will need to be in place to capture all transactions to have a complete population to analyze for disclosure, creating a significant burden to preparers.”

B. Financial Impact and Expenditure/Cost Metrics; Financial Estimates & Assumptions

The proposed amendments to Regulation S-X would require companies to disclose, subject to the 1% line-item threshold, (i) the financial impacts of severe weather events, other natural conditions and transition activities on any relevant line items in the company’s financial statements, and (ii) expenditures and capitalized costs to mitigate the risks of severe weather events or other natural conditions and expenditures related to transition activities. In addition, companies would be required to disclose whether estimates and assumptions underlying the amounts reported in the financial statements were impacted by risks and uncertainties associated with, or known impacts from, severe weather events and other natural conditions, the transition to a lower-carbon economy or any disclosed climate-related targets.

61% of public company letters and 19% of industry association letters commented on the disclosure requirements for financial metrics, estimates and assumptions, with particular focus on the definitions of “severe weather events” and “transition activities” and the difficulty in breaking out financial impacts and expenditures from standard business operations.

Sample Comments:

- “With respect to our business, one of the largest event-driven impacts to our financial statements is from the movement in commodity prices, which are directly and indirectly impacted in any given period by a multitude of supply, demand and other factors. Thus, it is impossible for us to measure and determine the impact of a single climate or weather-related event on our revenues and certain other financial statement line items or on commodity prices, nor can we bifurcate the impact of macroeconomic events from climate change events. This would be impractical to measure and report even if the Commission were to raise the threshold for reporting from one percent to a higher percentage threshold.”

- “Quantifying and providing the proposed financial impact metrics when the impact is the result of a mixture of factors, including events unrelated to climate, may be impractical. In such situations, we believe the Commission should permit a registrant to disclose that it was unable to make the required determination. Moreover, it would be helpful if the Commission could provide examples to illustrate impracticability.”

- “[T]he metrics proposed would provide no detail as to the underlying cause for the negative or positive impact from climate-related events or transition activities. The amount disclosed for each line item could be comprised of a number of smaller events that aggregate to an amount requiring disclosure under the Proposed Rules and would not identify which climate-related risks may have driven the amounts disclosed.”

- “In particular, we request additional specificity in regards to how, in preparing the proposed climate-related financial statement metrics, registrants should determine the financial impact of transition activities or climate-related physical risks and expenditures related to transition activities and the mitigation of physical risks. As currently drafted, for example, the proposed rules are unclear on how companies should distinguish climate-related impacts and expenditures from those that are part of normal business operations in order to apply the one percent threshold for disclosure.”

- “Attempting to assess the financial impact of energy transition risk will require companies to translate predictions about the actions of regulatory bodies, new technologies, changes in market behavior, and a host of other variables, into financial consequences, which, due to the fact that there is no standardized method for making such determinations, means that consistent, comparable, and reliable disclosure is unlikely to be achieved.”

C. Time Period Covered

Proposed Rule 14-01 of Reg. S-X would require the financial statement disclosures discussed above to be provided for a company’s most recently completed fiscal year and for each historical fiscal year included in the financial statements in the applicable filing.

35% of public company letters and 19% of industry association letters commented on the applicable time period for financial statement disclosures, with particular focus on the requirement to provide disclosure for historical periods prior to implementation of any final rule.

Sample Comments:

- “The Proposed Rule represents a significant sea change in financial reporting practices, and new processes and controls will have to be put in place to assess and identify relevant data. This will be a daunting task in and of itself, but being required to retroactively apply this requirement to historical financial data with the degree of accuracy that investors expect with respect to financial reporting is unfeasible.”

- “Under the Rule Proposal, large accelerated and accelerated filers with calendar year-ends would be required to file the assured GHG emissions metrics by March 1 and March 16, respectively. Under the EPA Rule, those same companies are required to submit unverified metrics by March 31. While we expect that the Rule Proposal’s deadline would be difficult for companies that do not report GHG emissions, even companies that have adopted GHG emissions reporting practices meant to comply with the EPA Rule would incur significant costs to adapt their controls and procedures to meet the Form 10-K reporting deadline. . . . Given the significant burden of completing the GHG emissions reporting and assurance processes within the proposed time frame, the likelihood that disclosures would be undermined by the need to further rely on assumptions and estimates in order to meet such time frame, and the significant cost savings that could be realized with a deadline that occurs after the publication of GHG emissions reports under the EPA Rule, we recommend that the Commission extend the deadline for GHG emissions disclosure.”

- “The required historical information will be difficult to obtain for periods prior to the current period when the Proposed Rules first take effect. . . . With the aim to reduce compliance burden, we would welcome a provision that permits the presentation of climate-related financial statement metrics only for the most recently completed fiscal year when the Proposed Rules first take effect and for subsequent years.”

- “The proposed rules should not require the retrospective disclosure of historic climate-related information, which would introduce data inherently exposed to a greater risk of inaccuracy and difficulty to assure given, in particular, that registrants would have had no opportunity to implement the systems and processes to collect the required data for those prior years.”

- “Compliance with the disclosure timeline contemplated by the Proposed Rule would be extremely onerous for [the association’s] members and other registrants, as it would require the assembly of data for calendar year 2021, which has already passed. For some registrants, systems needed to track the information required under the Proposed Rule were not in place to track all the required info at the time the Proposed Rule was issued, and attempting to retroactively determine that data will be extremely burdensome, if not impossible. For example, without a system to track fuel usage for fleet vehicles, going back and compiling that historical information with any reasonable degree of accuracy would not be possible.”

V. Other Significant Reactions to the Proposed Rules

A. Materiality

Very few items in the Proposed Rules are predicated on materiality. Other than in the context of Form 10-Q updating, only the climate change risk disclosures, the Scope 3 emissions disclosure requirement (i.e., disclosure required either if material or if included in a GHG emissions reduction target or goal), and certain details regarding emissions disclosures are predicated on materiality (and in the case of risk disclosures, the standard is “reasonably likely” to have a material impact).

52% of public company letters and 43% of industry association letters commented in some way that the Proposed Rules deviated from the long-standing, judicially accepted understanding of “materiality” under the federal securities laws.

Sample Comments:

- “The Proposed Rules depart from the general, long-standing materiality constraint on required disclosures. While the Commission has previously mandated certain disclosures irrespective of a materiality threshold, that is the exception. The general guidepost for disclosures in federal securities law has been information that a reasonable investor would consider important in deciding how to vote or make an investment decision. However, the Proposed Rules eschew a materiality standard in some areas and apply a modified version in others.”

- “We believe that climate-related risks should be disclosed based on the materiality standard that has been used by the Commission for many years and which is consistent with well-established and time-tested Supreme Court precedents. . . . This definition of materiality is foundational to the function of U.S. capital markets. Other frameworks for ESG disclosure have competing and non-aligned definitions of materiality when compared to the SEC’s well-established precedent . . . and we believe disclosures effectively requiring a different materiality framework are likely to create confusion and uncertainty for investors and registrants alike.”

- “[The company] believes it is critical for the Commission to maintain the time-tested materiality standard that serves as the cornerstone of the securities disclosure system: information is material if there is a substantial likelihood that a reasonable investor would consider it important or significant in deciding whether to buy or sell a security. . . . The fact that climate-related information is valuable or interesting to many stakeholders does not make it material. We believe that companies are best positioned to determine materiality standards for disclosure of climate-related information, in light of their specific business circumstances, and to engage with their investors to determine what information is most useful to them.”

- “The proposed rules, if adopted, would effectively compel all boards and management of public companies (but only of public companies) to subordinate their judgment of materiality to the SEC’s and treat essentially any and all climate-related matters, including any amount of Scope I and Scope II emissions, as material, regardless of whether there is a substantial likelihood that a reasonable shareholder would consider it important.”

- “The Proposed Rule substantially deviates from the longstanding conception of materiality under the federal securities laws which is supported by related case law. For decades, the existing concept of materiality has advanced the best interests of investors, encouraged capital formation, and helped ensure the integrity of our capital markets. In contrast, the Proposed Rule calls for the disclosure of granular climate-related information that is often immaterial under the standard of materiality that the United States Supreme Court handed down decades ago.”

B. Implementation Timing

The Proposed Rules provide for a phase-in implementation schedule, assuming that final rules are adopted and effective by the end of 2022. Large accelerated filers would be required to comply with the disclosure requirements (other than Scope 3) beginning with fiscal year-end 2023 (for years 2023, 2022 and 2021), accelerated and non-accelerated filers would be required to comply beginning with fiscal year-end 2024 (for years 2024, 2023 and 2022 if included in the Form 10-K) and smaller reporting companies would be required to comply beginning with fiscal year-end 2025 (for years 2025, 2024 and 2023 if included in the Form 10-K). Disclosure on Scope 3 emissions would be required the succeeding year for large accelerated, accelerated and non-accelerated filers.

52% of public company letters and 29% of industry association letters commented with concerns that the implementation timeline would be too short for registrants to comply with the final rules once adopted.

Sample Comments:

- “The timeline for implementing the Proposed Rule is far too aggressive. If adopted as proposed, the compliance date for the proposed disclosures (other than Scope 3 emissions disclosure) in annual reports for large accelerated filers . . . could be as early as the fiscal year 2023. That suggests that the necessary systems for compliance be in place by the end of this year and that we would have already needed to have them in place to the extent necessary for comparison to prior periods. For any adopted rule, there should be a multi-year transition period, even for large accelerated filers.”

- “Many companies will not have the necessary expertise or staff to adequately respond to the reporting requirements. As a result, they will need to rely heavily on outside consultants, which will further increase compliance costs. . . . This problem is compounded by the relatively brief phase-in period for compliance with the Rule Proposal. . . . One solution would be to extend the transition period for emissions disclosures by one or two years to allow companies to effectively implement the internal controls and procedures required for emissions disclosures.”

- “To enable compliance with the Proposed Rules, companies will need to expend significant effort to enhance data collection (including from third parties in their value chain), validation, reporting, control design, and third-party verification. . . . [The company] strongly recommends that the Commission extend the proposed implementation timeline such that the proposed disclosures, including GHG emission metrics, be required no earlier than for the 2024 fiscal year (filed in 2025), and preferably longer. It is critical to give registrants with sufficient time to ensure that their data is available and reliable in time for filing in the 10-K.”

- “As the Commission’s proposed standard would be different than [the EPA’s and other GHG] reporting standards, such difference would create additional burden on the underlying processes and systems for gathering the information. . . . As such, we believe that registrants need time to digest the Commission’s final rule and implement tracking mechanisms and/or system enhancements. . . . We recommend that the Commission provide a transition period of at least one year from the issuance of the final rule until the start of the first reporting period provided the Commission modifies the financial metric disclosure requirements as recommended herein or a transition period of at least two years if the final rule is issued substantially as proposed.”

- “We therefore respectfully ask the Commission to review and consider delaying the implementation timeline for all registrants and the phase-in periods for Scopes 1 and 2 emissions disclosure and assurance to at least five (5) years following the adoption of the final rules. This recommendation is consistent with the implementation timeline adopted for major recent changes to financial reporting standards such as the Financial Accounting Standards Board’s (FASB) implementation timeline for each of the revenue recognition and lease accounting standards, each of which provided public companies with significantly longer implementation timelines. . . . And prior to their issuance, the FASB worked for several years with stakeholders, including the financial statement preparer community, to finalize these rules. Neither rule contemplated changes that are as significant as those set forth in the Proposal.”

C. Increased Cost of Being a Public Company

The Commission estimates that annual direct costs to comply with the proposed rules (including both internal and external resources) would range from $490,000 (smaller reporting companies) to $640,000 (non-smaller reporting companies) in the first year and $420,000 to $530,000 in subsequent years. [3]

52% of public company letters and 43% of industry association letters raised concerns about the actual (and economic) cost of the Proposed Rules. Many believe the SEC underestimated the implementation costs, and a handful of companies provided quantitative estimates as to actual cost.

Sample Comments:

- “We are . . . concerned about the cost, complexity and practicability of complying with parts of the Proposal (in particular, the proposed amendments to Regulation S-X) that will be borne by registrants of all sizes, and which we believe, will significantly exceed the estimates set forth in the Proposal. Our company expects implementation costs in the $100-500 million range, and annual costs for on-going compliance in the $10-25 million range — costs that will ultimately be borne by investors and the public markets.”

- “This additional reporting [on GHG emissions] will come at a high costs: EPA estimated if it lowered its own de minimis reporting thresholds from 25,000 to 1,000 metric tons of CO2e per year it would cost an additional $266 million (in 2006 dollars). . . . EPA updated the reporting requirements for petroleum and natural gas systems in 2010. In doing so, EPA estimated that the incremental cost to reduce the bright line threshold from 25,000 to 1,000 would cost an additional $54.43 million (2006 dollars). . . . Based on EPA’s figures, the Proposed Rule could mean an additional cost to [the company] of $7,000,000 or more in 2006 dollars just to track and report Scope 1 emissions from additional facilities. These figures also suggest that the Commission has not fully accounted for the cost of this rule.”

- “[The company] estimates the cost of voluntarily reporting Scope 3 GHG emissions to be more than $1 million. . . . This does not include accounting personnel to incorporate Scope 3 emissions reporting into our Form 10-K or any commercial efforts needed to amend contracts or attempt to gather and verify Scope 3 emissions data across our value change to the extent it can be identified. Furthermore, [the company] estimates implementing the amendments to Regulation S-X would also be in the millions of dollars.”

- “[A small cap public company] estimate[s] that the total annual cost of satisfying the disclosure requirements set forth in the Proposal would be approximately $500,000 to $800,000, which would be significant for a company of our size.”

- “We believe the Commission’s cost estimates are significantly understated for large accelerated filers. . . . Currently, [the company’s] climate-related disclosures activities in line with TCFD recommendations require time and several million dollars in costs for data and information collection, IT system solutions, services provided and other related tools, techniques, and expertise. This does not include the significant additional time and cost of assurance of our performance data and disclosures.”

- “[W]e believe the SEC has significantly underestimated the costs of compliance, which we believe would be many multiples of the projected $640,000 per year initially and would likely increase over time.”

- “The cost of registrants trying to report in alignment with just certain aspects of TCFD for their first time on a voluntarily basis can be around $500,000. This does not account for the level of rigor, financial line items, attestation, and liability costs associated with complying with this Proposed Rule. The actual cost for complete alignment to TCFD could be up to $1,000,000 per registrant over several years. This does not include the annual cost associated with preparing for and conducting attestation.”

- “[B]y only considering the costs of compliance to the public companies that are required to file, SEC misses completely the costs to companies that supply SEC filers, the largest being the induced requirement to gather and report their GHG emissions to the filing company as a condition of their supply relationship. . . . [B]ecause filing companies will have to undertake the herculean task of estimating their Scope 3 emissions, they will have no other choice but to require their suppliers to provide their GHGs, even if those suppliers have no regulatory requirement otherwise to report to SEC or EPA.”

D. Timing Deadlines for Reporting

The Proposed Rules would require the new climate-related disclosure to be included annually in the registrant’s Form 10-K (and Form 20-F for foreign private issuers). By requiring disclosures in Form 10-K, large accelerated filers will need to finalize both the traditional year-end financial reporting and the new climate-related disclosure no later than 60 calendar days after the fiscal year end.

45% of public company letters and 24% of industry association letters commented on the reporting timeline for the new climate-related disclosure requirements, with many requesting additional time to prepare the necessary disclosure.

Sample Comments:

- “We have experience with reporting GHG emissions data and understand the time commitments and complexities involved to gather, model, analyze and verify the accuracy of such data. In addition to our disclosure of Scope 1 GHG emissions data in our Form 10-K, we also include Scope 2 and Scope 3 emissions data in our Climate Report, which is published significantly later in the year compared to our Form 10-K filing. We recommend that registrants be allowed to provide preliminary emissions data . . . for the most recently completed fiscal year as an estimated amount in the Form 10-K with final emissions data, with the corresponding attestation report on Scope 1 and Scope 2 emissions, provided in a subsequent reporting period (either later in the year on Form 10-Q or the following year Form 10-K).”

- “The Proposal’s requirement for all climate-related disclosures to be provided in a registrant’s annual report on Form 10-K will prove challenging. Registrants already face significant pressure to meet existing annual and quarterly reporting deadlines, and the addition of climate-related disclosures, particularly quantitative disclosures that will need to be accompanied by assurance, will only increase such pressures. Moving GHG emissions disclosures and assurance to a separate report, such as furnishing within a specialized disclosure in Form SD with a later reporting deadline in the calendar year, will provide companies with additional time to properly collect GHG emissions data and assurance providers sufficient time to render their opinions. As an alternative, it may also be advisable to report GHG emissions on a one-year lag to ensure sufficient time for reporting and assurance.”

- “The SEC financial reporting timelines are not consistent with current regulatory and voluntary reporting timelines. Currently our regulatory and voluntary reporting is based on verified annual data for the prior fiscal year. This means that GHG emissions data are collected and submitted to applicable regulators at the end of the first quarter following the reporting period. Voluntary disclosures such as our annual sustainability report and CDP submission are typically published at the end of the second quarter following the end of the reporting period. Transitioning to a reporting schedule that is consistent with SEC deadlines for Form 10-K will require an additional, parallel reporting process which will incorporate significant estimates (e.g., for the prior 4th quarter), reducing the accuracy of the information and its usefulness to investors and will impose a major burden on our existing reporting systems. A separate mid-year climate disclosure requirement would help ease the transition and avoid the potential need to update these disclosures based on actual data received after the Form 10-K filing deadline.”

E. Liability

The Proposed Rules would treat all climate-related disclosures as “filed” rather than “furnished” (other than those included in a foreign private issuer’s Form 6-K, which generally are “furnished”). This means that, in addition to general anti-fraud liability under Rule 10b-5 under the Exchange Act, such disclosures would be subject to incremental liability under Section 18 of the Exchange Act and, to the extent such disclosures are included or incorporated by reference into Securities Act registration statements, subject to liability under Sections 11 and 12 of the Securities Act.

45% of public company letters and 43% of industry association letters commented on liability concerns, with many requesting the climate-related disclosures be “furnished” rather than “filed” and that safe harbor protections from Sections 11, 12 and 17(a) of the Securities Act and Sections 10(b) and 18 of the Exchange Act be afforded for certain of the proposed disclosure requirements, including any forward-looking information and GHG emissions disclosure.

Sample Comments:

- “Due to the long-term and uncertain nature of certain climate-related information, particularly while associated frameworks and standards are still evolving, [the company] believes that climate-related disclosures should be furnished to, rather than filed with the Commission, and not be included as part of any annual or quarterly Sarbanes-Oxley Act certifications.”

- “[W]e believe that the new climate report should be treated as “furnished” instead of “filed” for purposes of liability under the Exchange Act, and not automatically incorporated by reference into Securities Act registration statements (where strict liability applies). This approach would appropriately recognize the novel and complex nature of the proposed disclosure requirements—including, among other items, GHG emissions data, scenario planning, targets and goals, and the detailed nature of many of the proposed requirements—which go far beyond information that has been required in SEC filed reports. In these circumstances, treating the information as furnished would provide appropriate liability protection while continuing to make the information widely available via the SEC’s EDGAR system.”

- “[I]f climate information is subject to liability under Section 18 of the Securities Exchange Act and the strict liability provisions of Section 11 of the Securities Act, issuers are likely to disclose information in the most limited manner possible, and they may be unwilling to provide additional information that could give investors context. For these reasons, until climate-related estimation, monitoring and measurement methodologies and processes are sufficiently mature to support the more rigorous liability standards, we believe it would be more appropriate to remove the private right of action under 10b-5 with respect to such disclosures, or allow registrants to furnish climate-related disclosures as part of a separate disclosure report, formally furnished to the SEC, or make such disclosures through existing sustainability reports.”

- “As climate change views and related rules and interpretations continue to evolve, we would appreciate the ability to furnish rather than file any mandated climate-related disclosures, particularly any disclosure requirements subject to significant interpretation or differences of opinion. Allowing such disclosures to be furnished and strengthening safe harbors around good faith disclosures will encourage greater disclosure transparency while climate and sustainability views evolve into greater uniformity.”

- “There should exist a meaningful safe harbor for the entirety of any final rule considering the unique challenges that the SEC itself recognizes registrants must overcome to meet the proposed climate-related disclosure obligations. The SEC should enhance the safe harbor to recognize the evolving nature and inherent uncertainties of assessing climate risks to the level of granularity (e.g., risks to specific locations and assets) required in the Proposed Rule. Registrants should be shielded from liability for forward-looking statements and any inaccuracy in the reporting of the many metrics that necessarily involve uncertainty and subjective or speculative judgment calls.”

F. SEC Authority to Implement Proposed Rules

26% of public company letters and 81% of industry association letters commented on whether the Commission has the authority to implement the Proposed Rules.

Several of these commenters also raised the First Amendment concern noted by Commissioner Hester Peirce in her dissent to the Proposed Rules. Commissioner Peirce expressed a view that the proposal exceeds the Commission’s statutory limits of authority “by using the disclosure framework to achieve objectives that are not [the Commission’s] to pursue and by pursuing those objectives by means of disclosure mandates that may not comport with First Amendment limitations on compelled speech.” [4]

Sample Comments:

- “The Proposal, as currently written, suffers from legal flaws that will undermine the validity of any final rule and the Commission’s objectives. Although information regarding climate risks and transition opportunities is important to many investors and companies, as evidenced by the Form 10-Ks and sustainability reports published by [association] members, the Proposal imposes an unprecedented degree of granularity and would require official reporting through the stringent requirements of Regulations S-X and S-K on predictive judgments that fall far outside of what federal securities laws demand. The Proposal also raises serious constitutional questions under the separation of powers. Furthermore, aspects of the Proposal would violate the First Amendment’s prohibition against compelled speech. If the Commission does not significantly alter the Proposal to address these concerns, then the final version of the rule will be vulnerable to invalidation on legal grounds.”

- “We agree it is critical for the Commission to adhere to the scope of its authority as established by Congress, to adhere to established precedent regarding materiality and to carefully consider the risks associated with compelled speech. We further agree with the API the Proposal is beyond the scope of the Commission’s authority, violates foundational principles regarding materiality, as that term has been interpreted by the U.S. Supreme Court, and raises significant Constitutional concerns.”

- “Congress has not given the SEC unlimited authority over the economy or climate change policy. The use of the [TCFD Framework] and the [GHG Protocol] as the basis of the disclosure framework for the proposal makes it clear that the SEC is attempting to achieve outcomes which are not within the agency’s authority. . . . Congress has yet to issue a specific mandate allowing the SEC to order climate-change disclosures.”

- “We share many of the additional concerns articulated by other commenters about the breadth, potential impacts and legal authority to implement the Proposal, including, among others, whether the Proposal is within the scope of authority granted to the SEC by Congress, is enforceable based on application of the major questions doctrine, or exceeds First Amendment limitations on compelled speech.”

VI. Select Remarks from Non-Reporting Companies

Non-reporting energy companies who submitted comment letters focused primarily on concerns with the Proposed Rules’ impact on the energy industry in general and, specifically, on smaller, private companies. Many raised concerns that the Proposed Rules would “operate to limit or deny financing to oil and natural gas companies.” As one sample comment noted, “[t]hese time-intensive, resource-heavy measures will impair the abilities of private companies to pursue their business plans and grow through private capital. Increased costs will create significant burdens even if such private companies ultimately never seek to access the public market.”

Non-reporting companies also raised concerns that the Proposed Rules, and in particular, the GHG emissions reporting requirements, would “undoubtedly demand additional information from . . . privately traded companies not otherwise subject to the SEC’s jurisdiction” and impact the ability of smaller suppliers to public energy companies to compete for business. As noted by a few commenters:

“[b]ecause any one company’s Scope 3 emissions permeate among potentially many hundreds or even thousands of companies and millions of consumers, they are nearly impossible to accurately measure, calculate, or otherwise estimate. SEC would be requiring companies . . . to determine emissions data that are not available from our suppliers, who may-or may not-have SEC reporting obligations. The rule would incentivize SEC filers to favor large suppliers who have the wherewithal to calculate and provide their emissions data while disadvantaging smaller suppliers that cannot.”

One commenter also noted the impact of the Proposed Rules on private companies seeking to go public:

“The Proposed Rule explicitly notes that the climate-related disclosures and data must be included in registration statements but, per the implementation timeline, provides a delayed compliance date for registrants other than large accelerated filers. A smaller private company contemplating an IPO that would, if already public, qualify as an accelerated filer or non-accelerated filer, would be required to comply with the Proposed Rule’s disclosure requirements before an existing accelerated filer or non-accelerated filer, thereby increasing the burden on new entrants to the public markets. Likewise, the Proposed Rule’s amendments to Form S-4 would require a private target company to present all the disclosures required by the Proposed Rule in a Registration Statement on Form S-4 registering the equity securities of the acquiror to be issued in an M&A transaction. For a non-reporting company that has not maintained such records (and which may have been indifferent as to whether its potential acquiror was a reporting company), such a disclosure requirement presents a significant potential barrier to being acquired in an M&A transaction or a SPAC merger.”

VII. Conclusion

The breadth and scope of the Proposed Rules predictably resulted in many comments from the energy industry. These comments are informative as to how the industry is reacting to the Proposed Rules and what steps may be necessary for companies to start taking to be positioned to comply with the Proposed Rules, when adopted. Gibson Dunn’s premier securities regulation and energy lawyers are available to assist companies with preparation and compliance with new disclosure requirements.

Endnotes

1For purposes of this post, we define energy companies to include companies in the oil and gas industry, including those in the exploration and production, midstream, downstream, and oilfield services sectors.(go back)

2See Release No. 33-11042, p. 9-10.(go back)

3See Release No. 33-11042, p. 373.(go back)

4See Commission Hester Peirce, “We are Not the Securities and Environment Commission—At Least Not Yet,” Mar. 21, 2022, https://www.sec.gov/news/statement/peirce-climate-disclosure-20220321.(go back)