Print

PrintSandra Boss is Global Head of Investment Stewardship and Michelle Edkins is Managing Director of Investment Stewardship at BlackRock, Inc. This post is based on their BlackRock memorandum.

Consistent with BlackRock’s fiduciary duty as an asset manager, BIS’ purpose is to support companies in their efforts to deliver long-term durable financial performance on behalf of our clients. These clients include public and private pension plans, governments, insurance companies, endowments, universities, charities and, ultimately, individual investors, among others.

BIS serves as an important link between our clients and the companies they invest in—and the trust our clients place in us gives us a great responsibility to advocate on their behalf. Our clients depend on BlackRock to help them meet their investment goals; the business and governance decisions that companies make will have a direct impact on our clients’ long-term investment outcomes and financial well-being. This post provides an overview of our proxy voting from July 1, 2021, through June 30, 2022, as part of our broader stewardship work engaging with the companies we invest in on behalf of our clients.

With one of the industry’s largest teams of stewardship and governance specialists from a range of disciplines, BIS is well-equipped to bring a globally consistent, locally nuanced perspective to our clients and to the companies in which we invest on their behalf. We engage with companies throughout each year and our engagements often span multiple years. This leads to stronger relationships with companies and more constructive outcomes for shareholders and businesses alike.

We work closely with BlackRock’s active investment colleagues to help ensure our stewardship work is grounded in encouraging the practices that support long-term corporate financial performance, rather than the pursuit of good governance for its own sake. Our analysts’ sector expertise and local market knowledge allows for informed dialogue on the issues most material to companies’ ability to create durable, long-term value for our clients.

This depth of experience also enables us to make informed, considered voting decisions—we do not rely on the recommendations of proxy advisors. We continued to take a measured approach to the stewardship policy enhancements that inform our voting, maintaining a consistent year-on-year view on what we find to be helpful as investors in assessing the material governance and sustainability risks facing the companies we invest in for our clients.

While BIS is central to our fiduciary approach, we also see a growing interest among investors—including our clients—in the corporate governance of public companies. That is why we announced BlackRock Voting Choice in October 2021 and continue to expand the opportunity for more clients to participate in proxy voting decisions over their listed equity investments, where legally and operationally viable. As detailed in our paper, It’s All About Choice, our ambition over time is to continue developing new technologies while working with industry partners to expand voting choice for even more clients—including individual investors.

Through all these efforts, we are working to serve our clients and stay ahead of their needs. Our sole focus remains on helping them achieve their long-term financial goals, because the money we manage is theirs, not ours.

Our Investment Stewardship toolkit

Engaging with companies

How we build our understanding of a company’s approach to corporate governance and sustainable business models, and how we communicate our views.

Voting in our clients’ interest

How we signal our support for or raise our concerns over a company’s corporate governance or business model. We may signal concerns by not supporting the election of directors or other management proposals, or by voting in support of a shareholder proposal. Voting on director elections is a globally consistent signal of concerns when boards do not seem to have acted in shareholders’ long-term financial interests.

Transparency in our activities

How we inform stakeholders of our work to advance the long-term economic interests of our clients. We continue to raise the bar on our transparency. This report illustrates our voting on behalf of our clients at 14,140 companies, highlighting the breadth and depth of our stewardship efforts on behalf of our clients in the 2021-22 proxy year. [1]

Our stewardship approach: engaging on material risks and opportunities for our clients

BlackRock was founded on the core premise of understanding investment risk and anticipating the needs of our clients, supporting them in achieving their long-term investment goals. Our stewardship team plays a key role in helping our clients navigate the governance and sustainability risks and opportunities that, in our view, can affect their paths towards reaching those goals. Companies continued to face complex strategic and operational challenges over the year, due to persistent geo-political and socio-economic factors. In our engagement with company boards and management, BIS has acknowledged these headwinds and continued to encourage a long-term focus.

We firmly believe in the value of engaging with companies. Encouraging responsible business operations serves the interests of long-term investors in public companies. BIS engages companies on behalf of BlackRock’s equity index funds and accounts and coordinates with portfolio managers with active positions in a company. When BIS engages a company, we do so from the perspective of a long-term investor. Engagement enables us to have ongoing dialogue with companies and build our understanding of the challenges they face. This is particularly important for our clients invested in indexed funds, which represent a significant majority of BlackRock’s equity assets under management, as they do not have the option to sell holdings in companies that are not performing as expected. Companies can continue to look to BIS, as a long-term shareholder on behalf of our clients, to provide constructive feedback as they enhance their corporate governance and sustainable business models. Likewise, we will communicate our views when we believe a company is not appropriately managing risks that could potentially impact our clients’ ability to meet their long-term investment goals.

Our industry-leading, specialist team of experienced stewardship analysts conducts year-round engagements with thousands of companies across 55 markets on behalf our clients and their millions of beneficiaries. This year, the BIS team continued our intensive, year-round engagement program, reaching a record-level 3,690 engagement meetings (3,650 last year) with 2,460 unique investee companies (2,340 last year). We continue to focus our engagement on a consistent set of five priorities that we believe are essential to the long-term financial performance of our clients’ investments: board quality and effectiveness; strategy, purpose, and financial resilience; incentives aligned with value creation; climate and natural capital; and company impacts on people.

In our engagements, we encourage companies to provide comprehensive disclosures on their long-term strategy, the milestones to delivering it, and the governance and operational processes that underpin their businesses and long-term financial performance. In addition to robust financial disclosures, we find it helpful when companies provide the data and narrative that help investors understand how they approach material, business relevant sustainability risks and opportunities. BlackRock has consistently advocated for enhanced reporting to help investors understand risks and opportunities in the business models of the companies they invest in. Better quality information leads to better investment decision-making and capital allocation. We are encouraged by the significant progress made over the past 12 months, at a global and market level, advancing towards a global baseline set of sustainability reporting standards. Once such standards are realized, we are hopeful that the reporting burden on companies can be reduced and the quality of information—both data and narrative—available to investors will be improved, supporting more efficient capital markets. These disclosures inform our voting and engagement activities.

Voting on behalf of clients who authorize BlackRock to do so

Informed by our Global Principles and market-level voting guidelines, we have expressed our support for or concern about companies’ management of issues that have a long-term impact on shareholder returns, such as sustainability risks and opportunities, through voting at annual general and special shareholder meetings. Globally, we voted on, behalf of those clients who authorized us to do so, at more than 18,000 shareholder meetings on more than 173,000 proposals. Similar to previous years, shareholder proposals represented less than 1% of the total proposals we voted on during the 2021-22 proxy year.

Our voting in support of management was largely consistent with the prior proxy year: globally we voted in support of 90% of directors standing for election and for all items on the agenda at 57% of shareholder meetings (also 57% last year). This year, BIS was more supportive of management in the Americas and EMEA, where companies have made significant progress on the governance and sustainability matters that inform our voting. In the Americas, we were more supportive of directors as companies made substantial improvements in board diversity; we did not support the election of 4% of directors (6% last year) for lack of board diversity. In EMEA, we were more supportive as companies adapted their remuneration policies and disclosures to align better with their long-term shareholder returns in the prolonged post-COVID economic environment, not supporting 6% of directors due to concerns about executive compensation (7% last year). In both the Americas and EMEA, we were also more supportive of companies with material climate risk in their business models as they improved their climate action plans and disclosures, voting to signal concern at 155 companies (264 last year). We were less supportive of companies in Asia, where director independence remains a significant governance concern for minority shareholders like our clients. Director independence concerns led us to not support the election of 8% of directors (6% last year) in APAC.

BIS centers our stewardship work in corporate governance. In our experience, sound governance, in terms of both process and practice, is critical to the success of a company, the protection of shareholders’ interests, and long-term shareholder value creation. That is why board quality and effectiveness remain a top engagement priority, and a key factor in the majority votes cast on behalf of clients. Like last year, our leading reasons for not supporting director elections—and management proposals more broadly—were governance-related: 1) lack of board independence, 2) lack of board diversity, 3) directors having too many board commitments and 4) executive compensation that was not aligned with company strategy or long-term performance.

Board quality and effectiveness remain a top engagement priority, and a key factor in the majority of votes cast on behalf of clients.

Like last year, our leading reasons for not supporting director elections –and management proposals more broadly –were governance-related:

- Lack of board independence

- Lack of board diversity

- Directors having too many board commitments

- Executive compensation not aligned with long-term performance

It is also our conviction that climate risk is investment risk, and we see growing recognition that climate risk and the energy transition are already transforming both the real economy and how people invest in it. As outlined in our commentary, Climate risk and the global energy transition, we looked to companies to make disclosures in line with the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD)—including in relation to governance, strategy, and risk management—that enable investors to assess their climate risk. For completeness, such disclosure was most helpful when it included scope 1 and 2 greenhouse gas (GHG) emissions metrics and meaningful short-, medium-, and long-term emissions reduction targets. [2]

We have been encouraged by the progress many companies in key sectors have made in their energy transition planning and actions, as detailed in their enhanced disclosures. Market-level initiatives, such as the Net Zero Banking Alliance and Oil & Gas Methane Partnership 2.0, have helped companies take steps relevant to their business models and sectors. We have also seen enhanced disclosure by many companies on how they are engaging on policies addressing climate risk and the energy transition, through their own corporate political activities and those of the trade associations of which they are active members. This has enabled us to be more supportive of management in our voting on shareholder proposals seeking enhanced disclosure on these issues this proxy voting year.

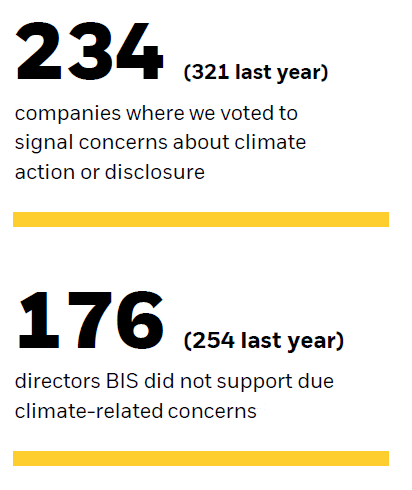

Globally, we voted to signal concerns about climate action or disclosure at 234 companies, or 1.7% (321 or 2.4% last year). [3] We did not support the election of 176 directors for climate-related concerns (254 last year). [4] We were pleased to note that 291—over a quarter—of the companies in our 1,000+ company climate focus universe have demonstrated marked progress in climate disclosures and targets during the last two years. [5] We engaged and/or voted on climate concerns at 81% of these improving companies.

2022 shareholder proposals more prescriptive than 2021

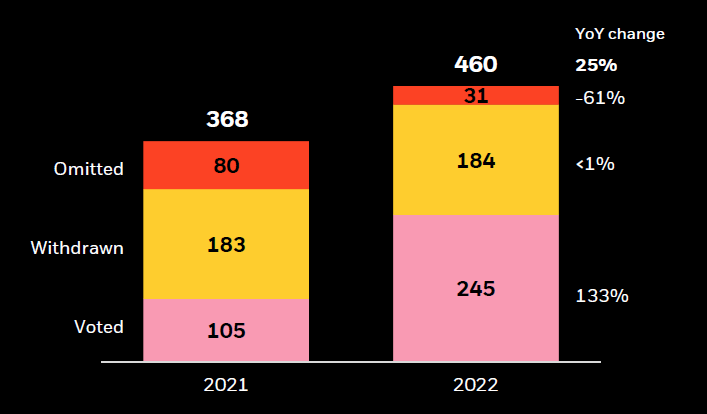

We consider well-crafted, well-targeted shareholder proposals to play a useful role in the stewardship toolkit. Our research indicates that proposals that receive high support from shareholders lead to beneficial responses from companies. [6] However, as we explained in our May commentary, 2022 climate-related proposals more prescriptive than 2021, [7] we observed a marked increase in E&S shareholder proposals that went to a vote (e.g., in the U.S. we saw a 133% increase) [8] and many more proposals were unduly constraining on management or were overly prescriptive as to information sought or timeframes. Others failed to recognize the progress made such that companies had largely met the ask of the proposal.

E&S shareholder proposals voted at U.S. companies attracted 27% shareholder support on average—down from 36% last year—which suggests that most investors took a measured, materiality-based approach in their analysis and voting on this year’s proposals. [9] A recent report noted that only 9% of the 208 E&S shareholder proposals in its sample passed, compared with 27% of 131 such proposals last year. [10]

Among the several themes we observed this year included proposals requesting:

- Ceasing providing finance to traditional energy companies;

- Decommissioning the assets of traditional energy companies;

- Requiring alignment of bank and energy company business models solely to a specific 1.5⁰C scenario;

- Changing articles of association or corporate charters to mandate climate risk reporting or voting;

- Setting absolute scope 3 GHG emissions reduction targets; [11]

- Directing climate lobbying activities, policy positions or political spending, among others.

Increased U.S. E&S shareholder proposal activity and less SEC no-action relief [12]

U.S. E&S shareholder proposal filings and votes up; SEC no-action relief down

Source: Institutional Shareholder Services (ISS) Voting Analytics Database (voted proposals); ISS Shareholder Proponent Database (omitted and withdrawn proposals).

How we voted on E&S shareholder proposals

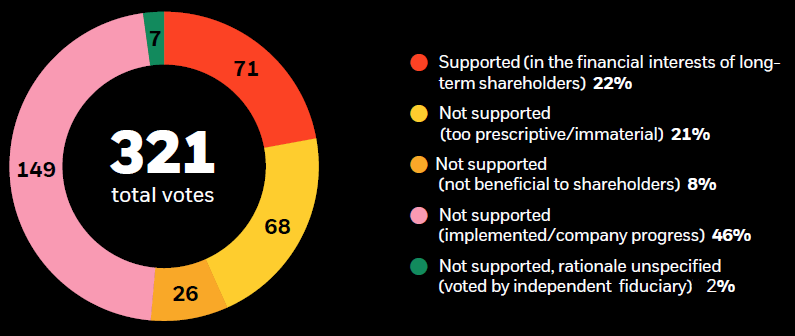

Globally, this proxy year we supported 22% of the E&S shareholder proposals that we voted on; in absolute terms, this reflects support for 71 E&S proposals (81 last year). Average market-wide support was 26%. [13]

Whereas last year we saw climate-related shareholder proposals that addressed material business risks and often requested reports providing information, as mentioned in the previous section, in 2021-22, BIS observed and assessed several notable themes that ultimately reduced our support for some shareholder proposals. For instance, such proposals sought decommissioning fossil fuel assets, elimination of financing and insurance underwriting for fossil fuel projects, and cessation of fossil fuel exploration and development. Many of these more prescriptive proposals attracted lower levels of investor support more broadly. [14]

Amongst social proposals, diversity equity and inclusion audits in the U.S. achieved notable support, with eight proposals passing and six others receiving more than 40% support; we supported 54% of these proposals this season.

When assessing shareholder proposals, we evaluate each proposal on its merit, with a singular focus on its implications for long-term value creation. We consider the business and economic relevance of the issue raised, as well as its materiality and the urgency with which we believe it should be addressed. [15] BIS supported 21% of all environmental, social, and governance (ESG) shareholder proposals put to a vote in the 2021-22 proxy year.

BIS reasons for votes on E&S shareholder proposals [16]

Source: BlackRock, Institutional Shareholder Services (ISS). ISS classifications used. Sourced on July 11 , 2022, reflecting data July 1, 2021 through June 30, 2022. Excludes Japan. [17]

Looking forward

We expect to continue to take a measured approach to our stewardship activities on behalf of clients. We continuously receive useful feedback from companies and clients as we engage over the proxy year, and these insights will help us refine our global principles and voting guidelines. We do not anticipate significant changes in these or in our engagement priorities, which we believe to be grounded in enduring factors that shape the ability of companies to deliver durable profitability. The context within which companies are managing their businesses will continue to be a consideration in our voting and engagement. We remain focused on outcomes for our clients that create long-term shareholder value and help them achieve financial well-being.

The complete publication, including footnotes, is available here.

Endnotes

1Source: BlackRock. Sourced on July 11, 2022, reflecting data from July 1, 2021 through June 30, 2022. Numbers are rounded to the nearest ten.(go back)

2The GHG Protocol Corporate Standard classifies a company’s GHG emissions into three “scopes.” Scope 1 emissions are direct emissions from owned or controlled sources. Scope 2 emissions are indirect emissions from the generation of purchased energy. Scope 3 emissions are all indirect emissions (not included in scope 2) that occur in the value chain of the reporting company, including both upstream and downstream emissions.(go back)

3Votes not supporting unique companies on climate include: 1) votes not supporting or abstaining on director elections and director-related proposals, and 2) votes supporting or abstaining on climate-related shareholder proposals.(go back)

4Abstentions are included.(go back)

5Limited to companies within the BIS climate focus universe who improved their GHG reduction targets since July 1, 2020 according to MSCI. See page 47 in this report for further detail.(go back)

6See page 10 in our report, “Our 2021 Stewardship Expectations.”(go back)

7This relates to the companies in the BIS U.S. voting universe where we voted on behalf of our clients.(go back)

8Source: ISS Voting Analytics.(go back)

9Source: BlackRock, Institutional Shareholder Services (ISS). Sourced on July 18, 2022 reflecting data from July 1, 2021 through June 30, 2022. The term “average” refers to “mean” shareholder support. Median shareholder support for E&S shareholder proposals in the U.S. was 21% for the 2021-22 proxy year, down from 33% last year.(go back)

10Freshfields Bruckhaus Deringer LLP. “Trends and Updates from the 2022 Proxy Season.” July 2022.(go back)

11Regarding scope 3 emissions, this is not to minimize value chain, or scope 3, GHG emissions. They are a major global societal issue and, for companies where they are material, the prospect of future policy change couldaffect the economic viability of their business models. To effect change in scope 3 GHG emissions in a fair and balanced way, policy action by governments will be necessary. Companies cannot solve scope 3 on their own. As national and regional policy expectations around scope 3 evolve and crystallize, we will look to companies to align their disclosures and commitments accordingly.(go back)

12Year 2021 reflects data from July 1, 2020-June 30, 2021. Year 2022 reflects data from July 1, 2021 -June 30, 2022. Omitted refers to proposals for which the SEC has granted“no-action relief” and are excluded from a company’s proxy without the proponent’s consent.(go back)

13Source: BlackRock, Institutional Shareholder Services (ISS). Sourced on July 18, 2022 reflecting data from July 1, 2021 through June 30, 2022. Excludes the Japanese market, where

numerous shareholder proposals are filed every year due to low filing barriers, and where shareholder proposals are often legally binding for directors in this market. Votes to not support

shareholder proposals includes withhold votes. Globally, median shareholder support for E&S shareholder proposals was 19% for the 2021-22 proxy year.(go back)

14Financial Times, “Investors at top US banks refuse to back climate proposals”, April 26, 2022.(go back)

15See page 14 of BIS’ Global Principles for a complete explanation of our approach to shareholder proposals.(go back)

16Does not include director election, director-related, or “other” proposals put forth by shareholders. BIS votes cast on shareholder proposals on behalf of our clients are independent of whether management recommended voting for or against the proposal.(go back)

17The independent fiduciary makes voting decisions based solely on BlackRock’s publicly available proxy voting guidelines, which aim to advance our clients’ long-term financial interests, and public information disclosed by the relevant company. See page 2 in our commentary, “How BlackRock Investment Stewardship Manages conflicts of interest.”(go back)