Print

PrintIra T. Kay is Managing Partner and Mike Kesner is Partner at Pay Governance LLC. This post is based on their Pay Governance memorandum. Related research from the Program on Corporate Governance includes Paying for Long-Term Performance (discussed on the Forum here) by Lucian Bebchuk and Jesse Fried.

Executive Summary

The Securities and Exchange Commission (SEC) released its final version of the rules mandated by Dodd-Frank regarding the disclosure of pay versus performance (PVP) on August 25, 2022. Initial rules were proposed in 2015, and follow-up proposals and invitations for comment were extended in late 2021 and early 2022 by the SEC. The SEC PVP disclosure is intended to provide investors with a clear analysis of the alignment of the top executives’ compensation actually paid (CAP) with the company’s financial and stock price performance. This analysis, while complex, may be viewed by investors as a window into the governance and workings of the company’s pay for performance model.

Pay Governance LLC has prepared this post with the intent of providing our clients and interested parties with a comprehensive yet clear picture of this new SEC disclosure requirement. This Executive Summary provides a snapshot of the new rules. The sections that follow the Executive Summary provide our interpretation of the SEC rules along with some commentary on the implications of the new disclosure. We want our readers to know, however, that we will be providing additional analysis and recommendations regarding the rules in the weeks ahead as we have time to study the SEC’s recommended rules more carefully.

We also encourage SEC-filing companies to begin gathering the data and developing the PVP discussion needed to comply with the new disclosure requirements. There is a great deal of disclosure detail that companies can begin to draft immediately; please refer to the last section of this post where we have recommended steps companies can take to initiate this process.

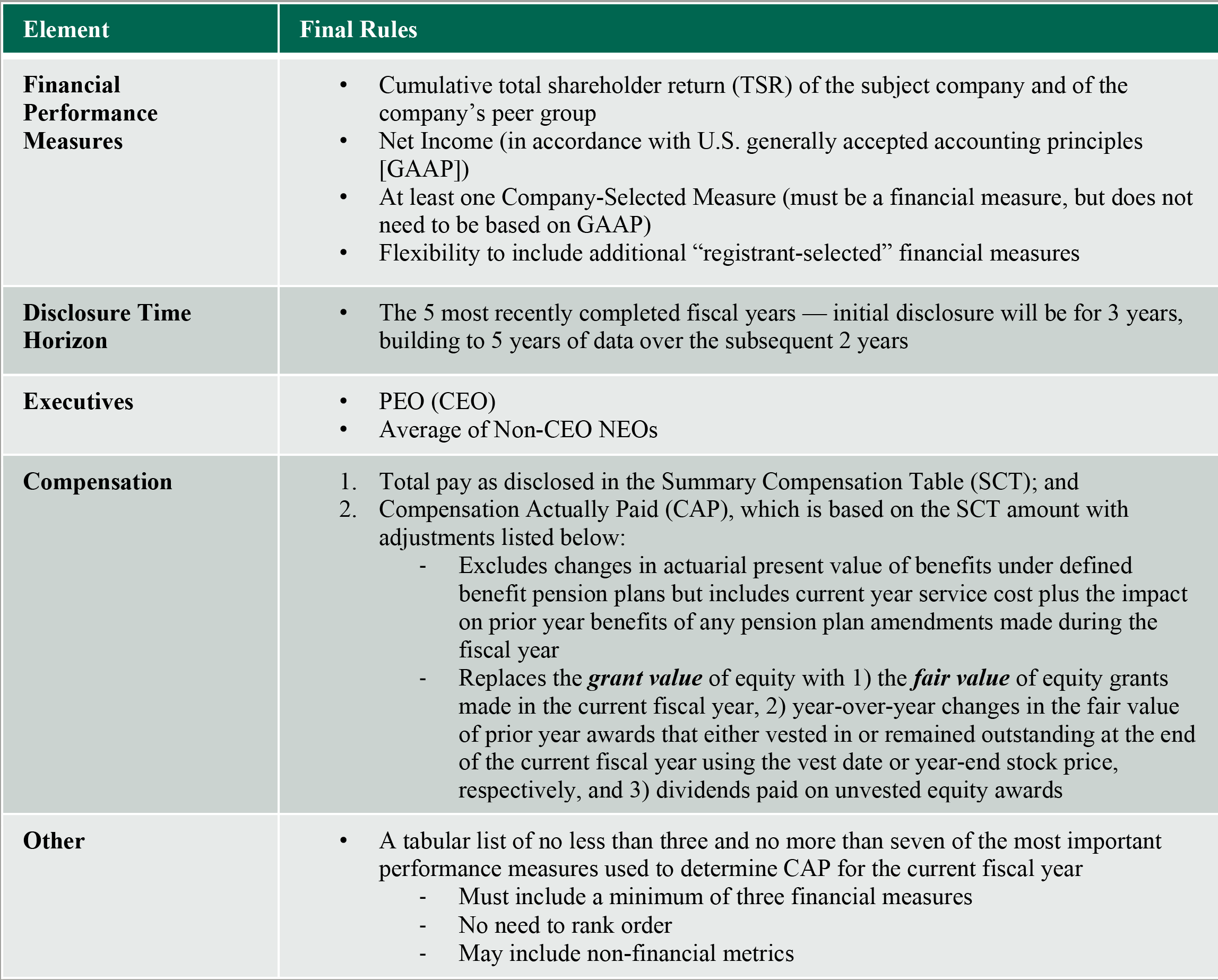

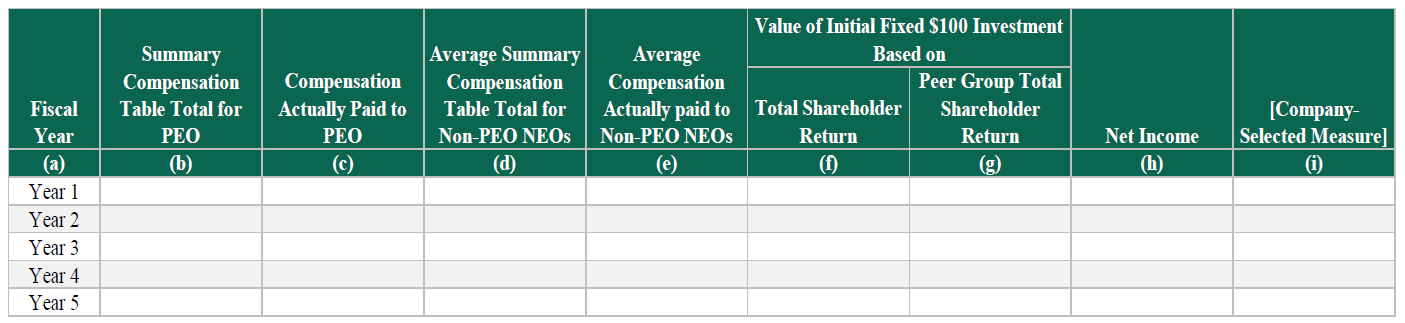

The new rules will become effective for companies with fiscal year disclosures ending on or after December 16, 2022. This means that companies on a calendar year will need to include their PVP disclosures in their 2023 proxies. In the table below, we have provided an overview of the key disclosure requirements and have included the required tabular disclosure mandated by the new rules.

Tabular PVP disclosure required by the final rules:

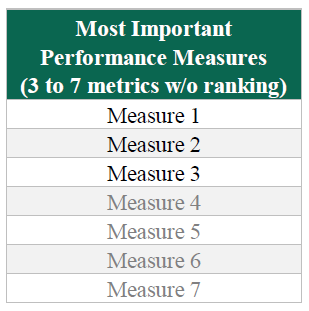

Tabular List of the company’s “most important” performance measures:

Background

The SEC’s 234-page release of the final rules appears to have carefully considered the often-conflicting comments received from investors, companies, consultants, and other interested parties in 2015 when the rules were first proposed. The final rules also reflect comments made in late 2021 as well as in 2022 when the rules were re-released by the SEC with several questions for comment.[1] The SEC acknowledges that the final rules will be more burdensome to comply with than the original proposal; however, the SEC believes that the additional effort will result in an improved level of accuracy in depicting PVP.

Required Disclosures in Tabular Format

The tabular disclosure required by the final rules is shown in the Executive Summary above. The primary tabular disclosure requires the reporting of the company’s compensation, company and peer total shareholder return and company financial performance for the 5 most recently completed fiscal years. The other tabular disclosure is composed of a list of no less than three and not more than seven of the most important performance measures used to determine compensation for the current fiscal year. This list must include at least three financial metrics and may include non-financial metrics.

Compensation

Companies will be required to include total compensation reported in the SCT for the CEO and the average total compensation of the other NEOs, with each amount juxtaposed against the CAP for each of the past 5 years. Importantly, the SCT and CAP amounts are not directly comparable, as the SCT includes 1 year of equity compensation whereas CAP includes the fair value of the current year equity awards and the change in value during the current year of unvested prior year equity awards and awards that vested during the year. Thus, no inference should be drawn between the amount reported in SCT and CAP each year, and it is notable the SEC does not require a comparison of these two columns in the PVP discussion.

Performance Measures

Companies will be required to include four mandated financial performance measures: (1) company cumulative TSR, (2) the peer group’s cumulative TSR (market cap-weighted), (3) net income (as reported on a GAAP basis), and (4) a company-selected metric (CSM). The CSM, according to the SEC, should be the metric the company believes is the most important financial metric for determining CAP in the current fiscal year. The company’s CSM cannot be TSR or net income, as those metrics are already included in the table, and it must be included in the top three to seven tabular list of most important metrics. The SEC will also allow companies to include additional columns in the table for other financial CSMs they believe are important metrics for evaluating PVP.

The SEC acknowledges that in many cases the CSM may be a non-GAAP metric, and such metrics will require disclosure of a reconciliation to GAAP. The reconciliation disclosure is not likely to be burdensome for most companies because such disclosures are already required for companies using non-GAAP metrics in their earnings releases or incentive plans.

While the SEC requires the inclusion of both the company and peer group TSR in the PVP table (which presumably is intended to provide context on how a company is performing), the PVP table does not include peer company comparisons for net income, CSM, or peer group compensation data, which may leave out important context for fully evaluating PVP.

“Three to Seven” Tabular Disclosure

The SEC disclosure rules require companies to report no less than three financial measures and no more than seven measures, which are the most important metrics used by the company to determine CAP for the current fiscal year. The SEC allows non-financial measures to be included in the list, unlike the primary tabular disclosure, which is limited to financial measures, provided the three financial measure minimum is met. The three to seven list may include TSR or net income (if applicable) in addition to the other metrics. Initially, the SEC wanted the metrics to be presented in ranked order of importance; however, that requirement has been dropped.

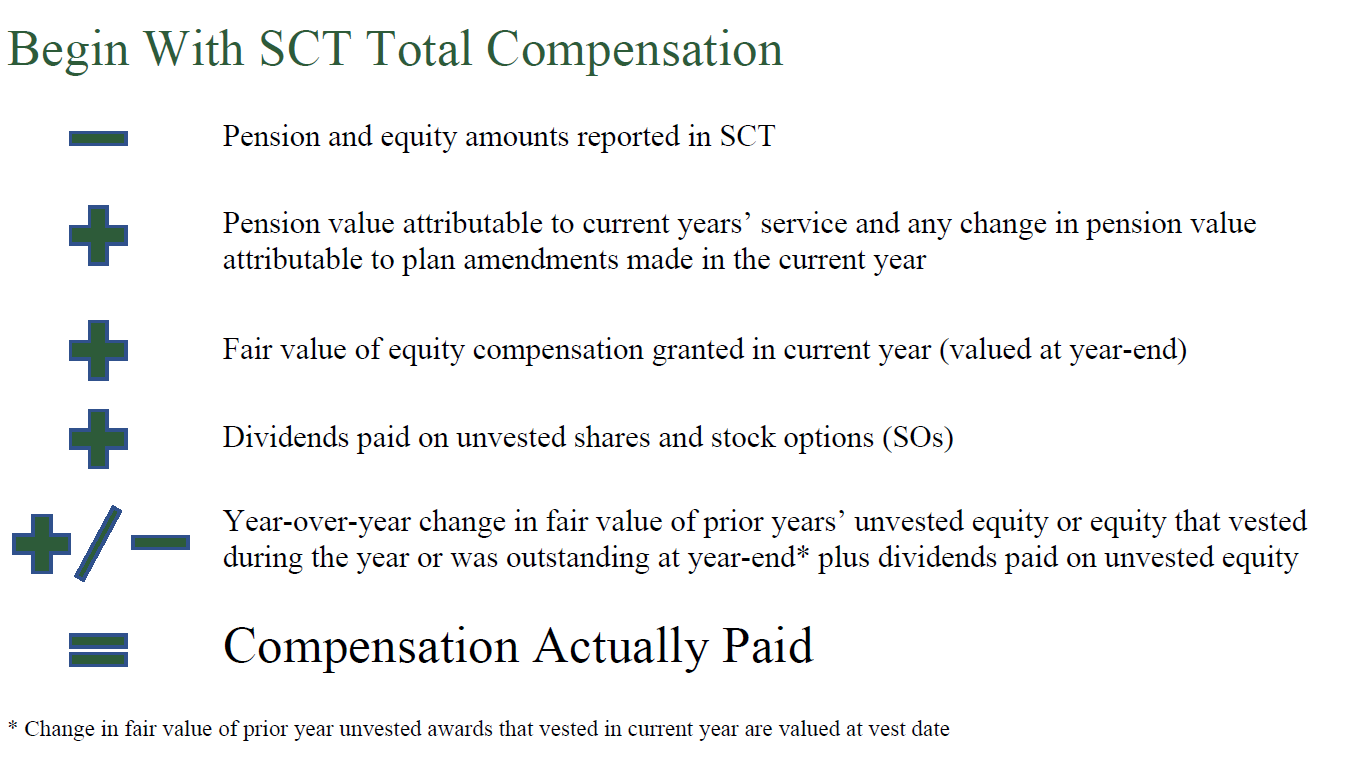

Calculating CAP

The disclosure of CAP was mandated by the Dodd-Frank legislation, but Congress left the SEC with significant discretion on how to define it for PVP comparisons. In the chart and discussion below, we have summarized the key components of CAP.

Fair Value of Equity Included in CAP

The amount of equity to be included in the calculation of CAP, according to the SEC, is intended to closely follow the concept of realizable pay.

The final rule requires that equity granted during the year be valued at year-end. In addition, year-over-year changes in the value of unvested equity granted in previous years are to be included in the calculation of CAP based on the year-end fair value or vesting date value if such vesting occurs during the year. Forfeitures of awards are included in the fair value calculation. This fair value requirement allows companies to report the value of equity at year-end, which corresponds to the stock price used in calculating TSR and is generally aligned with the current year financial measures.

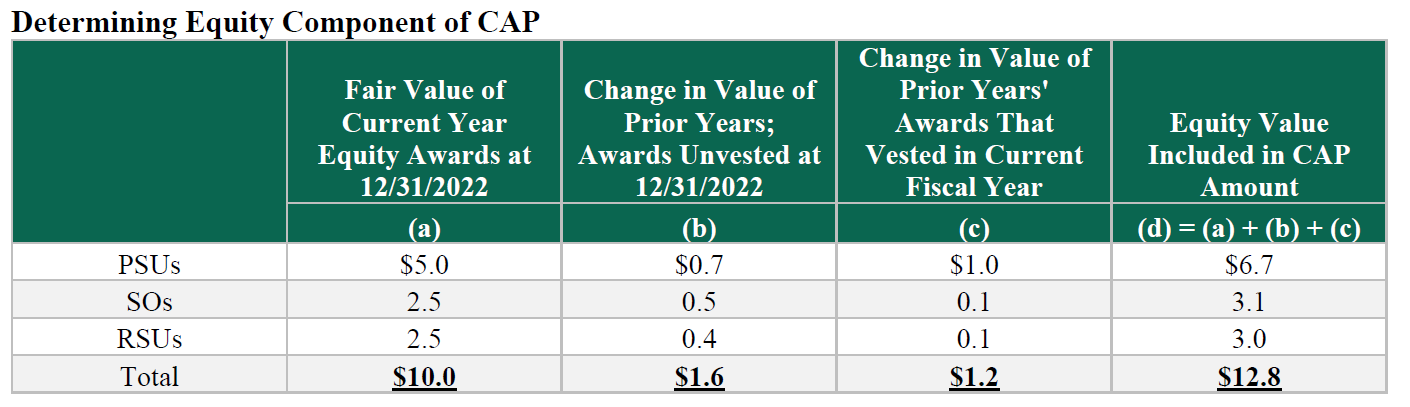

The following table provides an illustration of how the equity fair values are calculated. While not required by the SEC, it could be useful to include such a table in the PVP footnotes to help explain how the equity component of CAP was determined (in the same way perquisites and benefits are disclosed as a footnote to the Other Compensation column of the SCT). The example assumes a company grants 50% performance shares (PSUs), 25% stock options (SOs), and 25%-time vested restricted stock units (RSUs). The PSUs cliff-vest on the third anniversary of the grant date, whereas the SOs and RSUs vest ratably over the 3 years following the grant date. Performance criteria for the PSUs include 50% weighting based on relative TSR and 50% weighting based on cumulative operating income over the 3-year measurement period.

In the year of grant, each award is valued at year-end based on the valuation principles set forth in ASC 718 (column a). Thus, the PSUs that are linked to relative TSR will need to be valued using a Monte Carlo simulation with updated valuation assumptions, including the year-end stock price. The PSUs tied to the cumulative operating income metric will be valued based on year-end stock price and an updated assumption regarding the probability of such awards vesting. The SOs will be valued based on an updated Black Scholes or binomial model calculation based upon updated valuation assumptions (including the use of year-end stock price). The RSUs will be updated for the year-end stock price. It is understood that accrued dividends on such awards will also be included in the fair value calculation.

In addition, awards granted in prior years that remain unvested at year-end will be re-valued, and the increase or decrease in the fair value will need to be accounted for if such awards will be included in the current year CAP amount (column b).

Finally, awards that have vested (or are forfeited) during the current fiscal year will be valued as of their vesting date, and any increase or decrease from the prior year value will be included in the current year CAP (column c).

The sum of these components represents the equity value included in the CAP amount (column d).

Dividends Paid on Unvested Shares

The SEC also requires that dividends paid on unvested shares or SOs also be included in the CAP amount. As previously noted, accrued dividends are already included in the CAP amount.

Pension Amount to be Included in CAP

The SEC requires (1) “the actuarially determined service cost for services rendered by the executive during the applicable year” (the “service cost”) and (2) that the entire cost of benefits granted in a plan amendment during the covered fiscal year be included in CAP for the CEO and other NEOs. According to the SEC, these amounts are calculated each year for financial statement purposes and will not require significant effort to obtain the required information for the PVP table.

Executives Included in the PVP Table

The new SEC disclosure rules require the company to report SCT total compensation and CAP values for both the CEO and the average of the other NEOs included in the SCT. For some companies, these executives may change frequently, and the SEC requires that the SCT and CAP amounts included in the PVP table reflect the executives listed for that year’s proxy.

In the case of two CEOs in a particular year, the SEC requires companies report each CEO’s SCT compensation and CAP separately by adding additional columns to the table for each CEO. This is not permitted in the case of two CFOs or terminated executives that are included in the SCT, as the amount reported for other NEOs is based on the average of the reported NEO executives.

Calculation of TSR Values

The SEC specifies in the new rules that companies should report cumulative TSR in the same manner as required in Item 201(e) of Regulation S-K. Item 201(e) requires companies to assume an initial $100 investment in a company’s stock at the beginning of the disclosure period and to report the value at the end of each year based on stock price and the reinvestment of dividends in the company’s stock.

In transitioning to the new rules during the first year, the SEC requires companies to report 3 years of cumulative TSR as follows:

- 2022 cumulative TSR based on 2020-2022 results

- 2021 cumulative TSR based on 2020-2021 results

- 2020 cumulative TSR based on 2020 results

The 2023 and 2024 cumulative results will be added in subsequent years’ tables as follows:

- 2023 cumulative TSR based on 2020-2023 results

- 2024 cumulative TSR based on 2020-2024 results

Beginning in 2025 and every year thereafter, the cumulative TSR calculation will be reset each year, which may create comparability issues. For example, the cumulative TSR calculation for the 2025 fiscal year will assume that $100 was invested at the beginning of 2021 and will require that cumulative TSR be recalculated for 2021-2024 assuming 2021 is the base year (versus carrying over the cumulative TSR calculations for 2021-2024 from the prior year proxy statement). The changes in cumulative TSR will likely require additional explanation, as one year’s PVP table may show compensation that is fully aligned while a subsequent year may imply a lack of alignment because of the reset in the starting date for calculating cumulative TSR.

Peer Group TSR Calculations

The SEC will allow companies to use the peer group reported in the Item 201(e) disclosure or a peer group disclosed in the CD&A that is used for “compensation benchmarking purposes.” Item 201(e) requires the use of a published industry or line of business index. In addition, Item 201(e) also allows companies to use a company-selected peer group.

Although not entirely clear, we believe the final rules allow a company that discloses a relative TSR peer group in the CD&A to use that peer group in the PVP table. However, the peers’ TSR must be market cap-weighted when included in the PVP table.

Additionally, the SEC also requires that if the peer group or industry/business index group used to determine TSR changes between years, the company must provide an explanation for the change and provide a side-by-side comparison of TSR for the two peer sets over the applicable measurement period.

Additional Reporting and Disclosure Items

Companies will be required to explain the relationship between the CAP for the CEO and the average CAP of the other NEOs with respect to each of the performance metrics included in the PVP table (i.e., TSR, Net Income, and the designated CSM). In addition, companies must explain the relationship of the company’s TSR to its peers. This disclosure may be reported in a narrative or graphical format or a combination of the two.

Footnotes to the PVP table are required that identify the adjustments (exclusions and additions) to the SCT compensation amounts used to calculate CAP and the names of the other NEOs for each fiscal year.

Placing the PVP Disclosure Section in the Proxy

The SEC allow companies to include the PVP disclosure anywhere in the proxy. The SEC received several comments recommending this disclosure be integrated into the CD&A but decided against it because such placement “may cause confusion by suggesting that the registrant considered pay-versus-performance relationships in compensation decisions, which may or may not be the case.” The PVP disclosure must be tagged in inline XBRL, which—according to the SEC—will make the information easy to locate for small and large investors alike.

Special Exemptions and Rules Applicable to Selected Companies

Special rules are applicable to Smaller Reporting Companies, Emerging Growth Companies, foreign private issuers, registered investment companies, and companies that have recently gone public. With respect to Smaller Reporting Companies, they will only be required to disclose 3 years of data (2 years in the initial filing year). Additionally, such companies will not be required to report peer group TSR data, a CSM or list the three to seven most important performance measures. Emerging Growth Companies, foreign private issuers, and registered investment companies are exempt from all PVP disclosure requirements. Companies that have gone public recently are only required to report information for those years in which they were public entities.

Pay Governance’s Recommended Next Steps

In order to get a head-start on this extensive new disclosure requirement, companies may wish to consider some of the following activities:

- Begin compiling the cumulative TSR and CAP data for 2020 and 2021, as these amounts can be calculated now and are not dependent on 2022 year-end stock prices or equity awards granted or vested in 2022;

- Estimate the 2022 cumulative TSR and CAP data and prepare a proforma PVP table;

- Start analyzing the three to seven performance metrics that are driving pay outcomes for 2022 and identify from the list which metric(s) would be appropriate for inclusion as the CSM(s);

- Determine which peer group to use for TSR comparisons in the PVP table and evaluate the correlation of the company’s TSR with alternative indices/peer groups; and

- Begin work with the pension actuary regarding the retirement amounts to be included in the PVP table CAP amounts for 2020 and 2021 from both qualified and non-qualified retirement plans.

In preparing initial drafts of the PVP table and the accompanying narrative it may become clear that the CAP calculations and PVP table do not adequately capture the company’s pay for performance story. In these instances, it may be useful to consider a supplemental discussion to the PVP disclosure that presents an analysis of realizable pay and reporting of 3-year and 5-year performance and TSR data relative to peers.

Endnotes

1Pay Governance submitted comments in both 2015 and 2022, primarily about the definition of CAP and misalignment of the original timing of the CAP and performance periods. The SEC does reference our and other comment letters numerous times. The SEC acknowledges that the new definition of CAP was influenced by the comment letters.(go back)