Print

PrintDaniel Laddin is a founding partner and Louisa Heywood is an analyst at Compensation Advisory Partners. This post is based on their CAP memorandum. Related research from the Program on Corporate Governance includes Stealth Compensation via Retirement Benefits and Paying for long-term performance (discussed on the Forum here) both by Lucian A. Bebchuk and Jesse M. Fried.

A little more than 12 years after the 2010 Dodd-Frank Act was signed into law, the SEC has issued final rules on the topic. This was expected after the SEC re-opened the comment period on Pay Versus Performance disclosure in January. Intended to standardize the presentation of existing information related to the relationship between executive pay and company performance for investors, the final rules may also pose a new and significant burden on some companies with respect to their equity valuation processes and are substantially different from the proposed rules.

Dodd-Frank 953(a) requires issuers to show “…the relationship between executive compensation actually paid and the financial performance of the issuer…” The SEC’s definition of “compensation actually paid” is far removed from how many would interpret this term, particularly for equity-based compensation. It has decided to use an approach for equity-based compensation similar to “realizable pay” and essentially “marks to market” outstanding and unvested equity awards on a “fair value” basis from the grant date to the vesting date. This approach effectively accrues the equity value over the vesting period, with the heaviest impact on value likely to be in the year of grant. It is a fundamentally different approach from the proposed rules of 2015 where the value of equity would have been recognized in its entirety upon vesting, similar to existing definitions of “realized pay.”

The Pay Versus Performance requirements are meant to enable shareholders to directly compare executive compensation with company financial performance over a multi-year period. In the SEC’s view, assigning the burden of computing this relationship to investors is costly and inequitable. Therefore, the SEC implemented rules to standardize information presentation without, in its view, imposing unusual additional expense on issuers.

The new required disclosures are effective for filings at the next annual meeting for companies with fiscal years ending on or after December 16, 2022, so for calendar year companies, the next proxy will have to include the new disclosure.

CAP submitted comments to the SEC on the 2015 Proposed Rules, and our statement can be found here.

Overview of Final Rules under Section 953(a)

The final rules require companies to prepare a table disclosing compensation actually paid to the Named Executive Officers (NEOs) next to Summary Compensation Table totals and key metrics, over a five-year history (Exhibit 1). The metrics required to be disclosed in the table are as follows:

- Company’s indexed total shareholder return over the period [1]

- Indexed total shareholder return of peer group

- GAAP net income

- A financial metric of the company’s choosing

Exhibit 1

To supplement this tabular disclosure, companies will need to describe the relationship between compensation actually paid and each of the financial metrics included in the table, using a graphical and/or narrative approach. Finally, companies must provide a list of three to seven metrics they deem most important in making executive compensation decisions, which may include non-financial measures, if a minimum of three are financial metrics (Exhibit 2).

Exhibit 2

The rules require a three-year history in the proxy statement for fiscal year ended on or after December 16, 2022, a four-year history in the 2024 proxy and a full five-year history in 2025 and beyond. Smaller Reporting Companies (SRCs) will have pared-down requirements. The new Pay Versus Performance disclosure may be located anywhere in the proxy or information statement; it does not need to be incorporated into the Compensation Discussion & Analysis.

Pay Versus Performance Table

Compensation actually paid to the Principal Executive Officer(s) and other NEOs is intended to reflect a fair value assessment of compensation lined up with the most recent fiscal year. At a high level, the calculation for compensation for the PEO and other NEOs will be as follows:

- Cash compensation will likely mirror the Summary Compensation Table for most situations

- For companies with a defined benefit pension, the amount in the “change in pension value” will be replaced by the amount that is reflective of only the service cost for the respective year [2]

- And now for equity…. this is where it gets complicated!!! In contrast to the proposed rules, companies will need to revalue equity at the end of each year and report the change in value. Each in-process award will be “re-valued” (see details in exhibit) and vested awards will be valued based on the vesting date

- Awards with performance conditions deemed improbable to be achieved will be subtracted from the total, potentially giving shareholders insight into expected performance sooner than they would have received in the past since most companies did not disclose expected payouts until the end of the performance cycle

In response to sentiment that TSR does not capture the full financial picture of a company, and the reality that other metrics are consistently used in long-term performance share awards, the final rules require disclosure of TSR, TSR for the company-disclosed peer group, [3] GAAP Net Income and a third metric defined by the company. TSR is calculated as the value of a $100 fixed investment over the measurement period. The company-selected measure is intended to be a financial performance metric that the company finds represents the most important performance metric not already shown in the table for evaluating the link between compensation actually paid and company performance.

Key Performance Metrics Table

In the second required table, companies must report at least three and up to seven performance metrics that inform actual compensation decisions during the period. Three of the metrics must be financial performance metrics and any additional metrics may be non-financial measures if the company deems them among the seven most important measures impacting compensation actually paid. The company-disclosed metric in the pay versus performance table must be one of the metrics included in this table. The measures do not need to be ranked, a modification from the proposed rules in response to the complexity of determining rankings.

The SEC believes this disclosure will provide investors with visibility into which performance measures most strongly impact actual compensation paid and help investors assess whether compensation programs appropriately incent executives without undue burden or tedious complexity for issuers. With this list, the SEC aims to help companies reduce the risk of misrepresenting or providing an incomplete picture of pay versus performance alignment.

In practice, we anticipate that the listed metrics will align with the metrics used in the annual and long-term incentive awards. Companies will then have the opportunity to discuss the rationale for the metrics and how they influence compensation.

Description of Relationship between Actual Compensation and Financial Performance

Companies must substantiate the relationship between executive compensation actually paid and net income, and between executive compensation actually paid and the company-selected metric through graphs, charts and/or narrative text. Since GAAP metrics are used in the table and many companies use non-GAAP metrics in their compensation programs, this component is a key opportunity for issuers to provide compelling rationale for the measures and approaches used in their program that differ from GAAP net income.

Equity Valuation Under the Final Rules

The SEC has implemented equity valuation standards that present a departure from normal processes for most companies.

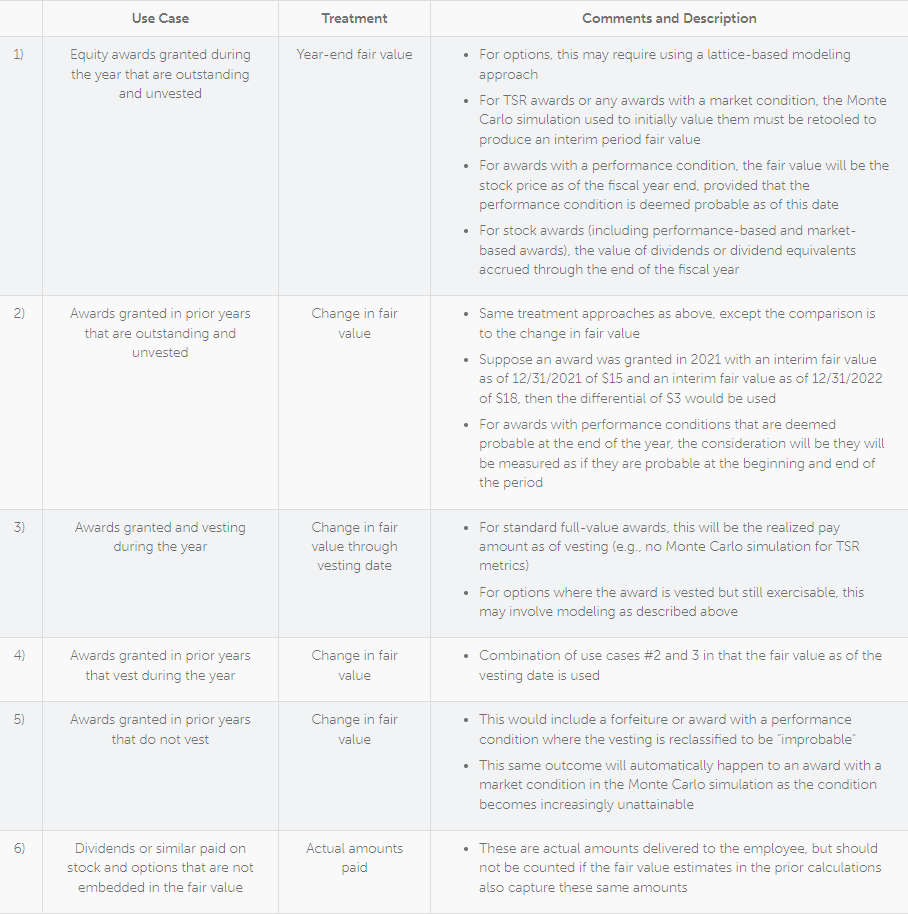

Under the Final Rules, equity awards are valued annually until vest to illustrate mid-cycle changes in fair value. The rules follow a syntax of addition and subtraction to produce a value of total equity earned by the executive that aligns with the financial performance measurement year. [4] Companies subtract the equity award values reported in the Summary Compensation Table and adjust based on the following:

- Fair value of equity awards granted, outstanding and unvested in the covered fiscal year as of the fiscal year end

- Change in fair value during covered fiscal year of awards granted in prior years that remain outstanding and unvested as of the end of the fiscal year

- For performance-contingent equity awards, fair value as of the end of the fiscal year based on probable outcome

- Change in fair value from end of prior fiscal year to vesting date for awards granted in prior years that vest in the covered fiscal year

- Fair value on date of vest for awards granted and vested in the same covered fiscal year

- Dollar value of any dividends or other earnings paid on stock or option awards in the covered fiscal year prior to vesting that are not otherwise reflected in fair value assessments of such awards

The implications of this methodology are aptly described in the following table produced by Equity Methods, a leading firm in the equity valuation space. See Equity Methods’ blog post for more detail on this topic and how companies should prepare for this disclosure.

Conclusion

Companies with fiscal years ending on 12/31/2022 will need to disclose this new information in their 2023 proxy statements. Given the complexity of the new rules and the requirement to provide supporting narrative disclosure that explains the relationship between compensation actually paid and financial performance, we recommend you begin the process of putting together the table now, recognizing you will not be able to finalize some items until after the end of 2022. We recommend that you do the following things between now and the end of the year:

- Identify data requirements for the new table (e.g., required equity valuations at the end of the year and at vesting dates, pension plan service cost, TSR, peer TSR, net income, etc.)

- Agree on peer group to be used for TSR

- Establish an approach to be used internally to determine the additional financial metric and the list of the three to seven most important financial metrics

- Reach out to internal/external advisors to help compile required information (e.g., finance/accounting, external equity valuation experts, actuaries)

- Develop initial mock-up of table with placeholders for year-end 2022 compensation and performance values

- Develop draft narrative disclosure describing the historical relationship between compensation actually paid and company performance

- Review draft disclosure with management and Compensation Committee

Given the newly required tables, companies will need to re-think the format of their disclosures to comply with the requirements and make the narrative easy to read for shareholders.

Endnotes

1Total shareholder return indexed to $100 invested at the beginning of the period the table. covers(go back)

2This will also include prior service cost if a plan is amended in such a way that impacts service cost in prior years.(go back)

3The peer group may be the same as the one used in the 10-K or an alternative peer group, such as the one used for benchmarking purposes. The rationale for the peer group and any changes year over year must be provided as well as the impact of changing the peer group on the relative TSR calculation.(go back)

4Equity awards granted prior to the base measurement year (prior to 2020) will not be included in the calculations.(go back)