Print

PrintEleazer Klein is a Partner and Brandon S. Gold and Abraham Schwartz are Associates at Schulte Roth & Zabel LLP. This post is based on a piece by Mr. Klein, Mr. Gold, Mr. Schwartz, Adriana Schwartz and Mario Kranjac. Related research from the Program on Corporate Governance includes The Long-Term Effects of Hedge Fund Activism (discussed on the Forum here); Dancing with Activists (discussed on the Forum here) both by Lucian A. Bebchuk, Alon Brav, and Wei Jiang; and Who Bleeds When the Wolves Bite? A Flesh-and-Blood Perspective on Hedge Fund Activism and Our Strange Corporate Governance System by Leo Strine.

This year, shareholder activism continued its post-COVID surge, with an increase in both the number of campaigns launched and the size of companies targeted. But while overall activity increased year-over-year, there was a decrease in the number of proxy fights, with more campaigns settling. It remains to be seen whether the onset of the universal proxy regime will reverse this (one-year) trend. Companies haven’t been waiting to find out, as the corporate weaponization of advance notice bylaws continued in 2021 and, based on recent events, seems poised to expand further in 2022. The continued slowdown in M&A activity is another trend to watch, as activist activity over the last two proxy seasons was impacted by an increase in M&A-related campaigns. On the topic of uncertainty, it is also worth noting that the effects of the SEC’s recently proposed amendments to Schedule 13D may have somewhat of a chilling effect on activist activity. Finally, ESG activism continued its march forward, but while it boasted a banner year in terms of aggregate activity, its success at the ballot box was questionable this year.

Overall Activist Activity Increased in 2022

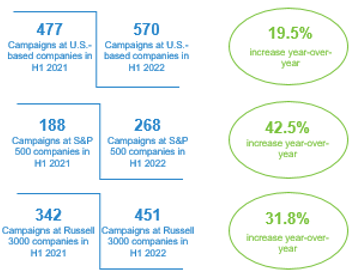

Despite, or perhaps fueled by, a volatile equity market environment, shareholder activism activity increased during the first half of 2022. In the U.S., activist campaigns and shareholder proposals increased 19.5% year-over-year. [1] Notably, H1 2022 saw a massive 42.5% increase in campaigns targeting S&P 500 companies. That this jump occurred in the wake of 2021’s marquee battle between Engine No. 1 and ExxonMobil Corporation, and Engine No. 1’s resounding victory, is no coincidence. The aura of invincibility historically associated with iconic and mega-cap companies has been pierced. When armed with well thought-out theses, stellar director candidates and credible plans for delivering shareholder value, activists can win at any company.

Not surprisingly, and consistent with this theme, campaigns at large-cap companies represented 51.9% of all U.S. campaigns launched in H1 2022, while mid-cap, small-cap and micro-cap companies represented 14.7%, 16.8%, and 16.4% respectively. [2]

While the established global activist fund managers remained active, first-time activists were a significant driver of campaign activity this year, accounting for 37% of all campaigns launched in H1 2022 at companies with a market capitalization of at least $500 million. [3] Looking ahead, the switch to the universal proxy regime, already underway, will introduce novel fight dynamics that may encourage even more new entrants to join the activism landscape.

U.S. Activism Activity

Campaign Objectives Remain Diversified

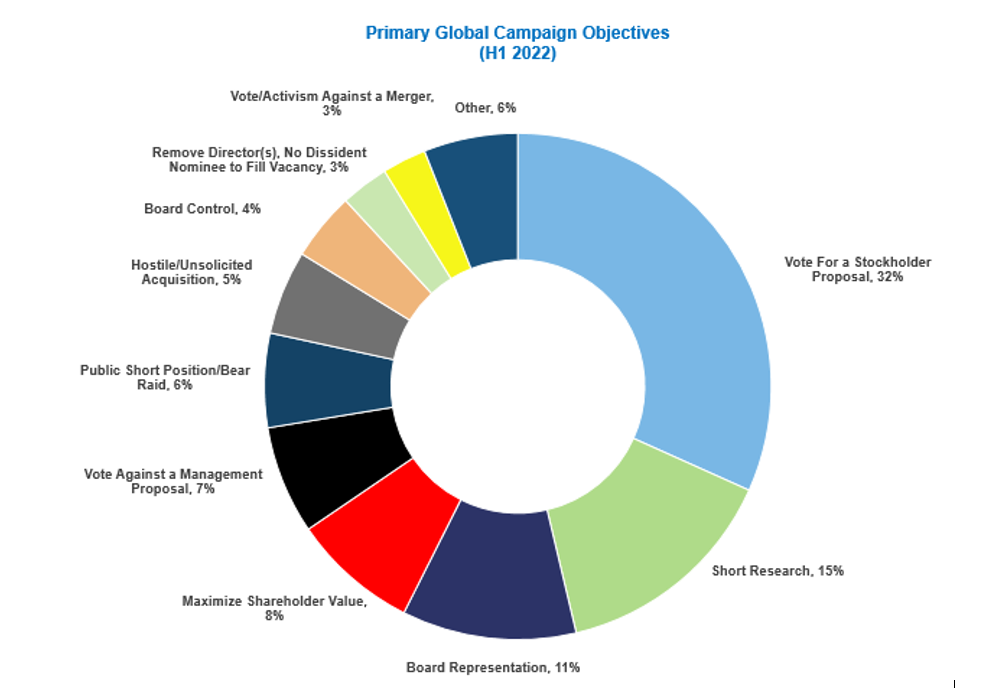

Campaigns in H1 2022 continued to represent a broad range of objectives. As could be expected, shareholder proposals represented the most common activist approach, totaling 32% of all activist-related activity. The number of 14a-8 proposal submissions thus far in 2022 (921) has already surpassed the full year total for 2021 (903). [4] In light of recently proposed amendments by the SEC that would limit certain substantive bases for companies to exclude 14a-8 proposals, it would not be surprising to see 14-8 proposals continue their growth trajectory in 2023 and beyond.

Outside of the 14a-8 context, board representation and shareholder value maximization continue to score among the top primary objectives for activists, representing nearly 20% of all campaign objectives.

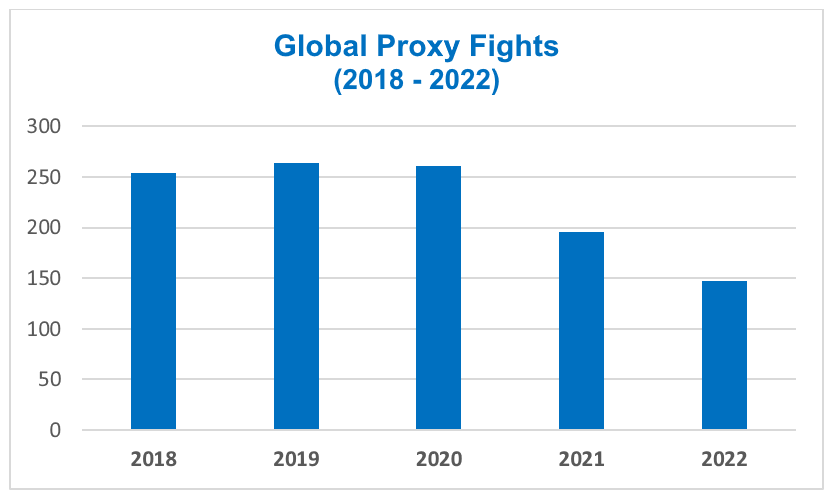

Fewer Proxy Fights During H1 2022

147 proxy fights have been launched year-to-date, down from 196, 261, 264 and 254 in 2021, 2020, 2019 and 2018, respectively. [5]

Part of this decrease can be attributed to an increase in settlement agreements, as there have been, year-to-date, 48 campaign settlement announcements globally, representing a 26.3% increase over the yearly settlement agreement total for 2021. [6] Market uncertainty and volatility were likely additional factors in the small number of proxy fights, as making a decision to ‘go all the way’ requires both a significant investment (of time and money) to run a protracted campaign and comfort with the illiquidity of having capital locked-up during the campaign, both of which could serve as deterrents to running proxy fights in the face of falling or erratic equity markets.

On a related note, settlement agreements continue to be the route of choice for securing board representation. Indeed, in H1 2022, of the 75 total board seats won at companies with a market capitalization exceeding $500 million, 91% were achieved through settlement agreements. [7]

Companies Weaponizing Advance Notice Bylaws

Originally designed to facilitate orderly shareholder meetings and election contests, advance notice bylaws, have, over the years, gradually morphed into a weapon for companies seeking to stifle shareholder dissent. Companies are increasingly alleging highly-technical disclosure deficiencies in nomination notices to block activist campaigns and threaten the viability of shareholder-driven agendas. The result has been the weaponization of advance notice bylaws by companies as a powerful defensive mechanism to preserve the status quo.

Companies now routinely amend their bylaws to make the process for shareholders to submit director nominations and proposals even more complex, expensive and time consuming. Two recent Delaware court decisions — Rosenbaum, et al. v CytoDyn Inc. et al. and Strategic Investment Opportunities v. Lee Enterprises — may only serve to encourage such behavior, as, in both cases, the Court upheld company rejections of nomination notices for purported failures to strictly comply with advance notice bylaws.

We have begun to see this play out in relation to the upcoming proxy season already. For example, certain public company bylaw amendments recently enacted purport to require activist fund managers to provide significant disclosures to the company regarding certain of a nominating shareholder’s limited partners and other private investors. Such bylaws are designed to discourage election contests and protect incumbent directors by increasing the costs to, and consequences of, shareholders seeking board representation.

Some additional recently enacted (and questionable) advance notice bylaws are focused on seeking confidential information regarding whether a shareholder has any plans to invest in and engage with unrelated companies in the future as well as requiring disclosure of any non-public engagements a shareholder may have had with other companies in years prior.

The M&A Slowdown Will Likely Affect Activism Levels in the Near Term

After reaching an all-time peak in 2021, global M&A volume has seen a notable decrease in 2022. In particular, Q3 2022 deal volume ($504 billion) represented a 52.9% decrease from Q3 2021 ($1.07 trillion) [8] and the second-lowest total deal volume of any quarter since Q1 2017. [9]

As the post-COVID activism landscape was impacted by a large number of M&A-related campaigns, it is not unreasonable to expect such activity to decline, as M&A-related activism is often focused on pushing for the abandonment or renegotiation of M&A agreements. This decline was already underway in 2022, as the number of M&A-related activist campaigns at companies with at least $500 million in market capitalization fell from 74 in H1 2021 to 42 in H1 2022, a 43% decline. [10]

Consistent with the recent downward trend in M&A generally, the number of M&A-related activist campaigns at companies with at least $500 million in market capitalization fell from a heady 74 campaigns in H1 2021 to a more ordinary 42 campaigns in H1 2022, representing a 43% decline [11] While M&A-related dissent remained a common campaign objective, representing 33.3% of campaign types in H1 2022, it fell below its historical average for 2018-2021 (41.6%).

Further, and with the M&A deals that are proposed in the coming year, activists may have more difficulty challenging deals as jittery shareholders weigh price and deal certainty against recent volatile equity markets and geopolitical instability. ISS opined that, in the current market, and considering rising macroeconomic headwinds, even deals with acquisitions prices that are well below recent valuations and peer sector transaction multiples, could be difficult for shareholders to turn down.

Whether the projected decrease in M&A-related activism will be filled elsewhere remains to be seen.

The Effect of Proposed Schedule 13D Amendments

Recent SEC rule proposals concerning beneficial ownership may also have an effect on campaign levels by making it more difficult for activists to profit off of their investment. For starters, shortening the deadline for an initial Schedule 13D filing from ten days to five days would limit the amount of stock an activist could acquire before public disclosure and therefore also limit its ability to benefit from any post-announcement ‘bump’. Similarly, the SEC has proposed a new rule, Rule 10B-1, which would require next day public disclosure of security-based swap positions that exceed certain thresholds. Disclosures could be required under this rule even where an activist has a purely economic position (and no voting rights) and alert market participants to an activist’s investment sooner than under the current disclosure regime.

In a similar vein, some of the other proposed changes broaden the scope of who is considered a beneficial owner for 13D reporting purposes, deeming holders of certain derivative securities settled exclusively in cash to be beneficial owners, even though holding the derivative security does not convey voting or investment power over the covered class of equity security. This would also have the effect of requiring an activist to become public sooner than it may have wanted, thereby curbing its economic upside, which could factor into whether an activist decides to run a campaign in the first place.

Another proposed 13D rule change, and the one that may be the most consequential, revolves around the question of how to define a “group” for beneficial ownership reporting purposes. Schedule 13D requires disclosure of the identity of a group and aggregates the group’s shares for purposes of the 5% beneficial ownership trigger. Historically, under SEC rules and relevant case law, a group has historically been deemed to be present when two or more shareholders “agreed” to act together with respect to a company’s securities. The proposed amendments, however, reflect the SEC’s contention that “an agreement is not a necessary element of group formation.” These changes would create uncertainty among shareholders regarding the facts and circumstances that constitute acting as a group and could have a chilling effect on the ordinary course communications among shareholders that are vital to an activist’s due diligence prior to launching a campaign.

ESG Outlook

Some commentators felt that ESG activism was poised for a strong 2022 proxy season following Engine No. 1’s victory at ExxonMobil as well as the capital inflows to ESG-focused funds in the second half of 2021. And while the number of environmental and social shareholder proposals and campaigns increased considerably in 2022, ESG campaign activism outcomes were mixed.

For starters, the success rate of environmental shareholder proposals significantly dropped year-over-year, from 18% in 2021 to 9.5% in 2022 so far. In ESG related board fights, activists suffered some high-profile defeats at the ballot box. Carl Icahn’s animal welfare-driven contest at McDonald’s Corporation was rejected by fellow shareholders, in the wake of which he abandoned a similarly themed campaign at The Kroger Company. The campaign at Huntsman Corporation, which included focused criticism of the company’s ESG record, lost at the ballot box, as well.

Underscoring this is that fact that institutional investors, whose support is pivotal to a campaign’s success, have made it clear that ESG proposals will be carefully scrutinized. Notably, BlackRock opted to oppose several of this year’s climate-related proposals on the basis that they “are more prescriptive or constraining on companies and may not promote long-term shareholder value.” [12]

While, as mentioned above, the SEC has proposed amendments to Rule 14a-8 that would make it more difficult for companies to exclude ESG-focused shareholder proposals, proposing shareholders should keep in mind that fellow shareholders will not provide carte blanche support for these proposals. A strong supporting statement will be necessary to gain the support of many of the large institutional investors.

Looking ahead, we believe the number of ESG campaigns and proposals will continue to rise and that, as shareholders modulate their ESG approach to match investor preferences, so will their track record of success.

Endnotes

1FactSet. (go back)

2FactSet. (go back)

3Lazard (H1 2022 Review of Shareholder Activism (lazard.com)). (go back)

4ISS Voting Analytics as of Oct. 16, 2022. (go back)

5FactSet. (go back)

6FactSet. (go back)

7Lazard. (go back)

8S&P Global ((Global M&A By the Numbers: Q3 2021 | S&P Global Market Intelligence (spglobal.com))). (go back)

9Bloomberg (ANALYSIS: All M&A Market Segments Saw Q3 Drop in Deal Volume (bloomberglaw.com)). (go back)

10Lazard. (go back)

11Lazard. (go back)

12BlackRock (https://www.blackrock.com/corporate/literature/publication/commentary-bis-approach-shareholder-proposals.pdf). (go back)