Print

PrintKai H. E. Liekefett and Derek Zaba are Partners, and Leonard Wood is a Senior Managing Associate at Sidley Austin LLP. Related research from the Program on Corporate Governance includes The Long-Term Effects of Hedge Fund Activism (discussed on the Forum here) by Lucian A. Bebchuk, Alon Brav, and Wei Jiang; Dancing with Activists (discussed on the Forum here) by Lucian A. Bebchuk, Alon Brav, Wei Jiang, and Thomas Keusch; and Who Bleeds When the Wolves Bite? A Flesh-and-Blood Perspective on Hedge Fund Activism and Our Strange Corporate Governance System (discussed on the Forum here) by Leo E. Strine, Jr.

The activism landscape in a post-pandemic world continues to evolve. This year has been characterized by a sharp increase in campaigns relative to recent years, a heightened focus on M&A transactions and increased presence of environmental, social and governance (ESG) themes. Amid all of this evolution, the recent implementation of the universal proxy card regime represents a step function change in activism campaigns, the impact of which is only beginning to be felt.

Post-Pandemic Rebound

Activism significantly rebounded in 2022, with total campaigns through Q3 up 39% over the same period last year, already nearly reaching the total for full-year 2021. In the United States, total campaigns have already surpassed the total for full-year 2021, with Q3 campaigns up 133% compared to last year. In addition, the increase appears to be accelerating, with Q3 seeing a 52% increase in global activism campaigns over the prior year, continuing the trend in both Q1 and Q2. Technology companies have recently been the most frequent targets, accounting for 22% of all activism campaigns launched in Q3. [1]

The increase in activism is due to several factors. Market conditions have been favorable for activists and characterized by a stock market that severely punishes any missteps, significantly lower valuations, and increased volatility. These factors have facilitated the increase in activist engagements, particularly in sectors that have been hit hardest by the market downturn. In addition, activist funds have larger amounts of capital to deploy than in recent years and any remaining constraints on activism from the pandemic have dissipated, creating a perfect storm for activism.

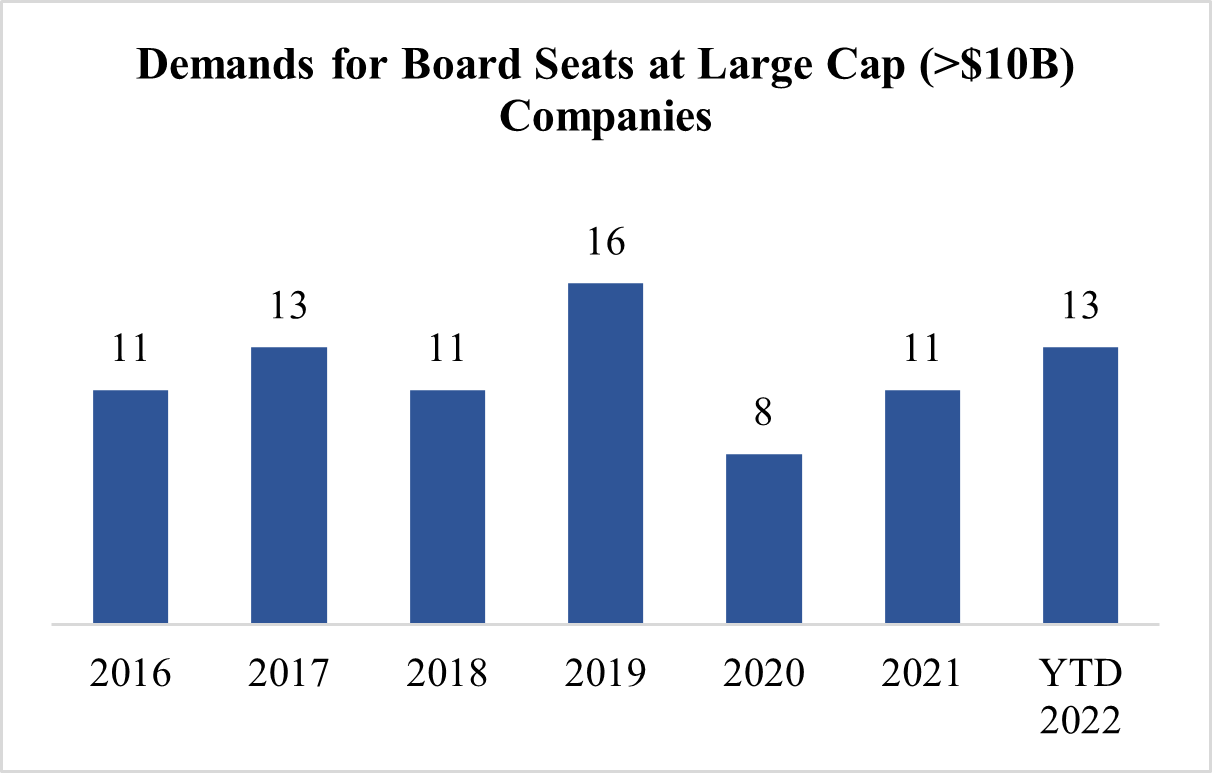

These factors have also made the acquisition of a meaningful stake in large-cap companies within reach for many small- and mid-sized activists who are looking for downside protection and lower volatility in the months ahead. Large-cap companies are on pace this year for seeing the highest number of demands for board seats.

In addition, the 2022 proxy season was an extension of recent years where companies were more successful at the ballot box than activists. The incumbent boards of U.S. companies successfully defeated all activist nominees at the ballot box in 65% of proxy fights in 2022 and 63% in 2021. This follows a 2017-2020 average success rate of 47%. [3] However, interpreting these results as activists enjoying fewer “successes” today than they have historically is misguided. Shareholder activism campaigns that culminate in a shareholder vote are, by far, the exception and not the rule. Extrapolating to conclusions based on that small dataset doesn’t reflect the bigger picture: non-proxy contest resolutions that result in “cooperation agreements” or remain undisclosed are far more prevelant. In our experience, companies and their advisors have been more selective about letting campaigns progress into full-blown proxy fights only when they have confidence that there will be strong shareholder support.

In part, this is fueled by companies increasingly prioritizing connectivity with their shareholders, particular with stewardship teams within large institutional investors.

“Sell First, Think Later”

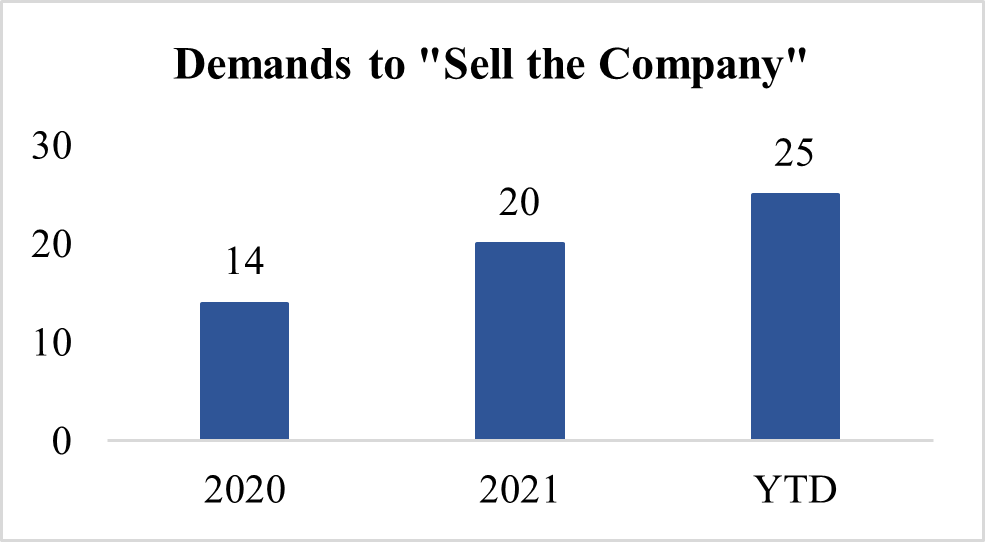

Along with the increase in total activism campaigns and demands at large cap companies, 2022 has seen an increase in M&A-related demands by activists. M&A demands were included in 32% of campaigns in Q1, 39% of campaigns in Q2 and 48% of campaigns in Q3, with no signs of slowing down. In fact, public demands for a sale of the company in 2022 through the date of publication already exceed the totals for both full-year 2021 and full-year 2020 [4]. This also does not include situations where the ultimate goal of an activist is to sell the company but, for tactical reasons, the activist chooses not to make such a goal widely known:

Despite market weakness relative to the post-pandemic boom in equity markets, activism focused on the sale of a company continues with good reason, with lower valuations providing greater potential for securing a significant percentage premium off of the prevailing share price. Furthermore, the sale of a portfolio company is a quicker way for an activist to generate returns than attempting to implement a broader operational thesis.

The ESG-ing of Activism

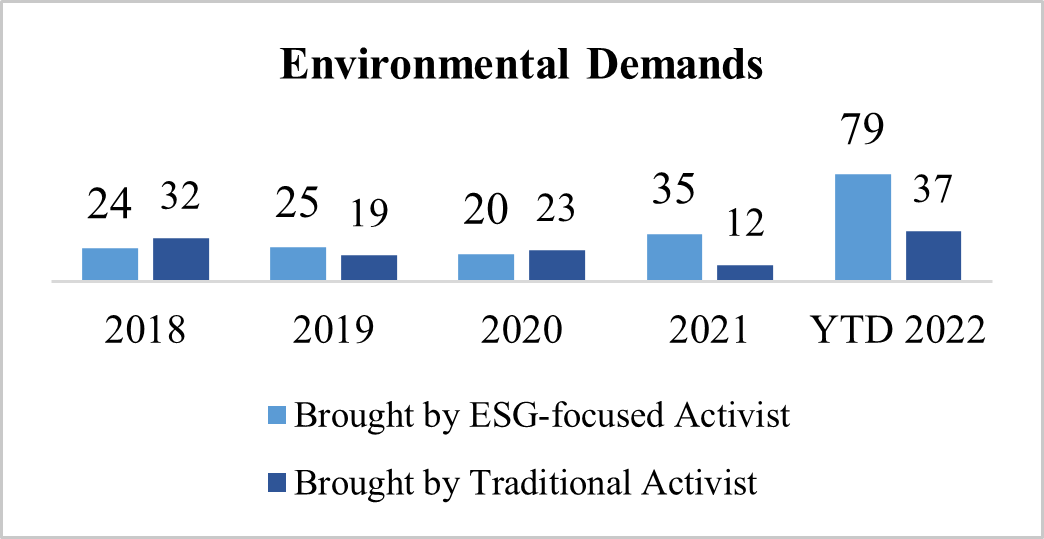

The “Me Too” movement, the social unrest of 2020 and the pandemic accelerated existing trends relating to ESG. This in turn elevated the discussion about the role of the company with respect to its shareholders and other stakeholders like its employees and the communities it operates in to an extent not seen before. With this wave came a substantial increase in activism focused on “environmental” and “social” prongs. Many traditional activists incorporated these themes into their campaigns opportunistically while some other investors ran campaigns purely focused on the key ESG practices and policies of target companies.

ESG-focused activism continued in 2022, with high-profile public campaigns targeting large- and mega-cap companies, and many more engagements occurring behind the scenes. As these issues have gained mindshare from many institutional investors and proxy advisory firms, companies have increased the attention they focus on these issues. While we expect ESG trends to continue, ESG activism has recently faced backlash from an “anti-ESG” contingent that is emerging. This includes a handful of states that have barred state pensions from investing in funds that target or incorporate ESG considerations into their investment and voting policies. Nevertheless, ESG trends are likely to continue with environmental and social themes increasingly favored by traditional activists.

Looking Forward: All Eyes on the Universal Proxy Rule

The implementation of the universal proxy regime continues to be the focal point for many as we enter into the next proxy season. The new rules, which apply to contested elections at public companies after September 1, 2022, require both company and a nominating shareholder to include all nominees up for election on their respective proxy cards. Historically, shareholders voting by proxy had to choose between selecting from the list of company nominees or the list dissident nominees. Under the new rules, shareholders can select from the combined pool of director nominees, allowing them to “mix and match” from the two slates. The impact on proxy contests will be significant.

Under the new regime, the qualifications and experiences of each director nominee will be a more critical component of the campaign. Activists will now being able to pit strong candidates directly against weaker incumbents, which may encourage voting for activist candidates even if they have not proved their “case for change” to an extent that shareholders would have previously elected to vote on the “dissident card”. In line with this, we expect directors with significant vulnerabilities (e.g., long tenure, age, perceived lack of relevant skills) to be subject to greater scrutiny and personalized attacks. Both Institutional Investor Services (ISS) and Glass Lewis have alluded that directors perceived as weak by shareholders and advisory firms will be particularly vulnerable. ISS predicted that, under the new system, boards will be “far less able to shield their weakest contributors.” [6] Glass Lewis suggested similarly that the new rules “will potentially make all incumbent directors on a board more vulnerable for replacement, whether they are specifically identified as a targeted director by the activist or not.” [7]

One implication is that activists are better positioned to make smaller gains with higher probabilities of success, regardless of whether they make a strong case for change at a company. We may already be seeing this take effect. There was a notable increase in early activist outreach to public companies in Q3 that has continued into Q4. We anticipate this will continue into the 2023 proxy season.

The new regime also creates a potential new opportunity for non-traditional activists such as special interest groups and private individuals with specific concerns. Because a universal proxy card requires a company to list all director candidates on its own proxy card, a nominating shareholder will no longer need to physically mail its own proxy materials multiple times. The cost savings will enable shareholders with smaller budgets—such as environmental activists, trade unions, non-governmental organizations and, of course, perennial gadflies—to run less costly issue-based proxy campaigns to nominate special interest candidates.

For more information, please visit Sidley’s Universal Proxy Card Resource Center.

Endnotes

1Source: Lazard, Q3 2022 Review of Shareholder Activism.(go back)

2Source: Activist Insight. Campaigns at U.S. companies by year of campaign announcement date.(go back)

3Source: FactSet.(go back)

4Source: Lazard, Q3 2022 Review of Shareholder Activism.(go back)

5Source: Activist Insight. Campaigns at U.S. companies by year of campaign announcement date.(go back)

6Source: Institutional Shareholder Services, “The UPC Era Begins” (September 2, 2022) https://www.issgovernance.com/library/the-upc-era-begins/.(go back)

7Source: Glass Lewis, “The Implementation, and Implications, of Universal Proxy Cards” (September 1, 2022) https://www.glasslewis.com/the-implementation-and-implications-of-universal-proxy-cards/.(go back)