Print

PrintAmit Batish is Director of Content at Equilar, Inc. Related research from the Program on Corporate Governance includes The Perils and Questionable Promise of ESG-Based Compensation (discussed on the Forum here) by Lucian A. Bebchuk and Roberto Tallarita; and Paying for Long-Term Performance (discussed on the Forum here) by Lucian A. Bebchuk and Jesse M. Fried.

As 2022 nears its close, companies across Corporate America are preparing for 2023 and what’s developing to be one of the most anticipated proxy seasons in recent years. In August 2022, the United States Securities and Exchange Commission (SEC) officially adopted its “Pay Versus Performance” rules, following several rounds of comments and proposals. The new rules require public companies to disclose information reflecting the relationship between compensation actually paid to a company’s named executive officers (NEOs) and the company’s financial performance.

The implementation of the SEC’s requirements—combined with constant pressure from investors and other key stakeholders to align executive pay with corporate performance—are compelling companies to begin the preparation of their proxy statements much earlier than usual. Nevertheless, companies will often rely on trends from the previous year in preparation of their disclosures. In this post, Equilar examines 2022 Say on Pay voting trends and the prevalence of pay for performance disclosures over the last five fiscal years to provide a sense of the current executive compensation landscape.

The concept of pay for performance has long been advocated by investors, particularly given the influence they have on pay packages. Following the 2008 financial crisis, the United States Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act in an effort to improve accountability in the financial system. As part of Dodd-Frank, several statutes were designed specifically targeted at executive compensation, including those related to Say on Pay and pay for performance. Since its adoption in 2011, Say on Pay has played a critical role in providing investors a platform to voice discontent over executive compensation misalignment with performance. However, despite the influential voice investors hold, the vast majority of executive pay packages are approved by shareholders.

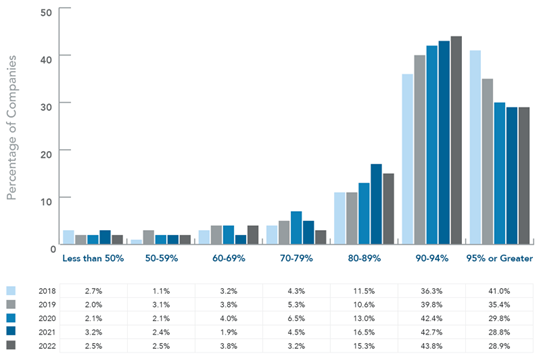

According to Equilar research, an overwhelming 97.5% of the Equilar 500—the 500 largest U.S. companies by revenue—passed Say on Pay in 2022. Nonetheless, a shifting trend is emerging—28.9% of Equilar 500 companies passed their Say on Pay vote with 95% support or greater, down 29.5% from 40.1% in 2018. While investors have grown more critical and weary of pay packages in recent years, 72.7% of Equilar 500 companies still passed their Say on Pay votes by a margin of 90% or greater in 2022, with under 3% of companies of failing in four of the last five years (2021 being the lone exception when 3.2% of companies failed).

Figure 1: Say on Pay Results (Equilar 500)

Meanwhile, higher thresholds set by proxy advisors pose another challenge for companies when it comes to Say on Pay. According to Institutional Shareholder Services (ISS)’s proxy voting guidelines, when a Say on Pay proposal receives less than 70% support, the firm will conduct a qualitative review of the compensation committee’s responsiveness to shareholder opposition at the next annual meeting. In 2022, 8.8% of Equilar 500 companies received less than 70% support, and that figure has increased from 7% in 2018.

Of course, the bigger question is whether or not the SEC’s new Pay Versus Performance rules will have any impact on Say on Pay results in the coming years. While it’s too soon to draw any specific conclusions, it’s in the best interest of companies to begin preparing how to tell their pay story. Say on Pay votes are typically based on the total value of an executive’s pay package as disclosed in the Summary Compensation Table for the given year; however, shareholders will often be interested in pay for performance alignment and compensation actually paid to executives at specific companies.

“Companies that have struggled on Say on Pay or are anticipating a struggle with Say on Pay are going to find that the new pay for performance disclosure probably doesn’t help them and will be looked at as well,” said Joe Yaffe, Partner and West Coast Chair, Executive Compensation and Benefits at Skadden, during a recent Equilar webinar covering the new rules.

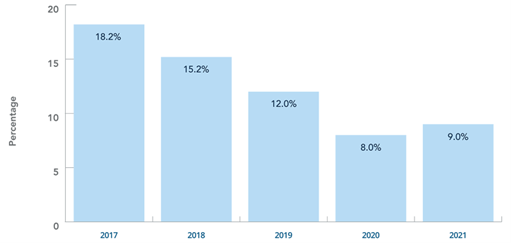

Nevertheless, another key disclosure on the topic that is worth examining is the prevalence of pay for performance disclosures. According to a review of the Equilar 100—a subset of the Equilar 500—just 9% of companies disclosed a pay for performance graph in their proxy statement in 2021. While this is up one percentage point from 2020, the figure is down overall by nearly 50% since 2017 when 18.2% of companies disclosed a pay for performance graph. The percentage of companies that disclosed a pay for performance graph also declined from 2017 to 2020, before slightly rebounding in 2021. Of course, given the SEC’s August announcement, the prevalence of disclosures around pay for performance is certainly expected to accelerate in the coming years.

Figure 2: Prevalence of Pay for Performance Graph Proxy Disclosures (Equilar 100)

Ultimately, the executive compensation landscape will be greatly impacted by the new rules implemented by the SEC. The onus is on companies to clearly and effectively tell their pay story and ensure that they meet the demand of investors, who will undoubtedly scrutinize the rigor of performance metrics tied to compensation plans and any problematic pay practices.