Print

PrintEric W. Hilfers, Jonathan J. Katz and Michael L. Arnold are Partners at Cravath, Swaine & Moore LLP. This post is based on a Cravath memorandum by Mr. Hilfers, Mr. Katz, Mr. Arnold, John W. White, Elad L. Roisman, and Matthew J. Bobby. Related research from the Program on Corporate Governance includes Stealth Compensation Via Retirement Benefits and Paying for Long-Term Performance (discussed on the Forum here) both by Lucian A. Bebchuk and Jesse M. Fried.

On August 25, 2022, the Securities and Exchange Commission (“SEC”) adopted a new disclosure rule to implement the “pay versus performance” disclosure requirements of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the “Dodd-Frank Act”). In particular, the new rule will require companies to quantify and describe (in both tabular and narrative format) the relationship between compensation actually paid to executives and company financial performance across multiple metrics.

The rule is complex and certain features, including newly required compensation calculations (including the new concept of executive compensation “actually paid”), will require issuers to expend significant resources on compliance. This obligation will be particularly burdensome in the near term given that most companies will have to provide the “pay versus performance” disclosures in their upcoming 2023 proxy statement and some of the initial disclosures will require information for the previous three years.

Historical Background and Commissioners’ View

Section 953(a) of the Dodd-Frank Act added Section 14(i) to the Securities Exchange Act of 1934 directing the SEC to adopt a rule requiring companies to disclose information about the relationship between executive compensation and financial performance. The SEC first proposed a “pay versus performance” rule in April 2015 and received significant feedback. After languishing for years as a proposal, the comment period was reopened in January 2022 and the SEC adopted the final rule in late August in a 3-2 vote. The final rule establishes a new Item 402(v) of Regulation S-K, which prescribes disclosures required in various filings.

SEC Chair Gary Gensler and Commissioners Caroline Crenshaw and Jaime Lizárraga voted in favor of the final rule. Their statements indicated that they supported the rule largely because they believed it will provide transparency, clarity and comparability to investors about executive pay. [1] Among the reasons for their support, Chair Gensler highlighted that the rule “makes it easier for shareholders to assess a public company’s decision-making with respect to its executive compensation policies”; [2] Commissioner Crenshaw noted that the “disclosures give investors insight into how performance measures impact executive compensation, in order to allow investors to better understand how boards pay their company executives”; [3] and Commissioner Lizárraga noted that “[c]ombined with other Dodd-Frank Act financial stability provisions, this rulemaking will reduce the likelihood of future taxpayer bailouts.” [4]

Commissioners Hester Peirce and Mark Uyeda dissented on the final rule. Commissioner Peirce’s concerns included that: (1) the costs of the final rule outweighed the benefits, (2) the final rule “will elicit costly, complicated, disclosure of questionable utility”, and (3) the rule could “distort how public companies compensate executives and how investors evaluate companies’ compensation decisions”. [5] Commissioner Uyeda raised concerns that: (a) the comment period reopening was too short; (b) the SEC should have reproposed the rule with updated data and analysis and cited the SEC’s avowed focus on obtaining robust economic data as set forth in the SEC’s 2022 Congressional Budget Justification, the Administrative Procedure Act, the Paperwork Reduction Act and the Regulatory Flexibility Act; and (c) the Commission did not accurately capture the costs of the rule. [6]

Important Things to Know

Below are questions highlighting issues of note for companies, directors and advisors about the new disclosure requirements:

- Which companies are affected? All registered issuers (other than emerging growth companies, registered investment companies and foreign private issuers) are required to provide this new disclosure. Smaller reporting companies can provide a scaled-back version of the disclosure.

- Which filings are affected? The new disclosure is required in all proxy and information statements that include Item 402 executive compensation disclosure for fiscal years ending on or after December 16, 2022. Thus, companies with calendar fiscal years will generally be required to include the new disclosures in their 2023 annual proxy statements. The information is not required in filings other than proxy and information statements, such as IPO registration statements, where Item 402 information is generally required.

- What time period does the disclosure cover? Information required to be provided in the new tabular disclosure (see Q4 below) covers the last five fiscal years, although for the first year that this new disclosure is provided (generally next year), only the last three fiscal years are required, with an additional year added over the next two years of disclosure.

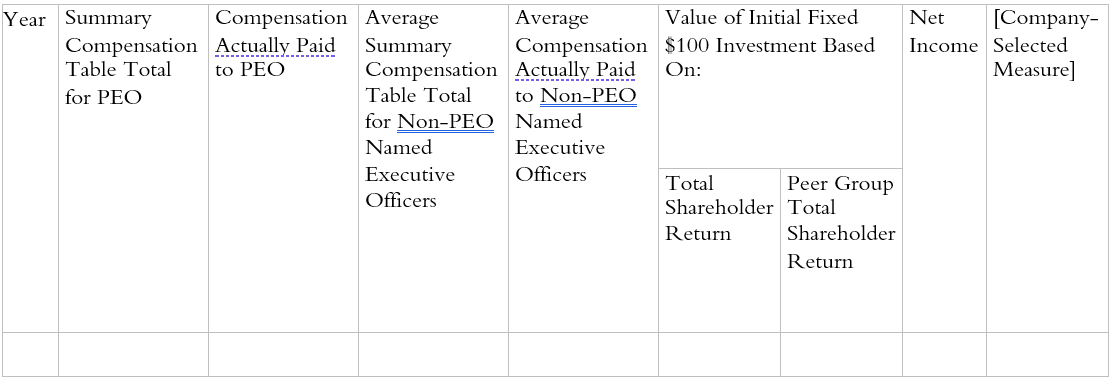

- What new tabular disclosure is required? The following new table is required, with a separate row for each covered year (see Q3 above). The table is intended to provide investors with standardized data on executive compensation in a manner that is easier to link to company performance than the amounts already disclosed in the Summary Compensation Table (“SCT”) and Compensation Discussion and Analysis (“CD&A”). Thus, the table includes existing SCT amounts, as well as a new calculation of “actually paid” compensation (see Q6 below for discussion of this new term). To provide investors with standardized data on company performance, the table also requires companies to calculate their cumulative total shareholder return (“TSR”) and the TSR of a peer group for each covered year. Similarly, companies must also include a calculation of their generally accepted accounting principles (“GAAP”) net income and an additional financial performance measure selected by the company (see Q8 below). Unlike other existing “principles-based” compensation disclosure obligations, the table must generally be included in the manner specified by the new rule in order to enable comparisons between companies.

Pay Versus Performance

5. What additional narrative disclosure is required to accompany the Pay Versus Performance table? In addition to the table, companies must describe (in graphic, narrative or a combined format) the relationship between compensation “actually paid” to the Principal Executive Officer (“PEO”) [7] and average actual compensation paid to non-PEO Named Executive Officers (“non-PEO NEOs”) and each of (i) the company’s cumulative TSR, (ii) its GAAP net income and (iii) a “Company-Selected Measure” (see Q8 below). A comparison of the company’s TSR and peer group TSR must also be included. In addition to the new table and associated narrative descriptions, further information about relevant financial measures is also required (see Q10 below).

6. How is executive compensation “actually paid” calculated? Executive compensation “actually paid” is based on the SCT total compensation figure, but adjusted to reflect the change in actual value of stock awards (e.g., stock options and restricted equity units) and defined benefit pension benefits during the covered year. [8] Calculating the “actually paid” value of equity awards is likely to require significant effort by issuers and their advisors as these values are not currently tracked in this manner by most issuers.

7. How are the TSR numbers calculated? The cumulative TSR for each fiscal year is measured over a period running from the last trading day before the covered fiscal year began through and including the end of the covered fiscal year, and is calculated assuming reinvested dividends. The closing price at the measurement point is then converted into a fixed investment of one hundred dollars in company stock (or the stocks of the peer group), so that the numbers included in the column are easily comparable. The TSR applicable to each entity in the peer group must be weighted according to the respective market capitalization of the entity at the beginning of each measurement period.

8. What is the “Company-Selected Measure”? The “Company-Selected Measure” is a financial performance measure selected by the company as “the most important financial performance measure” used to link compensation actually paid to company performance during the most recently completed fiscal year. If the Company-Selected Measure is not a financial measure under GAAP, additional disclosure is necessary to describe how the amount is calculated based on audited financial statements. Given the rule’s implementation date, most companies should start thinking now (working with the compensation committee, its independent compensation consultant and other advisors) about the Company-Selected Measure for 2022. This will likely have implications for future Company-Selected Measures and stakeholder engagement.

9. What constitutes the company’s “peer group” for this disclosure? What if the peer group changes? Companies may use either the same peer group used for purposes of Item 201(e) of Regulation S-K (the stockholder return performance graph generally included in an issuer’s Form 10-K) or the peer group used in the CD&A. [9] For purposes of the TSR calculations described in Q7 above, if a different peer group is used in a subsequent fiscal year, a footnote with an explanation for the change is required, as well as a comparison of the company’s cumulative TSR with the cumulative TSR of both the previous peer group and the new peer group.

10. What additional information on financial measures is required? Companies must provide a tabular, unranked list of generally no less than three and no more than seven of the most important financial performance measures used to link executive compensation and company performance during the most recently completed fiscal year. Companies may also include non-financial performance measures in the unranked list, as long as at least three financial metrics are included. Different lists may be provided for the PEO and non-PEO NEOs.

11. Where is the disclosure required to be located? Can additional disclosures be included? Will this disclosure need to be tagged for interactive data purposes? There is no required location for the pay versus performance disclosure. Our expectation is that companies will include the disclosure within the CD&A generally or at the end of the proxy statement as an additional section. The mandatory disclosure described above may be supplemented with additional tables and narratives, similar to other required disclosures. Registrants will be required to use Inline XBRL to tag their pay versus performance disclosure.

12. Will the new disclosures impact Say-on-Pay votes or other shareholder engagement? For the time being, our expectation is that the disclosure will not affect Say-on-Pay votes, since proxy advisors and similar institutions already calculate “realized” and “realizable” pay and compare that to financial metrics. However, proxy advisors and similar institutions may incorporate the numbers required by the new disclosure in the future. Issuers may wish to carefully consider whether to incorporate environmental, social and governance (“ESG”) measures as a non-financial performance measure if it aligns with their general ESG shareholder engagement strategy.

Given the extensive nature of the additional disclosure, in particular the calculations relating to compensation “actually paid” and TSR, companies should begin working with advisors now to prepare this disclosure. As noted above, this is particularly true because the initial disclosures will require information for three years and some of these years can be calculated now in advance. Detailed background about the amendments, including the SEC’s responses to certain public comments, and the text of the final rule can be found at the SEC’s website at www.SEC.gov/rules/final/2022/34-95607.

Endnotes

1See Chair Gary Gensler, “Statement on Final Rule Regarding Pay Versus Performance”, available at https://www.sec.gov/news/statement/gensler-statement-pay-vs-performance-082522; see Commissioner Caroline A. Crenshaw, “Late Summer Sunshine: Statement on the Adoption of Pay Versus Performance”, available at https://www.sec.gov/news/statement/crenshaw-statement-pay-vs-performance-082522; see Commissioner Jaime Lizárraga, “Statement on Pay versus Performance”, available at https://www.sec.gov/news/statement/lizarraga-statement-pay-vs-performance-082522.(go back)

2See Chair Gary Gensler, “Statement on Final Rule Regarding Pay Versus Performance”, available at https://www.sec.gov/news/statement/gensler-statement-pay-vs-performance-082522.(go back)

3See Commissioner Caroline A. Crenshaw, “Late Summer Sunshine: Statement on the Adoption of Pay Versus Performance”, available at https://www.sec.gov/news/statement/crenshaw-statement-pay-vs-performance-082522.(go back)

4See Commissioner Jaime Lizárraga, “Statement on Pay versus Performance”, available at https://www.sec.gov/news/statement/lizarraga-statement-pay-vs-performance-082522.(go back)

5See Commissioner Hester M. Peirce, “Neither Pay nor Performance”, available at https://www.sec.gov/news/statement/peirce-statement-pay-vs-performance-082522.(go back)

6See Commissioner Mark T. Uyeda, “Statement on the Final Rule Related to Pay Versus Performance”, available at https://www.sec.gov/news/statement/uyeda-statement-final-rule-related-pay-versus-performance-082522.(go back)

7If an issuer has more than one PEO in a covered year, disclosure of each PEO’s SCT total compensation and compensation “actually paid” is required, which means that two additional columns must be included in the table above.(go back)

8The specific amounts deducted or added, as well as the names of the PEO and non-PEO NEOs and applicable years, must be included in a footnote. If the assumptions used in valuing stock awards differ materially from those disclosed as of the grant date, such assumptions must be included in footnotes as well.

The final rule states that “Under the final rules, the definition of executive compensation actually paid for a fiscal year is, generally, total compensation as reported in the Summary Compensation Table for that year (i) less the change in the actuarial present value of pension benefits, (ii) less the grant-date fair value of any stock and option awards granted during that year, (iii) plus the pension service cost for the year and, in the case of any plan amendments (or initiations), the associated prior service cost (or less any associated credit), and (iv) plus the change in fair value of outstanding and unvested stock and option awards during that year (or as of the vesting date or the date the registrant determines the award will not vest, if within the year) as well as the fair value of new stock and option awards granted during that year as of the end of the year (or as of the vesting date or the date the registrant determines the award will not vest, if within the year). Adjustments (i) and (iii) with respect to pension plans will not apply to SRCs because they are not otherwise required to disclose executive compensation related to pension plans.”(go back)

9Unless the peer group is a published industry or line-of-business index, the members of the peer group must be disclosed in a footnote.(go back)