Print

PrintNicole Hallas is Manager of Research Analytics, Kayla Coello is a Research Analyst and Sarah Keohane is a Data Analyst at Audit Analytics. This post is based on an Audit Analytics memorandum by Ms. Hallas, Ms. Coello, Ms. Keohane, and Ms. Watson.

Executive Summary

Introduction

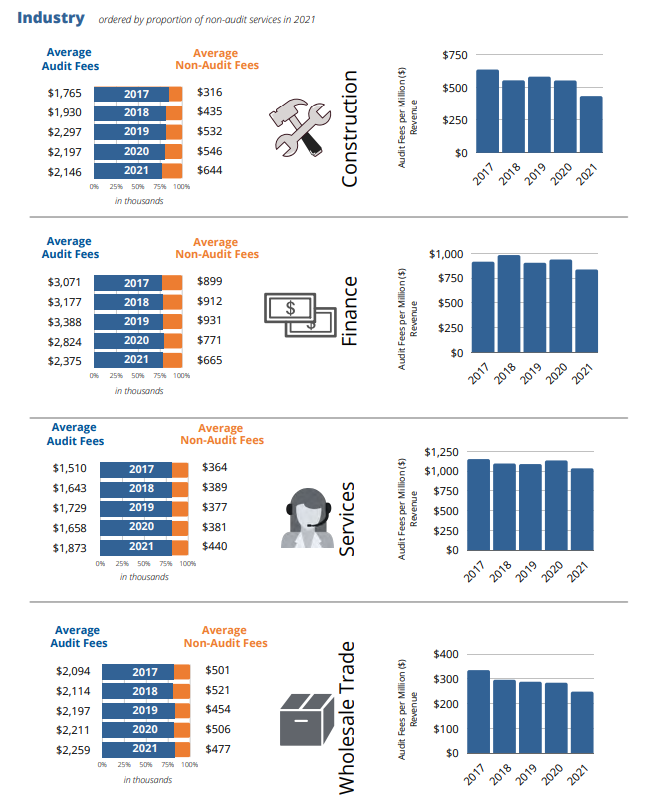

Analyzing fees paid to external auditors provides insights into audit risk and auditor independence.

Audit fees are an indicator of audit complexity and risk. Higher risk audits require more auditor resources (hours, personnel, specialists, etc.) to reduce audit risk to an acceptable level. Analyzing fees by industry, company size, and location can provide insight into the level of risk and

auditor effort various sectors of publicly listed companies entail.

This type of analysis is particularly relevant when comparing companies

that require an external auditor assessment on internal controls over

financial reporting. These assessments provide significant insight into an

entity’s risk and can require extra auditor effort. In “Abnormal Audit Fee and Audit Quality,” researchers found that “audit quality declines as actual audit fees depart from ‘normal fee’ levels.” [1] When analyzing year-over-year changes in audit fees, significant deviations from the norm can be identified and analyzed with overall market events, such as new regulations, enforcement actions, and filer status changes that affect the audit risk level and auditor effort.

Non-audit fees can also provide relevant information to financial statement users. Auditor independence is a primary focus of regulators, and as Anita Bandy, associate director in the division of enforcement at the SEC, stated, “[a]uditors play a fundamental role in protecting the reliability and integrity of financial reporting and must ensure that non-audit services do not come at the cost of their independence on audits of public companies.” [2] Worldwide, much discussion has centered around the effect that significant non-audit services have on external auditors’ level of independence. In response, the US and many European countries have enacted regulations to restrict the type of non-audit services allowed and, in many cases, the amount auditors can be paid for allowable non-audit services.

”The independence of the auditor, in both fact and appearance, is foundational to the credibility of the financial statements.” – Paul Munter SEC Acting Chief Accountant [3]

In this report, we seek to shed insight on audit and non-audit fee trends in the US market and explore the underlying drivers of these changes to promote a deeper understanding of the financial market.

Background: Audit and Non-Audit Fee Trends

Over the past 20 years, significant activity in the regulatory markets, both in the US and internationally, has affected audit fee and non-audit fee trends.

Throughout the 2000s, different aspects of the Sarbanes-Oxley Act of 2002 (SOX) went into effect. The initial ban on certain types of non-audit services had immediate implications for both audit and non-audit fees. Audit firms were no longer allowed to perform the following non-audit services [4] :

- Bookkeeping or other services related to the accounting records or financial statements of the audit client;

- Financial information system design and implementation;

- Appraisal or valuation services, fairness opinions, or contributions-in-kind reports;

- Actuarial services;

- Internal audit outsourcing services;

- Management functions or human resources;

- Broker or dealer, investment adviser, or investment banking services;

- Legal services;

- Expert services unrelated to the audit

Requirements to maintain and assess internal controls came into effect shortly after. All companies would need management to review the effectiveness of internal controls. Companies meeting the definition of accelerated or large accelerated filers would also have to obtain an auditor attestation on the effectiveness of internal controls.

In 2012, the Jumpstart Our Businesses Startups Act (JOBS Act) was signed into law, and the “emerging growth company” category of filers was created. [5] The new designation allowed companies to issue less extensive annual reports and exempted them from obtaining an auditor’s attestation of internal controls.

A succession of new accounting standards became effective over the past three years. In 2018, ASC 606 Revenue from Contracts with Customers went into effect. In 2019, ASC 842 Leases went into effect. And most recently, in 2020, ASC 326 Financial Instruments – Credit Losses went into effect. However, the standard was delayed due to the pandemic and was further delayed for smaller companies. These regulations required companies to make changes to existing accounting and financial reporting procedures.

With these changes, auditors must update prior-year audit testing and implement new procedures to determine if the companies’ new policies adequately meet the standards. Often, these changes take time to implement. Increases in audit complexity result in additional effort on the part of the external auditors. In response, during these periods of adjustment, auditors may need to increase audit fees.

Most recently, the SEC amended the definition of an accelerated filer during 2020.6 Companies with revenues less than $100 million and public float of between $75 million and less than $250 million no longer qualify as an accelerated filer. This exempts hundreds of companies from the auditor attestation on the effectiveness of internal controls.

Trends In Audit and Non-Audit Fees

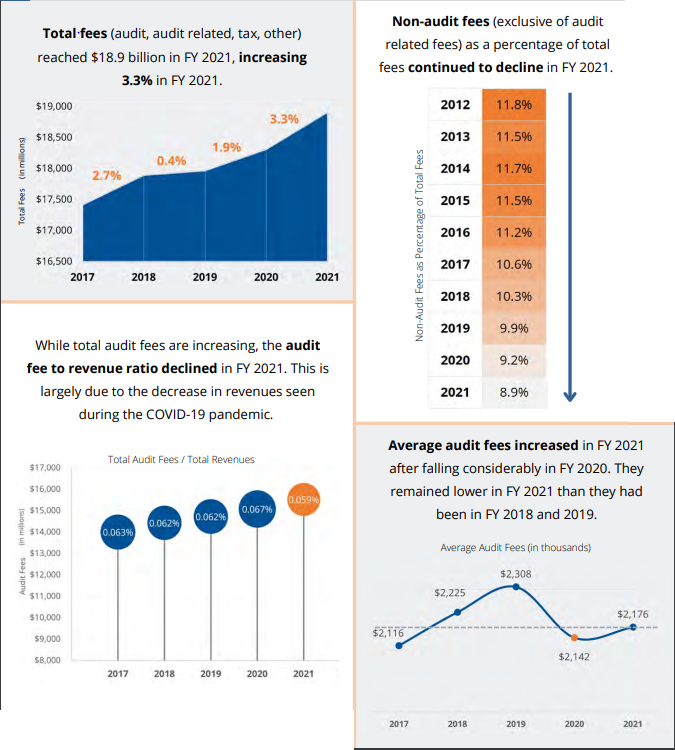

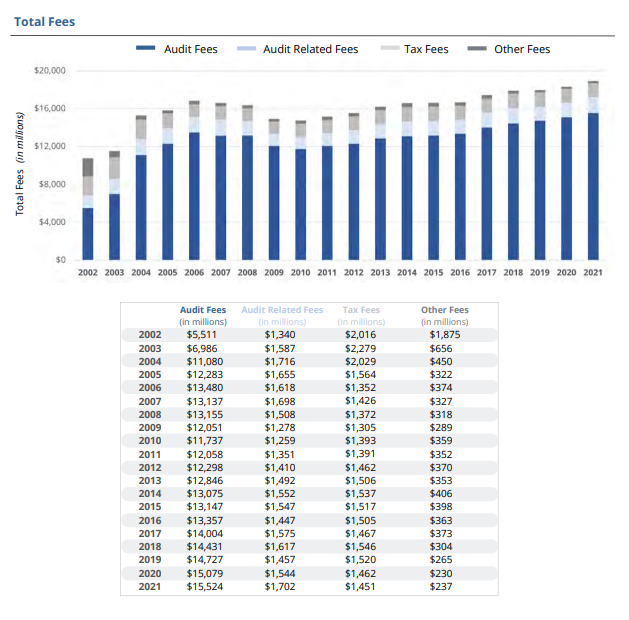

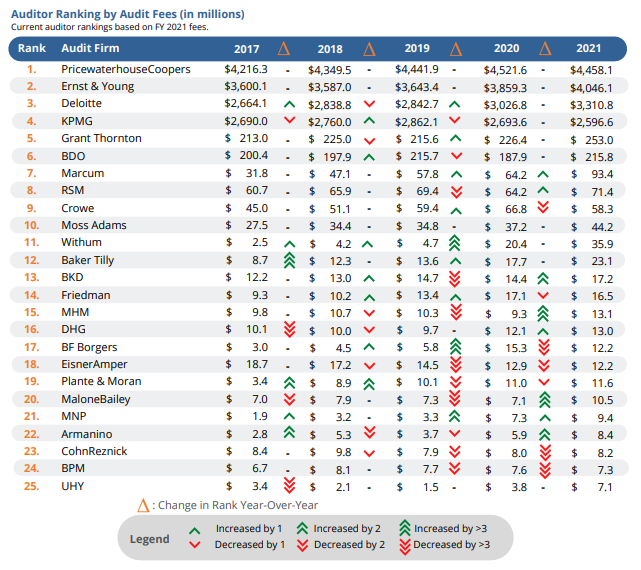

Total fees reached $18.9 billion in FY 2021, increasing 3.3% from 2020. This increase aligns with an increase in SEC registrants in the population between 2020 and 2021.

Independently, audit fees increased 2.9%, while audit-related fees increased 10.2%. Total tax fees decreased by 0.8%, continuing the downward trend that began in 2018. The total amount of other/miscellaneous fees increased by 3.0%.

The average amount that SEC registrants paid for an audit increased to $2,176,000 in 2021. Average audit-related fees increased to $239,000. Average tax fees decreased to $203,000, the lowest point since 2014, aligning with the lower overall amount paid in tax fees. The average amount of fees classified as “other” remained stable.

Factors Leading to Decrease in Average Audit Fees Between 2019-2020

- Impacts on audit work from the COVID-19 pandemic.

- An influx of special purpose acquisition companies (SPACs), which pay relatively low audit fees due to their lack of operations. This drove down the average fees by increasing the number of public companies.

- A change in filer status definition reclassified hundreds of companies from accelerated filers to nonaccelerated filers. Non-accelerated filers are not required to have their internal controls audited but remain in the company population, further driving down the average.

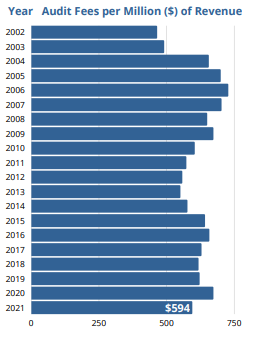

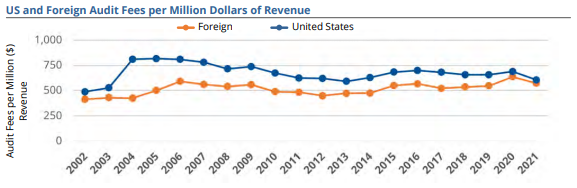

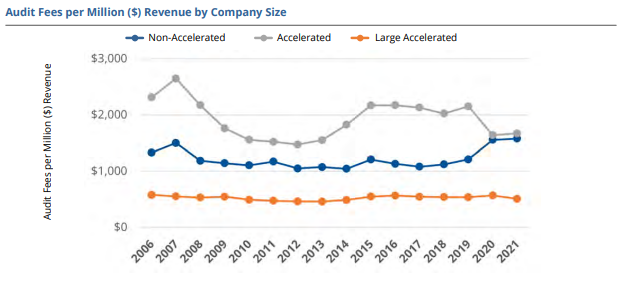

Audit fees per million dollars of revenue fell following the financial crisis of the late 2000s. Though fees never fell to the levels seen before the implementation of SOX.

An increase in audit fees per revenue was seen in 2020, largely due to the COVID-19 pandemic reducing revenues.

Audit fees per million dollars of revenue declined in 2021. However, this was expected, as revenues returned to pre-pandemic levels.

Impact of Sarbanes-Oxley Act (SOX) on Audit Fees

Audit fees grew while non-audit fees shrank rapidly following the enactment of the Sarbanes-Oxley Act of 2002 (SOX). SOX made several impactful changes. These changes included a requirement (SOX 404) to have internal controls assessed by management and assured by the independent audit firm. They also added limitations on the types of services that can be performed by a company’s independent audit firm.

The additional audit work required by SOX 404 resulted in audit fees per million dollars of revenue increasing by over 34% between 2003 and 2004.

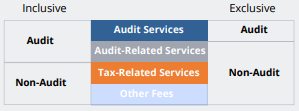

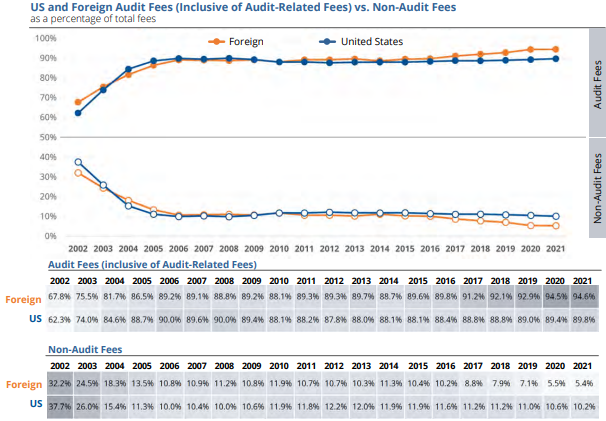

This report reviews fees paid to the independent audit firms of SEC registrants. When discussing audit fees and non-audit fees, services are grouped in two ways: inclusive and exclusive. The category ‘audit fees inclusive’ includes both audit services and audit-related services. The category ‘audit fees exclusive’ only includes audit services. When unidentified, audit fees are exclusive of audit-related fees.

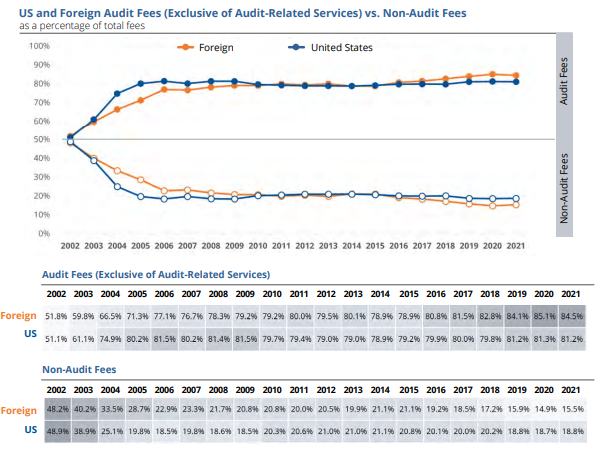

Non-audit fees, exclusive of audit-related fees, have declined – as a percentage of total fees – from approximately 36% in fiscal year 2002 to a low of 9% in fiscal year 2021.

The decline is due to a global focus on restricting certain non-audit services to safeguard auditor independence. With these changes, non-audit fees, consisting of tax and other/miscellaneous fees, have remained relatively consistent, hovering between 10-12% of total fees since 2005.

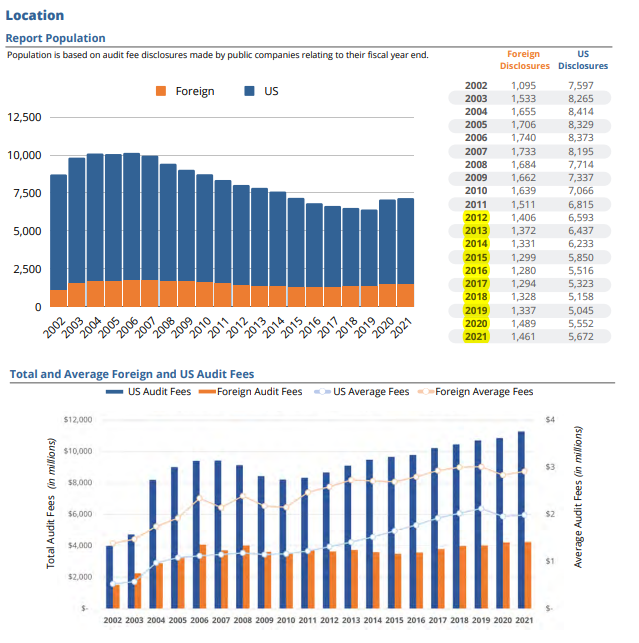

FY 2021 saw average audit fees increase to $1.9 million and $2.9 million for US and foreign companies, respectively.

Average audit fees for US and foreign companies have been mainly increasing since the implementation of SOX. This trend of increasing audit fees was reversed in 2020 due to several anomalies, including an influx of SPACs that pay lower than average audit fees and impacts due to the pandemic.

Impact of Location on Average Audit Fees

Average international audit fees tend to be higher than US fees because international companies listed in the US are, on average, larger than US companies listed in the US.

Effect of EU Directive 2014/56/EU on Audit Fees

Internationally, the largest recent event affecting audit and nonaudit fees was EU Directive 2014/56/EU. Effective in 2016, it outlined specific prohibited non-audit services and enforced a cap on permitted services provided by the auditor.

Due to the directive, permitted services were not allowed to exceed 70% of the average amount of the fees paid in the previous three years for the statutory audit. [7] This regulation is likely the driver of the divergence in non-audit fees after 2016.

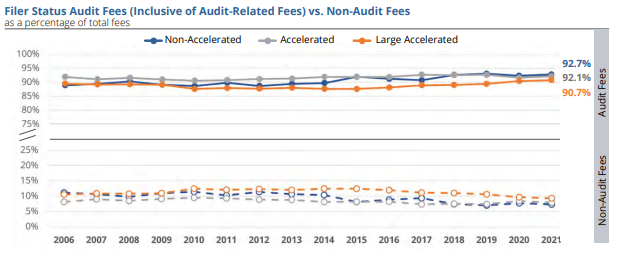

Audit fees inclusive of audit-related services increased as a percentage of total fees for both foreign and US registrants in FY 2021. Conversely, non-audit fees minimally decreased from 5.5% to 5.4% for foreign registrants, the lowest percentage of total fees recorded for foreign registrants. Non-audit fees for US companies decreased from 10.6% to 10.2%, the lowest amount of non-audit fees as a percentage of total fees since 2008.

Both US and foreign companies experienced a decrease in audit fees per million dollars of revenue between FY 2020 and 2021. Overall, US and international audit fees per million dollars of revenue are at their closest point since before the implementation of SOX.

Revenue increased at a faster rate than total audit fees for companies in both locations year-over-year. Total audit fees grew by 0.8% for foreign companies, while revenue grew by 12.0%. Similarly, total audit fees grew by 3.8% for US companies while revenue grew by 18.2%.

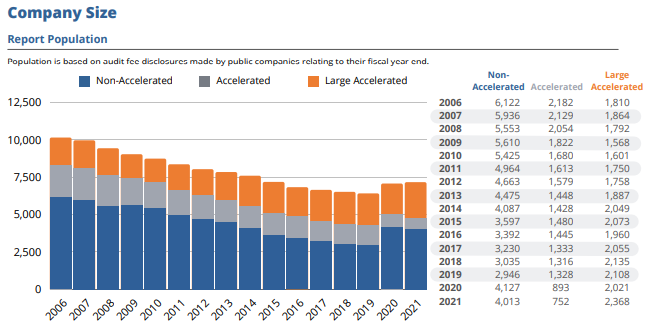

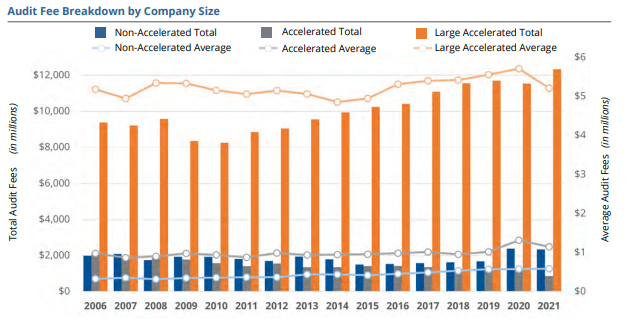

Aggregate audit fees for non-accelerated filers decreased 1.5% in FY 2021 after experiencing a substantial increase in 2020 due to the filer status change that reclassified accelerated filers to non-accelerated filers. Average audit fees for non-accelerated filers increased by 1.3%.

Aggregate audit fees for accelerated filers decreased 26.5% in FY 2021. This is the biggest drop in total audit fees since FY 2006 and is largely due to the decrease in the overall accelerated filer population. Average audit fees decreased by 12.7%.

Audit fees for large accelerated filers increased 6.9% in FY 2021. Conversely, average audit fees for large accelerated filers decreased by 8.8%.

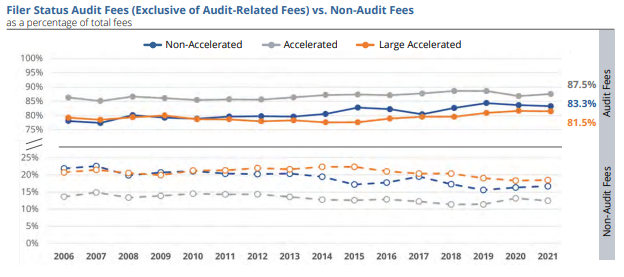

Audit fees exclusive of audit services decreased as a percentage of total fees for non-accelerated filers and large accelerated filers and increased for accelerated filers in FY 2021.

Conversely, non-audit fees increased from 16.4% to 16.7% for non-accelerated filers and from 18.4% to 18.5% for large accelerated filers. Non-audit fees for accelerated filers decreased from 13.2% to 12.5%.

Since the implementation of SOX, the percentage of fees paid for audit-related and non-audit services has hovered near 10% for companies of all sizes. FY 2021 saw the lowest percentage of audit-related and non-audit services as a percentage of total fees for all filer statuses.

In FY 2021, the percent of total fees attributed to audit-related and non-audit fees decreased across all filer statuses. For non-accelerated filers, audit-related and non-audit fees decreased from 7.7% of total fees to 7.3%. For accelerated filers, audit-related and non-audit fees decreased from 8.4% to 7.9%. For large accelerated filers, audit-related and non-audit fees decreased from 9.6% to 9.3%.

After a slow decline following the completion of the implementation of SOX 404, accelerated filers began to see audit fees per million dollars of revenue increase in the mid-2010s. In FY 2020, however, fees fell sharply due to the reclassification of hundreds of accelerated filers as non-accelerated filers. This also increased the audit fees per million dollars of revenue for non-accelerated filers.

In FY 2021, audit fees per million dollars of revenue for non-accelerated and accelerated filers were consistent with each other. Audit fees per million dollars of revenue have remained consistent for large accelerated filers since FY 2006, though slightly declined in FY 2021.

Database Overview and Methodology

Overview

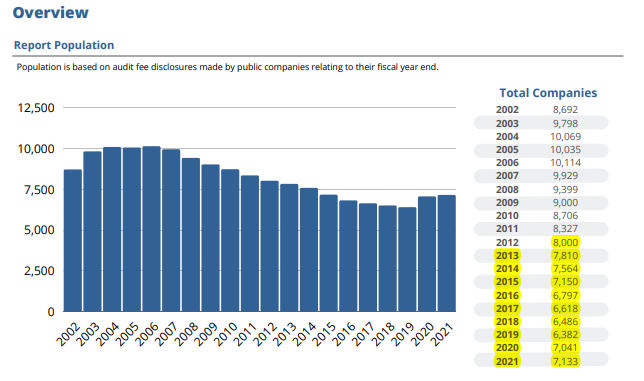

The Audit Analytics SEC Audit Fees database can be used to benchmark audit fees, track significant changes in audit fees, and monitor non-audit fee spend. This database makes it easy to identify audit fees, auditrelated fees, tax-related fees, and other fees paid to a company’s independent audit firm. Data covers all ’33 and ’34 Act filers since 2000.

Data is updated daily and can be accessed through the Audit Analytics website, data feeds, or through the Wharton Research Data Services (WRDS).

Methodology

Fee information comes from Forms 10-K, 20-F, 40-F, and DEF 14A. The analysis excludes subsidiaries and affiliates that are included in a parent’s audit fees, ’40 Act filers, trusts, and companies that reported $0 in audit fees. Years refer to the fiscal year the fee information relates.

Companies that do not identify as large accelerated or accelerated filers are classified as non-accelerated filers. This includes non-accelerated filers, smaller reporting companies, and companies that do not disclose a filer status. Companies without a determinable filer status are excluded.

Endnotes

1https://meridian.allenpress.com/ajpt/article-abstract/31/3/1/54552/Abnormal-Audit-Fee-and-Audit-Quality?redirectedFrom=fulltext(go back)

2https://www.sec.gov/news/press-release/2019-184(go back)

3https://www.sec.gov/news/statement/munter-audit-2021-10-26(go back)

4https://www.sec.gov/news/press/2003-9.htm(go back)

5https://www.sec.gov/education/smallbusiness/goingpublic/EGC(go back)

6https://www.sec.gov/corpfin/secg-accelerated-filer-and-large-accelerated-filer-definitions(go back)

7https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:32014R0537&from=EN(go back)