Print

PrintMerel Spierings is a Researcher for the ESG Center at The Conference Board. This post is based on her Conference Board memorandum, in partnership with ESG analytics firm ESGAUGE and compensation advisory firm Semler Brossy. Related research from the Program on Corporate Governance includes The Perils and Questionable Promise of ESG-Based Compensation (discussed on the Forum here) by Lucian A. Bebchuk and Roberto Tallarita; Paying for Long-Term Performance (discussed on the Forum here); Pay without Performance: The Unfulfilled Promise of Executive Compensation; and Executive Compensation as an Agency Problem, all by Lucian Bebchuk and Jesse M. Fried.

Introduction

As companies address two fundamental and related shifts—the intensified focus on environmental,

social & governance (ESG) issues driven by investors, employees, consumers, business partners, ESG rating agencies, and regulators, [1] and the shift to a multistakeholder form of capitalism [2] —corporate boards are not only incorporating nonfinancial matters into discussions of company strategy and business plans, but also increasingly considering ESG performance measures in incentive plans. At the same time, there are concerns about the benefits of incorporating ESG measures into compensation, the risks of doing so (e.g., rewarding the wrong behaviors, setting inadequate targets, and creating guaranteed bonuses), and challenges in providing investors with what they view as sufficient transparency and specificity in ESG-based pay plans. These concerns have now been compounded by skepticism about whether ESG can actually drive financial performance for companies and investors alike. [3]

Insights for What’s Ahead

- The vast majority of S&P 500 companies are now tying executive compensation to some form of ESG performance—growing from 66 percent in 2020 to 73 percent in 2021. The most significant increase was found in companies’ use of diversity, equity & inclusion (DEI) goals, rising from 35 percent in 2020 to 51 percent in 2021, as investors and other stakeholders continue to focus on diversity—making it a priority for companies as well. And as a result of the ever-growing attention to climate change, the share of S&P 500 companies that tied carbon footprint and emission reduction goals to executive pay also grew considerably, from 10 percent in 2020 to 19 percent in 2021.

- Companies are embracing different approaches to factoring ESG into executive pay and are continuing to refine their ESG measures as they expand their reach. For example, some companies are moving from including ESG measures as part of the often-qualitative individual performance section of the annual incentive plan to incorporating ESG performance as a more quantitative modifier of the company’s overall financial performance rating, which is more aligned with investors’ preferences and expectations. Other companies are expanding the scope of those whose compensation is affected by ESG measures beyond the C-suite, reflecting that achieving ESG goals requires the collective effort of the employee base more widely.

- Leading reasons companies are incorporating ESG measures into executive compensation, according to a poll of roundtable participants, are to signal that ESG is a priority, to respond to investor expectations, and to achieve ESG commitments the firm has made. While these are valid reasons, they also raise concerns. For example, some large institutional investors are skeptical about tying compensation to ESG measures, especially if there is not a strong business case for doing so and if the ESG goals are not sufficiently challenging or specific. Further, there are other less costly and disruptive ways of signaling ESG is a priority, including building ESG factors into professional development, succession, and promotion practices. Companies can also convey or achieve their commitment to ESG by enhancing disclosure on ESG performance.

- Companies should consider using ESG operating goals for one to two years before including them in compensation. That allows time to see if those goals are truly relevant for the business, develop strong management and employee buy-in, and address any kinks in measurement methodology and reporting. It is especially important for companies to take time to validate and socialize ESG goals before rolling them out as part of compensation plans for a broader management or employee base.

- It takes time to develop and compile reliable, meaningful data that can be used to measure and report actual performance against ESG goals. Companies can start by putting together a steering committee with representatives from various functions (e.g., compensation, finance, sustainability) who are engaged in the company’s strategy, and understand and have access to the data needed to measure and report on ESG performance.

- Companies can link executive compensation to ESG successfully; however, they will need to go beyond simply “following the trend.” Actions companies will need to take include 1) identifying goals that are material, durable, and auditable, 2) assessing whether what the firm’s peers are doing in this area is instructive, 3) deciding whether to make performance measures absolute or relative to the market, and quantitative or qualitative, 4) determining the scope of those whose compensation is affected by ESG goals, 5) considering timing and assessing whether the ESG goal is appropriate for the annual or long-term incentive plan, 6) ensuring the type of metric reflects the firm’s corporate culture, 7) carefully considering the reaction of various stakeholder groups, and 8) reevaluating goals periodically to ensure that the ESG measures are still relevant and effective.

- Companies will need to explain why including or adjusting ESG goals in compensation programs makes business sense and will “move the needle” on the firm’s performance and impact. Investors will want to understand how modifying the company’s compensation is necessary to achieve the firm’s financial, operating, and ESG goals—and whether the goals are sufficiently challenging to put compensation “at risk.” Those covered by the compensation programs will want to understand why a portion of their compensation is now linked to ESG goals. In some cases, the rationale may be obvious, such as when a company includes compliance-related goals in the wake of a widespread compliance failure. In other cases, boards and senior management will want to carefully consider whether they have a compelling narrative for adopting or adjusting such goals, especially as most companies say that including ESG measures in executive compensation is no more than “medium important” to their overall ESG efforts.

- Measuring the full impact of including ESG performance goals in compensation is more challenging than measuring the impact of traditional operating or financial metrics. Companies should consider what they are trying to achieve by including ESG measures in compensation programs: is it to improve the firm’s ESG performance, to enhance its operating and financial performance, to signal that ESG (or a specific ESG metric) is a priority, to have a meaningful impact on society and the environment, or some combination of all four? If companies are actually seeking to have a broader impact on society and the environment, they may want to give serious consideration to how, if at all, they are incentivizing executives to work collaboratively with others in the industry and across the firm’s value chain—because making a measurable difference may require collective action.

About the ReportIn 2021, we advised companies to carefully assess the benefits and costs of incorporating ESG measures into executive compensation, and we discussed which pitfalls to avoid. [4] Since then, much has changed. More investors are expressing their views (or rather concerns) on the topic, and companies have now rolled out their ESG-based pay programs, gained experience in implementing the program through at least one pay cycle, and learned about communication with executives and shareholders alike. To capture lessons learned in linking executive compensation to ESG and explore the road ahead, The Conference Board ESG Center, in collaboration with Semler Brossy, held a roundtable at the end of the US proxy season in 2022 on ESG Performance Metrics in Incentive Plans that was attended by 120 compensation, ESG, sustainability, and governance executives from 72 firms. The discussion focused on the current trends in linking executive compensation to ESG performance, the lessons learned in the last two years, the ultimate goal(s) of ESG measures in incentive plans, and how to measure the full impact of using these measures. This report provides findings and insights based on that discussion, as well as data provided by ESG data analytics firm ESGAUGE. |

Current State of Play

Companies have been effectively tying some portion of executive compensation to ESG measures for decades. For example, they have successfully linked executive compensation to increasing diversity in the workforce, customer satisfaction, employee and product safety, and anticorruption programs. And driven by an ever-growing and widening focus on ESG issues, the percentage of S&P 500 companies that have adopted ESG performance measures continues to grow steadily—from 66 percent in 2020 to 73 percent in 2021. [5]

But companies are embracing different approaches, which generally fall within one of four categories:

- Stand-alone ESG metric: ESG is incorporated through specific (often quantitative) metrics;

- Business strategy scorecard: ESG goals are included and assessed as part of a broader scorecard of ESG or nonfinancial business priorities;

- Individual performance assessment: ESG is considered as part of an executive’s individual performance rating, which is often a discretionary assessment by the company’s compensation committee;

- Modifier: ESG can be used to adjust the financial performance rating, the overall rating, or the payout under a plan. [6]

As shown in Figure 1, ESG goals are most commonly integrated into executives’ individual performance assessment (49 percent) and the business strategy scorecard (48 percent), followed by a stand-alone metric (24 percent). Relatively few firms (6 percent) use ESG as a modifier to the ratings or payout. Please note that firms sometimes use a combination of approaches, which is why the percentages in the chart exceed 100 percent.

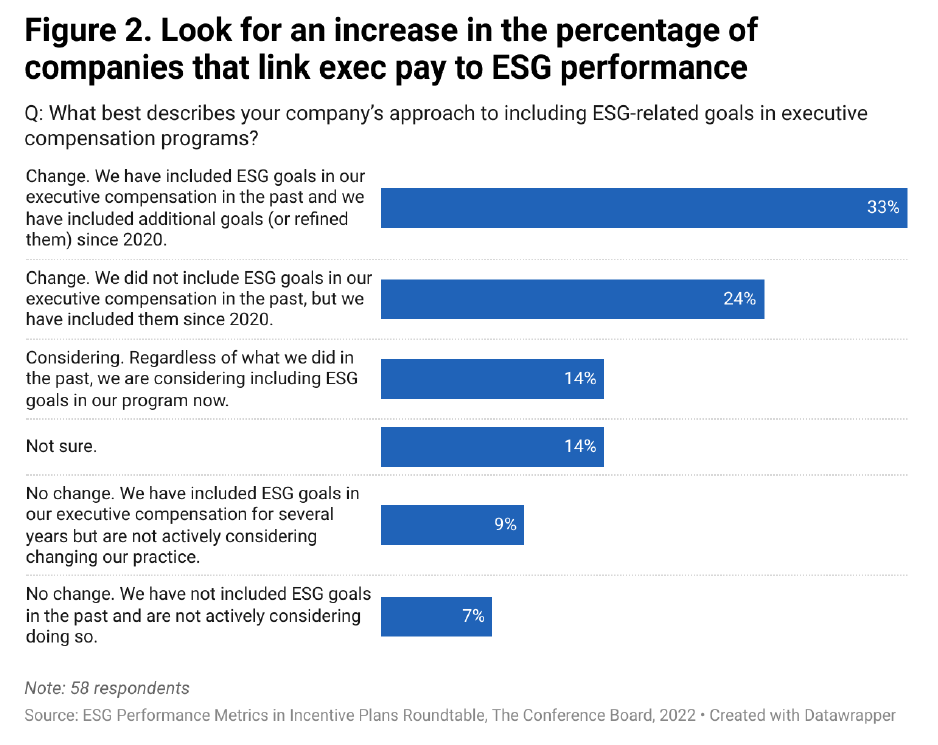

Companies’ approaches to including ESG measures in executive pay are prone to change. For example, a majority (57 percent) of roundtable attendees indicated that their firm’s approach has changed in recent years—with many adding goals since 2020—while only 16 percent indicated no change compared to the past.

Companies that have adopted ESG measures are continuing to refine them and expand their reach. Indeed, some companies are moving from including ESG measures as part of the individual performance section of the annual bonus plan to incorporating ESG performance as a modifier of the company’s financial performance rating. This has the benefit of mirroring how some investors view ESG. Others include ESG goals in a business strategy scorecard and take a data-driven, quantitative approach, but with a qualitative overlay that leaves room for compensation committee or board discretion. And some have more deeply embedded ESG goals as key pillars in the company’s compensation program—for example, evaluating each executive in four key areas: financial return, sustainable/quality growth, impact on the environment and society, and the firm’s reputation as a trusted partner.

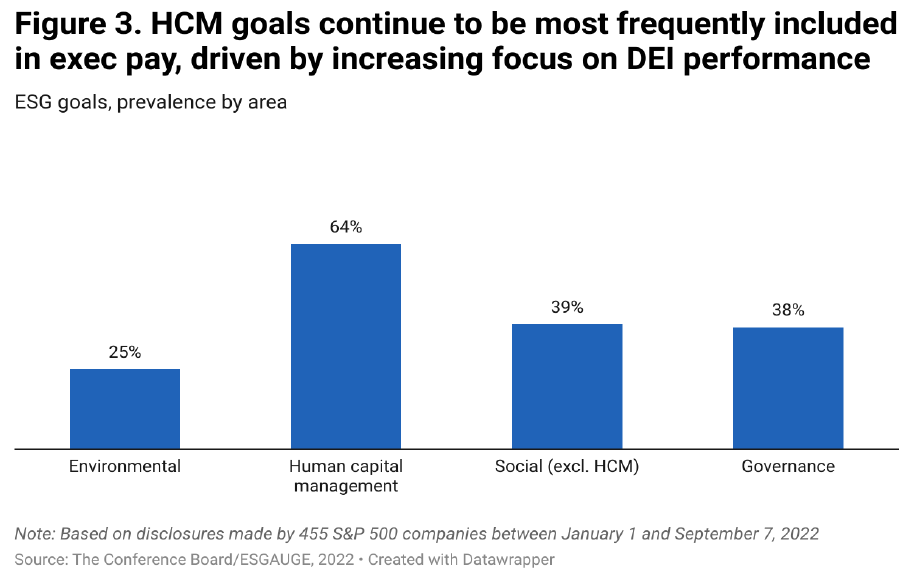

Human capital management (HCM) performance goals continue to be most frequently included in executive compensation plans and were found in 64 percent of S&P 500 companies. This makes sense as investors and other stakeholders are laser-focused on a wide array of HCM topics. HCM is followed by social (other than HCM), governance, and environmental goals (found, respectively, in 39 percent, 38 percent, and 25 percent of S&P 500 companies). Moreover, compared to 2020, environmental performance goals grew the most in popularity last year (from 16 percent in 2020 to 25 percent in 2021) as a result of the increased focus on topics such as climate, plastics, and biodiversity.

When drilling down on the most prevalent metric in each ESG area, we find a significant increase in the use of DEI goals. The share of S&P 500 companies that tied executive compensation to DEI performance grew from 35 percent in 2020 to 51 percent in 2021. Carbon footprint and emission reduction (the most common environmental performance goal) and succession planning (the most common governance goal) also increased. Customer satisfaction (the most prevalent social measure) decreased, however. [7]

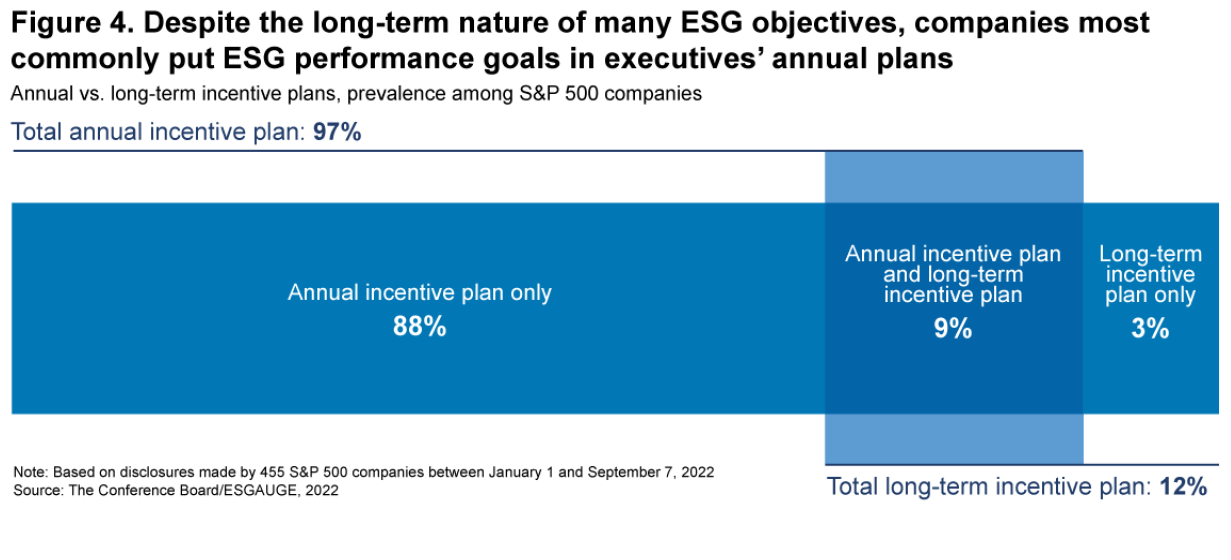

Despite the long-term nature of many ESG objectives, it’s most common for companies to put these in their executives’ annual incentive plan. Indeed, nearly 97 percent of S&P 500 companies that incorporated ESG performance metrics in incentives did so in 2021. Only 12 percent of companies put ESG measures in their executives’ long-term plan.

On the one hand, this might be the result of companies still experimenting with what works and what doesn’t. On the other hand, equity incentives have more accounting complexity, and companies may be hesitant to use the type of formulaic goals needed to ensure fixed accounting for ESG metrics. [8]

There are significant differences between business sectors when it comes to the inclusion of ESG performance goals in executive pay, with all companies in the utilities sector and 90 percent of energy companies tying ESG measures to executive pay, compared to only 55 percent of companies in the consumer discretionary and IT sectors. A likely reason is that companies in heavily scrutinized sectors (e.g., for employee health & safety or carbon footprint/emissions reduction) are more inclined to demonstrate that ESG is a priority through executive compensation than companies in sectors that are less scrutinized.

Drivers of ESG Measures in Executive Compensation

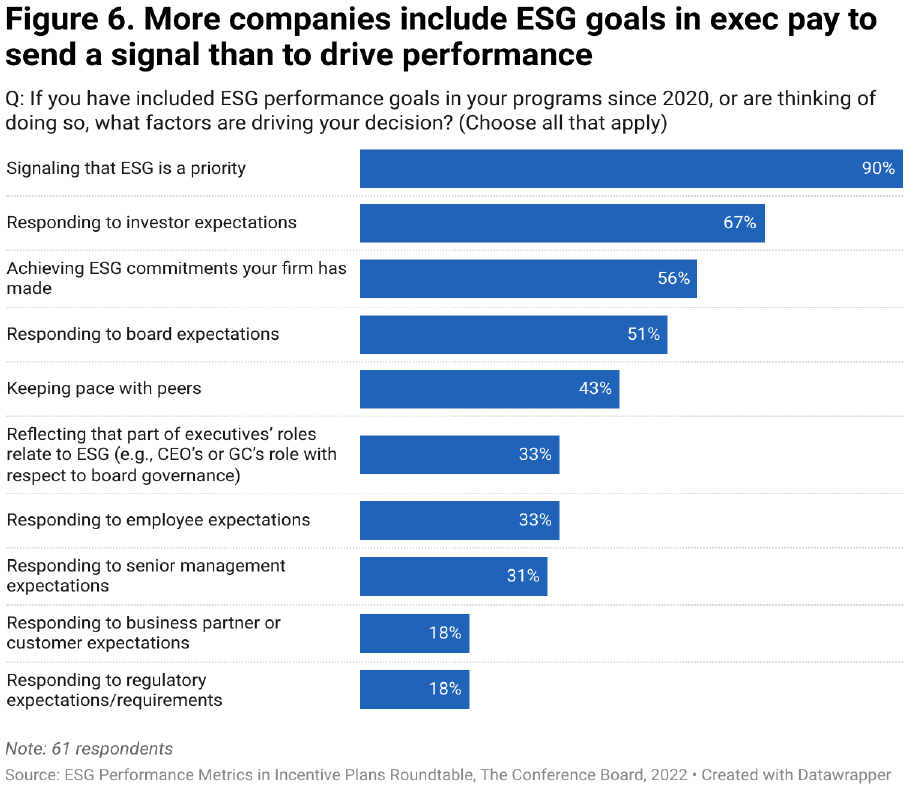

In addition to providing adequate compensation to attract and retain key leaders, executive compensation programs typically incorporate a variety of components to influence and reward the behaviors needed to successfully execute the company’s strategy. [9] ESG performance measures should be seen in this context. Now, various factors can drive the decision to adopt ESG measures—and companies may try to achieve different goals for doing so—but the roundtable discussion revealed that some of the leading reasons US companies are currently incorporating nonfinancial measures into executive compensation are 1) signaling that ESG is a priority, 2) responding to (perceived) investor expectations, and 3) achieving previously made ESG commitments.

To be sure, incorporating ESG goals in incentive plans—and holding executives responsible for delivering on these goals—can not only demonstrate the importance a company places on ESG, but also drive the corporation’s ESG and broader business performance. Adopting ESG measures also sheds light on the company’s ESG priorities and thus can serve as a communication tool for investors and other stakeholders.

Investor Support for ESG-Based Pay Is Not MonolithicDespite what companies might think, investors—especially in the US—do not uniformly support incorporating ESG measures into executive compensation. In fact, some large institutional investors have been agnostic about ESG-based pay due to the lack of standardization and transparency, and according to ISS’s 2021 Global Benchmark Policy Survey, 52 percent of investors believe ESG goals should only be used in executive pay if they are specific and measurable—even though many companies may believe it’s more appropriate to assess performance as part of the “individual performance” section of an incentive plan, especially when they don’t have much experience with using such goals. et, even investors who are less focused on specific metrics may view companies’ efforts with some skepticism: if a board decides to link part of executives’ bonuses to qualitative ESG performance, investors may wonder whether the targets are rigorous enough, or whether that portion of the bonus is more or less guaranteed because the goals are fairly easy to achieve and/or executives are merely paid for something they already are (or should be) doing. Moreover, companies have only so much “real estate” in their executive compensation plans to devote to specific goals, and investors are wary of crowding out other important financial or strategic goals. Additionally, some ESG goals, particularly those relating to the environment, might be so long term that they aren’t a good match for traditional executive incentive plans. Lastly, in some industries, certain ESG topics—such as employee health & safety and anticorruption—are so integral to a company’s core operational and financial performance that including additional goals in a compensation plan may be redundant. Other ways to signal commitment to ESG Before adding ESG performance measures to their executive compensation plans, companies should therefore assess what they are already doing to reward progress toward their ESG goals. Companies will also want to engage in dialogue with their investors to better understand their expectations regarding ESG generally and solicit their views on the use of ESG goals in incentive plans specifically. After all, companies can consider other ways to demonstrate that ESG is a priority and/or achieve previously made ESG commitments. It may be more effective, for example, to build ESG factors into professional development, succession, and promotion practices. This will send a powerful message, both internally and externally, regarding how seriously the company is taking the execution of its ESG strategy. Companies can also convey their commitment to ESG—as well as instill a sense of accountability—through effective public disclosure on ESG performance. |

In addition to responding to investor concerns, companies are incorporating ESG measures to address other stakeholder expectations, including those of boards and employees. Indeed, just as social issues are often raised by board members, [10] so is the drive from the top of the house when it comes to linking executive compensation to ESG goals. And employees may want companies to put their (executives’) money where their mouth is.

The roundtable discussion also revealed important reasons for not including ESG measures in executive compensation. These include 1) the difficulty in defining specific goals, 2) concern about the ability to measure and report actual performance against ESG goals, 3) skepticism about whether such goals are actually effective in driving performance, and 4) the fact that ESG performance is already covered by existing performance measures. However, only a minority of roundtable attendees indicated their company hasn’t included (nor plans to include) ESG goals in compensation programs.

ESG Performance Goals: Europe vs. the USState of play in Europe Although Europe has seen an uptick in the inclusion of ESG measures in executive compensation in recent years, it is not significantly ahead of the US—and there are considerable differences in the inclusion of ESG goals among the various countries. Forty-two of the top 100 European companies include some kind of ESG metric as a variable component of executive pay. Countries where ESG performance measures are relatively common include France, where roughly 70 percent of the largest 50 companies use them as of 2021; the UK, where 54 percent of companies include some kind of ESG metric; and Switzerland, where one-third of the top 100 companies and two-thirds of the large-cap index companies link executive pay to ESG. [11] But while the influence of ESG in executive compensation is growing in certain European countries, the practice of integrating ESG goals is not consistent across all European countries. For example, it is not a common practice yet in Sweden, Norway, Denmark, and the Baltics. Different drivers for the adoption of ESG performance goals In Europe, the trend to link ESG performance to executive pay is predominantly driven by regulations and an evolution in corporate governance codes. For example, “say-on-pay” regulations in several European countries are adding further provisions to encourage the link between sustainability and pay; the Shareholder Rights Directive II provides for increased transparency about nonfinancial metrics in compensation plans; the French corporate governance code recommends integration of ESG metrics in executive compensation plans; and the Financial Conduct Authority recently outlined three new diversity targets for UK-listed companies, including a goal for boards to be at least 40 percent gender diverse. [12] In the US, on the other hand, the trend is largely market driven. It’s unlikely that any of the SEC’s upcoming disclosure rules will require inclusion of ESG factors in compensation programs. Indeed, the SEC’s recently adopted Final Rule on Pay Versus Performance does not require disclosure of nonfinancial measures—even though registrants may supplement their mandatory pay-for-performance disclosure with a discussion of ESG goals (or any other nonfinancial performance measure). |

Laying the Groundwork for ESG-Based Pay

Before linking executive compensation to ESG measures, companies should consider taking several steps, including determining whether there really is a business case for ESG and if so, why this is not yet reflected in the current incentive pay program. If there is a business case, companies will want to carefully evaluate the incremental costs and benefits of adopting ESG performance goals—and assess their readiness for adding such goals. Part of this assessment is ensuring the firm’s ESG goals are 1) clearly defined, 2) aligned with its business strategy, and 3) reflective of its key ESG risks and opportunities.

How Do You Decide What ESG Areas Truly Matter? Insights from a Roundtable on How CEOs Can Drive ESG at Their CompanyTo determine what ESG issues truly matter for them, companies should focus on ESG through the lens of their strategy, with awareness of stakeholder views. Companies that integrate ESG into business strategy and planning processes don’t just view ESG as a source of risk but capitalize on business opportunities and innovation associated with emerging environmental and social issues. Therefore, instead of viewing ESG merely as a matter of governance, risk management, and/or compliance, companies should assess where they can have the biggest impact—as this is where their biggest opportunities lie. Indeed, figuring out what ESG areas can have the biggest positive impact on the long-term welfare of the company, its stakeholders, society at large, and the natural environment can serve as a guide in determining which ESG factors are central to the firm’s long-term value proposition. Source: The Conference Board ESG Center Roundtable Discussion on How CEOs Can Drive ESG at Their Company, July 28, 2022 |

Some other considerations companies will want to keep in mind before introducing or adding ESG performance goals to incentive plans:

- It can take six to eight months for a board to decide whether and how to incorporate ESG into executive compensation. The timing may vary depending on whether the company has experience with using such goals, the maturity of the company’s ESG program, and the level of buy-in from management. Generally speaking, however, that timeline should allow the relevant committees and board to reach agreement on which measures to include and how.

- But the process should begin much earlier. Ideally, ESG goals will have been built into the business plan and/or used by the company for one to two years to assess business performance in those areas before being included in executive compensation. This allows time to validate their importance and effectiveness, ensure there is strong buy-in from all levels of the organizations, and work through any issues in measurement methodology and reporting. Indeed, ESG goals generally require a deeper level of engagement with the business. Moreover, getting buy-in upfront will make it easier to communicate about actual ESG performance afterwards.

- A longer time frame should especially be expected if ESG goals apply to the broader employee base. For a performance measure to be effective, everyone needs to understand the goal, its connection to the business, and their own role in achieving it. It’s also important to consider potential unintended consequences of applying ESG measures to the broader employee base—for example, when different parts of the organization start competing with each other for resources to achieve the goals. Therefore, companies should not only break down goals into manageable time frames and action steps, but also assign responsibility for implementation to specific teams and individuals, clarify how employees can influence ESG performance and what outcomes define success, and facilitate interdepartmental collaboration. [13] All of this takes time.

- It also takes time to develop the ability to measure and report ESG performance. Developing and compiling reliable, meaningful data is therefore essential. Companies can start by putting together a cross-functional steering committee with representatives from compensation, finance, sustainability, and others who are involved in the company’s strategy and have access to the data that are (or might be) needed to measure ESG performance. The steering committee can also decide how and when to review the data, so it won’t be a last-minute exercise.

- Companies that have a global reach should be sure to understand how ESG issues and goals translate internationally. Even though some ESG goals (such as gender equality) can generally be applied globally, others (such as racial equality) can’t as easily. [14] But setting different goals for executives across the globe can send the wrong message. Therefore, the board and management will want to discuss how goals vary globally before such goals are adopted into incentive plans.

- Companies should consider upfront how to address changes in ESG performance measures. It is common for compensation committees to make adjustments when determining whether the company has achieved its financial goals set forth in annual incentive plans, including adjustments for accounting changes, significant acquisitions or divestitures, unexpected changes in regulation, etc. Especially given that companies are incorporating ESG measures into executive compensation to send a signal to investors, they need to be sensitive to the impact that adjustments can have on the company’s credibility with investors and others. At a minimum, boards and management should consider the types of adjustments that will be permissible (e.g., M&A or pandemic related) and disclose how the board may exercise its discretion in those instances.

Generally, a compensation plan should run for two to three years without significant adjustments. And regardless of the firm’s approach to adjustments, it’s critical that compensation remain at risk, be performance-based, and ideally reward relatively strong performance. The roundtable discussion furthermore revealed that some adjustments are easier than others. For example, it is relatively straightforward to adjust goals in light of an acquisition or divestiture. Other adjustments require more judgment. For example, the pandemic helped food companies in certain ways (e.g., consumers bought food in bulk) but hurt them in other ways (e.g., they could not meet sales goals for “portion control products”—snacks that have fewer calories and are individually wrapped). Companies that do need to make an adjustment should critically assess why the original goal isn’t working and be sure to communicate with transparency, integrity, and humility.

Steps for Linking Executive Compensation to ESG Goals

Companies can successfully link compensation to ESG, but this requires a rigorous and methodical approach tailored to the company’s particular circumstances and strategy, rather than merely “following the trend” or overly relying on peer data to inform the design of their compensation program. The following steps can help:

- Identify ESG goals that are material, durable, and auditable. For their ESG performance measures to appeal to investors, companies should be transparent and demonstrate that those goals indeed are linked to the company’s strategy and long-term value proposition, and that they are measurable, reportable, and provide accountability—especially when adopting a more qualitative approach (e.g., when they are included in the business strategy scorecard). Goals that don’t meet these criteria may be met with investor skepticism.

- Without simply mimicking them, assess what peers are doing in this area, both in the US and internationally, and decide whether to make performance measures absolute or relative to the market. To this end, companies will also want to talk to their investors and other stakeholders—not for answers, but for options to consider. For example, to incentivize the outperformance of peers, some investors encourage the adoption of a relative performance metric, such as but not limited to relative total shareholder return, as these metrics “may help align executive pay during both good and poor market conditions by protecting against outsized (or undersized) payments to executives. Relative metrics can be used alongside appropriate absolute metrics (such as net sales, operation income, or return on investment).” [15]

- Examine the extent to which ESG should affect the compensation of executives and employees beyond the C-suite. Some companies are expanding the scope of those whose compensation is affected by ESG goals beyond the CEO or C-suite, reflecting that achieving ESG goals requires the collective effort of the employee base more widely. In deciding to whom to apply ESG goals, companies will want to consider both the link between the goal and the business strategy and the scope of responsibility for implementing the goal within the organization.

- Consider timing and explain why the ESG goal is appropriate for a one- or three-year performance plan. According to ISS’s 2021 Global Benchmark Policy Survey, 81 percent of investors deem both short-term and long-term incentives appropriate for ESG performance goals, depending on circumstances. Indeed, although ESG goals tend to have long time horizons—often longer than an executive team’s tenure—specific behaviors can be rewarded so that individual executives are motivated to drive ESG performance. [16] Even when the nature of the goals is long term, the annual plan can thus be an appropriate place to include ESG measures, as it ensures the company continues to make progress, offers immediate feedback, and provides the flexibility to set different goals in Year 1, 2, 3, etc. as a company proceeds on its ESG journey. However, this requires companies to define short-term targets with defined increments that executives can address during their tenure.

- Ensure the type of metric reflects the firm’s corporate culture, and carefully consider the reaction of various stakeholder groups. Some companies respond strongly to qualitative performance goals, so this type of metric may very well be sufficient from an internal perspective. At the same time, companies should factor in what matters to their key stakeholders, such as climate, gender equality, or racial diversity.

- Reevaluate goals periodically to ensure ESG performance is supporting financial performance, and assess whether the measures are still needed. Certain ESG goals may be met in a specific time frame and can be dropped from a compensation plan, some may be evergreen (e.g., employee safety), and others may evolve over time (e.g., DEI). Boards and management should have a clear understanding at the outset in which time frame, if any, the company should achieve a goal.

Ultimate Goal(s) of ESG Measures in Incentive Plans—And How to Determine Impact

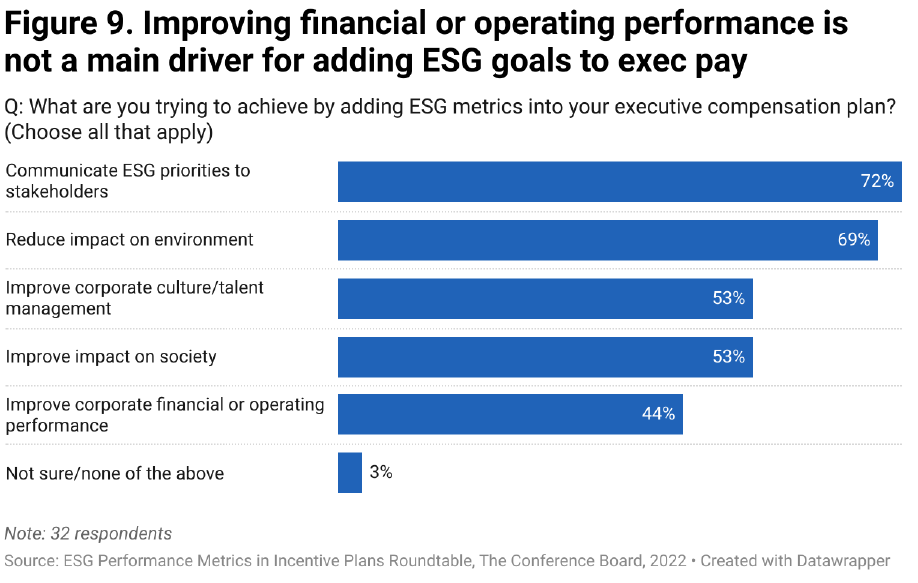

The roundtable discussion revealed that companies generally view the inclusion of ESG performance goals in executive compensation programs as part of a broader effort to achieve their ESG initiatives. Indeed, 67 percent of roundtable attendees rated ESG performance goals as being of only medium importance to their overall ESG efforts. In other words, incorporating ESG measures into compensation is just one tool in companies’ ESG toolbox.

Interestingly, for most companies, improving corporate financial or operating performance isn’t a main driver for adding ESG goals to their executive compensation plan. According to the roundtable participants, other drivers are more important, including communicating ESG priorities to stakeholders, reducing the company’s impact on the environment, improving the company’s impact on society, and improving corporate culture/talent management. If anything, this confirms that a shift toward multistakeholder capitalism—in which companies are placing a higher priority on serving the long-term welfare of constituents, such as employees, beyond their shareholders—truly is underway.

Measuring the impact of tying ESG goals to executive compensation programs is not as straightforward as measuring the impact of financial or operational goals. Some companies look at their reputation with stakeholders to gauge their impact on environmental and social issues. Others see employee engagement as a measure of success, as employees generally appreciate working for a company that’s trying to make a difference in the world. In any case, companies are looking beyond financial performance to assess their broader societal and environmental impact. However, one company can’t single-handedly change the world, so improving impact on environment and society needs to be a collaborative effort. Companies may therefore want to consider explicitly incorporating collaboration across their value chains and industry into their ESG goals.

Conclusion

To date, many companies have adopted ESG performance measures to signal that ESG is a priority, in response to perceived investor pressure, or to achieve previously made ESG commitments. Ideally, however, companies should incorporate ESG goals because they are linked to the company’s strategy and can drive meaningful change.

Going forward, companies may want to build ESG goals into their business plan for a few years before incorporating them into compensation programs. And if companies are looking to have a positive impact on an environmental or social issue, they may want to consider other ways of advancing ESG goals rather than adding any specific ESG metric. Indeed, companies should assess how they can incentivize executives to effectuate change across the company’s value chain and industry. After all, moving the needle on big issues can’t be done alone.

Endnotes

1Paul Washington, ESG Essentials: Who’s Driving the Focus on ESG?, The Conference Board, July 2022.(go back)

2Charles Mitchell et al., Toward Stakeholder Capitalism, The Conference Board, December 2021.(go back)

3ESG Funds: Is Green the Color of Money? The Conference Board CEO Perspectives podcast, August 2022.(go back)

4Paul Washington, ESG Metrics in Executive Compensation? The Conference Board, November 2021; Linking ESG Metrics to Executive Compensation: Virtue Signaling or Paying for Impact? The Conference Board Global Compensation & Benefits Watch webcast, in collaboration with Semler Brossy, September 2021.(go back)

5The data presented in this report are provided by ESG data analytics firm ESGAUGE. Data for 2021 are based on disclosures made by S&P 500 companies from January 1 through September 7, 2022 (N=455), and data for 2020 are based on disclosures made in 2021 (N=497). Please visit our ESG Incentive Plan Metrics Benchmarking Tool to see what ESG performance goals firms are using across not only the S&P 500 but the entire Russell 3000. (Available to subscribers only.)(go back)

6Id.(go back)

7Whereas customer satisfaction is a more traditional metric, the goals that are growing in prevalence reflect more contemporary ESG priorities.(go back)

8John Borneman et al., ESG + Incentives 2022 Report, Volume 1, Semler Brossy, July 2022.(go back)

9Washington, ESG Metrics in Executive Compensation?(go back)

10Paul Washington and Merel Spierings, Choosing Wisely: How Companies Can Make Decisions and a Difference on Social Issues, The Conference Board, June 2021.(go back)

11Anuj Saush et al., Integrating ESG into Executive Pay: Key Considerations (European Perspective), The Conference Board, June 2022.(go back)

12Saush et al., Integrating ESG into Executive Pay.(go back)

13Blair Jones et al., A Board’s Guide to ESG and Incentives, Semler Brossy, April 2022.(go back)

14Lindsay Beltzer, Addressing Racism Through Corporate Citizenship: A Global Perspective (Brief 1), The Conference Board, August 2022.(go back)

15Vanguard Investment Stewardship Policy Insights: Highlighting Vanguard’s Views on Executive Compensation, May 2022.(go back)

16Jones et al., A Board’s Guide to ESG and Incentives.(go back)