Print

PrintJulia Forbess is a Partner and Ron C. Llewellyn is Counsel at Fenwick & West LLP. This post is based on their Fenwick memorandum. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) by Lucian A. Bebchuk and Roberto Tallarita; Does Enlightened Shareholder Value add Value (discussed on the Forum here) by Lucian A. Bebchuk, Roberto Tallarita, and Kobi Kastiel; Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy—A Reply to Professor Rock by Leo E. Strine, Jr. (discussed on the Forum here); and Stakeholder Capitalism in the Time of Covid (discussed on the Forum here) by Lucian A. Bebchuk, Roberto Tallarita, and Kobi Kastiel.

Overview

In 2022, many smaller biotech companies appear to be making progress toward addressing the environmental, social and governance (ESG) risks and opportunities affecting them and their industry. As a follow-up to our report Biotech’s ESG Crossroads, released earlier this year, we re-examined the ESG disclosure practices of 48 of the 50 public biotech companies that we previously researched (the subject companies).[1]

While ESG disclosures still remain relatively brief and largely qualitative, we noted a substantial increase in ESG reporting in 2022 by the subject companies that may signal the growing realization by biotech companies of the importance of ESG to their stakeholders. This guide reviews the trends in ESG reporting for these companies in 2022 and provides suggestions for how biotech companies can initiate or enhance their ESG reporting.

2022 ESG Disclosure Trends

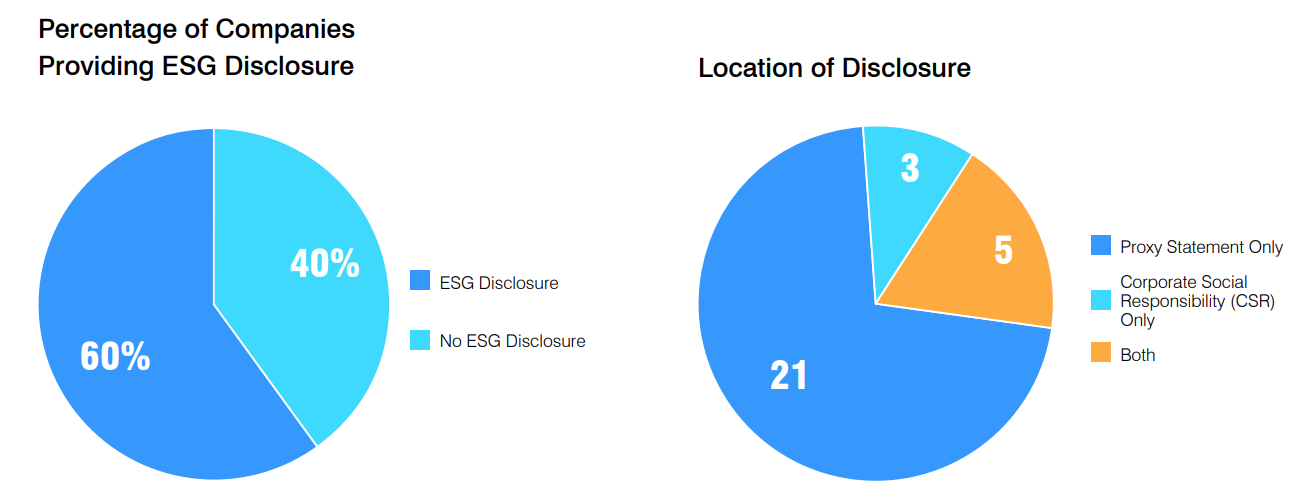

When we first looked at ESG reporting for biotech companies in 2021, relatively few companies had reported any ESG data. Overall, just 30% of the subject companies publicly disclosed ESG information as a unified set of risks and opportunities under an umbrella term such as “ESG,” “sustainability” or “corporate social responsibility.” Furthermore, only nine, or 18%, and five, or 10%, of the companies had provided disclosure in their proxy statements or standalone reports, respectively, with three companies providing disclosure in both documents.

In contrast, since the beginning of 2022 through September 30, at least 26, or approximately 54%, have provided ESG disclosure in their proxy statements and eight companies, or approximately 17%, provided ESG disclosure in standalone reports. Five of the companies reviewed in 2022 provided ESG disclosure in both documents.

We focused our 2022 analysis on ESG disclosure contained in proxy statements or standalone reports, as these are the platforms where companies generally provide the most extensive disclosures. Overall, 29, or approximately 60%, of the subject companies provided ESG disclosure on either platform in 2022, more than double the number providing ESG disclosure on either platform — 11, or approximately 22% — in 2021.

When ESG-reporting companies provided their ESG disclosure in their proxy statements, the disclosure was generally brief and qualitative. The average disclosure consisted of a few paragraphs describing ESG initiatives and programs at a high level, usually broken into separate sub-sections for discrete ESG topics such as “environment” or “community impact.”

The topics discussed most often included those related to human capital resources (e.g., diversity and employee engagement and training), corporate governance and the environment (excluding greenhouse gas [GHG] emissions). ESG disclosure was often found in its own section, typically under the caption “Environmental, Social and Governance,” “Corporate Social Responsibility” or a similar title.

Several companies noted that they were still in the process of developing their ESG strategy or that they had plans to expand upon their ESG disclosure in the near future. Seventeen, or 59%, of the ESG-reporting companies were including an ESG section in their proxy statements for the first time, and many of these expressed some intention to build on their disclosure as their capabilities and understanding of their ESG risks and opportunities increased.

Companies generally provided more substantive disclosure in standalone “ESG” or “Corporate Social Responsibility” reports (CSRs) compared to proxy statements. CSRs ranged from 19 to 73 pages in length with an average length of approximately 35 pages and provided information on an average of seven ESG topics.

Given the length of these reports and the depth of the disclosures, some companies drew a distinction between the information in their CSRs and their filings with the U.S. Securities and Exchange Commission (SEC), including emphasizing that disclosure of certain topics in CSRs did not imply that those topics were “material” under U.S. securities laws, or explicitly stating that such reports were not incorporated by reference into their proxy statements or other SEC filings.

Use of Standards and Frameworks for Disclosure

Many companies rely on third-party standards and frameworks to inform the ESG topics that they disclose. Some of the most commonly utilized standards and frameworks include the Sustainability Accounting Standards Board (SASB) standards and the Task Force on Climate-related Financial Disclosures (TCFD) framework.

SASB provides a set of sustainability disclosure topics and accounting metrics deemed to be most relevant to investors based on a company’s industry. Five, or 17%, of the ESG-reporting companies that disclosed information in standalone reports stated that they reported to or were influenced by the SASB standards, typically the SASB Biotechnology & Pharmaceuticals Standard.

These standards provide for disclosure in the following areas for biotech companies:

- Safety of clinical trial participants

- Access to medicines

- Affordability and pricing

- Drug safety

- Counterfeit drugs

- Ethical marketing

- Employee recruitment, development and retention

- Supply chain management

- Business ethics

Similarly, in addition to SASB, the Biopharma Investor ESG Communications Initiative, a collaboration of senior biopharma executives and investors to identify decision-useful sustainability information, provides the ESG Communcations Guidance 4.0. The guidance offers recommendations for ESG reporting for biotech companies that can be used in conjunction with other frameworks and standards.

Its high-priority topics for the biopharma sector include: access to healthcare and medicine pricing; business ethics, integrity and compliance; climate change; clinical trial practices; ESG governance; environmental impacts; human capital management; innovation; pharmaceuticals in the environment and antimicrobial resistance; product quality and patient safety; risk and crisis management; and supply chain management.

The International Sustainability Standards Board (ISSB), which was formed in 2021 by the International Financial Reporting Standards Foundation, is also developing a set of industry-specific standards for sustainability-related financial disclosure that many believe will become the dominant global sustainability standards. ISSB expects to issue its final standards by the end of 2022. ISSB’s standards for biotech companies are likely to draw upon SASB, providing for similar qualitative and quantitative disclosure.

Common ESG Disclosure Topics

Even when employing a standard or framework for their ESG disclosures, the subject companies typically just addressed some of the suggested topics and did not provide many of the associated quantitative metrics. The following topics were discussed most often by the subject companies.

Human Capital Resources

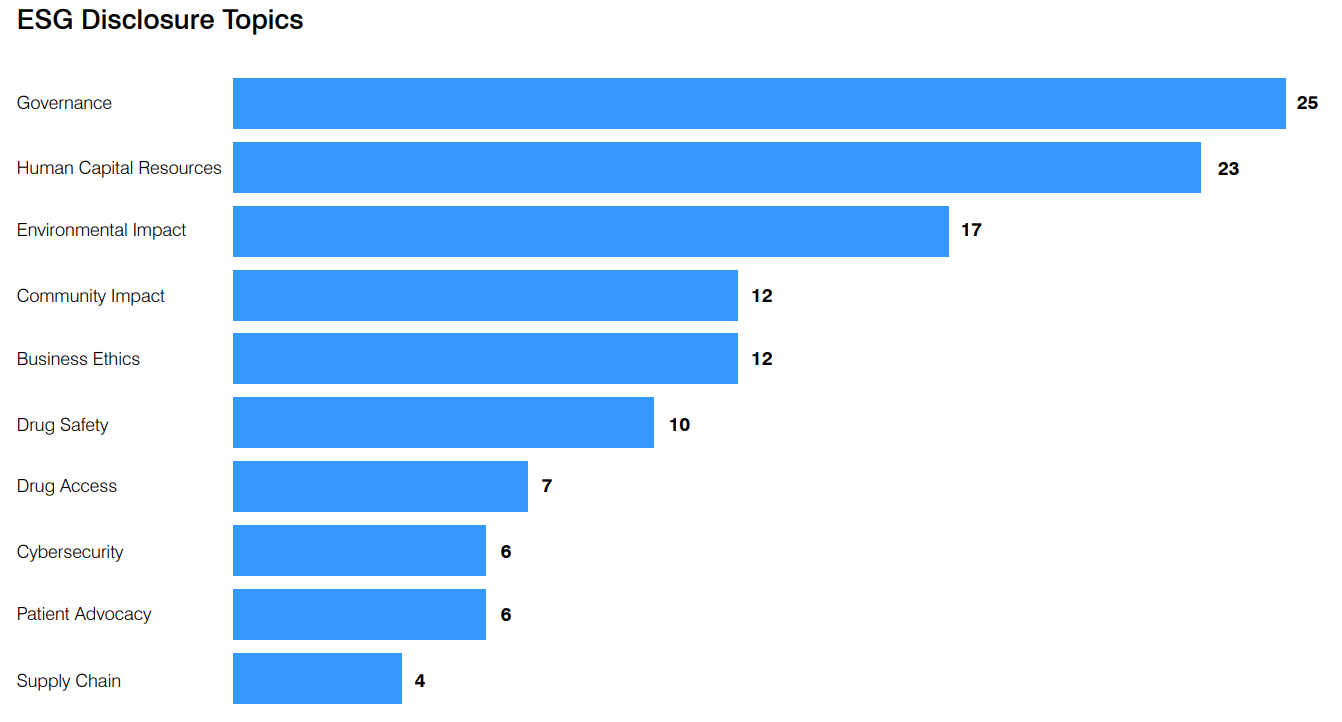

Human capital represented one of the most popular ESG disclosure topics with 23, or 79%, of the ESG-reporting companies disclosing data related to human capital issues, including the most common ones noted below.

- Diversity, Equity and Inclusion (DEI). Companies often provided both qualitative and quantitative DEI data. Qualitative data included descriptions of hiring initiatives, formation of employee resource groups (ERG), programs to increase representation of underrepresented groups in the life sciences, and bias awareness training. Quantitative DEI information often consisted of aggregated employee demographic information according to gender and race/ethnicity. Demographic information was also provided based on role (e.g., manager, executive or professional).

- Employee Engagement. Companies described efforts to engage with their employees to increase retention. Some companies touted high engagement survey participation rates while others wrote more generally about their engagement efforts. Employee Safety. Companies spoke about efforts to provide a safe work environment. In particular, many companies disclosed their policies in response to the COVID-19 pandemic, such as providing for remote working arrangements or establishing in-office measures to prevent the spread of the virus.

- Employee Training. Companies discussed various programs to train and develop their employees, allowing them to build careers. Such programs were lauded for facilitating greater retention.

- Compensation and Benefits. Companies described their compensation plans and the various benefits offered to employees, including 401(k) plans, health plans, incentive plans and family leave policies.

Public companies are also required to disclose human capital resources information in the business sections of their Forms 10-K to the extent that they are material to an understanding of their business. The subject companies took a variety of approaches to harmonize their human capital resources disclosures in their Forms 10-K with their proxy statement disclosures. Some chose to provide very brief disclosure of human capital resources in their Forms 10-K and more detailed information in the ESG sections of their proxy statements, while others favored the opposite approach, expanding upon their human capital practices in their Forms 10-K and condensing their proxy statement disclosures.

Governance

Although there are several corporate governance–related disclosure requirements for the proxy statement, 16 of the ESG-reporting companies also discussed their governance practices in the ESG sections of their proxy statements, and all companies included corporate governance disclosure in their CSRs. Some companies identified codes of conduct and ethics, corporate governance guidelines and board committee charters when discussing their governance practices. Cross-referencing more extensive disclosures of these documents in other parts of the proxy statement was also used in some cases.

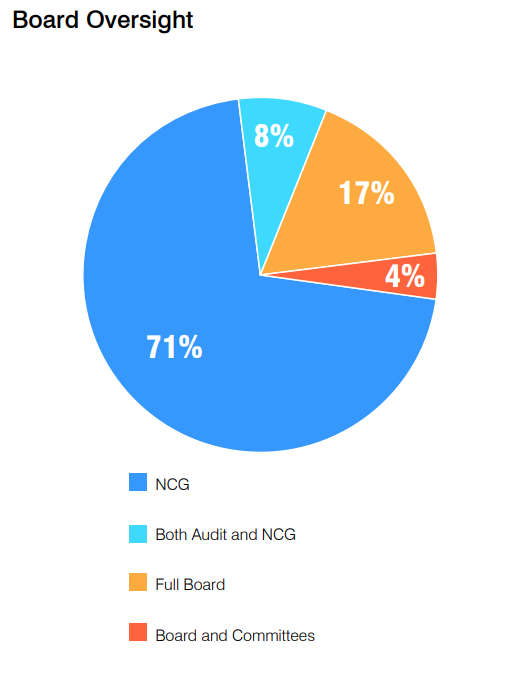

Governance disclosure often discussed the board’s oversight of ESG matters, including whether the full board or a particular committee or multiple committees had primary oversight of ESG. Twenty-four, or 50%, of the subject companies (representing 83% of the ESG-reporting companies) disclosed the board or board committee oversight of ESG matters. Seventeen, or 71%, of these companies disclosed the nominating and corporate governance (NCG) committee (or its equivalent) had primary responsibility for ESG matters.

The remaining companies disclosed oversight as follows: the full board (four, or 17%), both the audit and NCG committees (two, or 8%), and the board and its committees (one, or 4%). In such cases, companies often disclosed responsibility for ESG in their proxy statement’s descriptions of committee charters as applicable.

Governance disclosures also addressed management’s role in overseeing ESG, including the formation of committees or working groups to set ESG strategy, gather and verify data and report regularly to the board. Companies also noted engagement efforts by board members or management with key shareholders and other stakeholders on certain ESG issues.

Most companies provided demographic statistics (gender and race/ethnicity) for their boards, typically on an aggregated basis. Companies listed on Nasdaq are subject to board diversity rules adopted in 2021, which require companies to provide board diversity information in their proxy statements or on their websites in a tabular format (for more information on the Nasdaq rule see our alert here).

Accordingly, many of the Nasdaq-listed subject companies reported such disclosure for the first time in their proxy statements. In addition, one company disclosed an initiative to achieve board diversity through a requirement that a minimum number of diverse candidates be included in every board member search to ensure a diverse mix of board candidates.

Environmental Impacts

When discussing environmental initiatives, the 17, or 59%, of ESGreporting companies that reported on this measure generally focused on qualitative activities, and few quantitative metrics were provided. The companies disclosed activities such as reducing waste and energy consumption and recycling. In addition, they cited company policies, programs or amenities that encouraged environmental sustainability (e.g., remote work, paper-use reduction and recycling). Companies also noted their investments in energy-efficient systems and facilities.

Several companies also represented that they complied with environmental requirements and regulations, though none of the subject companies disclosed GHG emissions data, which has commanded the attention of numerous investors and other stakeholders and has been the subject of recent SEC rulemaking. For a discussion of the SEC’s proposed rules regarding climate risk disclosure see our alert here.

Business Ethics

Generally, the 12, or 41%, of the ESG-reporting companies that disclosed business ethics practices described their codes of business conduct and ethics or similar documents, which is also required under the federal proxy rules, and described related training. Companies also referenced compliance programs, including policies and procedures to encourage reporting and protect whistleblowers. Such compliance policies included those related to product quality and safety, clinical trials, responsible sales and marketing, and supply chains. Furthermore, some companies noted that suppliers and vendors were required to represent that they complied with applicable laws and such compliance policies.

Community Impact

Twelve, or 41%, of the ESG-reporting companies discussed their interactions with their outside communities, often noting corporate philanthropy or community service programs. Disclosure included qualitative descriptions of companies’ donations to or support for organizations in the communities in which they operated, such as through sponsoring internships. Some of these activities were focused on specific causes, such as increasing representation for minorities and other underrepresented groups in clinical trials or in the scientific or medical fields generally.

Drug Safety

Ten, or 34%, of the ESG-reporting companies referenced the clinical trial process. However, only four companies provided specific metrics regarding recalls or fatalities associated with their products or any Federal Drug Administration (FDA) enforcement actions. In each case the company reported that it had no such incidents to report.

Drug Access

Seven, or 24%, of the ESG-reporting companies included disclosure of drug access policies, and generally discussed efforts to engage with stakeholders to address access to drug treatments, including by entering into advance purchase agreements to allocate and distribute medications such as vaccines.

Cybersecurity

Six, or 21%, of the ESG-reporting companies chose to address cybersecurity and measures taken to safeguard patient information and other sensitive data. Companies generally provided qualitative disclosure regarding testing, audit committee oversight, employee training and ensuring vendor compliance with cybersecurity protocols.

Patient Advocacy/Engagement

Six, or 21%, of the ESG-reporting companies discussed their work with patient advocacy organizations to bring therapies to patients. Disclosures also mentioned partnering with patients during clinical trials to shape trial designs.

Supply Chain Management

Four, or 14%, of the ESG-reporting companies briefly discussed their relationship with suppliers and vendors, noting that vendors were vetted and monitored based on risk. Companies also stated that suppliers and vendors were expected to adhere to the companies’ policies and all legal and regulatory requirements. In some cases, the disclosure described the company’s supplier code of conduct, which applied to its suppliers and their subcontractors and suppliers. One company also discussed its supplier diversity program, which aimed to increase opportunities for women, minorities and veterans.

Beginning or Enhancing ESG Disclosures

As demonstrated by the subject companies, ESG disclosure practices still vary in the biotech sector. For biotech companies looking to initiate ESG reporting, there are several issues for consideration.

Determine the Most Important ESG Risks and Opportunities for Your Company

While ESG frameworks and standards may identify ESG topics that may be most important to biotech companies and their investors, each recommended disclosure topic may not be relevant to every biotech company. A company should perform its own assessment of the ESG issues that are most relevant for its business and on which it wants to publicly report. This determination may be aided by a third-party framework or standard, benchmarking against the ESG disclosures of peer companies and/or engaging with its key stakeholders, including institutional investors.

- Frameworks and Standards. The SASB standards are favored by many large institutional investors, such as BlackRock. However, disclosure is voluntary, so a company can decide which topics or metrics to disclose initially and expand its disclosure over time.

- Peer Company Benchmarking. Looking at other public biotech companies at a similar development stage or with similar products may help a company to determine appropriate ESG disclosure topics and metrics. It may also reveal the information that investors and other stakeholders may be expecting from the company in the absence of direct engagement.

- Direct Engagement. Outside of its own analysis, direct engagement with its most important stakeholders may offer a company the best means for determining what information it should disclose. A biotech company’s stakeholders may include its shareholders, patients, employees, suppliers, business partners, government agencies and the community in which it is located. Discussions with stakeholders can help to ensure that a company is disclosing the most relevant information to its stakeholders.

Oversight

Once a company decides the ESG topics or metrics on which it wants to focus, it should establish an appropriate management structure and controls and procedures to implement its ESG strategy. This may consist of forming an internal working group of senior members of key corporate functions such as finance, legal, risk management and relevant business units.

Regardless of the oversight structure, the person or persons responsible for oversight should coordinate with relevant business functions to ensure that data is collected, verified and reported to the board of directors and externally. This also necessitates that disclosure controls and procedures are in place to ensure that ESG information is accurate and to reduce the risk of fraudulent disclosures.

The company’s board of directors (or one or more of its committees) should also oversee ESG. This would entail understanding how ESG impacts the company’s strategy, understanding the primary ESG risks and opportunities for biotech companies and engaging with key investors and other stakeholders on ESG issues. For more information on establishing effective disclosure controls for ESG reporting and oversight, see our alert here.

Leveraging Existing Disclosures

A company should consider those ESG activities that it may be conducting already and how it may better highlight them. For example, summaries of donations or philanthropic activities in the community that may currently reside on the company’s website can be repurposed for use in the ESG section of its proxy statement or as part of a standalone report. A company’s proxy statement offers a practical and convenient place to provide ESG disclosure, as it must already include descriptions of the company’s corporate governance practices.

Existing proxy statement disclosure could be enhanced to indicate how the board provides oversight for ESG (e.g., revising the descriptions of the board committee’s responsibilities to note oversight of ESG or an aspect of ESG). Furthermore, the governance policies and documents disclosed in other sections of the proxy statement could be summarized or cross-referenced in an ESG section. A company can also repurpose or expand upon the human capital resources disclosure from its Form 10-K in its proxy statement.

Most public biotech companies are likely already tracking or reporting significant ESG data. However, ESG reporting, particularly in SEC filings, is subject to the SEC’s anti-fraud provisions. Even disclosures on websites or standalone reports that prove to be false or misleading can subject a company to litigation or an SEC enforcement action, as demonstrated by SEC v. Vale S.A. (No. 22- cv-2405), in which the SEC charged a Brazilian mining company with making false and misleading claims about the safety of its dams in its public sustainability reports and other public filings.

Accordingly, in addition to making sure its ESG disclosures are accurate in its SEC filings, a company should make sure that they are also consistent across platforms. The SEC has also scrutinized and issued comment letters where certain ESG disclosure was included in a public company’s sustainability report but not its Form 10-K, which underscores the importance of establishing appropriate disclosure controls.

As a company increases its resources and improves its infrastructure, it should be in a better position to augment its ESG disclosure. Over time, a company may look to expand upon some of its ESG initiatives and related reporting. Such expansion will necessitate the gathering and verification of additional data and the related establishment of controls and procedures required for analysis and verification. For example, in discussing how it addresses environmental concerns, a company may initially just disclose qualitative sustainability initiatives, such as recycling policies or charging stations for electronic vehicles.

Gradually, it may evolve to tracking and reporting its Scope 1 and Scope 2 GHG emissions and energy usage. Eventually, it could set and disclose scientifically based targets for GHG emissions reduction. Because of the additional effort that would be required to gather more granular and quantitative data, a company would need to increase its internal and/or external resources to be able to provide such data, which may take more time for a less mature or profitable company. However, potential mandates could force companies to develop their ESG programs sooner than planned.

The Potential Impact of Regulation

The interest in ESG has led to increased scrutiny from regulators and the prospect for more mandated ESG disclosure. The SEC has signaled a desire to enact regulations requiring public companies to provide more prescriptive ESG disclosure. As noted, in March 2022, the SEC proposed sweeping regulations that could require companies to provide extensive disclosure on climate risk in their annual reports on Form 10-K and registration statements.

Similarly, in March 2022, the SEC proposed rules that would require public companies to disclose their cybersecurity risk management, strategy, governance, and incidents in current and periodic reports (for more information see our alert here). The SEC has also indicated that it intends to propose rules that would require disclosure in the key ESG areas of board diversity and human capital resources. If these rules are adopted, they would change the voluntary nature of much of ESG reporting in the U.S. and accelerate the timetables for companies to begin ESG reporting.

As noted above, this could also present a hardship to less mature biotech companies that may find it difficult to harness the resources needed to report the required information. As a result, companies that have not started reporting on these measures should consider preparing for such reporting ahead of actual mandates.

Conclusion

Despite some recent criticisms of ESG and its proponents, demands for ESG information, including by large institutional investors and regulators, is expected to continue. Biotech companies that fail to provide ESG disclosure risk greater scrutiny, criticism and potentially higher capital costs by failing to address ESG. Although the costs of gathering some types of ESG data or implementing some initiatives may be challenging, companies can still pursue an incremental approach, addressing the “low-hanging fruit” and expanding their capabilities and related disclosure as their operations grow.

Endnotes

1Out of the original 50 companies reviewed, two were acquired and are no longer reporting companies. (go back)