Print

PrintMatthew Behrens is Counsel and Giulia La Scala is an Associate at Shearman & Sterling LLP. This post is based on a Shearman & Sterling piece by Mr. Behrens, Ms. La Scala, Doreen Lilienfeld and Gillian Moldowan and is part of the 20th Annual Corporate Governance Survey publication of Shearman & Sterling LLP. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) by Lucian A. Bebchuk and Roberto Tallarita; For Whom Corporate Leaders Bargain (discussed on the Forum here) by Lucian A. Bebchuk, Kobi Kastiel, and Roberto Tallarita; Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy—A Reply to Professor Rock (discussed on the Forum here) by Leo E. Strine, Jr.; and Stakeholder Capitalism in the Time of Covid (discussed on the Forum here) by Lucian A. Bebchuk, Kobi Kastiel, and Roberto Tallarita.

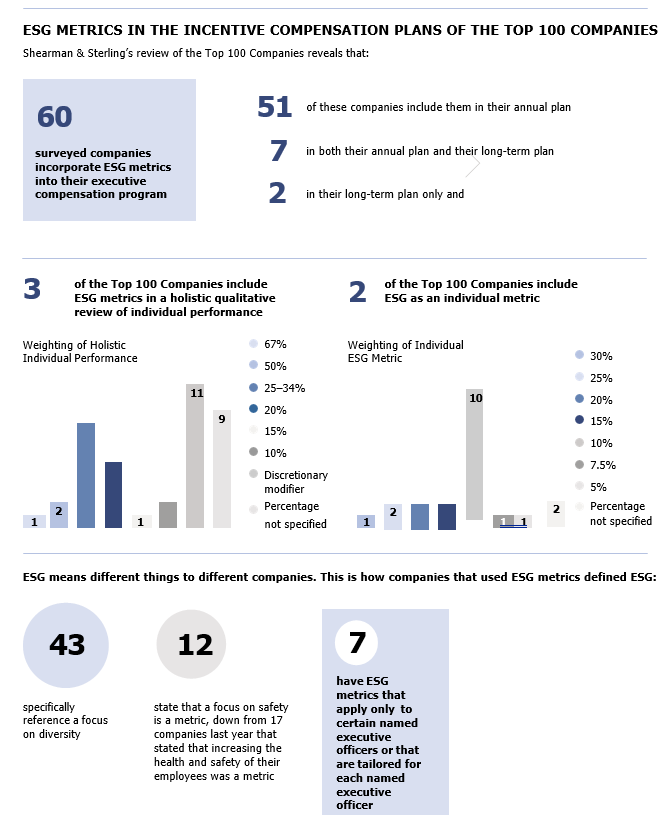

The “stakeholder” view of corporate governance, which argues that corporate decision-makers have a responsibility to consider the impact of corporate activities not only on shareholders but on society as a whole, has long been debated, with some scholars even finding arguments in the writings of Adam Smith that companies may weigh competing stakeholder claims.[1] Recent years, however, have witnessed the “stakeholder” view no longer confined to the ivory halls of academia, but present in the wood-paneled board rooms of institutional investors and the fluorescent-light-drenched offices of government regulators. For those that would argue that issuers are embracing this view, the continuing growth of ESG metrics in incentive compensation plans has become a primary piece of evidence. For example, this year our survey data shows that 60 of the Top 100 Companies disclose that they incorporate ESG metrics into their incentive compensation programs, which is a 19% increase from last year.

Notwithstanding their seeming embrace of the “stakeholder” view, U.S. issuers are facing increasing pressure to prove that their claims of stakeholder focus are grounded in fact and evidenced by action. To that end, disclosures around ESG metrics in incentive plans are increasingly being challenged as vague or lacking the transparency necessary for outsiders to gain a true understanding of the issuer’s ESG goals and management’s performance against those goals.[2] Notwithstanding this desire for more detailed compensation-related ESG disclosure, issuers face the ongoing challenge of how to define meaningful and objective metrics. Further, as work continues on the establishment of a global set of standards for ESG reporting similar to financial reporting (particularly with respect to climate reporting), questions remain as to whether such a standard would in fact be beneficial.

This article summarizes the current status of incentive compensation disclosures and the challenges to those disclosures, as well as focusing on the work being done to establish a more transparent reporting regime. Finally, the article offers considerations for issuers looking to provide more meaningful disclosure around the use of ESG metrics or considerations in their incentive compensation programs.

EVIDENCE OF DISSATISFACTION

While the number of issuers incorporating ESG metrics into their incentive compensation programs is steadily increasing, so too are expressions of dissatisfaction with the quality of the related proxy disclosures. The ESG metrics companies link to compensation often are criticized as being overly broad, vague and qualitative, making it challenging to assess how and why the metrics were chosen and weighted. Consistent with that criticism, our survey data shows that most issuers include ESG metrics as part of a larger performance metric, rather than as an individual metric. Taking “diversity” as an example, this year 43 issuers specifically reference a focus on this metric. However, only 15 of them included it as an individual metric, and only seven of them gave an insight on the methodology used to assess whether the diversity metric had been satisfied.

Investors have begun to voice their dissatisfaction with the level and quality of ESG disclosures in respect of equity incentive plans. For example, the RBC Global Asset Management 2021 Responsible Investment Survey showed that 72% of institutional investors in the U.S., Canada, Europe and Asia apply ESG principles as part of their investment approach and decision making and 84% believe that ESG integrated portfolios are likely to perform as well or better than non-ESG integrated investments. Notwithstanding this focus on ESG, only 37% of the surveyed investors stated that they were somewhat satisfied or very satisfied with the current amount of ESG related disclosures and a slightly smaller percentage said they were satisfied with the quality of the disclosures. Further, BlackRock Investment Stewardship stated in its 2022 Global Principles that, although it does not have a position on the use of ESG-related criteria in incentive programs, when used, those metrics should be as rigorous as other targets. Blackrock further notes that robust disclosure is essential for investors and that it will “advocate for continued improvement in companies’ reporting.”

Further, in January of 2022, the Securities and Exchange Commission (SEC) reopened the comment period for its proposed rule to implement the pay vs. performance disclosure requirements mandated by Section 953(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010. The rule, which was finalized in August of 2022, requires proxy disclosure of how executive compensation paid by an issuer relates to the financial performance of the issuer. As initially proposed by the SEC in 2015, the proposed rule required tabular disclosure of amounts actually paid in the relevant year, as well as the cumulative and absolute total shareholder return (TSR) of the issuer over the same period. In its January 2022 release, however, the SEC asked whether additional factors beyond TSR should be disclosed, including a “Company-Selected Measure,” which would be the issuer’s assessment of the most important measure used to determine compensation. In addition, issuers would be required to disclose a list of up to the five most important measures used by the issuer to link compensation to performance.[3] The SEC also asked how it should contemplate developments with respect to ESG related metrics in formulating its final rule.

A number of commentators used the proposal as an opportunity to criticize the quality of issuer disclosures with respect to ESG-linked compensation. For example, Dimensional Fund Advisors LP stated that the ESG metrics are “ill-defined or inherently difficult to quantify” and asked for “clear disclosure” of how each metric is utilized and why it is aligned with shareholder interests in the event ESG is identified as an important measure used to determination compensation. The overriding sentiment, however, was articulated by commentators such as Loring, Wolcott & Coolidge Trust, LLC and Principles for Responsible Investment, which noted that vague ESG factors may inappropriately boost executive pay by allowing for ESG targets that are too easily achievable.

The focus on ESG disclosures cited by the commentators above also was echoed by SEC Commissioner Caroline A. Crenshaw, who, in her statement accompanying the release, cited to her previous comment that “without reliable and consistent disclosures about those ESG targets, I wonder whether investors and Boards have the tools to accurately assess if such targets have been met and if that alignment between executive pay and ESG targets has been achieved.” Similarly, Commissioner Allison Herren Lee asked commentators to inform the SEC of how the “increased flexibility” of the release may “facilitate investor analysis of the use of [ESG] metrics and targets in compensation plans.”

EFFORTS TO HARMONIZE METRIC SETTING

Notwithstanding the desire for more robust disclosures, the debate continues about whether there should be a global standard of reporting for ESG metrics. For example, SEC Commissioner Hester M. Peirce has stated that “global reliance on a centrally determined set of metrics could undermine the very people- centered objectives of the ESG movement by displacing the insights of the people making and consuming products and services.”[4] On the other side of the debate are organizations such as the Americans for Financial Reform Education Fund, which, in their comment letter to the SEC, noted that the SEC should require that “ESG pay for performance measures be standardized in alignment with other SEC proposals currently or soon under consideration.” Similarly, the Responsible Asset Allocator Initiative at New America, in arguing for inclusion of ESG metrics in the pay vs performance rule, stated that “to avoid greenwashing, the metrics should be material to the company and to its industry, as defined by internationally recognized standards setting organizations …”

The last year has witnessed a number of proposals aimed at providing standardized reporting of ESG metrics. Below are two of the most prominent recent developments in the area:

ACTION ITEMS FOR INCORPORATING ESG METRICS

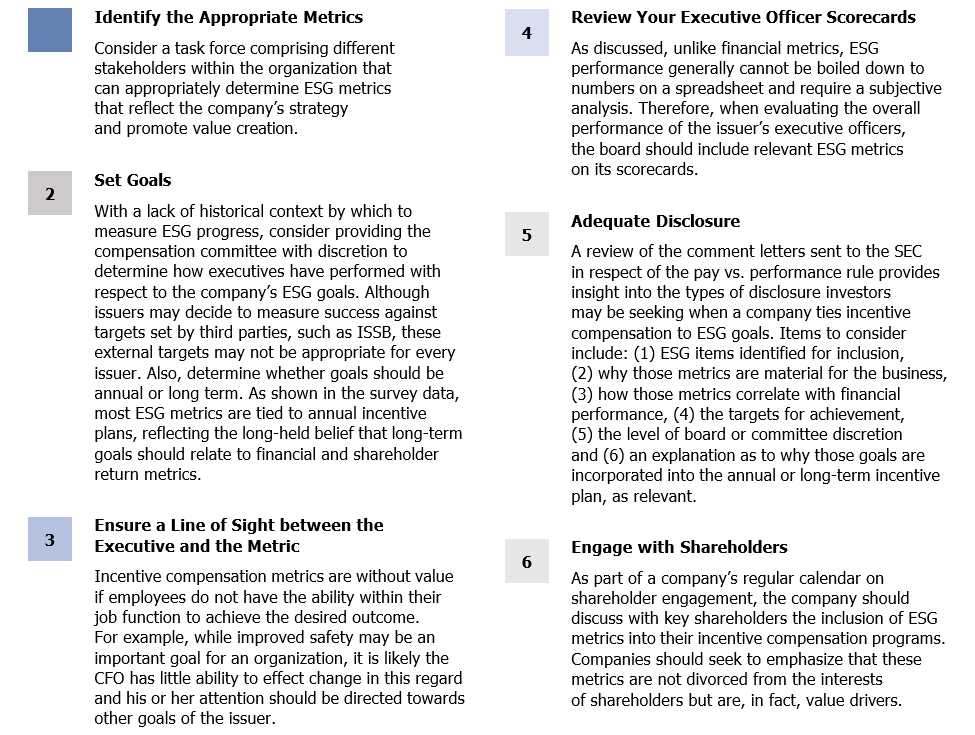

The following is a list of action items for companies looking to incorporate ESG metrics into their incentive compensation programs and provide related disclosure that will go towards satisfying investors:

The DOL’s Rules on ESG Investing for ERISA Plans — The Pendulum Swings AgainIn promulgating its proposed rule on climate-related disclosures, the SEC characterized the proposal not as an ESG proposal, but rather as one aimed at providing information on risks that are reasonably likely to have a material impact on business, results of operations or finances. The debate over the economic relevance of ESG factors is perhaps most notable, however, at the Department of Labor (DOL), where each new administration offers its own set of guidance or rules as to the extent to which ERISA plan fiduciaries may consider ESG factors when making plan investments. In December of 2020, the DOL published a final rule with respect to ESG investing in the ERISA context. Purporting to reflect the DOL’s long-standing position that ERISA fiduciaries may not sacrifice investment returns in order to promote social, environmental or other policy goals, ESG factors may be considered only to the extent they present material economic risks or opportunities. In addition, if two alternative investments appear economically indistinguishable, a fiduciary may “break the tie” by relying on ESG factors. Because, however, the DOL (at that time) believed true ties rarely exist, a fiduciary must document the basis for concluding that the investment alternatives were indistinguishable. Upon taking office, the Biden administration swiftly announced that it would not enforce the December 2020 rule and, in October of 2021, promulgated its own proposed rule intended to eliminate concerns surrounding investments in ESG funds that are economically advantageous. Echoing guidance issued under previous Democrat administrations, the proposed rule explicitly acknowledges that consideration of the projected return of a portfolio may require an evaluation of ESG factors. |

Endnotes

1See J.A. Brown & W.R. Forster, “CSR and Stakeholder Theory: A Tale of Adam Smith,” Journal of Business Ethics, at 112, 301–312, https://link.springer.com/article/10.1007/s10551- 012-1251-4 (2013).(go back)

2See L A. Bebchuk, & R. Tallarita, “The Perils and Questionable Promise of ESG-Based Compensation,” Forthcoming, Journal of Corporation Law (2022) Harvard Law School Program on Corporate Governance Working Paper 2022–3, https://ssrn.com/ abstract=4048003 or http://dx.doi.org/10.2139/ ssrn.4048003 (March 4, 2022).(go back)

3The final rule requires disclosure of the company’s net income and a company-selected financial performance measure. In addition, the company must list at least three, and up to seven, financial measures used to link compensation to performance.(go back)

4See Hester Peirce, “Rethinking Global ESG Metrics,” Views — the Eurofi Magazine, at 208, https://www.sec.gov/news/public-statement/rethinking-global-esg-metrics (April 14,2021).(go back)