Print

PrintMartha Carter is Vice Chair & Head of Governance Advisory, Sean Quinn is a Senior Managing Director, and Sydney Carlock is a Managing Director at Teneo. This post is based on a Teneo memorandum by Ms. Carter, Mr. Quinn, Ms. Carlock, and Matt Filosa. Related research from the Program on Corporate Governance includes Rationalizing the Dodd-Frank Clawback by Jesse M. Fried.

On October 28th 2022, the SEC adopted the final compensation-related rule of the Dodd Frank Act, requiring companies to recoup compensation that was previously awarded to certain executives based on false information.

Whereas companies were able to implement other Dodd-Frank compensation-related rules without fundamentally changing their pay plans (such as the CEO pay ratio disclosure requirements), the clawback rule requires the NYSE and NASDAQ to update their listing standards and issuers to adopt a specific policy that affects the amount of compensation executives will ultimately take home. The rule was published in the Federal Register on November 28, 2022,[1] and exchanges have 90 days to publish their revised listing standards to – be effective no later than November 28, 2023.

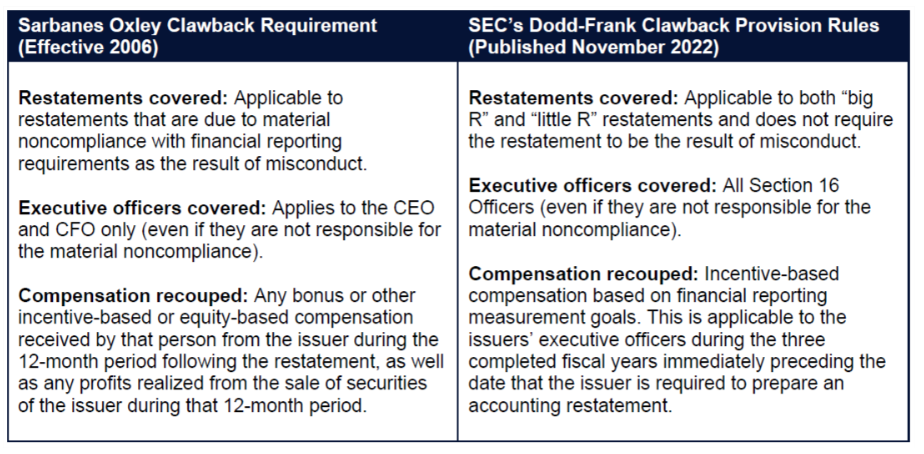

The new clawback requirements differ considerably from the prior clawback mandate under the Sarbanes-Oxley Act of 2002 which, in addition to implementing and reporting certain accounting controls, requires the recoupment of erroneously paid compensation to the CEO and CFO for material restatements resulting from misconduct (see Appendix). We believe this rule will have a significant impact on how compensation is structured and earned, with the largest potential implications highlighted below.

More Clawbacks

Most S&P 500 companies had a clawback policy in place prior to the SEC’s announcement. However, the new requirements are much more expansive than typical clawback provisions, applying in a wider variety of situations to a larger group of employees.

- Clawbacks will be required for more types of restatements, including restatements that are not material.

In addition to “big R” restatements[2], the rule also covers “little R” restatements, which correct errors that are seen as immaterial, and which typically do not require disclosure on an 8-K filing. According to the SEC, 76% of all restatements in 2020 were “little R” restatements. - A restatement does not need to be the result of fraud to trigger a clawback.

This contrasts with many existing clawback policies that apply to restatements resulting from fraud or misconduct. - The new rule applies to more executives than are covered under most existing policies.

All Section 16 Officers are covered under the SEC’s rule. Many existing policies apply only to certain NEOs, or those directly responsible for the restatement. - The use of compensation committee discretion is limited.

The rule states that issuers are not allowed to recoup less compensation than what was erroneously paid unless they prove that it is unrecoverable. While there is some leeway in how to recover compensation (e.g., setting up a deferred payment plan), there is less flexibility in determining whether to recover compensation.

Given these factors, clawbacks are poised to become far more prevalent, which may lead companies to tailor compensation design to avoid the logistical pitfalls and expenses associated with recoupment.

More Fixed or Time-Based Compensation (With More Shareholder Pushback)

Some have expressed concern that the possibility of recoupment lowers the perceived value of incentive compensation, creating retention risks for issuers. As a result, some companies are likely to increase the proportion of fixed, discretionary or time-based compensation, which is not subject to recoupment. However, doing so will result in pushback from shareholders and other stakeholders. Investors and proxy advisors have been clear that they have little appetite for a reduction in performance-based compensation without a commensurate reduction in magnitude, even if there is a change in the regulatory environment[3].

More Mandatory Deferrals or Extended Vesting

The logistics of recouping paid compensation can prove challenging under the rule, which will likely lead some companies to defer payment of some or all earned incentives. The clawback rule applies to compensation earned in the three-year lookback period on a pre-tax basis, meaning that executives will have to pay back the full pre-tax amount even if they have paid taxes on it; a clawback could result in a net loss to the executive. Deferring the payment of earned compensation until after the lookback period could prevent executives experiencing additional financial burden in the event of a restatement and avoid the logistical headaches of recouping compensation that has already been paid.

More Tax Gross-Ups Paid to Executives

Because erroneously paid compensation is to be recouped on a pre-tax basis, it is likely that some companies will provide a tax gross-up payment to executives who would otherwise face a net loss as a result of the clawback. Proxy advisors and investors oppose gross-ups in many instances and may raise concerns of the additional compensation expense associated with these payments.

More ESG-Based Compensation

The rule applies to compensation that is based on the achievement of a financial reporting measurement goal, including non-GAAP financial goals. Compensation that is paid at the compensation committee’s discretion (unless it is paid from a bonus pool that is determined funded based on a financial metric) or compensation that is tied to strategic or subjective metrics is not subject to recoupment under the new rule. As previously noted, shareholders and proxy advisors will likely have little tolerance for significant increases in discretionary compensation. Quantitative ESG metrics and other quantifiable non-financial metrics are not included in the rule but do not raise investor concern associated with overreliance on discretion. As such, we may see an increase in both their usage and the portion of incentive compensation that they determine.

More Complications Around TSR and Stock Price Goals

The SEC has stated that the rule encompasses incentive-based compensation tied to TSR and stock price “because improper accounting affects such measures and, in turn, results in excess compensation,” noting that “big R” restatements are more likely to have a stock price impact. Determining the impact of the error that led to the restatement on stock price could prove challenging, involving costly and complicated analyses. As the SEC does not provide prescriptive guidance on performing these calculations, issuers are to use reasonable estimates to determine the amount of compensation to recoup in this situation – and they must disclose the methodology they use. As TSR and stock price are ubiquitous in stock plans, issuers are unlikely to (and should not) do away with these metrics in incentive plans altogether. However, companies that are faced with these complicated analyses following a restatement may be less likely to include stock price or TSR metrics in plans in the future.

More Opportunity for Activist Criticism

Companies are required to disclose not only their clawback policy, but also information about amounts they have recouped or have yet to recoup following a restatement. Among other things, issuers must disclose the aggregate amounts recouped that year, as well as, for each executive, the amounts that have yet to be recouped that were outstanding for 180 days or longer since the date the issuer determined the amount owed. Companies with high outstanding amounts awaiting recoupment risk drawing criticism from activists and other shareholder groups.

In Conclusion

While it may be a case of the tail wagging the dog, the new clawback rule will likely create a shift in how executive compensation is structured and paid to mitigate the logistical challenges of recoupment. Some solutions are shareholder friendly (payment deferrals and increased use of ESG metrics), while others (increasing discretionary and / or time-based compensation, gross-up provisions) could invite shareholder and proxy advisor criticism, ultimately impacting say-on-pay and compensation committee vote results.

While companies may not be required to implement clawback policies until early 2024, the upcoming proxy season will draw additional scrutiny of pay-performance linkage given the SEC’s new pay-for-performance rules – as well as the looming recession.

As such, companies should carefully consider how any changes to pay structure will be received by various stakeholders (including investors and proxy advisors) and make sure the proxy disclosure regarding these changes is tailored to an investor audience.

Appendix

Endnotes

1The final rules were published in the Federal Register on November 28, 2022. The rule requires each exchange to file its proposed listing standards within 90 days of this date (February 26, 2023). These listing standards must be effective within one year of the publication date (November 28, 2023). Issuers will be required to adopt a compliant recovery policy within 60 days of this (January 27, 2024 at the latest)(go back)

2“Big R” restatements correct errors that are material to previously issued financial statements. “Little R” restatements correct errors that are not material to previously issued financial statements but would result in a material misstatement if (a) the errors were left uncorrected in the current report or (b) the error correction was recognized in the current period.(go back)

3For instance, when the 2017 Tax Cuts and Jobs Act removed the tax deductibility of non-performance-based compensation (as opposed to the previous $1 million threshold for fixed pay), the few companies that significantly increased fixed compensation came under intense scrutiny from investors and proxy advisors.(go back)