Print

PrintMartha Carter is Vice Chair & Head of Governance Advisory, Matt Filosa and Sean Quinn are Senior Managing Directors at Teneo. This post is based on a Teneo memorandum by Ms. Carter, Mr. Filosa, Mr. Quinn, and Sydney Carlock. Related research from the Program on Corporate Governance includes The Agency Problems of Institutional Investors (discussed on the Forum here) by Lucian Bebchuk, Alma Cohen, and Scott Hirst; Index Funds and the Future of Corporate Governance: Theory, Evidence, and Policy (discussed on the Forum here) by Lucian Bebchuk and Scott Hirst; The Specter of the Giant Three (discussed on the Forum here) by Lucian Bebchuk and Scott Hirst; and The Limits of Portfolio Primacy (discussed on the Forum here) by Roberto Tallarita.

Earlier this year, Republican Senators introduced the “INDEX” Act that would require passively managed funds to vote proxies in accordance with the instructions from their clients. The proposed bill followed the announcement of BlackRock’s “Voting Choice” initiative that provides clients the option to vote proxies themselves. Vanguard and SSGA have announced similar initiatives that provide clients with more voting choices, and Institutional Shareholder Services (ISS) has launched a service to help other asset managers do the same. While the INDEX Act is intended to lessen the influence of large asset managers over corporate affairs, these investor proxy voting initiatives are meant to promote greater shareholder democracy. We can expect more asset managers to implement similar voting options for their clients to keep up with their peers. These initiatives are likely to have a significant impact on companies – from shareholder engagement strategies and voting outcomes to other stakeholders such as the media.

Defining “Pass-Through” Voting: What’s New and What’s Not New?

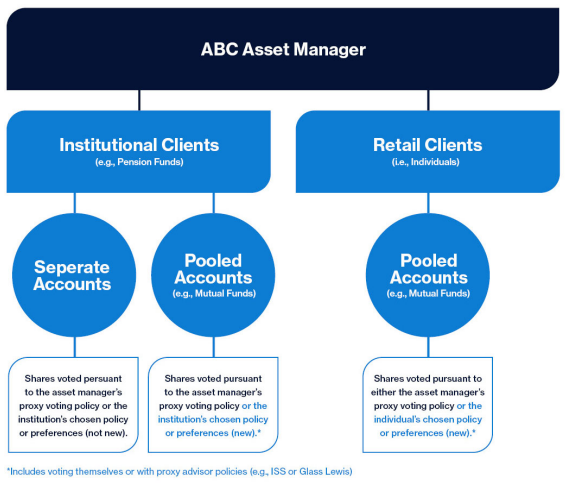

Institutions with “separate” accounts have always had the option to vote.

Asset managers hold institutional investor client assets in either “separate” accounts (with no other investors) or “pooled” accounts (with other investors). Institutional clients that have separate accounts have always had the option to vote proxies themselves, although historically most have not.[1] Instead, many of these institutions have opted to vote pursuant to the asset manager’s proxy policy because they did not have the staff, expertise or access to technological capabilities to vote proxies themselves. However, increasing scrutiny of proxy votes along with technological advancements may increase the number of institutions in “separate” accounts that choose to vote proxies themselves.

Institutions in “pooled” accounts now have the option to vote.

Institutional clients that have “pooled” accounts, such as indexed mutual funds, do not own the shares of companies held in the mutual fund – it is the asset manager that owns the shares. As such, the asset manager has historically voted these shares without input from the underlying institutional client. However, as they already do with “separate” accounts, asset managers are now offering institutional clients in pooled vehicles the ability to vote proxies themselves (please see graphic in the Appendix). These initiatives seem to be gaining traction: BlackRock recently reported that $157 billion of institutional assets invested in indexed mutual funds have elected to vote proxies since its Voting Choice program launched earlier this year – almost 10% of eligible institutional assets.

Individuals in “pooled” accounts will soon have the option to vote.

The other significant new development is that BlackRock, Vanguard and other asset managers have indicated that these voting options will soon be available to retail investors – individuals invested in mutual funds via their retirement or other savings plans. While retail investors have not traditionally voted at the same rate as institutions, approximately 25% of retail investors do vote proxies currently – not an insignificant number. And this number could increase if proxy voting continues to be made simpler and easier for individual investors not only in the U.S. but also in Europe, where the voting choice concept originated a few years ago.

Potential Consequences for Companies

1. “Empty” engagement

An asset manager that owns 10% of a company’s shares may not have proxy voting power for all 10% of those shares. As described above, this is not a new concept. But asset managers seem to be intent on lowering the percentage of shares for which they have voting power to promote shareholder democracy. How much lower is anyone’s guess. For example, an asset manager that owns 10% of a company’s stock may eventually only control the vote for 6% of the shares. How should companies weigh that asset manager’s views on an issue? How will companies locate and engage with that 4% of the votes determined by the asset manager’s clients?

Given that votes on shareholder proposals, Say on Pay and proxy contests can be won or lost on thin margins, company engagement programs will need to be refreshed regularly to ensure they are reaching the ultimate decision makers, including retail investors. Companies may also choose more targeted disclosure via supplemental filings and/or social media messaging.

2. Back to the future

There was an intense debate years ago about whether asset managers were abdicating their fiduciary responsibility by simply following the voting recommendations of proxy advisory firms. Despite disclosures from asset managers to the contrary, regulatory and legal debates over the impact of proxy advisory firms continue today. Yet the voting options being put forth by asset managers for their clients all include an option to automatically vote pursuant to a proxy advisory firm voting policy – including voting policies that are more progressive than the standard proxy advisor voting policies (e.g., ISS Climate Voting Policy). If this form of shareholder democracy gains additional traction among asset manager clients, proxy advisory firms could gain greater influence over voting outcomes at company shareholder meetings.

3. Power to the people

Over the past few years, retail investors have rallied together online to support the stock prices of companies like GameStop and AMC Entertainment. These “meme stocks” demonstrated the power of retail investors to overcome their historical apathy and impact corporate America through viral online campaigns in a way never seen before. If retail investors in mutual funds have greater power to vote proxies, they could also start online campaigns that seek to impact voting outcomes – especially if voting is made simple and easy by the asset managers through which they are invested. Activist investors may also see an opportunity to gain the support of the newly empowered retail investors in their proxy campaigns, especially those relating to ESG issues where individual investors may have a more populist view than institutions (e.g., executive compensation). Considering all of this, engagement with retail investors will likely become much more important for companies.

4. Misinformation campaigns

As described above, products that help individual investors exercise these newly acquired voting options are increasingly being launched in the marketplace. Ensuring the accuracy of company information included in these products and on social media platforms will be a high priority for companies to address any misperceptions or misinformation campaigns directed against them.

In addition, a company will now need to develop communications plans to educate those individual and institutional shareholders not previously included in its engagement program to ensure clear and accurate understanding. We can also expect that ESG issues such as climate and diversity will be in the spotlight – adding to the importance that companies clearly communicate their ESG strategy to critical stakeholders, including the media.

What Happens Next?

At this point, there are more questions than answers on the potential impacts that “pass-through” voting will have on companies. But these initiatives are gaining momentum, and we believe that companies will need to make adjustments to their investor engagement strategies in the coming years. Companies should closely monitor the developments of “pass-through” voting, as well as other related initiatives such as universal proxies and greater executive compensation disclosure, for their potential impact on future shareholder engagement and annual shareholder meetings.

Appendix

A simple “pass-through” proxy voting diagram

Endnotes

1Because institutions with separate accounts directly own the shares of the companies invested in the fund, this is technically not “pass through” voting.(go back)