Print

PrintLaura Sanderson co-leads the Board and CEO Advisory Partners in Europe and Sarah Galloway is co-head of the Global Sustainability Practice at Russell Reynolds Associates. This post is based on a Russell Reynolds Associates memorandum by Ms. Sanderson, Ms. Galloway, Louise Belloin, Molly Conte, Beth Hawley, and Emily Meneer. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) and Does Enlightened Shareholder Value Add Value? (discussed on the Forum here) both by Lucian A. Bebchuk and Roberto Tallarita; Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy—A Reply to Professor Rock (discussed on the Forum here) by Leo E. Strine, Jr.; Stakeholder Capitalism in the Time of Covid (discussed on the Forum here) by Lucian A. Bebchuk, Kobi Kastiel, and Roberto Tallarita; and Corporate Purpose and Corporate Competition (discussed on the Forum here) by Mark J. Roe.

The business case for sustainability has never been stronger

Organizations are under increasing pressure to create holistic approaches to sustainability and broader Environmental, Social and Governance (ESG) strategies to meet regulatory requirements and societal and investor expectations. At the same time, sustainability also presents an enormous opportunity for value creation to those that develop more sustainable products or solutions.

Russell Reynolds Associates examined the role boards can play in activating sustainability across their organization, setting out:

- The importance of forging a collaborative relationship with the management team

- The four key areas of board responsibility when it comes to sustainability

- Actionable recommendations and examples of implementing effective sustainability oversight

An increasing number of companies are in the process of transforming their business and operating models to deliver sustainable value to their customers, employees, investors, and the wider societal context in which they operate. However, most boards and management teams are struggling with this transition.

Activating sustainable leadership requires a high degree of coordination, starting with the board and senior leadership becoming aligned on the sustainability vision and roadmap, and allowing next-generation leaders and front-line employees to become conduits for embedding the sustainability agenda into the fabric of the organization. This results in more unified messaging when interfacing with customers, suppliers, and other external stakeholders.

Why boards and management teams need to work together on sustainability

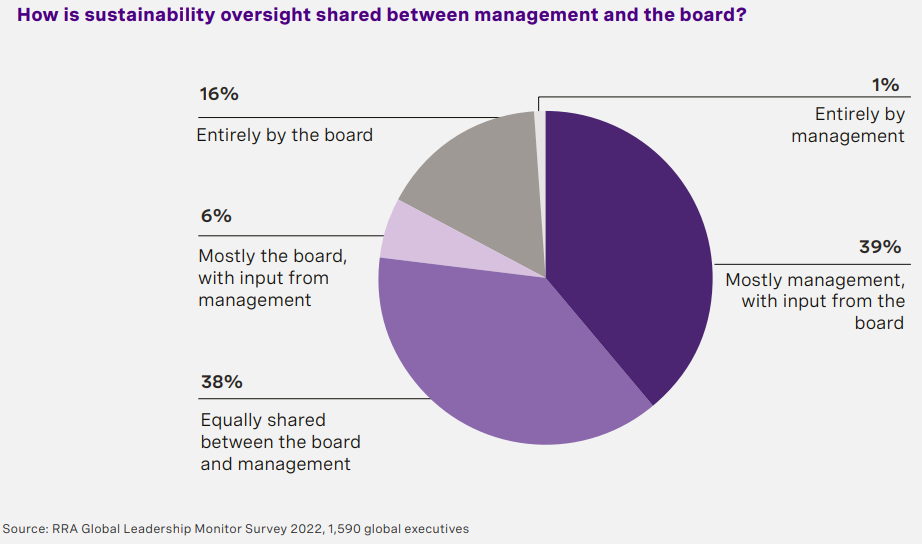

RRA’s 2021 research on the board’s role in sustainable leadership found that a collaborative relationship between the board and management team is essential to achieving sustainability targets. This was confirmed in RRA’s 2022 Global Leadership Monitor, a survey of 1,590 global executives, as the majority of leaders reported that responsibility for the sustainability strategy is shared across their organization’s leadership either 1) equally between the board and the management team, or 2) mostly within the management team with input from the board.

This highlights the need for board of directors and management collaboration when it comes to sustainability strategy and governance. When this partnership works well, sustainability initiatives are thoughtful and productive, eventually becoming fully integrated into the business over the long term. When the board and management struggle to reach alignment, sustainability efforts risk being disjointed or unsuccessful. While both parties are responsible for successful sustainability outcomes, the board’s responsibilities are distinct from management’s.

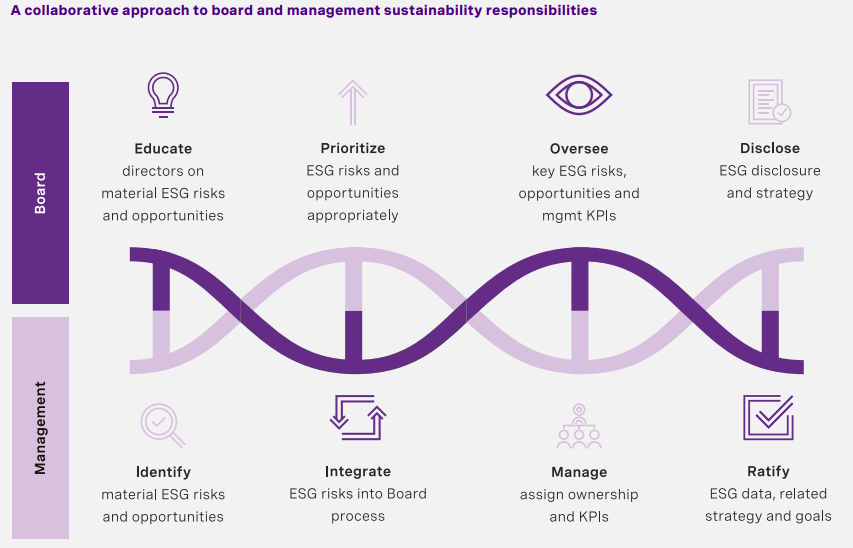

The four key board responsibilities for driving and governing sustainability

Board directors should focus their sustainability oversight broadly on four key responsibilities:

1. Educating

2. Integrating

3. Overseeing

4. Ratifying

| Regional, and local laws, as well as directives and corporate governance guidelines, must be considered as boards review and create new sustainable governance practices. |

Educate

Educate directors on material sustainability risks and opportunities to equip the board to productively contribute to their company’s sustainability strategy discussions.

With the increasing pressure on companies to deliver visible sustainability results, the board must be able to appropriately challenge the CEO and management on key strategic decisions regarding sustainability matters. The goal is not for the board to become sustainability experts, but rather to possess the baseline understanding of stakeholder expectations and how sustainability can create value and reduce risk.

The board should also be able to address questions across stakeholder groups, particularly shareholders, who are increasingly conscious of risks to their investments in companies that are not performing in terms of sustainability indicators. This is not just about appointing a standalone sustainability director. Ultimately everyone on the board must be able to engage in productive discussions around sustainability. This will require enabling directors to educate themselves.

Actions boards can take to educate directors:

1. Create dedicated sustainability training sessions: Organize dedicated training sessions on sustainability with external or internal specialists to provide deeper technical perspectives (e.g., independent external sustainability counsel).

2. Conduct materiality assessments: Consider conducting a materiality assessment to determine the specific sustainability factors that are of the most importance to the company and its key stakeholders. Holistic understanding of materiality is key. In some jurisdictions, companies should be conversant in the concept of “double materiality,” which looks at both the climate-related impacts on the company and at the company’s impacts on the climate and other dimensions of sustainability.[1]

3. Prioritize stakeholder engagement: Engage with critical stakeholders (investors, employees, customers, suppliers, and broader communities within which the company operates) on sustainability opportunities and risks to understand their priorities, challenges, and perceived opportunities.

4. Educate committee chairs and members on sustainability: The audit chair and members of the committee should be educated on sustainability reporting and the audit thereof. Equally, nomination committee members need to be educated in a way that enables them to appoint future board directors that bring relevant sustainability experience and skills. When codices require dedicated sustainability expertise on boards, leverage that expert to help educate and inform other board members.

5. Develop a shared sustainability framework: Discussions will be most effective if the board and management have a common sustainability framework and vocabulary

Case StudyA German MDAX constituent with revenues of approximately 10 billion euros organized multiple workshops with external advisors to further educate their board on sustainability. The workshops included presentations from a leading management consulting firm and from RRA on the role of the board in driving sustainable leadership. These workshops were part of the board’s ongoing journey to become more familiar with the strategic, governance and leadership challenges of sustainability and enable them to make informed decisions about how to oversee and ratify sustainability reporting more effectively. Moreover, it also helped them reflect on how they can work with management on driving forward the sustainability agenda and its associated value creation opportunities. |

Questions the board should ask itself:

|

Integrate

Integrate sustainability risks and objectives into board processes and internal control and risk management system.

Integrating sustainability into the board’s day-to-day responsibilities is critical to the governance of sustainability risks and opportunities, ensuring that sustainability matters are front and center for the company. The board must also comply with local corporate governance.

Actions boards can take to integrate sustainability into the board’s responsibilities:

1. Include sustainability in planning conversations: Make sustainability an integral and consistent part of the board’s and CEO’s agenda.

2. Fully integrate sustainability into the board’s process: Depending on the maturity of the company’s sustainability approach and other mechanisms to get sustainability issues front and center for the board, different models can be applied (e.g., creating a sustainability committee). Regardless of model, sustainability should ultimately be integrated fully into the board’s oversight of strategy and risk in all relevant settings.

3. Create accountability: Each committee should be held accountable for designated sustainability oversight responsibilities, in addition to integrating sustainability into the overall board’s agenda.

Sustainability committeesRequirements around dedicated sustainability/ESG committees vary by jurisdiction. Beyond regulatory requirements, the choice will depend upon the company’s specific context, board culture, industry, and regional norms. For example, 13% of S&P 500 companies[2] have a dedicated committee or a committee tackling ESG matters, versus 33% of the DAX 40[3] and 54% of FTSE 100.[4] However, a sustainability committee should not be considered a proxy for the company’s level of commitment to sustainability. Many companies that are considered leading in terms of sustainability have found it more effective to integrate the topic across the entirety of the board’s work, either in other committees or at the full board level, as opposed to having a standalone committee. |

Case StudyThe board of a Canadian TSX constituent that operates as an apparel manufacturer with a market cap of approximately CA$7.5 billion has been integrating sustainability factors throughout its responsibilities. They have prioritized codifying sustainability oversight in their Corporate Governance and Social Responsibility Committee charter and disclosing data for multiple external frameworks. This supports establishing clear goals and a communication strategy around those objectives. The board considers sustainability to be a key strategic growth pillar. |

Questions the board should ask itself:

|

Oversee

Oversee key sustainability risks, opportunities, and management’s KPIs on an ongoing basis and in close partnership with the management team.

Incorporating sustainability strategy oversight into the board’s responsibilities is essential for staying aware of the company’s progress towards sustainability objectives and to provide appropriate feedback to management. Without intentional and regular board review of activity, progress, and outcomes, sustainability cannot be meaningfully integrated into strategic decisions.

Actions boards can take to oversee sustainability progress:

1. Set clear metrics: Agree on clear metrics with the management team to track progress towards established goals. Be transparent about progress and highlight potential or new hurdles on the journey. Establish board norms of reviewing sustainability and other non-financial metrics as regularly as the board reviews financials.

2. Discuss progress frequently: Discuss progress on sustainability measures at every board meeting, as well as with the CEO and management team. Encourage regular sustainability updates from management, establishing direct lines of communication from executives leading ESG initiatives, where appropriate and agreed upon by the CEO.

3. Stay informed about risks and opportunities: Stay informed about the evolution of sustainability risks and opportunities and encourage sharing on related topics. Pay attention to the internal control and risk management systems, which should incorporate sustainability-related risks. This should include the processes and systems for recording and processing sustainability-related data.

4. Integrate sustainability into culture oversight: Consider the board’s oversight of company culture and develop an understanding of the extent of employee alignment on sustainability issues throughout all levels of the organization to identify any potential gaps.

Case StudyAn American NYSE constituent in the organic food distribution industry with a market cap of over $1 billion reviews, at least annually, the company’s policies and strategies addressing environmental, social and governance concerns, including sustainability and corporate responsibility, from a corporate governance standpoint and recommends any modifications to address evolving requirements of various stakeholders. |

Questions the board should ask itself:

|

Ratify

Ratify management’s sustainability metrics and related disclosures.

The board is accountable for sustainability disclosures, which enables the company to showcase its commitments and progress to investors, customers, employees, and policymakers.

Actions boards can take to oversee sustainability progress:

1. Communicate the sustainability journey: Validate and visibly champion decisions made by the management team regarding the sustainability journey.

2. Report on sustainability metrics: Include reporting on sustainability progress and in appropriate disclosures, either as stand-alone reports or incorporated into other disclosures, such as the annual report. Sign-off on major sustainability commitments and be accountable for them in front of all stakeholders.

3. Prioritize compliance and audit of sustainability goals: Confirm the accuracy of non-financial reporting and public market disclosures, potentially including a third-party audit of such information. Evaluate oversight processes for compliance with relevant local corporate governance codes and laws.

4. Proactively monitor for sustainability-related risks: Proactively monitor and prepare for any new reporting requirements on the horizon.

Case StudyNovo Nordisk is a leading healthcare business headquartered in Denmark, with revenues of $22 billion. For decades, sustainability has been a priority for Novo Nordisk and the topic is owned by the entire board. The board makes all key decisions on sustainability and is involved in strategy discussions and solving hard business issues. Executives proactively reach out to and engage with board members on their specific areas of expertise. The company has a set of 10 guiding principles, The Novo Nordisk Way, which underpin every key decision. The company uses a facilitation approach to ensure that the entire company lives up to the Novo Nordisk Way. Issues are addressed locally, and a consolidated report is shared with the board and management. Since 2004, Novo Nordisk has published one integrated annual report covering their financial, environment and social statement, as well as management review. The ESG reporting is in accordance with relevant disclosure standards, including those of the IFRS Foundation, the Taskforce on Climate-related Financial Disclosures (TCFD) and the Carbon Disclosure Project (CDP). |

Questions the board should ask itself:

|

Recommendations to fully integrate sustainability into board governance processes

Implement temporary multi-committee responsibility

Governing and overseeing sustainability is the responsibility of the entire board. However, to achieve this, companies might need a temporary structure while integrating sustainability practices into the board.[5] The model that requires the least structural change, while also distributing responsibility across several groups of non-executive directors, is the multi-committee responsibility model.

Under this model, each committee on the board integrates sustainability into their responsibilities. When this model is employed, take care to ensure that sustainability items that don’t clearly fit into an existing committee remit do not fall through the cracks, and that the overall approach to sustainability oversight is consistent and harmonious.

Case StudyLinde PLC is a global multinational industrial gas and engineering company with sales of $31 billion in 2021. The board’s oversight of ESG risks and opportunities is integral to their business strategy. As stated in their 2022 Proxy Statement, the board and its committees actively oversee Linde’s ESG strategy, programs, and policies, which are managed on a day-to-day basis by senior executives. The board revised certain committee charters to specify ESG programs and practices. In 2021, Linde undertook a comprehensive review of its ESG program and practice oversight, resulting in several actions to increase board oversight:

|

Cultivate a sustainable mindset in current and future board directors

Cultivate a sustainable mindset among existing board directors by investing in education on sustainability as it pertains to the industry and company. This education also includes understanding the respective stakeholder groups’ concerns and wishes, which are key to the business’s sustainability transformation. When appointing new directors, rather than selecting a dedicated sustainability specialist, appoint directors with a sustainable mindset and with skills relevant to the company’s sustainability challenges and opportunities to infuse sustainable leadership across the board.

Integrate sustainability into organizational culture

Fully integrating sustainability into a business requires a major cultural transformation. Like other transformation efforts, board oversight is critical. Today, sustainability represents a significant value creation opportunity in its broadest sense for people, planet, and profits. To fully capture this value creation opportunity, there must be organizational alignment around ambition, strategy, culture, and internal and external communications. Sustainability impacts the entire organization and the ecosystem in which it functions—boards need to be exposed to all material aspects.

Endnotes

1Double materiality’: what is it and why does it matter? – Grantham Research Institute on climate change and the environment (lse.ac.uk)(go back)

2Navigating The ESG Journey In 2022 And Beyond | Deloitte US;(go back)

3DAX Supervisory Boards Include More Women Than Ever | Russell Reynolds Associates(go back)

4Mattison Public Relations | More than half of FTSE 100 companies now have a board-level ESG committee – the next metric in ESG corporate comms(go back)

5Ron Soonieus, “Designing Sustainability Governance: Board structures and practices for better ESG performance,” INSEAD Corporate Governance Centre, March 2022.(go back)