Print

PrintSandy Boss is Global Head of Investment Stewardship, John Roe is Head of Investment Stewardship (BIS) in the Americas, and Jessica McDougall is a Director at BlackRock Inc. This post is based on their BlackRock memorandum.

These guidelines should be read in conjunction with the BlackRock Investment Stewardship Global Principles.

Introduction

As stewards of our clients’ investments, BlackRock believes it has a responsibility to engage with management teams and/or board members on material business issues and, for those clients who have given us authority, to vote proxies in the best long-term economic interests of their assets.

The following issue-specific proxy voting guidelines (the “Guidelines”) summarize BlackRock Investment Stewardship’s (“BIS”) philosophy and approach to engagement and voting, as well as our view of governance best practices and the roles and responsibilities of boards and directors for publicly listed U.S. companies. These Guidelines are not intended to limit the analysis of individual issues at specific companies or provide a guide to how BIS will engage and/or vote in every instance. They are to be applied with discretion, taking into consideration the range of issues and facts specific to the company, as well as individual ballot items at shareholder meetings.

Voting guidelines

These guidelines are divided into eight key themes, which group together the issues that frequently appear on the agenda of shareholder meetings:

- Boards and directors

- Auditors and audit-related issues

- Capital structure

- Mergers, acquisitions, asset sales, and other special transactions

- Executive compensation

- Material sustainability-related risks and opportunities

- General corporate governance matters

- Shareholder protections

Boards and directors

An effective and well-functioning board is critical to the economic success of the company and the protection of shareholders’ interests, inducting the establishment of appropriate governance structures that facilitate oversight of management and the company’s strategic initiatives. As part of their responsibilities, board members owe fiduciary duties to shareholders in overseeing the strategic direction, operations, and risk management of the company. For this reason, BIS sees engagement with and the election of directors as one of our most critical responsibilities.

Disclosure of material issues that affect the company’s long-term strategy and value creation, including, when relevant, material sustainability-related factors, is essential for shareholders to appropriately understand and assess how effectively the board is identifying, managing, and mitigating risks.

Where a company has not adequately demonstrated, through actions and/or disclosures, how material issues are appropriately identified, managed, and overseen, we will consider voting against the re-election of those directors responsible for the oversight of such issues, as indicated below.

Independence

It is our view that a majority of the directors on the board should be independent to ensure objectivity in the decision-making of the board and its ability to oversee management. In addition, all members of audit, compensation, and nominating/governance committees should be independent. Our view of independence may vary from listing standards.

Common impediments to independence may include:

- Employment as a senior executive by the company or a subsidiary within the past five years

- An equity ownership in the company in excess of 20%

- Having any other interest, business, or relationship (professional or personal) which could, or could reasonably be perceived to, materially interfere with the director’s ability to act in the best interests of the company and its shareholders

We may vote against directors who we do not consider to be independent, including at controlled companies, when we believe oversight could be enhanced with greater independent director representation. To signal our concerns, we may also vote against the chair of the nominating/governance committee, or where no chair exists, the nominating/governance committee member with the longest tenure.

Oversight role of the board

The board should exercise appropriate oversight of management and the business activities of the company. Where we determine that a board has failed to do so in a way that may impede a company’s long-term value, we may vote against the responsible committees and/or individual directors.

Common circumstances are illustrated below:

- Where the board has failed to facilitate quality, independent auditing or accounting practices, we may vote against members of the audit committee

- Where the company has failed to provide shareholders with adequate disclosure to conclude that appropriate strategic consideration is given to material risk factors (including, where relevant, sustainability factors), we may vote against members of the responsible committee, or the most relevant director

- Where it appears that a director has acted (at the company or at other companies) in a manner that compromises their ability to represent the best long-term economic interests of shareholders, we may vote against that individual

- Where a director has a multi-year pattern of poor attendance at combined board and applicable committee meetings, or a director has poor attendance in a single year with no disclosed rationale, we may vote against that individual. Excluding exigent circumstances, BIS generally considers attendance at less than 75% of the combined board and applicable committee meetings to be poor attendance

- Where a director serves on an excessive number of boards, which may limit their capacity to focus on each board’s needs, we may vote against that individual. The following identifies the maximum number of boards on which a director may serve, before BIS considers them to be over-committed:

In addition, we recognize that board leadership roles may vary in responsibility and time requirements in different markets around the world. In particular, where a director maintains a Chair role of a publicly listed company in European markets, we may consider that responsibility as equal to two board commitments, consistent with our EMEA Proxy Voting Guidelines. We will take the total number of board commitments across our global policies into account for director elections.

Risk oversight

Companies should have an established process for identifying, monitoring, and managing business and material risks. Independent directors should have access to relevant management information and outside advice, as appropriate, to ensure they can properly oversee risk. We encourage companies to provide transparency around risk management, mitigation, and reporting to the board. We are particularly interested in understanding how risk oversight processes evolve in response to changes in corporate strategy and/or shifts in the business and related risk environment. Comprehensive disclosures provide investors with a sense of the company’s long-term risk management practices and, more broadly, the quality of the board’s oversight. In the absence of robust disclosures, we may reasonably conclude that companies are not adequately managing risk.

Board Structure

Classified board of directors/staggered terms

Directors should be re-elected annually; classification of the board generally limits shareholders’ rights to regularly evaluate a board’s performance and select directors. While we will typically support proposals requesting board de-classification, we may make exceptions, should the board articulate an appropriate strategic rationale for a classified board structure. This may include when a company needs consistency and stability during a time of transition, e.g., newly public companies or companies undergoing a strategic restructuring. A classified board structure may also be justified at non-operating companies, e.g., closed-end funds or business development companies (“BDC”),[3] in certain circumstances. However, in these instances, boards should periodically review the rationale for a classified structure and consider when annual elections might be more appropriate.

Without a voting mechanism to immediately address concerns about a specific director, we may choose to vote against the directors up for election at the time (see “Shareholder rights” for additional detail).

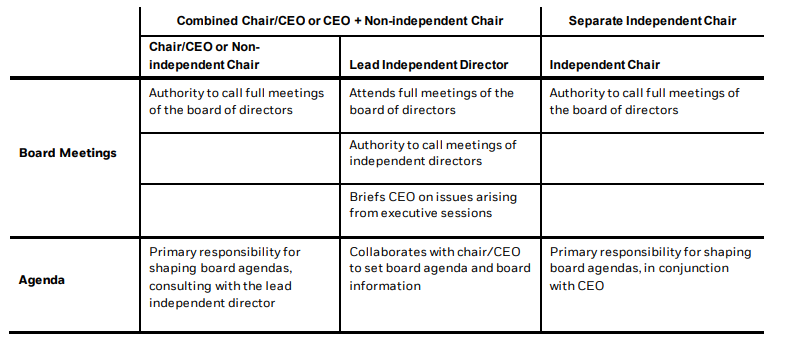

Independent leadership

There are two commonly accepted structures for independent leadership to balance the CEO role in the boardroom: 1) an independent Chair; or 2) a Lead Independent director when the roles of Chair and CEO are combined, or when the Chair is otherwise not independent.

In the absence of a significant governance concern, we defer to boards to designate the most appropriate leadership structure to ensure adequate balance and independence.[4] However, BIS may vote against the most senior non-executive member of the board when appropriate independence is lacking in designated leadership roles.

In the event that the board chooses to have a combined Chair/CEO or a non-independent Chair, we support the designation of a Lead Independent director, with the ability to: 1) provide formal input into board meeting agendas; 2) call meetings of the independent directors; and 3) preside at meetings of independent directors. These roles and responsibilities should be disclosed and easily accessible.

The following table illustrates examples[5] of responsibilities under each board leadership model:

CEO and management succession planning

Companies should have a robust CEO and senior management succession plan in place at the board level that is reviewed and updated on a regular basis. Succession planning should cover scenarios over both the long-term, consistent with the strategic direction of the company and identified leadership needs over time, as well as the short-term, in the event of an unanticipated executive departure. We encourage the company to explain their executive succession planning process, including where accountability lies within the boardroom for this task, without prematurely divulging sensitive information commonly associated with this exercise.

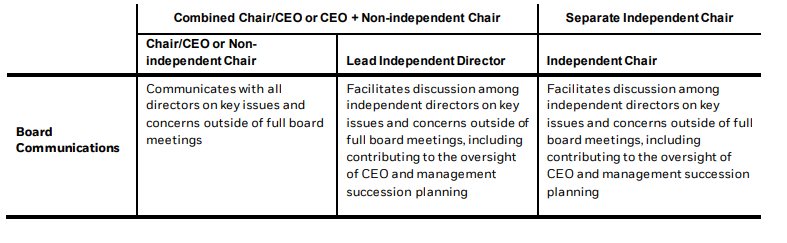

During a CEO transition, companies may elect for the departing CEO to maintain a role in the boardroom. We ask for disclosures to understand the timeframe and responsibilities of this role. In such instances, we typically look for the board to have appropriate independent leadership structures in place. (See chart above.)

Director compensation and equity programs

Compensation for directors should generally be structured to attract and retain directors, while also aligning their interests with those of shareholders. In our view, director compensation packages that are based on the company’s long-term value creation and include some form of long-term equity compensation are more likely to meet this goal.

Board composition and effectiveness

Director qualifications and skills

We encourage boards to periodically review director qualifications and skills to ensure relevant experience and diverse perspectives are represented in the boardroom. To this end, performance reviews and skills assessments should be conducted by the nominating/governance committee or the Lead Independent Director. This process may include internal board evaluations; however, boards may also find it useful to periodically conduct an assessment with a third party. We encourage boards to disclose their approach to evaluations, including objectives of the evaluation; if an external party conducts the evaluation; the frequency of the evaluations; and, whether that evaluation occurs on an individual director basis.

Board term limits and director tenure

Where boards find that age limits or term limits are the most efficient and objective mechanism for ensuring periodic board refreshment, we generally defer to the board’s determination in setting such limits. BIS will also consider the average board tenure to evaluate processes for board renewal. We may oppose boards that appear to have an insufficient mix of short-, medium-, and long-tenured directors.

Board diversity

As noted above, highly qualified, engaged directors with professional characteristics relevant to a company’s business enhance the ability of the board to add value and be the voice of shareholders in board discussions. In our view, a strong board provides a competitive advantage to a company, providing valuable oversight and contributing to the most important management decisions that support long-term financial performance.

It is in this context that we are interested in diversity in the boardroom. We see it as a means to promoting diversity of thought and avoiding ‘group think’ in the board’s exercise of its responsibilities to advise and oversee management. It allows boards to have deeper discussions and make more resilient decisions. We ask boards to disclose how diversity is considered in board composition, including professional characteristics, such as a director’s industry experience, specialist areas of expertise and geographic location; as well as demographic characteristics such as gender, race/ethnicity, and age.

We look to understand a board’s diversity in the context of a company’s domicile, market capitalization, business model, and strategy. Increasingly, we see leading boards adding members whose experience deepens the board’s understanding of the company’s customers, employees, and communities. Self identified board demographic diversity can usefully be disclosed in aggregate, consistent with local law. We believe boards should aspire to meaningful diversity of membership, at least consistent with local regulatory requirements and best practices, while recognizing that building a strong, diverse board can take time.

This position is based on our view that diversity of perspective and thought—in the boardroom, in the management team and throughout the company—leads to better long-term economic outcomes for companies. Academic and other research reveals correlations between specific dimensions of diversity and effects on decision-making processes and outcomes.[6] In our experience, greater diversity in the boardroom contributes to more robust discussions and more innovative and resilient decisions. Over time, greater diversity in the boardroom can also promote greater diversity and resilience in the leadership team, and the workforce more broadly. That diversity can enable companies to develop businesses that more closely reflect and resonate with the customers and communities they serve.

In the U.S., we believe that boards should aspire to at least 30% diversity of membership, [7] and we encourage large companies, such as those in the S&P 500, to lead in achieving this standard. In our view, an informative indicator of diversity for such companies is having at least two women and a director who identifies as a member of an underrepresented group.[8] We recognize that it may take time and that companies with smaller market capitalizations and in certain sectors may face more challenges in pursuing diversity. Among these smaller companies, we look for the presence of diversity and take into consideration the progress that companies are making.

In order to help investors understand overall diversity, we look to boards to disclose:

- How diversity, including demographic factors and professional characteristics, is considered in board composition, given the company’s long-term strategy and business model

- How directors’ professional characteristics, which may include domain expertise such as finance or technology, and sector- or market-specific experience, are complementary and link to the company’s long-term strategy

- The process by which candidates for board positions are identified, including whether professional firms or other resources outside of incumbent directors’ networks are engaged to identify and/or assess candidates, and whether a diverse slate of nominees is considered for all available board nominations

To the extent that, based on our assessment of corporate disclosures, a company has not adequately explained their approach to diversity in their board composition, we may vote against members of the nominating/governance committee. Our publicly available commentary provides more information on our approach to board diversity.

Board size

We typically defer to the board in setting the appropriate size and believe that directors are generally in the best position to assess the optimal board size to ensure effectiveness. However, we may vote against the appropriate committees and/or individual directors if, in our view, the board is ineffective in its oversight, either because it is too small to allow for the necessary range of skills and experience or too large to function efficiently.

Board responsiveness and shareholder rights

Shareholder rights

Where we determine that a board has not acted in the best interests of the company’s shareholders, or takes action to unreasonably limit shareholder rights, we may vote against the appropriate committees and/or individual directors. Common circumstances are illustrated below:

- The Independent Chair or Lead Independent Director, members of the nominating/governance committee, and/or the longest tenured director(s), where we observe a lack of board responsiveness to shareholders, evidence of board entrenchment, and/or failure to plan for adequate board member succession

- The chair of the nominating/governance committee, or where no chair exists, the nominating/governance committee member with the longest tenure, where board member(s) at the most recent election of directors have received against votes from more than 25% of shares voted, and the board has not taken appropriate action to respond to shareholder concerns. This may not apply in cases where BIS did not support the initial vote against such board member(s)

- The Independent Chair or Lead Independent Director and/or members of the nominating/governance committee, where a board fails to consider shareholder proposals that (1) receive substantial support, and (2) in our view, have a material impact on the business, shareholder rights, or the potential for long-term value creation

Majority vote requirements

Directors should generally be elected by a majority of the shares voted. We will normally support proposals seeking to introduce bylaws requiring a majority vote standard for director elections. Majority vote standards generally assist in ensuring that directors who are not broadly supported by shareholders are not elected to serve as their representatives. As a best practice, companies with either a majority vote standard or a plurality vote standard should adopt a resignation policy for directors who do not receive support from at least a majority of votes cast. Where the company already has a sufficiently robust majority voting process in place, we may not support a shareholder proposal seeking an alternative mechanism.

We note that majority voting may not be appropriate in all circumstances, for example, in the context of a contested election, or for majority-controlled companies or those with concentrated ownership structures.

Cumulative voting

As stated above, a majority vote standard is generally in the best long-term interests of shareholders, as it ensures director accountability through the requirement to be elected by more than half of the votes cast. As such, we will generally oppose proposals requesting the adoption of cumulative voting, which may disproportionately aggregate votes on certain issues or director candidates.

Auditors and audit-related issues

BIS recognizes the critical importance of financial statements to provide a complete and accurate portrayal of a company’s financial condition. Consistent with our approach to voting on directors, we seek to hold the audit committee of the board responsible for overseeing the management of the independent auditor and the internal audit function at a company.

We may vote against the audit committee members where the board has failed to facilitate quality, independent auditing. We look to public disclosures for insight into the scope of the audit committee responsibilities, including an over view of audit committee processes, issues on the audit committee agenda, and key decisions taken by the audit committee. We take particular note of cases involving significant financial restatements or material weakness disclosures, and we look for timely disclosure and remediation of accounting irregularities.

The integrity of financial statements depends on the auditor effectively fulfilling its role. To that end, we favor an independent auditor. In addition, to the extent that an auditor fails to reasonably identify and address issues that eventually lead to a significant financial restatement, or the audit firm has violated standards of practice, we may also vote against ratification.

From time to time, shareholder proposals may be presented to promote auditor independence or the rotation of audit firms. We may support these proposals when they are consistent with our views as described above.

Capital structure proposals

Equal voting rights

In our view, shareholders should be entitled to voting rights in proportion to their economic interests. In addition, companies that have implemented dual or multiple class share structures should review these structures on a regular basis, or as company circumstances change. Companies with multiple share classes should receive shareholder approval of their capital structure on a periodic basis via a management proposal on the company’s proxy. The proposal should give unaffiliated shareholders the opportunity to affirm the current structure or establish mechanisms to end or phase out controlling structures at the appropriate time, while minimizing costs to shareholders. Where companies are unwilling to voluntarily implement “one share, one vote” within a specified timeframe, or are unresponsive to shareholder feedback for change over time, we generally support shareholder proposals to recapitalize stock into a single voting class.

Blank check preferred stock

We frequently oppose proposals requesting authorization of a class of preferred stock with unspecified voting, conversion, dividend distribution, and other rights (“blank check” preferred stock) because they may serve as a transfer of authority from shareholders to the board and as a possible entrenchment device. We generally view the board’s discretion to establish voting rights on a when-issued basis as a potential anti-takeover device, as it affords the board the ability to place a block of stock with an investor sympathetic to management, thereby foiling a takeover bid without a shareholder vote.

Nonetheless, we may support the proposal where the company:

- Appears to have a legitimate financing motive for requesting blank check authority

- Has committed publicly that blank check preferred shares will not be used for anti-takeover purposes

- Has a history of using blank check preferred stock for financings

- Has blank check preferred stock previously outstanding such that an increase would not necessarily provide further anti-takeover protection but may provide greater financing flexibility

Increase in authorized common shares

Increase in authorized common shares BIS will evaluate requests to increase authorized shares on a case-by-case basis, in conjunction with industry-specific norms and potential dilution, as well as a company’s history with respect to the use of its common shares.

Increase or issuance of preferred stock

We generally support proposals to increase or issue preferred stock in cases where the company specifies the voting, dividend, conversion, and other rights of such stock and where the terms of the preferred stock appear reasonable.

Stock splits

We generally support stock splits that are not likely to negatively affect the ability to trade shares or the economic value of a share. We generally support reverse stock splits that are designed to avoid delisting or to facilitate trading in the stock, where the reverse split will not have a negative impact on share value (e.g., one class is reduced while others remain at pre-split levels). In the event of a proposal for are verse split that would not proportionately reduce the company’s authorized stock, we apply the same analysis we would use for a proposal to increase authorized stock.

Mergers, acquisitions, transactions, and other special situations

Mergers, acquisitions, and transactions

In assessing mergers, acquisitions, or other transactions– including business combinations involving Special Purpose Acquisition Companies (“SPACs”) – BIS’ primary consideration is the long-term economic interests of our clients as shareholders. Boards should clearly explain the economic and strategic rationale for any proposed transactions or material changes to the business. We will review a proposed transaction to determine the degree to which it has the potential to enhance long-term shareholder value. While mergers, acquisitions, asset sales, business combinations, and other special transaction proposals vary widely in scope and substance, we closely examine certain salient features in our analyses, such as:

- The degree to which the proposed transaction represents a premium to the company’s trading price. We consider the share price over multiple time periods prior to the date of the merger announcement. We may consider comparable transaction analyses provided by the parties’ financial advisors and our own valuation assessments. For companies facing insolvency or bankruptcy, a premium may not apply

- There should be clear strategic, operational, and/or financial rationale for the combination

- Unanimous board approval and arm’s-length negotiations are preferred. We will consider whether the transaction involves a dissenting board or does not appear to be the result of an arm’s-length bidding process. We may also consider whether executive and/or board members’ financial interests appear likely to affect their ability to place shareholders’ interests before their own, as well as measures taken to address conflicts of interest

- We prefer transaction proposals that include the fairness opinion of a reputable financial advisor assessing the value of the transaction to shareholders in comparison to recent similar transactions

Contested director elections and special situations

Contested elections and other special situations[9] are assessed on a case-by-case basis. We evaluate a number of factors, which may include: the qualifications and past performance of the dissident and management candidates; the validity of the concerns identified by the dissident; the viability of both the dissident’s and management’s plans; the ownership stake and holding period of the dissident; the likelihood that the dissident’s strategy will produce the desired change; and whether the dissident represents the best option for enhancing long-term shareholder value.

We will evaluate the actions that the company has taken to limit shareholders’ ability to exercise the right to nominate dissident director candidates, including those actions taken absent the immediate threat of a contested situation. BIS may take voting action against directors (up to and including the full board) where those actions are viewed as egregiously infringing on shareholder rights.

We will consider a variety of possible voting outcomes in contested situations, including the ability to support a mix of management and dissident nominees.

Poison pill plans

Where a poison pill is put to a shareholder vote by management, our policy is to examine these plans individually. Although we have historically opposed most plans, we may support plans that include a reasonable “qualifying offer clause.” Such clauses typically require shareholder ratification of the pill and stipulate a sunset provision whereby the pill expires unless it is renewed. These clauses also tend to specify that an all-cash bid for all shares that includes a fairness opinion and evidence of financing does not trigger the pill, but forces either a special meeting at which the offer is put to a shareholder vote or requires the board to seek the written consent of shareholders, where shareholders could rescind the pill at their discretion. We may also support a pill where it is the only effective method for protecting tax or other economic benefits that may be associated with limiting the ownership changes of individual shareholders. Lastly, we look for shareholder approval of poison pill plans within one year of adoption of implementation.

Reimbursement of expense for successful shareholder campaigns

We generally do not support shareholder proposals seeking the reimbursement of proxy contest expenses, even in situations where we support the shareholder campaign. Introducing the possibility of such reimbursement may incentivize disruptive and unnecessary shareholder campaigns.

Executive compensation

A company’s board of directors should put in place a compensation structure that balances incentivizing, rewarding, and retaining executives appropriately across a wide range of business outcomes. This structure should be aligned with shareholder interests, particularly the generation of sustainable, long-term value.

The compensation committee should carefully consider the specific circumstances of the company and the key individuals the board is focused on incentivizing. We encourage companies to ensure that their compensation plans incorporate appropriate and rigorous performance metrics, consistent with corporate strategy and market practice. Performance-based compensation should include metrics that are relevant to the business and stated strategy and/or risk mitigation efforts. Goals, and the processes used to set these goals, should be clearly articulated and appropriately rigorous. We use third party research, in addition to our own analysis, to evaluate existing and proposed compensation structures. We hold members of the compensation committee, or equivalent board members, accountable for poor compensation practices and/or structures.

There should be a clear link between variable pay and company performance that drives sustained value creation for our clients as shareholders. Where compensation structures provide for a front-loaded[10] award, we look for appropriate structures (including vesting and/or holding periods) that motivate sustained performance for shareholders over a number of years. We generally do not favor programs focused on awards that require performance levels to be met and maintained for a relatively short time period for payouts to be earned, unless there are extended vesting and/or holding requirements.

Compensation structures should generally drive outcomes that align the pay of the executives with performance of the company and the value received by shareholders. When evaluating performance, we examine both executive teams’ efforts, as well as outcomes realized by shareholders. Payouts to executives should reflect both the executive’s contributions to the company’s ongoing success, as well as exogenous factors that impacted shareholder value. Where discretion has been used by the compensation committee, we look for disclosures relating to how and why the discretion was used and how the adjusted outcome is aligned with the interests of shareholders. While we believe special awards[11] should be used sparingly, we acknowledge that there may be instances when such awards are appropriate. When evaluating these awards, we consider a variety of factors, including the magnitude and structure of the award, the scope of award recipients, the alignment of the grant with shareholder value, and the company’s historical use of such awards, in addition to other company-specific circumstances.

We acknowledge that the use of peer group evaluation by compensation committees can help calibrate competitive pay; however, we are concerned when the rationale for increases in total compensation is solely based on peer benchmarking.

We support incentive plans that foster the sustainable achievement of results – both financial and nonfinancial – consistent with the company’s strategic initiatives. Compensation committees should guard against contractual arrangements that would entitle executives to material compensation for early termination of their contract. Finally, pension contributions and other deferred compensation arrangements should be reasonable in light of market practices. Our publicly available commentary provides more information on our approach to executive compensation.

Where executive compensation appears excessive relative to the performance of the company and/or compensation paid by peers, or where an equity compensation plan is not aligned with shareholders’ interests, we may vote against members of the compensation committee.

“Say on Pay” advisory resolutions

In cases where there is a “Say on Pay” vote, BIS will respond to the proposal as informed by our evaluation of compensation practices at that particular company and in a manner that appropriately addresses the specific question posed to shareholders. Where we conclude that a company has failed to align pay with performance, we will vote against the management compensation proposal and relevant compensation committee members.

Frequency of “Say on Pay” advisory resolutions

BIS will generally support annual advisory votes on executive compensation. It is our view that shareholders should have the opportunity to express feedback on annual incentive programs and changes to long-term compensation before multiple cycles are issued. Where a company has failed to implement a “Say on Pay” advisory vote within the frequency period that received the most support from shareholders or a “Say on Pay” resolution is omitted without explanation, BIS may vote against members of the compensation committee.

Clawback proposals

We generally favor prompt recoupment from any senior executive whose compensation was based on faulty financial reporting or deceptive business practices. We also favor prompt recoupment from any senior executive whose behavior caused material financial harm to shareholders, material reputational risk to the company, or resulted in a criminal proceeding, even if such actions did not ultimately result in a material restatement of past results. This includes, but is not limited to, settlement agreements arising from such behavior and paid for directly by the company. We typically support shareholder proposals on these matters unless the company already has a robust clawback policy that sufficiently addresses our concerns.

Employee stock purchase plans

Employee stock purchase plans (“ESPP”) are an important part of a company’s overall human capital management strategy and can provide performance incentives to help align employees’ interests with those of shareholders. The most common form of ESPP qualifies for favorable tax treatment under Section 423of the Internal Revenue Code. We will typically support qualified ESPP proposals.

Equity compensation plans

BIS supports equity plans that align the economic interests of directors, managers, and other employees with those of shareholders. Boards should establish policies prohibiting the use of equity awards in a manner that could disrupt the intended alignment with shareholder interests, such as the excessive pledging or heading of stock. We may support shareholder proposals requesting the establishment of such policies

Our evaluation of equity compensation plans is based on a company’s executive pay and performance relative to peers and whether the plan plays a significant role in a pay-for-performance disconnect. We generally oppose plans that contain “evergreen” provisions, which allow for automatic annual increases of shares available for grant without requiring further shareholder approval; we note that the aggregate impacts of such increases are difficult to predict and may lead to significant dilution. We also generally oppose plans that allow for repricing without shareholder approval. We may oppose plans that provide for the acceleration of vesting of equity awards even in situations where an actual change of control may not occur. We encourage companies to structure their change of control provisions to require the termination of the covered employee before acceleration or special payments are triggered (commonly referred to as “double trigger” change of control provisions).

Golden parachutes

We generally view golden parachutes as encouragement to management to consider transactions that might be beneficial to shareholders. However, a large potential payout under a golden parachute arrangement also presents the risk of motivating a management team to support a sub-optimal sale price for a company.

When determining whether to support or oppose an advisory vote on a golden parachute plan, BIS may consider several factors, including:

- Whether we determine that the triggering event is in the best interests of shareholders

- Whether management attempted to maximize shareholder value in the triggering event

- The percentage of total premium or transaction value that will be transferred to the management team, rather than shareholders, as a result of the golden parachute payment

- Whether excessively large excise tax gross-up payments are part of the pay-out

- Whether the pay package that serves as the basis for calculating the golden parachute payment was reasonable in light of performance and peers

- Whether the golden parachute payment will have the effect of rewarding a management team that has failed to effectively manage the company

It may be difficult to anticipate the results of a plan until after it has been triggered; as a result, BIS may vote against a golden parachute proposal even if the golden parachute plan under review was approved by shareholders when it was implemented.

We may support shareholder proposals requesting that implementation of such arrangements require shareholder approval.

Option exchanges

There may be legitimate instances where underwater options create an overhang on a company’s capital structure and a repricing or option exchange may be warranted. We will evaluate these instances on a case-by-case basis. BIS may support a request to reprice or exchange underwater options under the following circumstances:

- The company has experienced significant stock price decline as a result of macroeconomic trends, not individual company performance

- Directors and executive officers are excluded; the exchange is value neutral or value creative to shareholders; tax, accounting, and other technical considerations have been fully contemplated

- There is clear evidence that absent repricing, employee incentives, retention, and/or recruiting may be impacted

BIS may also support a request to exchange underwater options in other circumstances, if we determine that the exchange is in the best interests of shareholders.

Supplemental executive retirement plans

BIS may support shareholder proposals requesting to put extraordinary benefits contained in supplemental executive retirement plans (“SERP”) to a shareholder vote unless the company’s executive pension plans do not contain excessive benefits beyond what is offered under employee-wide plans.

Material sustainability-related risks and opportunities

It is our view that well-run companies, where appropriate, effectively evaluate and manage material sustainability-related risks and opportunities[12] as a core component of their long-term value creation for shareholder and business strategy. At the board level, appropriate governance structures and responsibilities allow for effective oversight of the strategic implementation of material sustainability issues.

When assessing how to vote – including on the election of directors and relevant shareholder proposals – robust disclosures are essential for investors to understand, where appropriate, how companies are integrating material sustainability risks and opportunities across their business and strategic, long-term planning. Where a company has failed to appropriately provide robust disclosures and evidence of effective business practices, BIS may express concerns through our engagement and voting. As part of this consideration, we encourage companies to produce sustainability-related disclosures sufficiently in advance of their annual meeting so that the disclosures can be considered in relevant vote decisions.

We encourage disclosures aligned with the reporting framework developed by the Task Force on Climate related Financial Disclosures (TCFD), supported by industry-specific metrics, such as those identified by the Sustainability Accounting Standards Board (SASB), now part of the International Sustainability Standards Board (ISSB) under the International Financial Reporting Standards (IFRS)Foundation. [13] While the TCFD framework was developed to support climate-related risk disclosures, the four pillars of the TCFD – governance, strategy, risk management, and metrics and targets – are a useful way for companies to disclose how they identify, assess, manage, and oversee a variety of sustainability-related risks and opportunities. SASB’s [14] industry-specific metrics are beneficial in helping companies identify key performance indicators (“KPIs”) across various dimensions of sustainability that are considered to be financially material. We recognize that some companies may report using different standards, which may be required by regulation, or one of a number of private standards. In such cases, we ask that companies highlight the metrics that are industry- or company-specific.

We look to companies to:

- Disclose the identification, assessment, management, and oversight of material sustainability related risks and opportunities in accordance with the four pillars of TCFD

- Publish material, investor-relevant, industry-specific metrics and rigorous targets, aligned with SASB (ISSB) or comparable sustainability reporting standards

Companies should also disclose any material supranational standards adopted, the industry initiatives in which they participate, any peer group benchmarking undertaken, and any assurance processes to help investors understand their approach to sustainable and responsible business conduct.

Climate risk

It is our view that climate change has become a key factor in many companies’ long-term prospects. As such, as long-term investors, we are interested in understanding how companies may be impacted by material climate-related risks and opportunities—just as we seek to understand other business-relevant risks and opportunities—and how these factors are considered within their strategy in a manner that is consistent with the company’s business model and sector. Specifically, we look for companies to disclose strategies that they have in place that mitigate and are resilient to any material risks to their long-term business model associated with a range of climate-related scenarios, including a scenario in which global warming is limited to well below 2°C, and considering global ambitions to achieve a limit of 1.5°C. [15] It is, of course, up to each company to define their own strategy: that is not the role of BlackRock or other investors.

BIS recognizes that climate change can be challenging for many companies, as they seek to drive long-term value by mitigating risks and capturing opportunities. A growing number of companies, financial institutions, as well as governments, have committed to advancing decarbonization in line with the Paris Agreement. There is growing consensus that companies can benefit from the more favorable macroeconomic environment under an orderly, timely, and equitable global energy transition.[16] Yet, the path ahead is deeply uncertain and uneven, with different parts of the economy moving at different speeds.[17] Many companies are asking what their role should be in contributing to an orderly and equitable transition—in ensuring a reliable energy supply and energy security and in protecting the most vulnerable from energy price shocks and economic dislocation. In this context, we encourage companies to include in their disclosures a business plan for how they intend to deliver long-term financial performance through a transition to global net zero carbon emissions, consistent with their business model and sector.

We look to companies to disclose short-, medium-, and long-term targets, ideally science-based targets where these are available for their sector, for Scope 1 and 2 greenhouse gas emissions (GHG) reductions and to demonstrate how their targets are consistent with the long-term economic interests of their shareholders. Many companies have an opportunity to use and contribute to the development of low carbon energy sources and technologies that will be essential to decarbonizing the global economy over time. We also recognize that continued investment in traditional energy sources, including oil and gas, is required to maintain an orderly and equitable transition—and that divestiture of carbon-intensive assets is unlikely to contribute to global emissions reductions. We encourage companies to disclose how their capital allocation to various energy sources is consistent with their strategy.

At this stage, we view Scope 3 emissions differently from Scopes 1 and 2, given methodological complexity, regulatory uncertainty, concerns about double-counting, and lack of direct control by companies. While we welcome any disclosures and commitments companies choose to make regarding Scope 3 emissions, we recognize that these are provided on a good-faith basis as methodology develops. Our publicly available commentary provides more information on our approach to climate risk and the global energy transition.

Natural capital

The management of nature-related factors is increasingly a core component of some companies’ ability to generate sustainable, long-term financial returns for shareholders, particularly where a company’s strategy is heavily reliant on the availably of natural capital, or whose supply chains are exposed to locations with nature-related risks. We look for such companies to disclose[18] how they consider their reliance and use of natural capital, including appropriate risk oversight and relevant metrics and targets, to understand how these factors are integrated into strategy. We will evaluate these disclosures to inform our view of how a company is managing material nature-related risks and opportunities, as well as in our assessment of relevant shareholder proposals. Our publicly available commentary provides more information on our approach to natural capital.

Key stakeholder interests

In order to deliver long-term value for shareholders, companies should also consider the interests of their key stakeholders. While stakeholder groups may vary across industries, they are likely to include employees; business partners (such as suppliers and distributors); clients and consumers; government and regulators; and the constituents of the communities in which a company operates. Companies that build strong relationships with their key stakeholders are more likely to meet their own strategic objectives, while poor relationships may create adverse impacts that expose a company to legal, regulatory, operational, and reputational risks.

Companies should effectively oversee and mitigate material risks related to stakeholders with appropriate due diligence processes and board oversight. Where we determine that company is not appropriately considering their key stakeholder interests in a way that poses material financial risk to the company and its shareholders, we may vote against relevant directors or support shareholder proposals related to these topics. Our publicly available commentary provides more information on our approach.

Conversely, we note that some shareholder proposals seek to address topics that are clearly within the purview of certain stakeholders. For example, we recognize that topics around taxation and tax reporting are within the domain of local, state, and federal authorities. BIS will generally not support these proposals.

Human capital management

A company’s approach to human capital management (“HCM”) is a critical factor in fostering an inclusive, diverse, and engaged workforce, which contributes to business continuity, innovation, and long-term value creation. Consequently, we ask companies to demonstrate a robust approach to HCM and provide shareholders with disclosures to understand how their approach aligns with their stated strategy and business model.

Clear and consistent disclosures on these matters are critical for investors to make an informed assessment of a company’s HCM practices. Companies should disclose the steps they are taking to advance diversity, equity, and inclusion; job categories and workforce demographics; and their responses to the U.S. Equal Employment Opportunity Commission’s EEO-1 Survey. Where we believe a company’s disclosures or practices fall short relative to the market or peers, or we are unable to ascertain the board and management’s effectiveness in overseeing related risks and opportunities, we may vote against members of the appropriate committee or support relevant shareholder proposals. Our publicly available commentary provides more information on our approach to HCM.

Corporate political activities

Companies may engage in certain political activities, within legal and regulatory limits, in order to support public policy matters material to the companies’ long-term strategies. These activities can also create risks, including: the potential for allegations of corruption; certain reputational risks; and risks that arise from the complex legal, regulatory, and compliance considerations associated with corporate political spending and lobbying activity. Companies that engage in political activities should develop and maintain robust processes to guide these activities and mitigate risks, including board oversight.

We depend on companies to provide accessible and clear disclosures so that investors can easily understand how their political activities support their long-term strategy, including on stated public policy priorities. When presented with shareholder proposals requesting increased disclosure on corporate political activities, BIS will evaluate publicly available information to consider how a company’s lobbying and political activities may impact the company. We will also evaluate whether there is general consistency between a company’s stated positions on policy matters material to their strategy and the material positions taken by significant industry groups of which they are a member. We may decide to support a shareholder proposal requesting additional disclosures if we identify a material inconsistency or feel that further transparency may clarify how the company’s political activities support its long-term strategy. Our publicly available commentary provides more information on our approach to corporate political activities.

General corporate governance matters

IPO governance

Boards should disclose how the corporate governance structures adopted upon a company’s initial public offering (“IPO”) are in shareholders’ best long-term interests. We also ask boards to conduct a regular review of corporate governance and control structures, such that boards might evolve foundational corporate governance structures as company circumstances change, without undue costs and disruption to shareholders. In our letter on unequal voting structures, we articulate our view that “one vote for one share” is the preferred structure for publicly-traded companies. We also recognize the potential benefits of dual class shares to newly public companies as they establish themselves; however, these structures should have a specific and limited duration. We will generally engage new companies on topics such as classified boards and supermajority vote provisions to amend bylaws, as we think that such arrangements may not be in the best interests of shareholders over the long-term.

We may apply a one-year grace period for the application of certain director-related guidelines (including, but not limited to, responsibilities on other public company boards and board composition concerns), during which we ask boards to take steps to bring corporate governance standards in line with our policies.

Further, if a company qualifies as an emerging growth company (an “EGC”) under the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”), we will give consideration to the NYSE and NASDAQ governance exemptions granted under the JOBS Act for the duration such a company is categorized as an EGC. An EGC should have an independent audit committee by the first anniversary of its IPO, with our standard approach to voting on auditors and audit-related issues applicable in full for an EGC on the first anniversary of its IPO.

Corporate form

Proposals to change a corporation’s form, including those to convert to a public benefit corporation (“PBC”) structure, should clearly articulate the stakeholder groups the company seeks to benefit and provide detail on how the interests of shareholders would be augmented or adversely affected with the change to a PBC. These disclosures should also include the accountability and voting mechanisms that would be available to shareholders. We generally support management proposals to convert to a PBC if our analysis indicates that shareholders’ interests are adequately protected. Corporate form shareholder proposals are evaluated on a case-by-case basis.

Exclusive forum provisions

BIS generally supports proposals to seek exclusive forum for certain shareholder litigation. In cases where a board unilaterally adopts exclusive forum provisions that we consider unfavorable to the interests of shareholders, we will vote against the Independent Chair or Lead Independent director and members of the nominating/governance committee.

Reincorporation

We will evaluate the economic and strategic rationale behind the company’s proposal to reincorporate on a case-by-case basis. In all instances, we will evaluate the changes to shareholder protections under the new charter/articles/bylaws to assess whether the move increases or decreases shareholder protections. Where we find that shareholder protections are diminished, we may support reincorporation if we determine that the overall benefits outweigh the diminished rights.

Multi-jurisdictional companies

Where a company is listed on multiple exchanges or incorporated in a country different from their primary listing, we will seek to apply the most relevant market guideline(s) to our analysis of the company’s governance structure and specific proposals on the shareholder meeting agenda. In doing so, we typically consider the governance standards of the company’s primary listing, the market standards by which the company governs themselves, and the market context of each specific proposal on the agenda. If the relevant standards are silent on the issue under consideration, we will use our professional judgment as to what voting outcome would best protect the long-term economic interests of investors. Companies should disclose the rationale for their selection of primary listing, country of incorporation, and choice of governance structures, particularly where there is conflict between relevant market governance practices.

Adjourn meeting to solicit additional votes

We generally support such proposals unless the agenda contains items that we judge to be detrimental to shareholders’ best long-term economic interests.

Bundled proposals

Shareholders should have the opportunity to review substantial governance changes individually without having to accept bundled proposals. Where several measures are grouped into one proposal, BIS may reject certain positive changes when linked with proposals that generally contradict or impede the rights and economic interests of shareholders.

Other business

We oppose voting on matters where we are not given the opportunity to review and understand those measures and carry out an appropriate level of shareholder oversight.

Shareholder protections

Amendment to charter/articles/bylaws

Shareholders should have the right to vote on key corporate governance matters, including changes to governance mechanisms and amendments to the charter/articles/bylaws. We may vote against certain directors where changes to governing documents are not put to a shareholder vote within a reasonable period of time, particularly if those changes have the potential to impact shareholder rights (see “Director elections”). In cases where a board’s unilateral adoption of changes to the charter/articles/bylaws promotes cost and operational efficiency benefits for the company and its shareholders, we may support such action if it does not have a negative effect on shareholder rights or the company’s corporate governance structure.

When voting on a management or shareholder proposal to make changes to the charter/articles/bylaws, we will consider in part the company’s and/or proponent’s publicly stated rationale for the changes; the company’s governance profile and history; relevant jurisdictional laws; and situational or contextual circumstances which may have motivated the proposed changes, among other factors. We will typically support amendments to the charter/articles/bylaws where the benefits to shareholders outweigh the costs of failing to make such changes.

Proxy access

It is our view that long-term shareholders should have the opportunity, when necessary and under reasonable conditions, to nominate directors on the company’s proxy card.[19]

Securing the right of shareholders to nominate directors without engaging in a control contest can enhance shareholders’ ability to meaningfully participate in the director election process, encourage board attention to shareholder interests, and provide shareholders an effective means of directing that attention where it is lacking. Proxy access mechanisms should provide shareholders with a reasonable opportunity to use this right without stipulating overly restrictive or onerous parameters for use, and also provide assurances that the mechanism will not be subject to abuse by short-term investors, investors without a substantial investment in the company, or investors seeking to take control of the board.

In general, we support market-standardized proxy access proposals, which allow a shareholder (or group of up to 20 shareholders) holding three percent of a company’s outstanding shares for at least three years the right to nominate the greater of up to two directors or 20% of the board. Where a standardized proxy access provision exists, we will generally oppose shareholder proposals requesting outlier thresholds.

Right to act by written consent

In exceptional circumstances and with sufficiently broad support, shareholders should have the opportunity to raise issues of substantial importance without having to wait for management to schedule a meeting. Accordingly, shareholders should have the right to solicit votes by written consent provided that: 1) there are reasonable requirements to initiate the consent solicitation process (in order to avoid the waste of corporate resources in addressing narrowly supported interests); and 2) shareholders receive a minimum of 50% of outstanding shares to effectuate the action by written consent.

We may oppose shareholder proposals requesting the right to act by written consent in cases where the proposal is structured for the benefit of a dominant shareholder to the exclusion of others, or if the proposal is written to discourage the board from incorporating appropriate mechanisms to avoid the waste of corporate resources when establishing a right to act by written consent. Additionally, we may oppose shareholder proposals requesting the right to act by written consent if the company already provides a shareholder right to call a special meeting that offers shareholders a reasonable opportunity to raise issues of substantial importance without having to wait for management to schedule a meeting.

Right to call a special meeting

In exceptional circumstances and with sufficiently broad support, shareholders should have the opportunity to raise issues of substantial importance without having to wait for management to schedule a meeting. Accordingly, shareholders should have the right to call a special meeting in cases where a reasonably high proportion of shareholders (typically a minimum of 15% but no higher than 25%) are required to agree to such a meeting before it is called. However, we may oppose this right in cases where the proposal is structured for the benefit of a dominant shareholder, or where a lower threshold may lead to an ineffective use of corporate resources. We generally think that a right to act via written consent is not a sufficient alternative to the right to call a special meeting.

Consent solicitation

While BlackRock is supportive of the shareholder rights to act by written consent and call a special meeting, BlackRock is subject to certain regulations and laws that place restrictions and limitations on how BlackRock can interact with the companies in which we invest on behalf of our clients, including our ability to participate in consent solicitations. As a result, BlackRock will generally not participate in consent solicitations or related processes. However, once an item comes to a shareholder vote, we uphold our fiduciary duty to vote in the best long-term interests of our clients, where we are authorized to do so.

Simple majority voting

We generally favor a simple majority voting requirement to pass proposals. Therefore, we will generally support the reduction or the elimination of supermajority voting requirements to the extent that we determine shareholders’ ability to protect their economic interests is improved. Nonetheless, in situations where there is a substantial or dominant shareholder, supermajority voting may be protective of minority shareholder interests, and we may support supermajority voting requirements in those situations.

Virtual meetings

Shareholders should have the opportunity to participate in the annual and special meetings for the companies in which they are invested, as these meetings facilitate an opportunity for shareholders to provide feedback and hear from the board and management. While these meetings have traditionally been conducted in-person, virtual meetings are an increasingly viable way for companies to utilize technology to facilitate shareholder accessibility, inclusiveness, and cost efficiencies. Shareholders should have a meaningful opportunity to participate in the meeting and interact with the board and management in these virtual settings; companies should facilitate open dialogue and allow shareholders to voice concerns and provide feedback without undue censorship. Relevant shareholder proposals are assessed on a case-by-case basis.

Endnotes

1A public company executive is defined as a Named Executive Officer (NEO) or Executive Chair(go back)

2In addition to the company under review.(go back)

3A BDC is a special investment vehicle under the Investment Company Act of 1940 that is designed to facilitate capital formation for small and middle-market companies(go back)

4CTo this end, we do not view shareholder proposals asking for the separation of Chair and CEO to be a proxy for other concerns we may have at the company for which a vote against directors would be more appropriate. Rather, support for such a proposal might arise in the case of overarching and sustained governance concerns such as lack of independence or failure to oversee a material risk over consecutive years(go back)

5This table is for illustrative purposes only. The roles and responsibilities cited here are not all-encompassing and are noted for reference as to how these leadership positions may be defined.(go back)

6For a discussion on the different impacts of diversity see: McKinsey, “Diversity Wins: How Inclusion Matters”, May 2022; Harvard Business Review, Diverse Teams Feel Less Comfortable – and That’s Why They Perform Better, September 2016; “Do Diverse Directors Influence DEI Outcomes”, September 2022(go back)

7We take a case-by-case approach and consider the size of the board in our evaluation of overall composition and diversity. Business model, strategy, location, and company size may also impact our analysis of board diversity. We acknowledge that these factors may also play into the various elements of diversity that a board may attract. We look for disclosures from companies to help us understand their approach and do not prescribe any particular board composition.(go back)

8Including, but not limited to, individuals who identify as Black or African American, Hispanic or Latinx, Asian, Native American or Alaska Native, or Native Hawaiian or Pacific Islander; individuals who identify as LGBTQ+; individuals who identify as underrepresented based on national, Indigenous, religious, or cultural identity; individuals with disabilities; and veterans.(go back)

9Special situations are broadly defined as events that are non-routine and differ from the normal course of business for a company’s shareholder meeting, involving a solicitation other than by management with respect to the exercise of voting rights in a manner inconsistent with management’s recommendation. These may include instances where shareholders nominate director candidates, oppose the view of management and/or the board on mergers, acquisitions, or other transactions, etc.(go back)

10Front-loaded awards are generally those that accelerate the grant of multiple years’ worth of compensation in a single year(go back)

11“Special awards” refers to awards granted outside the company’s typical compensation program.(go back)

12By material sustainability-related risks and opportunities, we mean the drivers of risk and value creation in a company’s business model that have an environmental or social dependency or impact. Examples of environmental issues include, but are not limited to, water use, land use, waste management, and climate risk. Examples of social issues include, but are not limited to, human capital management, impacts on the communities in which a company operates, customer loyalty, and relationships with regulators. It is our view that well-run companies will effectively evaluate and manage material sustainability-related risks and opportunities relevant to their businesses. Governance is the core means by which boards can oversee the creation of durable, long-term value. Appropriate risk oversight of business-relevant and material sustainability-related considerations is a component of a sound governance framework.(go back)

13The International Financial Reporting Standards (IFRS) Foundation announced in November 2021 the formation of an International Sustainability Standards Board (ISSB) to develop a comprehensive global baseline of high-quality sustainability disclosure standards to meet investors’ information needs. SASB standards will over time be adapted to ISSB standards but are the reference reporting tool in the meantime.(go back)

14The ISSB has committed to build upon the SASB standards, which identify material, sustainability-related disclosures across sectors. SASB Standards can be used to provide a baseline of investor-focused sustainability disclosure and to implement the principles-based framework recommended by the TCFD, which is also incorporated into the ISSB’s Climate Exposure Draft. Similarly, SASB Standards enable robust implementation of the Integrated Reporting Framework, providing the comparability sought by investors.(go back)

15The global aspiration to achieve a net-zero global economy by 2050 is reflective of aggregated efforts; governments representing over 90% of GDP have committed to move to net-zero over the coming decades. In determining how to vote on behalf of clients who have authorized us to do so, we look to companies only to address issues within their control and do not anticipate that they will address matters that are the domain of public policy.(go back)

16For example, BlackRock’s Capital Markets Assumptions anticipate 25 points of cumulative economic gains over a 20-year period in an orderly transition as compared to the alternative. This better macro environment will support better economic growth, financial stability, job growth, productivity, as well as ecosystem stability and health outcomes.(go back)

17https://www.blackrock.com/corporate/literature/whitepaper/bii-managing-the-net-zero-transition-february-2022.pdf(go back)

18While guidance is still under development for a unified disclosure framework related to natural capital, the emerging recommendations of the Taskforce on Nature-related Financial Disclosures (TNFD), may prove useful to some companies.(go back)

19BlackRock is subject to certain regulations and laws in the United States that place restrictions and limitations on how BlackRock can interact with the companies in which we invest on behalf of our clients, including our ability to submit shareholder proposals or elect directors to the board.(go back)