Print

PrintLarry Fink is Founder, Chairman and CEO of BlackRock, Inc. This post is based on Mr. Fink’s annual letter to investors.

Music plays a big role in my life. As a kid growing up in California, I used to go to the local record shop, buy a piece of vinyl and listen to the album on my record player. I still listen to records, though less often than when I was young. Today, streaming allows me to listen with ease to the whole album of an artist, or just that artist’s greatest hits, or a playlist of my own compilations, or those of other listeners. We have so much choice at our fingertips.

Technology has also made financial markets much more affordable and accessible. Forty years ago, buying a stock or bond was a laborious process that required calling a stockbroker. The fees investors paid weren’t always clear. Now anyone with a smartphone and a brokerage account has tens of thousands of ETFs, mutual funds, and single stocks at their fingertips, and can make a purchase with a few clicks. Technology has greatly expanded the amount of choice for savers and investors. It can’t eliminate risks from investing (as we’ve seen all too vividly this past week), but technology has made financial markets more transparent, as well as easier and cheaper to access.

Making investing more accessible, affordable, and transparent to more people is core to our mission at BlackRock.

We are a fiduciary to our clients. The money we manage belongs to our clients who trust us to manage their investments to help them prepare for the future. Our fiduciary duty is to serve each and every client by seeking the best risk-adjusted returns within the investment guidelines they set for us. The powerful simplicity of our business model is that when we deliver value for our clients, we also create more value for our shareholders.

Part of supporting our clients includes speaking out on issues important to their investments. I’ve long believed that it’s critical for CEOs to use their voice in the world – and there’s never been a more crucial moment for me to use mine. I will do so whenever and wherever I believe it can serve the interests of our clients and the firm.

In recent years, I have written two letters each year – one on behalf of our clients to CEOs and the other to BlackRock shareholders. In November, on the anniversary of BlackRock introducing Voting Choice, I wrote to both CEOs and our clients to share my views on the transformative power of choice in proxy voting.

As we start 2023, it is clear to me that all of our stakeholders – BlackRock shareholders, clients, employees, partners, the communities where we operate, and the companies in which our clients are invested – are facing so many of the same issues. For that reason, this year, I am writing a single letter to investors, and we are sharing it with all of our stakeholders.

Clients have always been central to all we do. Today we serve clients who have a wide range of investment objectives, preferences, time horizons, and risk tolerances. We offer them choices to help them reach their investment goals. And we manage their assets consistent with their objectives and guidelines.

The new dollars – or euros, pounds or yen – that our clients award us are what our CFO, Martin Small, refers to as “units of trust.” This trust our clients place with us to help them achieve their financial goals is something we take extremely seriously. We are humbled that across the globe, because of that trust, clients turn to us more than any other firm in our industry. While most of our peers [1] saw net outflows in 2022, clients entrusted BlackRock to manage nearly $400 billion in long-term net new assets – including $230 billion in the U.S. alone. These industry-leading results reflect a strong endorsement by our clients of the choices we offer, the advice we provide, the long-term investment performance we have delivered, and the fiduciary standard we uphold.

These industry-leading results reflect a strong endorsement by our clients of the choices we offer, the advice we provide, the long-term investment performance we have delivered, and the fiduciary standard we uphold.

2022 was one of the most challenging market environments in history – a year in which both equity and bond markets declined for the first time in decades – and the challenges have continued into 2023. Through this, our people have stayed focused on delivering for our clients and providing them with outcomes suited to each of their unique goals and needs.

There are many people with opinions about how we should manage our clients’ money. But the money doesn’t belong to these people. It’s not ours either. It belongs to our clients, and our responsibility and our duty is to them.

Choice has never been more important to BlackRock than it is today because we have never served a broader and more diverse set of clients. We see opinions diverging across regions – including the U.S. and Europe – and even within regions – especially in the U.S. That divergence creates challenges for a truly global asset manager like BlackRock. But I believe that in this environment the diversity of our offerings, our global perspective and insights, and our approach of always putting our clients’ preferences at the center of our work remain powerful competitive advantages.

BlackRock has grown as more and more clients have placed their trust in us, and that growth in turn has allowed us to deliver better outcomes for both our clients and our shareholders. Our scale means we can deliver not only greater choice, but also financial benefits to clients through lower fees, tighter bid-ask spreads when trading securities, and more diversified service-provider relationships. In our iShares business, for example, we offer over 1,300 ETFs – more than any other firm. And since 2015, iShares fee reductions have helped investors save nearly $600 million.[2]

It is not only in ETFs where clients have benefitted from cost savings. Over five years, the asset-weighted average fees paid by our U.S. mutual fund and ETF investors, for example, have come down by approximately 35% [3] as clients benefit from our scale and product choice. This means our clients can keep more of what they earn and have a better opportunity to reach their financial goals.

At the same time, we are focused on delivering for our shareholders by maintaining strong margins. Our scale, technology and innovation help us continuously improve our operational excellence and drive cost savings that can then be used to fund investments back into the business to support future growth.

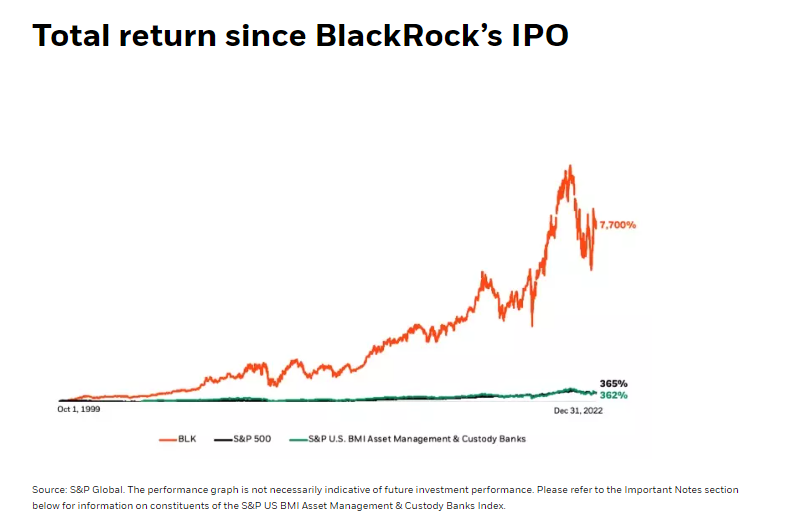

It’s through our scaled, fiduciary model – which is centered on empowering our clients with comprehensive choices across the whole portfolio – that we have been able to deliver performance for our shareholders. We are proud to be the highest-performing financial services stock in the S&P 500 since our IPO in 1999, delivering a total return of 7,700%. [4]

The BlackRock story

2023 marks the 35th anniversary of the founding of the firm and 24 years since our initial public offering, milestones I couldn’t have imagined back in the late eighties. A lot has changed since then (although I’m still a big fan of my favorite 80s band Talk Talk and think they only got better with their later albums). Yet, when I reflect on our journey, certain things have remained consistent over the decades.

BlackRock as an asset manager is a fiduciary. We manage money on behalf of our clients to help them or the people they serve achieve their financial goals, including saving for retirement, a home, or a child’s education. It’s a huge source of pride for everyone at BlackRock that we play a role in helping millions of people around the world experience financial well-being. Knowing that we’ve helped firefighters and teachers retire with dignity after a lifetime of service, or that we’ve helped a family take some of the stress out of paying for college, is what gives me such pride in what we do.

One of BlackRock’s most critical tasks as a fiduciary investor for our clients is to identify short- and long-term trends in the global economy that might affect our clients’ investments. We do this across all sectors, including those that are essential to the future of the economy such as healthcare, technology and energy.

Our clients are often investing for the long term, and we evaluate all kinds of long-term investment risks that could impact their portfolios – such as inflation, geopolitics, or the energy transition.

People around the world turn to BlackRock for our unique investment insights and guidance, comprehensive investment solutions, investment performance track record, and world-class investment and technology capabilities. It is our duty to provide clients with our perspective on matters that can affect asset prices and to help them navigate constantly evolving markets and industries. Our commitment to our clients’ financial interests is unwavering, undivided, and always designed for their specific needs.

Our commitment to our clients’ financial interests is unwavering, undivided, and always designed for their specific needs.

The price of easy money – are the dominoes starting to fall?

Since the financial crisis of 2008, markets were defined by extraordinarily aggressive fiscal and monetary policy. As a result of these policies, we’ve seen inflation move sharply higher to levels not seen since the 1980s. To fight this inflation, the Federal Reserve in the past year has raised rates nearly 500 basis points. This is one price we’re already paying for years of easy money – and was the first domino to drop.

Bond markets were down 15% last year, but it still seemed, as they say in those old Western movies, “quiet, too quiet.” Something else had to give as the fastest pace of rate hikes since the 1980s exposed cracks in the financial system.

This past week we saw the biggest bank failure in more than 15 years as federal regulators seized Silicon Valley Bank. This is a classic asset-liability mismatch. Two smaller banks failed in the past week as well. It’s too early to know how widespread the damage is. The regulatory response has so far been swift, and decisive actions have helped stave off contagion risks. But markets remain on edge. Will asset-liability mismatches be the second domino to fall?

Prior tightening cycles have often led to spectacular financial flameouts – whether it was the Savings and Loan Crisis that unfolded throughout the eighties and early nineties or the bankruptcy of Orange County, California, in 1994. In the case of the S&L Crisis, it was a “slow rolling crisis” – one that just kept going. It ultimately lasted about a decade and more than a thousand thrifts went under.

We don’t know yet whether the consequences of easy money and regulatory changes will cascade throughout the U.S. regional banking sector (akin to the S&L Crisis) with more seizures and shutdowns coming.

We don’t know yet whether the consequences of easy money and regulatory changes will cascade throughout the U.S. regional banking sector with more seizures and shutdowns coming.

It does seem inevitable that some banks will now need to pull back on lending to shore up their balance sheets, and we’re likely to see stricter capital standards for banks.

Over the longer term, today’s banking crisis will place greater importance on the role of capital markets. As banks potentially become more constrained in their lending, or as their clients awaken to these asset-liability mismatches, I anticipate they will likely turn in greater numbers to the capital markets for financing. And I imagine many corporate treasurers are thinking today about having their bank deposits swept nightly to reduce even overnight counterparty risk.

And, there could yet be a third domino to fall. In addition to duration mismatches, we may now also see liquidity mismatches. Years of lower rates had the effect of driving some asset owners to increase their commitments to illiquid investments – trading lower liquidity for higher returns. There’s a risk now of a liquidity mismatch for these asset owners, especially those with leveraged portfolios.

As inflation remains elevated, the Federal Reserve will stay focused on fighting inflation and continue to raise rates. While the financial system is clearly stronger than it was in 2008, the monetary and fiscal tools available to policymakers and regulators to address the current crisis are limited, especially with a divided government in the United States.

With higher interest rates, governments can’t sustain recent levels of fiscal spending and the deficits of previous decades, the U.S. government spent a record $213 billion on interest payments on its debt in the fourth quarter of 2022, up $63 billion from a year earlier. In the U.K., as gilts plunged last fall following the announcement of significant unfunded tax cuts, we saw how swiftly markets react when investors lose faith in their government’s fiscal discipline.

After years of global growth being driven by record high government spending and record low rates, the world now needs the private sector to grow economies and elevate the living standards of people around the globe. We need leaders in both government and corporations to recognize this imperative and work together to unleash the potential of the private sector.

An economy of fragmentation

These dramatic changes in financial markets are happening at the same time as equally dramatic changes in the landscape of the global economy – all of which will keep inflation elevated for longer.

I wrote in last year’s letter to shareholders about the profound shifts in globalization that we would see in 2022 as a result of Russia’s invasion of Ukraine. The seeds of a backlash against globalization were planted long before this war in Europe. In 2017, I highlighted how globalization and technological change were dividing communities and impacting workers. The societal implications included Brexit, upheaval in the Middle East, and political polarization in the U.S.

Covid isolation has heightened this charged environment and led to greater protectionism and polarization. The lack of face-to-face interaction has had a profound effect on humanity. Video calls are no substitute for meeting in person or sharing a meal. The ability to connect has never been more important, whether you are the manager of a dozen people, the CEO of a multinational corporation or the leader of a global superpower wrestling with the new geopolitical landscape.

Employees want to connect with their companies and citizens want to believe in their governments, but polarization and fragmentation have eroded trust and diminished hope.

The repeated shocks of the past few years have also dramatically reshaped supply chains. The pandemic highlighted the need for supply chains to be resilient. Russia’s invasion of Ukraine and growing geopolitical tensions have brought national and economic security front and center.

Whether it is for food and energy or computer chips and AI, companies and countries are all looking to ensure they are not dependent on supply chains exposed to geopolitical tensions. Increasingly, they want to source essential goods close to home even if it means higher prices. These shifts are producing a less integrated, more fragmented global economy. Leaders in public and private sectors are essentially trading off efficiency and lower costs for resilience and national security. It is understandable public policy. But for investors it is important to recognize the risks and opportunities it creates.

Governments are playing a bigger role in where products can be sourced and where capital should be allocated as they look to keep the production of critical components inside their borders. This means capital won’t necessarily be allocated to the businesses that deliver the maximum market return regardless of where they are located.

This may produce better national security outcomes with more resilient and secure supply chains. But in the near term, the effects are highly inflationary. This tradeoff between price and security is one of the reasons I believe inflation will persist and be more difficult for central bankers to tame over the long term. As a result, I believe inflation is more likely to stay closer to 3.5% or 4% in the next few years.

This new economy of fragmentation brings risks – like elevated inflation – but also opportunities.

I believe that North America could be one of the biggest global beneficiaries. We have a large and diverse labor force. We have abundant natural resources, with the potential for both energy and food security. Public policy is helping to keep chip manufacturing in the U.S., and the latest innovations in AI have become a new preoccupation. Other national winners will emerge as well.

Leaders in public and private sectors are essentially trading off efficiency and lower costs for resilience and national security… This trade-off between price and security is one of the reasons I believe inflation will persist and be more difficult for central bankers to tame over the long term.

Building a hopeful future for retirees

The world faces a “silent crisis” when it comes to retirement. You rarely hear about it in the news media. It’s not part of the political dialogue in most countries. And corporate leaders rarely discuss it – not in public anyway. It doesn’t make headlines or attract attention because it’s not immediate. It’s not this year’s – or even next year’s – problem. But it is a crisis. And the longer we delay the conversation about it, the larger the crisis grows.

Lower market-return expectations, higher housing and healthcare costs for retirees, and the shifting of retirement risks to individuals have all made it more challenging than ever to support increased longevity.

To help address this crisis, we must understand some of the issues driving the retirement crisis at both the global and local levels. Populations in Europe, North America, China, and Japan are aging due to increased lifespans and falling birth rates. Fertility rates have fallen to an all time low of 1.7 births per woman in the U.S., 1.5 births in Europe, and 1.2 births in China. This has profound implications for each of these markets over time. It will result in a smaller working population and cause income to grow more slowly or even decline.

Countries and companies need to pursue a “productivity imperative.” Successful countries will be those with higher healthy life expectancies, greater labor force participation rates, and higher rates of productivity. Successful companies that generate durable returns for shareholders will be those able to find enough workers, engage them at high rates of productivity, and find enough customers.

Another challenge is understanding why some people can save effectively for retirement and others cannot. Even in wealthier countries, many people lack the ability to save; and if they do save, they often use those savings for an emergency, rather than investing for retirement. In some countries people are actually over saving but under-investing. If they are keeping their money in the bank rather than investing in the market, they won’t generate the returns necessary to retire with dignity. In order to retire comfortably, people need to invest their savings over decades and take advantage of the long term returns delivered by the growth of the capital markets.

Long-term investing requires trust in the financial system and a fundamental belief that tomorrow will be better than today. We need leaders today who will give people reasons to be hopeful, who can articulate a vision for a brighter future. And, we need institutions that inspire trust. So much of what we have lost over the past few years – through Covid, war in Europe, political polarization, geopolitical fragmentation, and macro-economic shifts – has eroded optimism, trust, and a belief in a better future.

There’s so much fear today: fear of economic insecurity, fear about what world the next generation will inherit, fear of how the “polycrisis” that characterizes the economic and political landscape will shape the future. But I remain an optimist. The world has faced major crises before. We got through them by confronting problems, imagining a better future, creating connections, and driving innovation forward. We need to do the same today. Our job as leaders is to show people how to see in challenges opportunities that can be captured.

Investing for the future is an act of hope and optimism

More than half of the money BlackRock manages is related to retirement. So helping people finance retirement is a major focus of ours. To help future retirees, we need to understand what’s driving financial decision-making in different markets and how to become a trusted partner to those who are trying to plan for their long-term needs.

People only invest if they believe in the future and believe in the integrity of financial and regulatory institutions; otherwise they keep their money under the mattress or make risky financial moves in the hope of overnight riches. When people are afraid, they may save, but they won’t invest. Investing for a financial goal like retirement is an act of hope and optimism, demonstrating a long-term perspective, trust in financial institutions, and belief in the integrity of the market.

A lack of hope, particularly as we head into a period of uncertainty and economic malaise – if not a full-blown recession – might be one of the biggest barriers to turning savers into long-term investors. In a global survey last year asking if people thought their families would be better off in five years, the results were at an all-time low in 24 of 28 countries.[6]

Investing for a financial goal like retirement is an act of hope and optimism, demonstrating a long-term perspective, trust in financial institutions, and belief in the integrity of the market.

Levels of trust in financial institutions and hope for the future vary greatly country by country. Even in the U.S., where capital markets have been a huge success story over the years, just 58% of Americans are invested in the stock market. [7] Americans and others around the world who invested $1,000 in an S&P 500 index tracker 10 years ago and left it alone would have over $3,000 (that same $1,000 in BlackRock stock would have done quite a bit better and be over $4,000).[8] For those who put it under the mattress or in an empty coffee can, that $1,000 would be worth even less after inflation. That is the power of investing. Our job at BlackRock includes helping more people benefit from the power of the capital markets by making investing more accessible, affordable, and transparent.

In the same way that the internet enabled streaming to transform the music industry, society needs to transform how people plan for retirement. We need to do that in a way that’s tailored to the unique needs of each local market, culture, and regulatory system. There is no global solution to this crisis. BlackRock is working in many markets around the world to lower barriers to investing by creating choices that make market access frictionless and affordable wherever our clients are.

2023 marks the 30th anniversary of BlackRock pioneering the first target-date fund in the U.S., called LifePath. BlackRock manages $350 billion in LifePath target-date fund assets today, and our retirement business serves approximately 40 million Americans. LifePath Paycheck, a solution we announced in 2020 for the U.S. market, is designed to give access to a lifetime income stream in retirement. Eleven large plan sponsors, representing over $20 billion in target-date assets and over 500,000 participants, have elected to work with BlackRock to implement LifePath Paycheck as the default investment option in their employees’ retirement plans. And this year, BlackRock made a minority investment in Human Interest, which aims to expand access to retirement plans to small- and medium-sized businesses, an under-served segment of the market.

In Germany, we’re offering ETF savings plans through digital distributors like Scalable Capital and Trade Republic, giving investors easier access to the capital markets. In France, we’re partnering with Boursorama to make it easier for banking customers to turn savings into long-term investments. We’re also exploring opportunities in many other markets to provide local investment solutions to help address retirement challenges.

Helping clients navigate and invest in the global energy transition

Investing for the long term requires taking a long-term view of what will impact returns, including demographics, government policy, technological advancements, and the transition to a low carbon economy. In the near term, monetary and fiscal policy will be the major driver of returns. Over the long run, investors also need to consider how the energy transition, among other factors, will impact the economy, asset prices, and investment performance.

For years now, we have viewed climate risk as an investment risk. That’s still the case. Anyone can see the impact of climate change in the natural disasters in California or Florida, in Pakistan, across Europe and Australia, and in many other places around the world. There’s more flooding, more wildfires, and more intense storms. In fact, it’s hard to find a part of our ecology – or our economy – that’s not affected. Finance is not immune to these changes. We’re already seeing rising insurance costs in response to shifting weather patterns.

According to Munich Re, insurers had to cover $120 billion for natural catastrophes in 2022, [9] – a once unthinkable figure. This drives up insurance prices and will have a huge impact on homeowners, some of whose homes may simply become unaffordable to insure.

The U.S. housing market could see significant changes if people relocate to areas less affected by changing weather patterns. To prevent an exodus from coastal zones and areas affected by drought and wildfires, some governments have been subsidizing or replacing private insurance. Most flood insurance policies currently providing coverage in Florida are underwritten by the federal government’s National Flood Insurance Program (NFIP). The NFIP has had to borrow funds from the U.S. Treasury and is currently $20.5 billion in debt. [10]

The transition to a low-carbon economy is top of mind for many of our clients. Our clients have a range of investment objectives and perspectives. We have clients who want to invest in ways that seek to align with a particular transition path or to accelerate that transition. We have clients who choose not to. We offer choice to help clients reach their investment goals, and we manage their assets consistent with their objectives and guidelines.

Changes to government policy, technology, and consumer preferences will create significant investment opportunities. Some of our clients want to take advantage of opportunities created in areas like infrastructure investments that will benefit both households and economies.

Many of our clients also want access to data to ensure that material sustainability risk factors that could impact long-term asset returns are incorporated into their investment decisions. This is why we partner with other companies and provide insights into how a changing climate and the transition may affect portfolios over the long term. These clients track the transition to lower carbon emissions just as they track any other driver of investment risk. They want our help to understand the likely future paths of carbon emissions, how government policy will impact these paths, and what that means in terms of investment risks and opportunities. It is not the role of an asset manager like BlackRock to engineer a particular outcome in the economy, and we don’t know the ultimate path and timing of the transition. Government policy, technological innovation, and consumer preferences will ultimately determine the pace and scale of decarbonization. Our job is to think through and model different scenarios to understand implications for our clients’ portfolios.

That’s why BlackRock has been so vocal in recent years in advocating for disclosures and asking questions about how companies plan to navigate the energy transition. As minority shareholders, it’s not our place to be telling companies what to do. My letters to CEOs are written with a single goal: to ensure companies are going to generate durable, long-term investment returns for our clients.

At BlackRock we use data and analytics to help our clients understand how the energy transition is evolving and give them choices about how they would like to invest in emerging opportunities. Better data is essential. More than half of the companies in the S&P 500 now voluntarily report Scope 1 and Scope 2 emissions. I expect that number will continue to rise.[11] But as I have said consistently over many years now, it is for governments to make policy and enact legislation, and not for companies, including asset managers, to be the environmental police.

Transition toward lower carbon emissions will reflect the regulatory and legislative choices governments make to balance the need for secure, reliable and affordable energy with orderly decarbonization.

We know that the transition will not be a straight line. Different countries and industries will move at different speeds, and oil and gas will play a vital role in meeting global energy demands through that journey. Many of our clients see the investment opportunities that will come as established energy companies adapt their businesses. They recognize the vital role energy companies will play in ensuring energy security and a successful energy transition.

We are working with energy companies globally that are essential in meeting societies’ energy needs. To ensure the continuity of affordable energy prices during the transition, fossil fuels like natural gas, with steps taken to mitigate methane emissions, will remain important sources of energy for many years ahead. BlackRock is also investing, on behalf of our clients, in responsibly-managed natural gas pipelines. For example, in the Middle East, we invested in one of the largest pipelines for natural gas, which will help the region utilize less oil for power production.

Governments are taking bigger steps to drive a transition toward lower carbon emissions. For example, we see the Inflation Reduction Act in the U.S. creating significant opportunities for investors to allocate capital to the energy transition. This legislation commits an estimated $369 billion for investment in energy security and climate change mitigation. This is attracting investment into existing and emerging technologies like carbon capture and green hydrogen. We are creating opportunities for clients to participate in infrastructure and technology projects, including the building of carbon capture storage pipelines and technology that turns waste into clean burning natural gas.[12] European governments are also developing incentives to support the transition to a net zero economy and drive growth.

Some of the most attractive investment opportunities in the years ahead will be in the transition finance space. Given its importance to our clients, BlackRock’s ambition is to be the leading investor in these opportunities on their behalf.

I wrote last year that the next 1,000 unicorns won’t be search engines or social media companies. Many of them will be sustainable, scalable innovators – startups that help the world decarbonize and make the energy transition affordable for all consumers. I still believe that. For clients who choose, we’re connecting them with these investment opportunities.

Our approach to investing in the transition is the same as our approach across our platform: we provide choice to our clients; we seek the best risk-adjusted returns within the mandate they give us; and we underpin our work with research, data, and analytics.

Transforming proxy voting with greater client choice

We continue to innovate in a variety of areas to expand the choices we offer clients. Some of our clients have expressed interest in a more direct role in the stewardship of their capital, and we have sought to deliver solutions that enable them to vote their shares. As I wrote last year to clients and corporate CEOs, I believe that, if widely adopted, voting choice can enhance corporate governance by bringing new voices into shareholder democracy.

BlackRock has been at the forefront of this innovation for years, and we have seen other asset managers follow our lead and adopt similar efforts. Nearly half of our index equity assets under management are now eligible for Voting Choice. This includes all the public and private pension plan assets we manage in the U.S., as well as retirement plans serving more than 60 million people around the world. Clients representing over $500 billion in AUM have chosen to participate in Voting Choice to express their preferences.

When I first started writing letters to the CEOs of the companies in which our clients are invested, my entire focus was on stewardship and ensuring engagement that centers on creating long-term value for our clients. We set out to build the best global stewardship team in the industry – to engage with companies on corporate governance not just during proxy season, but year-round because we didn’t think that the industry’s reliance on just a few proxy advisors was appropriate. We believed that our clients expected us to make independent and well-informed decisions about what was in their best financial interest. And we still do.

Making these decisions requires understanding how companies are responding to evolving risks and opportunities. Changes in globalization, supply chains, geopolitics, inflation, monetary and fiscal policy, and climate all can impact a company’s ability to deliver durable value. Our stewardship team works to promote better investment performance for our clients, the asset owners. The team does that by understanding how a company is responding to these factors where financially material to the company’s business, and by advocating for sound governance and business practices. For many of our clients who have entrusted us with this important responsibility, BlackRock’s stewardship efforts are core to what they are seeking from us.

At the same time, we believe that adding more voices to corporate governance can further strengthen shareholder democracy. But democracy only works when people are informed and engaged. As more asset owners choose to direct their own votes, they need to make sure they are investing the time and resources to make informed decisions on critical governance issues. Proxy advisors can play an important role. But if asset owners rely too much on a few proxy advisors, then their voice may fall short of its potential. I certainly believe that the industry would benefit from more proxy advisors who can add diversity of views on shareholder issues.

Amid these shifts, companies will also need to find new ways to reach their shareholders who choose to direct their own votes, and robust disclosures and advances in the proxy ecosystem will become even more important.

How the voting ecosystem changes over the next decade can be a transformative force that reshapes corporate governance.

Benefits of our client-centric approach resonating in our results

Today and throughout BlackRock’s history, we have focused on delivering the best risk-adjusted financial returns for clients – consistent with their individual guidelines and objectives. We are relentless about staying ahead of their needs, providing them with more choice, and innovating to help them achieve financial well-being. And clients are coming to BlackRock more than ever before.

BlackRock captured a leading share of long-term industry flows in 2022 and delivered positive organic base fee growth for the year. Over the past five years, BlackRock has delivered an aggregate $1.8 trillion in total net inflows, or 5% average organic asset growth, compared with flat or negative industry flows. Over this five-year period, markets have had rallies and contractions, but BlackRock has consistently delivered growth, demonstrating the power of our diversified platform.

BlackRock generated nearly $400 billion in long-term net new assets in 2022, reflecting the decisions by thousands of organizations and investors that continually place their trust in BlackRock.

Flows were positive across regions, including $230 billion of long-term net inflows in the U.S. We generated organic asset growth across index, active and all long-term asset classes – from fixed income to equity to multi-asset to alternatives – as clients turned to BlackRock for solutions for their whole portfolio.

Market declines and the strengthening U.S. dollar reduced BlackRock’s AUM by $1.7 trillion in 2022, impacting our financial results. Our clients have also been impacted by the complex market environment of 2022, and BlackRock is working with clients of all sizes around the world as they reshape their portfolios for the future. Against the current backdrop, BlackRock has an even greater obligation to help our clients wade through the uncertainty and give them confidence to invest for the long term.

We see many opportunities for our clients to capitalize on market disruption – to rethink portfolio construction, to benefit from the renewed income-generating potential of bonds, or to reallocate to sectors that may be more resilient in the face of elevated inflation and market

distress. BlackRock is uniquely positioned to help clients navigate opportunities in this environment across their entire portfolio because of our diversified platform and integrated investment management, technology, and advisory expertise.

Our whole portfolio approach is resonating more than ever and underpinned the record $192 billion of long-term net inflows from institutional clients in 2022, led by several significant outsourcing mandates. In an increasingly complex investing environment, we’re seeing very strong demand from clients looking to partner with BlackRock for outsourced solutions. In the past two years, we are honored to have been entrusted to lead a number of outsourced mandates totaling over $300 billion in AUM, spanning existing and new clients and capabilities. These clients are choosing BlackRock because of our scale, resources, and expertise to take on the challenges of the markets, and we expect this to continue into 2023.

In 2022, BlackRock helped millions of investors plan for their financial futures as they continued to turn to iShares ETFs. iShares ETFs led the industry with $220 billion of net inflows. We are proud that iShares offers the most choice in the industry – in 2022 alone, we launched over 85 new ETFs globally.

Bond ETFs led iShares growth, generating a record $123 billion of net inflows. We again led industry flows, and six of the top ten asset-gathering bond ETFs in 2022 were iShares. In 2022, we celebrated the 20th anniversary of bond ETFs, and today we provide over 450 bond ETF choices across our $760 billion iShares fixed income platform.

Over the past 20 years, bond ETFs have broken down many barriers to fixed income investing, simplifying how all types of investors access markets. Bond ETFs connected the fragmented fixed income market with transparent and liquid on-exchange trading and provided a simple way for investors to buy a portfolio of bonds for a known bid-ask spread and relatively low fees. We believe that bond ETFs will continue to catalyze advances in fixed income market structure and will become further integrated into an increasingly modern, electronic fixed income marketplace.

The need for income and uncorrelated returns against the backdrop of higher inflation, distress in the banking sector and a more challenged market for public equities will continue to drive demand for private markets. In 2022, we raised $35 billion in client capital across our alternatives platform, led by private credit and infrastructure. We’re successfully scaling successor funds, delivering larger funds through raises of subsequent fund vintages. For example, in 2020, our third Global Energy and Power Infrastructure Fund raised a total of $5 billion, surpassing the total assets of vintages I and II combined. In 2022, the most recent fund in the franchise raised $4.5 billion in initial investor commitments at first close, achieving over half its targeted size of $7.5 billion.

BlackRock’s diversified infrastructure funds are also providing benefits to communities in the U.S. and around the world. In 2022 we announced an agreement to form Gigapower, a joint venture with one of our diversified infrastructure funds and AT&T. Upon closing, Gigapower will provide a fiber network to customers and communities outside of AT&T’s traditional service areas. The network will advance efforts to bridge the digital divide and ultimately help spur local economies in the communities in which Gigapower operates.

Our multi-decade investment into Aladdin continues to differentiate BlackRock as an asset manager and as a leading fintech provider. Periods of market volatility have historically underscored the importance of Aladdin, and in 2022 we saw record client mandates. We see clients doubling down on technology and leveraging fewer providers to do more with less; this is evidenced by our mandates in 2022, with about half spanning multiple Aladdin products.

In addition to our investment and technology capabilities, our Financial Markets Advisory (FMA) group plays a critical role in advising financial and official institutions. In 2022, we successfully transitioned the last remaining assets that we were proud to manage for the New York Federal Reserve Bank in connection with programs designed to facilitate access to capital for businesses and to support the economy early in the pandemic.

We also are very proud that our FMA group is working pro bono with the government of Ukraine to provide advice on designing an investment framework. The goal is ultimately creating opportunity for both public and private investors to participate in the reconstruction and recovery of the Ukrainian economy.

My calls with President Zelenskyy over the past six months have been humbling. The courage and spirit of the Ukrainian people have inspired millions around the world, and even as they continue to fight on the battlefield they are planning for rebuilding their country after the war. They exemplify the hope that we all should have, and BlackRock is grateful to be able to help them lay a foundation to realize their hope for a free, peaceful, and prosperous Ukraine.

Digital assets

If there’s one part of financial services that’s caught the headlines over the past year, it’s digital assets, not least due to the collapse of FTX. But beyond the headlines – and the media’s obsession with Bitcoin – very interesting developments are happening in the digital asset space. In many emerging markets – like India, Brazil and parts of Africa – we are witnessing dramatic advances in digital payments, bringing down costs and advancing financial inclusion. By contrast, many developed markets, including the U.S., are lagging behind in innovation, leaving the cost of payments much higher.

For the asset management industry, we believe the operational potential of some of the underlying technologies in the digital assets space could have exciting applications. In particular, the tokenization of asset classes offers the prospect of driving efficiencies in capital markets, shortening value chains, and improving cost and access for investors. At BlackRock we continue to explore the digital assets ecosystem, especially areas most relevant to our clients such as permissioned blockchains and tokenization of stocks and bonds.

While the industry is maturing, there are clearly elevated risks and a need for regulation in this market. BlackRock is committed to operational excellence, and we plan to apply the same standards and controls to digital assets that we do across our business.

Strategy for long-term growth

For the past three decades, BlackRock has led by listening to our clients. Our growth reflects this deep commitment to understanding their needs, building our strategy to address them in the context of market opportunities, and then executing with discipline.

For the past three decades, BlackRock has led by listening to our clients. Our growth reflects this deep commitment to understanding their needs, building our strategy to address them in the context of market opportunities, and then executing with discipline.

In 2022, our management team and Board spent time assessing our strategy for growth over the next three to five years. We challenged ourselves to think about what actions we’d take if we knew that markets would be more range-bound and volatile for the next several years. We had this discussion recognizing that we can learn and build off crisis and change. How do we execute on opportunities that emerge amid market dislocation and industry disruption? How do we make sure we come through even stronger, as we’ve done throughout our history?

We emerged with strong conviction in our strategy and our ability to execute with scale and expense discipline. Our strategy remains centered on growing Aladdin, iShares, and private markets, keeping alpha at the heart of BlackRock, leading in sustainable investing, and advising clients on their whole portfolio.

And we see growing opportunities in areas like transition finance, institutional outsourcing, more customization of both institutional and wealth portfolios, and alternative investments for wealth clients globally.

Clients increasingly want to work with BlackRock as a global, multi-product, and solutions-oriented asset manager, with a strong investment culture and the ability to solve for technology needs. Even as the largest asset manager in the world, we still have only 3% share of a fragmented industry’s revenue. We continue to target 5% organic growth through a market cycle and expect to outperform the industry in both down and up markets.

We are honored that our clients entrusted us with nearly $400 billion of long-term net new assets in 2022. Looking ahead, we see similar client needs shaping the opportunity set.

The role of fixed income in a portfolio is increasingly relevant – for the first time in years, investors can earn very attractive yields without taking much duration or credit risk. Institutions and individuals targeting something around a 7% return have had to manage allocations across equities, bonds and alternatives to try to reach that yield. Today, they can meet that target by investing almost entirely in bonds.

Clients are coming to BlackRock to help them pursue generational opportunities in the bond market, and our $3.2 trillion fixed income and cash platform is well-positioned to capture accelerating demand. In addition to our industry-leading bond ETF flows, clients are turning to BlackRock’s diversified active platform. And we believe that recent concerns about the security of cash in bank deposits will further accelerate demand for cash management options we provide.

Our notable successes in onboarding and executing significant outsourcing mandates over the past several years have catalyzed dialogue with more clients. Early in 2023, two significant pension clients announced they had selected BlackRock for significant OCIO mandates, trusting BlackRock to look after the pensions of their members. These are yet more examples of how BlackRock’s range of resources, experience, and deep connectivity in local markets are resonating with clients.

As clients increasingly want to outsource or consolidate providers, the power of BlackRock’s diversified investment and technology platform becomes even more evident. We can offer solutions across clients’ whole portfolios – including market leadership across ETFs, active, and private markets. In ETFs, we expect the industry to reach $15 trillion in the next few years, with iShares leading that growth. In active, we are finding new ways to generate alpha and offer dynamic active allocation with model portfolios. And the investment we have made over the years in our private markets platform is positioning us to capture emerging opportunities in private credit, infrastructure and transition finance – particularly if we see less lending from banks.

Aladdin is foundational to how we serve clients across our platform. It is not only the operating system that unites all of BlackRock; it is a key component of many of our largest client relationships. Our momentum in Aladdin has never been stronger, evidenced by a record year of net sales in 2022, and our advisory capabilities continue to play a critical role in our dialogue with clients.

As BlackRock has demonstrated many times since our founding, challenging environments create unique opportunities for future growth, and we’ve always emerged stronger and more deeply connected with our clients. I believe the best of BlackRock is ahead of us, and we are committed to delivering the power of our unified platform to benefit our clients, employees, and shareholders.

Developing our leadership and our culture

Last year, I had a significant birthday, and that milestone has certainly been a moment for reflection on my own leadership and BlackRock’s role and responsibilities through the years.

When we founded BlackRock, I was 35: I couldn’t have imagined it would grow into the company it is today. I learned a great deal about leadership during that time, and my most important responsibility now is growing and mentoring leaders across the firm.

I have never been more excited about the talent, expertise, and leadership at the firm and their potential to keep innovating ahead of our client needs, delivering value for shareholders, and driving BlackRock into the future.

BlackRock – and many corporations across sectors – successfully pivoted to working remotely during the pandemic. Modern technology and remote work proved to be saviors of the economy. We learned that while working remotely our leaders could execute in their verticals very well. But clients do not come to BlackRock because we can deliver on one or two or three verticals – they come to us because we can deliver our full platform in a One BlackRock experience – what we call horizontal leadership.

BlackRock’s most successful leaders work horizontally. They work across teams and groups to innovate, drive forward our goals, and deliver for our clients. We have a diverse leadership team, but they are all united by their commitment to working together to serve our clients.

The past three years have been a challenge for any corporate culture. Isolation, followed by an uneven reopening, risks eroding corporate culture and making it harder for employees who are new to the team to learn and grow. This is something I hear from nearly every corporate leader I speak with.

Successful CEOs understand the need to build bonds with the full range of their stakeholders – but especially their employees. Last year, I wrote to corporate leaders about the importance of adapting to the new world of work and forging strong connections with employees. BlackRock research shows a strong correlation between companies with better culture and values ratings compared to industry peers and their stock returns.[13] More than a year later this imperative is even more essential. In a world where companies’ ability to attract the best talent can mean the difference between success and failure, building bonds that go beyond just a paycheck has never mattered more.

During the pandemic, BlackRock worked tirelessly to keep our teams connected and our culture vibrant. We even undertook a firmwide effort to renew and refresh the BlackRock Principles – which have guided us throughout our history. We now are focused on bringing our people back together in person, including in our new headquarters in New York and in our offices and with clients across the globe.

We always want to stay ahead of our clients’ needs, and to do so we need to maintain a focus on productivity, innovation, and connectedness. That means having people working side-by-side, not staring at one another on screens. As I look ahead, the major challenge for the next generation of leaders will be bringing people back to the office in order to forge the cultural bonds a company needs to succeed.

Our Board of Directors

Our Board plays a crucial role in our long term success, including reviewing BlackRock’s long-term strategy and evaluating the risks and opportunities for our business. Their diverse expertise and experience help guide the firm and strengthen our corporate governance.

We give careful consideration to the composition of our Board to ensure it is positioned to be successful over the long term. We are committed to evolving our Board over time to reflect the breadth of our global business and look for directors with a diverse mix of experience and qualifications.

We are incredibly fortunate to have had Beth Ford as a valued director of BlackRock, bringing new perspectives and expertise to the Board. In 2022, Beth decided it was appropriate for her to step down from our Board given her spouse’s new position as CIO of the Minnesota State Board of Investment. We are grateful for the many contributions that Beth made as a member of BlackRock’s Board.

Our Board shares my focus on ensuring we’re developing the next generation of leaders for the company. As we continually innovate and evolve our business to stay ahead of our clients’ needs, we also evolve our organization and our leadership team. Key to delivering the full power of One BlackRock to our clients is having a senior leadership team with deep experience, knowledge and connectivity across the entire firm – a team that embraces horizontal leadership.

We make organizational and leadership changes every few years because we believe these changes bring great benefits to our clients, our shareholders, our firm and to our leaders themselves. These changes keep us more tightly connected, and they stimulate fresh thinking, helping us better anticipate clients’ needs. In 2022, we announced several of our senior leaders would take new roles to enhance their diversity of experience, global perspective and One BlackRock connectivity that will allow them to lead BlackRock to new heights.

Gary Shedlin is one of the leaders who has had a profound impact on the BlackRock you know today. One of the changes to our leadership reflected Gary’s desire to take on a new role, once again working directly with clients. He is a great friend and has helped drive strong growth for BlackRock and our shareholders in the past 10 years as CFO and for many years before that as an advisor. I’m glad he’s continuing with us at BlackRock as a Vice Chairman focusing on a number of our strategic client relationships. I’m happy to be partnering with Martin Small as our new CFO. He has deep knowledge and expertise from his 16 years at BlackRock across a variety of different roles – a true example of someone who has demonstrated horizontal leadership at the firm.

Looking ahead

Writing this letter is always an opportunity to reflect on the past year and think about what the future might bring. When I wrote last year, Russia had just invaded Ukraine, globalization was shifting, inflation was rising and interest rates were about to move sharply higher. The world is still grappling with many of these changes and the market volatility that comes with them. I am so proud of how our leadership team guided our firm, delivered for our clients, created value for our shareholders, and gave back to our communities.

My deep belief in the power of the capital markets and the importance of being invested in them is as strong as it was when we founded BlackRock 35 years ago. I know that belief is firmly held by my colleagues at BlackRock across all parts of the organization. Their commitment to living our purpose, evolving ahead of clients’ needs, and making access to the capital markets easier and more affordable for people around the world make me incredibly optimistic for the future.

I’ve changed how I listen to music, but I return to some tracks again and again. The same is true when it comes to themes I advocate for on behalf of our clients. I use my voice to advocate for BlackRock’s clients, to encourage people to invest with a long-term perspective and to speak out about risks and opportunities that investors need to navigate. Since BlackRock’s founding, we have always been unwavering in our commitment to serving our clients, and by doing so, we have delivered outsized returns for our shareholders.

Endnotes

1U.S. publicly traded traditional large cap asset managers.(go back)

2BlackRock as of September 30, 2022. Cumulative cost-savings figure is calculated by taking the difference between the previous fund expense ratio and the new fund expense ratio from 2015 through September 30, 2022, multiplied by the fund assets under management at the time of the fund reduction. Methodology does not account for compounding savings over time.(go back)

3Source: Morningstar, ‘2021 U.S. Fund Fee Study’ page 14.(go back)

4Data is reflective of October 1, 1999– December 31, 2022. Past performance is not indicative of future results.(go back)

5Federal government current expenditures: Interest payments (NA000308Q) | FRED | St. Louis Fed (stlouisfed.org)(go back)

6Edelman Trust Barometer, January 2023, pages. 6-7(go back)

7Gallup, May 12, 2022(go back)

8Data is reflective of January 1, 2013– December 31, 2022. Past performance is not indicative of future results.(go back)

9Munich Re, January 10, 2023(go back)

10NFIP Debt, FEMA, November 4, 2022(go back)

11IEA, October 26, 2022(go back)

12https://www.blackrock.com/institutions/en-us/literature/investor-education/inflation-reduction-act-q-a.pdf(go back)

13BlackRock analysis, 2023(go back)