Print

PrintIra T. Kay is Managing Partner and Founder, Mike S. Kesner is a Partner, and Ed Sim is a Consultant at Pay Governance LLC. This post is based on a Pay Governance memorandum by Mr. Kay, Mr. Kesner, Mr. Kim, and Linda Pappas. Related research from the Program on Corporate Governance includes Rationalizing the Dodd-Frank Clawback (discussed on the Forum here) by Jesse M. Fried; Pay without Performance: The Unfulfilled Promise of Executive Compensation and Executive Compensation as an Agency Problem both by Lucian Bebchuk and Jesse M. Fried.

The SEC released its final version of the rules mandated by Dodd-Frank regarding the disclosure of pay versus performance (PVP) on August 25, 2022. Since then, thousands of calendar-year U.S. companies have been working diligently to prepare the required information for their 2023 proxies, including compensation actually paid (CAP), a new definition of compensation that is intended to demonstrate the potential value of total pay that has been or may be received by proxy-named executive officers. Importantly, many of the components included in the SEC’s definition of CAP are highly contingent on future financial performance and stock price and do not reflect compensation actually received during the year.

There is a long history of media, government officials, academics, pension funds, and investors criticizing U.S. companies for executive pay and performance disconnects. Such disconnects may be caused, for example, by large grants of time-vested shares and may also be driven in part by the use of grant date fair value of equity incentives that are not adjusted for actual, post-grant financial performance or stock price changes. These grant date values are currently disclosed in the Summary Compensation Table (SCT) and Grants of Plan-Based Awards Table. The SEC PVP disclosure is intended to provide investors with a clear analysis of the alignment or misalignment of the top executives’ CAP with the company’s financial and stock price performance over a 5-year period, starting with 3 years of data in the inaugural year. This analysis, while complex, was intended by the SEC to be viewed by investors as a window into the governance and workings of the company’s pay for performance model.

Pay Governance LLC has prepared this post using the PVP disclosure of 50 S&P 500 companies that filed their proxies on or before March 10, 2023, based on data collected by ESGAUGE. [1]

Our Analysis

Because virtually all publicly traded companies use short-term cash and stock-based incentives that are valued for CAP purposes using recent operating and stock price performance, it was expected that the SEC’s new PVP disclosure requirement would demonstrate some degree of alignment of the companies’ executive compensation with stock price and financial performance. What was unknown was just how strong the alignment might be and if the new disclosure would truly assist shareholders in understanding the relationship of a company’s pay and performance.

To begin addressing these questions, we used the 50 companies’ PVP data to calculate the degree of alignment based on the year-over-year (YOY) change in CAP compared to the YOY change in total shareholder return (TSR), relative TSR, GAAP net income, and the company selected measure. For this initial study, we focused on whether changes in CAP were directionally correlated with each company’s changes in TSR. We illustrate this approach in examples in Table 1 below. Future Viewpoints will explore the alignment with the other measures, but preliminary analysis of these measures also shows alignment with CAP (although to a lesser degree than observed with TSR in our initial sample).

Given the initial year’s PVP disclosure is limited to the 3 most recently completed fiscal years, our analysis reflects 2 years of change (i.e., 2021 vs 2020 and 2022 vs 2021) for 50 companies yielding a total sample size of 100 data points. Because the PVP disclosure adds an additional fiscal year each of the next 2 years, there will eventually be a “rolling” 5-year data set to evaluate the alignment of pay and performance.

We used the following taxonomy to categorize each data point:

- “Positive Alignment” is where the changes for both YOY CAP and YOY TSR are positive.

- “Negative Alignment” is where the changes for both YOY CAP and YOY TSR are negative.

- “Not Aligned, but Positive” is where change in YOY CAP is negative and change in YOY TSR is positive.

- “Not Aligned, but Negative” is where change in YOY CAP is positive and change in YOY TSR is negative.

Table 1: Illustration of Assessment of YOY CAP and TSR Alignment for Individual Companies

Table 1 (column b) shows that the Company 1 Principal Executive Officer’s (PEO’s) CAP increased by 40% from 2020 to 2021 and cumulative TSR (column c) increased by 45%. For 2021 to 2022, the Company 1 PEO’s CAP decreased by 141% and cumulative TSR declined 32%. Company 1 demonstrates positive and negative alignment in 2021 and 2022, respectively. It also illustrates the potential volatility of CAP and the substantial impact of stock price and earned or expected incentive payouts on CAP, which is what most compensation committees intend when designing and setting executive compensation. Table 1 (column e) shows that the Company 2 PEO’s CAP decreased by 3% from 2020 to 2021 and cumulative TSR (column f) increased by 12%. While not directionally aligned, it is unlikely shareholders would vote against Say on Pay in this situation. For 2021 to 2022, the Company 2 PEO’s CAP increased by 51% and cumulative TSR declined by 9% which falls under our category of not aligned.

Our Findings

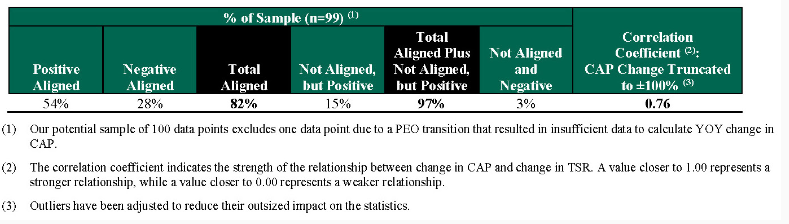

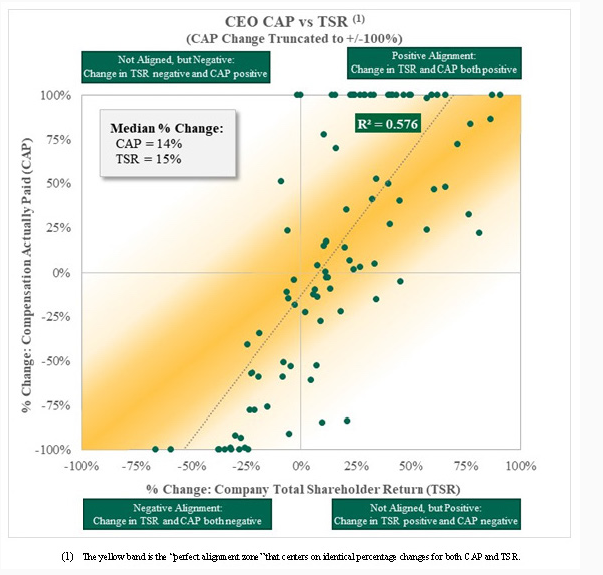

The overall findings for the full sample are straightforward and unambiguous, as seen in Table 2 and Chart 1: we find that the vast majority of companies have directionally aligned changes in CAP and cumulative TSR.

Based on our analysis, we found that:

82% of the companies in the analysis demonstrated directional alignment of change in CAP and cumulative TSR (53% positive and 28% negative alignment).

- Initial findings also show that 83% of the companies with positive alignment also outperformed the peer group TSR and that 86% of the companies with negative alignment performed below the peer group TSR.

15% of the companies in the sample had a negative change in CAP and a positive change in cumulative TSR, which we have labeled as “not aligned, but positive.” This may have been due to downward adjustments in expected performance share plan payouts and/or transition in CEO incumbents.

The remaining 3% of companies in the sample had positive changes in CAP and negative changes in TSR, which we have labeled “not aligned, but negative.” For this sample, it appears the disconnect was related to a substantial increase in compensation granted during the year and/or transition in CEO incumbents. Further, these same 3% of companies show positive alignment with both net income and the company-selected metric.

Table 2: Results of Analysis of Alignment of Change in CAP with Change in TSR

Chart 1: Change in CEO CAP versus Change in TSR for 50 S&P 500 Early Filers

Conclusions

While it may be too early to draw definitive conclusions given the relatively small sample size, our findings are encouraging: changes in CEO CAP show alignment to changes in Company TSR, which is what shareholders expect due to the significant proportion of CEO pay delivered through equity-based compensation. Should these early findings continue to show alignment, the new PVP disclosure would appear to support shareholders’ consistent strong support for Say on Pay over the past 12 years.

This new disclosure provides an additional tool to review pay decisions in the context of the relationship between pay and performance. While we believe the new PVP disclosure is a better tool for evaluating pay for performance than relying on the grant date fair value of equity awards, there are alternative methodologies for evaluating pay for performance alignment, such as a realizable pay [2] analysis, that evaluates a company’s relative realizable pay rank and performance rank over a 3-5 year period.

While this Viewpoint considers the directional alignment of changes in CAP and TSR performance, future Viewpoints will take a more in-depth look at these figures. For instance, we will examine the magnitude of such alignment and identification of the causal factors driving CAP besides TSR, such as the impact of changes in equity-based compensation grant values over time as reflected in the SCT and executive transitions.

Endnotes

1The analysis is based on data provided by ESGAUGE.(go back)

2Pay Governance’s definition of realizable pay includes the sum of salary, actual annual incentives/bonuses earned, time-vested equity awards valued as of the end of the measurement period, long-term performance plan awards valued as of the end of the measurement period (based on actual and/or projected payout levels), and the in-the-money value of stock options as of the end of the measurement period.(go back)