Print

PrintPeter Reali is Managing Director and Global Head of Stewardship and Anthony Garcia is Senior Director of Investment Stewardship at Nuveen. This post is based on their Nuveen memorandum.

Proxy voting is one of few systematic and comparable ways for stakeholders to compare how different managers view a company’s environmental, social, and governance (ESG) program. However, aggregating proxy votes by support levels and incentivizing leadership based on quantity of support for particular ESG themes or based on third-party leaders/ laggards lists means taking a snapshot that can inadvertently favor short-term stewardship proof points over long-term stakeholder progress.

In our view, the 2023 proxy season is likely to put the following four perspectives into the spotlight:

1. Market-first approaches or focus on thematic objectives without considering company- or industry-context will fail to regain the support levels from pre-2022 proxy seasons.

Recent proxy seasons suggest that large investors may advocate for companies to have impact where it supports long-term, sustainable value but are not mandating through the proxy vote a particular course of action for how and when companies must achieve impact.

2. Stewardship, and in particular proxy voting, may sometimes be better suited to mitigating negative outcomes than advocating for fundamental changes of the business to yield positive outcomes.

Proxy voting by itself is likely insufficient to catalyze fundamental change in a company business model. However, proxy voting can be a discrete signal that a company is lagging its peers on a material issue or is making insufficient progress in line with investors’ expectations.

3. There may be a growing disconnect between companies targeted for insufficient environmental and social (E&S) performance relative to a target rather than relative to industry peers or impact opportunities.

Long-term commitments are only as meaningful as the targets associated with those commitments and not all companies have the same level of impact alignment embedded into the targets.

4. Investors and stakeholders must seek balance between company comparability across ESG key performance indicators (KPIs) and the nuances of company and industry risks and opportunities if the goal is to work collaboratively toward solutions rather than pressure companies to meet unrealistic expectations.

The market has come to accept the limitations of a single ESG rating to encapsulate the entirety of a company’s strategy, operations, products, services, and the positive and negative externalities associated with each. Companies are beginning to shift away from ESG commitments that focus solely on improving third-party ESG ratings and toward company-specific narratives on how ESG strategies and KPIs influence business decisions.

To encourage companies to continue integrating ESG into core business strategies, investors must show evidence of bringing the enhanced disclosure into the investment process. No investor will disclose a specific investment thesis on a particular company, but proxy voting can be one avenue where investors can signal to companies an understanding (or lack thereof) and/or acceptance (or disapproval) of positive ESG momentum or an ESG strategy that is projected to create or hinder long-term value.

For investors that continually ratchet E&S expectations through proxy voting with the intent to raise market norms, upcoming proxy seasons may reach an end-game status where no more escalation is possible. Were this to occur, some asset managers may need to check the alignment between their stewardship and investment objectives and either reconsider stewardship strategies or understand that the only remaining strategy is divestment.

The outcomes of the 2022 proxy season included stakeholders calling both for more and less integration of ESG issues into investment decisions. Nonetheless, there is a viable approach to proxy voting that can navigate the sometimes conflicting incentives of balancing short-term conviction with long-term investment objectives.

2022 Proxy Season: The Bifurcation of ESG Importance

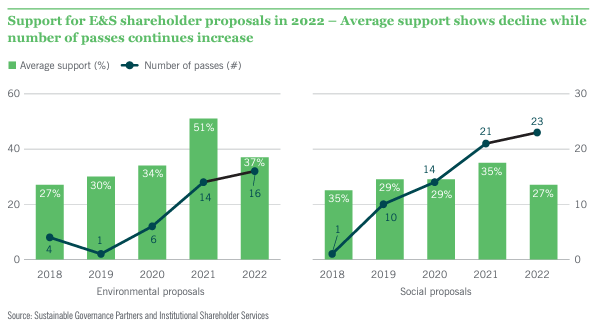

The 2022 proxy season contained mixed messages. On one hand, it was a record for both the number of E&S shareholder proposals filed and the number of E&S shareholder proposals that received majority support (941 and 562, respectively). [1] On the other hand, average support level for E&S proposals dropped to the lowest levels since 2018. [2]

Similarly, investors have signaled an expectation for company action on addressing stakeholder issues, yet the companies that currently account for the largest negative stakeholder externalities continue to receive high support for election of directors.

To understand the disconnect, it is important to acknowledge the differences between companies that have no defined strategy and companies that have demonstrated transparency and accountability to manage ESG risks but are not currently having an intentional and measurable impact for stakeholders.

The SEC’s updated interpretation of proposals with a “socially significant policy issue” changed the type of proposals that passed the no-action review process and were ultimately included in the proxy for a vote; additionally, the anti-ESG movement influenced aggregate shareholder proposal support levels as most investors choose not to support proposals that intended to rein in company ESG commitments. Companies have also internalized the investor views expressed in recent proxy seasons and are showing responsiveness to calls for increased transparency. [3]

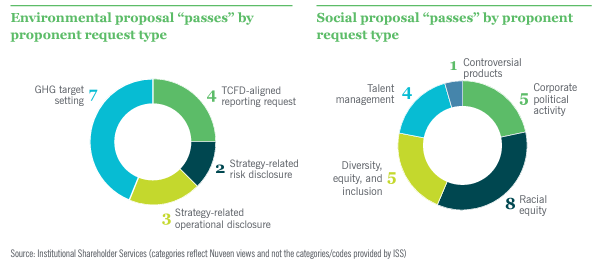

Beyond those specific influences, a takeaway from 2022 proxy season is that institutional investors focus on influencing company strategy or oversight whereas stakeholders more likely seek to influence company action. For example, proposals that requested the company take a specific action, such as elimination of financing to carbon-intensive businesses, received an average support of 21%, whereas proposals that sought general accountability through company strategy, such as setting GHG emissions reduction targets, received an average support of 39%. Looking even more closely, proposals that specifically requested targets inclusive of Scope 3 emissions received on average 36% support, whereas more general proposals on showing accountability through emissions reduction targets of any type received on average 63% support.

Director Elections: Strategy and Oversight Are Integrated Into Vote Outcomes and Investment Performance

Investors can vote with or against a director nominee but must balance all the individual and companywide ESG (and financial) assessments into one vote decision.

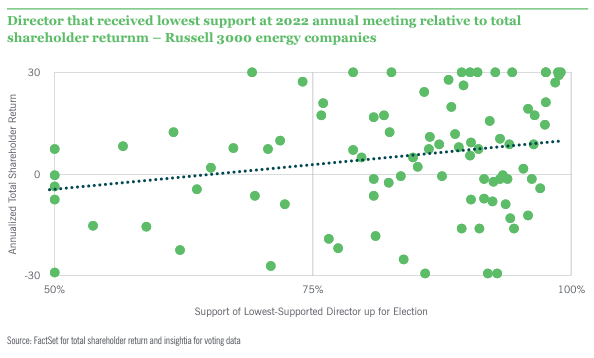

In looking at director support levels for carbon intensive industries such as the energy industry, there is no evidence that shareholders are targeting companies with the largest carbon footprints. Among the largest energy companies, no company had a director receive less than 80% support during the 2022 proxy season. Whether assessing carbon footprints on absolute emissions (the real-world impact) or emissions intensity (to standardized company climate performance regardless of size), climate impact is not driving investor dissent.

The existence of a positive correlation between emissions and director support is likely a matter of governance issues taking precedence over environmental or social issues in institutional investor voting and large-cap companies generally being aligned with governance best practices.

The correlation that has more explanatory power is total shareholder return, where poorly performing companies are more likely to have low director support. The performance-based perspective does not imply a disregard of climate risk but implies that the company strategy regarding how to address climate change is integrated into both proxy vote and investment decision-making.

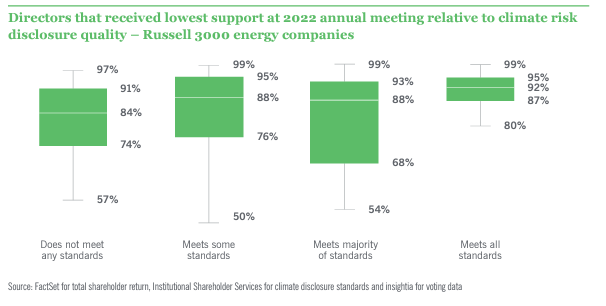

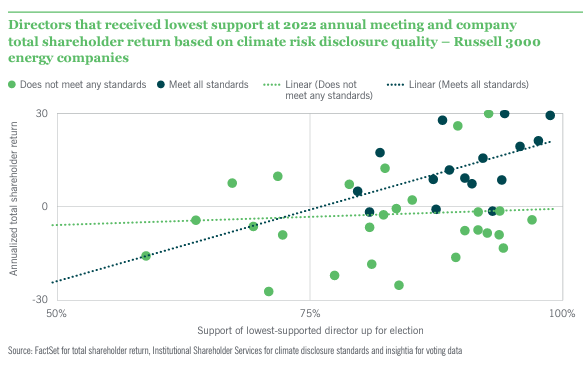

The alignment between director support and the quality of TCFD reporting perhaps most closely demonstrates how investors align investment and stewardship objectives. Companies that disclose robust climate-risk strategies in line with the TCFD

framework on average have higher levels of support than companies that are only partially aligned with the TCFD standards. Companies that do not provide any disclosure that meet TCFD standards have the lowest average levels of support.

The quality of TCFD reporting also has some correlation to company performance. Few companies with a robust climate strategy had negative absolute total shareholder return. Over the past three years, whereas companies without a clearly disclosed strategy saw more mixed performance.

What is most relevant in connecting stewardship and investment objectives is that the quality of TCFD reporting increases the correlation between total shareholder return and director support levels. The better the quality of climate-risk information that investors have for integration into the investment process, the more likely investors are to vote against (for) poorly (high-) performing companies. Investor understanding of company climate strategy creates more conviction in the assessment of future risks and opportunities which, in turn, influences both company stock price and director votes.

Expectations for 2023 proxy season

The pullback in shareholder proposal support in 2022 is unlikely to damper stakeholder advocacy in the 2023 proxy season. Rather, it is likely that stakeholders will escalate tactics to further their goals in the form of more targeting of directors, including the potential use of universal proxies to nominate new directors. As noted in Nuveen’s 2022 proxy season preview, there is a correlation between board refreshment and improving company decarbonization. The question for 2023 is whether investors see decarbonization as the intent or the byproduct of how the board oversees company strategy and how much the market focuses on past performance or company strategy as the indicator of future risks and opportunities.

Targeting Companies to Set Science-Based Targets

Company climate risk management often is evidenced through setting GHG emissions reductions targets. In this regard, validation of emissions targets by the Science-based target initiative (SBTi) is seen as a key credential. However, there remains a disconnect between the perceived level of corporate commitment and real-world decarbonization.

The disconnect has two potential sources: i) companies are more likely to make progressive climate commitments when the issue is less material to their operations, or business operations are naturally aligned with the trend in decarbonization; ii) the incentive provided to carbon-intensive companies to show “progress” has resulted in the transfer of intensive assets from companies more sensitive to stakeholder expectations to companies that are less influenced by stakeholder pressure or long-term risks.

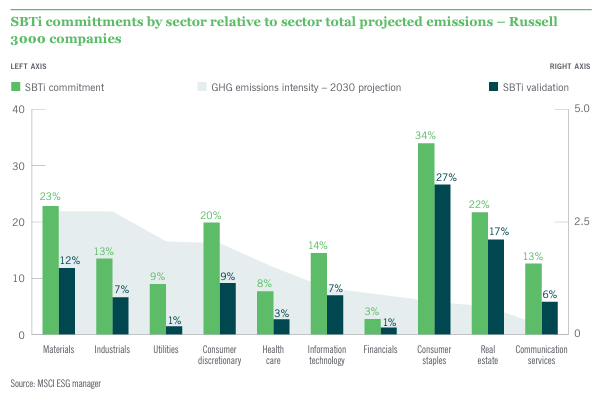

Approximately 13% of Russell 3000 companies have committed to SBTi target-setting and 7% have had some climate target validated by the SBTi. SBTi currently does not validate targets for oil/gas companies and banks. Therefore, two industries that are at the center of the stakeholder focus on climate risk and climate financing must be validated separately from the market-standard credential provided through SBTi.

In addition, there is a disconnect across sectors with the highest carbon footprints and the percent of companies that are committed to emissions reductions.

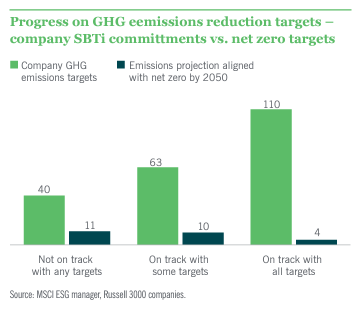

While SBTi status is often used as analogous with net zero standards, SBTi targets may be either near term, long-term, or net zero. Therefore, companies can potentially set short-term targets that are consistent with SBTi standards for alignment with the 1.5-degree goals of the Paris Agreement but still fall short of net zero standards. In fact, companies that are not meeting their company-set targets are nonetheless more likely to be aligned with net zero projections than companies that are on track with all company-set targets. In this regard, overemphasis on target-setting, but not necessarily focusing on the change implied by the company-set target, can have a detrimental effect on the long-term goal of a net zero economy.

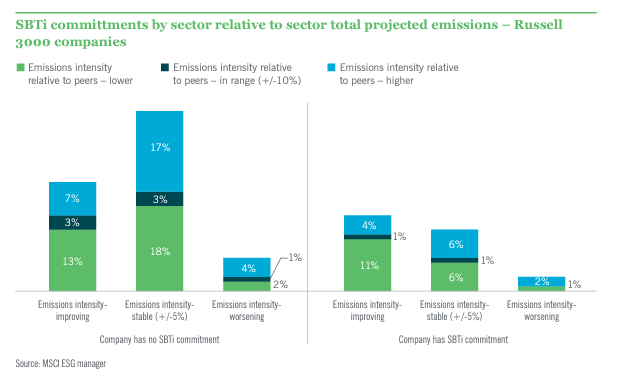

Another means of assessing companies is via actual decarbonization; both relative to peers and company specific progress. Overall, there are only 10% of companies whose emissions intensity has increased by more than 5% over the past three years. In this regard, stakeholders may be overprescribing specific company actions when the current strategy employed by most companies is directionally aligned with the long-term stakeholder goal of decarbonization.

On the other hand, companies with increased emissions intensity are twice as likely to already have higher emissions intensity relative to peers. Similarly, companies with emissions intensity lower than peers are twice as likely to be continuing to reduce emissions intensity. The small number of companies (10%) that operate close to the overall industry average in terms of emissions intensity shows a bifurcation in the market in terms of business models and/or commitment to carbon reduction.

In terms of stewardship, the question is whether the market is correctly identifying companies that represent the most significant risk, as well as the probability that stewardship can move a company from a worsening to improving category or from a higher to a lower category. In this regard, an SBTi

commitment does appear to drive higher levels of improvement. Nearly half of companies with an SBTi commitment are improving their emissions intensity whereas only about one-third of companies without such a commitment are improving their emissions intensity.

As investors shift the focus from achieving discrete outcomes to more long-term company assessments, the market may better understand how to best use stewardship resources to see company-specific improvement versus requiring a change in portfolio construction as the most effective means to mitigate company- or market-wide risk.

Expectations for 2023 proxy season

The focus on GHG emissions reduction targets should continue to garner significant support as well as catalyze positive momentum for decarbonization. In certain industries, clear evidence of decarbonization success strategies adopted by leading companies may translate into some strategy-specific proposals receiving significant support.

However, proposals that are overly prescriptive in terms of an unproven value-add business strategy, or a business strategy with the potential of significant unintended consequences, may continue the trend from 2022 of not having the same level of institutional support. Institutional investors may also begin to consider the quality of the targets being set or requested and the connection between those targets and company financial or stakeholder performance.

In this regard, aggregate support levels for climate voting activity may continue to remain below the 2021 high water mark; however, there is likely to be higher level of conviction behind investor support levels, which may include more willingness for escalation in subsequent years if the company does not develop a more robust forward-looking and long-term strategy.

There is a Diversity of Views Included In Votes on Diversity and Inclusion

While environmental shareholder proposals generally all intend the same impact, social proposals have a larger variety of intent. An “inclusive economy” is a more abstract concept compared to a net zero economy.

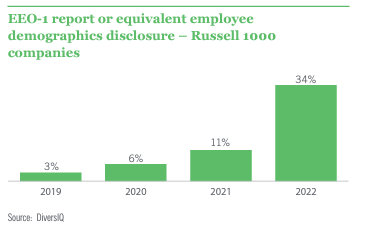

Nonetheless, there has been a strong call to action for companies to address diversity and inclusion, both internally, and externally as a matter of racial equity. The progress in company-provided disclosure has been more rapid than the decade-plus of advocacy for sustainability reporting to regulatory mandates for climate disclosure. For S&P 500 companies, which generally have the largest workforces in the U.S., more than 70% have voluntarily disclosed EEO-1 reports as of December 2022.

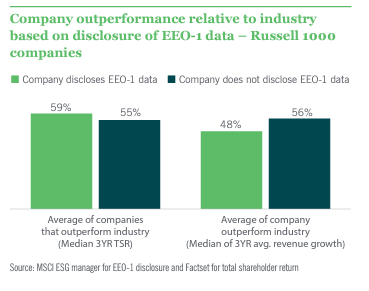

Transparency regarding workforce demographics will not itself cause impact. However, there are early indicators that companies that are being proactive in terms of transparency are recognizing the business imperative to improve workforce recruitment, retention, and promotion and focusing specifically on the portion of the population that historically has faced more systematic challenges in terms of career opportunity and development.

One interpretation of this chart is that companies that are transparent outperform the market in terms of TSR growth. The general sentiment of diversity outperforming from a business-case perspective is well-established in the marketplace. [4]

Beyond that, the implication of being a growth company generally includes a need to grow employee headcount. The snapshot view of EEO-1 reporting fails to address company risk or success in recruiting, retention, or promotion across the workforce, let alone in specific roles that will drive continued growth or where specific skills are most competitive in the market. In this regard, workforce diversity is not a static achievement but an ongoing process that companies must manage. It may also explain why companies that are growing less in terms of revenue growth are more stable in their human capital management and therefore more comfortable providing workforce snapshots. Whereas growing companies are concerned about volatility in demographic snapshots because of total workforce growth.

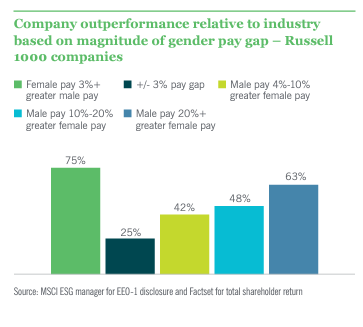

In addition, setting workforce targets has more potential unintended consequences relative to target and setting for GHG emissions and decarbonization. Research shows some pay inequality correlates to higher company valuation. [5] Similarly, the chart above demonstrates that companies with the lowest gap in pay inequality are most likely to underperform relative to industry peers and the proportion of outperformance increases with the magnitude of the pay gap. Nonetheless, firms where women earn more than men are the most likely to outperform industry peers.

The inequality is not necessarily driven by discriminatory (conscious or unconscious) corporate activities, but rather could be a byproduct of a company identifying its high-performing employees and investing in those employees through higher pay and promotion opportunities. While the sample of firms where women earn more on average than men is small, the outperformance may suggest that these companies have unlocked new and better means of understanding employee expectations and identifying employees that add value to the firm. Additionally, in the macro context, companies that are overly focused on philosophies such as equal pay for equal work or other narrow assessments of meritocracy may fail to realize a contagion effect of unconscious or systemic issues that will hinder human capital development over the long-term.

What is also missing from the analysis of looking only at relative market performance is whether, or to what extent, diversity is being appropriately valued. More nuanced research has noted lower future growth expectations for companies with higher percentages of diversity in management, and that these lowered growth expectations are generally misaligned with past financial performance of those companies. [6]

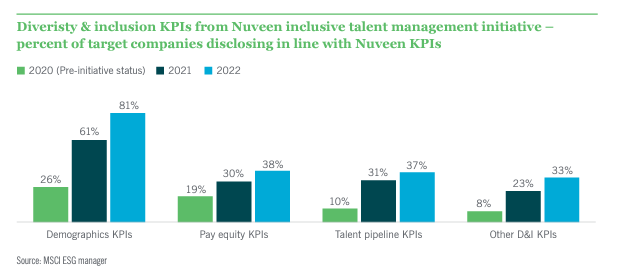

The Nuveen inclusive talent management initiative is not necessarily a market representative sample, but the set of focus companies nonetheless suggests that there is a disproportional focus on employee demographics and further opportunity to address pay equity, talent pipeline, and other material KPIs to create a more robust strategy regarding workforce diversity and inclusion.

It is likely that shareholder proposals for EEO-1 reporting at companies that have yet to disclose will receive significant support; similarly, given the rate of adoption of disclosure it is also likely that some investors will escalate the lack of disclosure into votes against directors.

Expectations for 2023 proxy season

It is likely that stakeholders will continue the focus on pay equity, but the support for shareholder proposals on the issue has been inconsistent year-over-year. In terms of getting to majority support, the question is whether pay equity is the goal itself or is the byproduct of better overall human capital management.

Other stakeholders request more open-ended disclosure improvements that address the talent pipeline, company culture, and racial equity. These proposals are likely to see significant support, but the reasons will vary across investors as many of these proposals encapsulate several issues and KPIs. While 30%+ support can still send a market signal, the lack of specificity on specific issues or KPIs will not give companies sufficient guidance beyond what is shared in engagement or investor vote rationales that are publicly disclosed. Assuming companies are responsive to majority-supported proposals for racial equity audits, the question is whether those reports include any information that wasn’t already part of company strategy.

Workforce diversity and inclusion is a subset of an inclusive economy which itself is a subset of the array of social issues stakeholders seek to address through stewardship. While the market is likely to evolve toward expectations of target-setting, strategic development, and impact on social issues, institutional investors have yet to coalesce around a set of KPIs to make such assessments. In this regard, stakeholders should be mindful of the CEO pay ratio, which is quantitative and disclosed by all companies, but has had limited value in driving stewardship objectives or informing investment objectives.

The Path Forward for an Efficient Stewardship Market

The analysis here does not imply that ESG investment or stewardship objectives are fundamentally flawed and should be scaled back. Instead, the nuance necessary for successful integration suggests that more, and increasingly diversified, efforts are necessary to develop proof points on the value, and the limitations, of stewardship activity in creating change.

The world is now profoundly altering the ways in which it generates and uses energy, as an example, so we believe “to divest or not to divest” isn’t even the right question – because it fails to capture the many, complex considerations that investors face in the energy sector. In fact, the right question is: “What does it mean today to invest in energy in a truly responsible manner – one that serves the best interest of both investors and the world at large?”

It’s a question with profound implications not only for investors, but also regulators and policymakers, nongovernmental organizations, investment standard setters, private business and even individual citizens. For our part, we firmly believe that ownership is a potent lever for redirecting and guiding existing assets toward better outcomes, financial and societal, for the investors we serve.

Endnotes

1Georgeson. A Look Back at the 2022 Proxy Season. Previous record for number of shareholder proposals voted was 438 in 2020 and previous record for number of proposals filed was 837 in 2021.(go back)

2Sullivan & Cromwell. 2022 Proxy Season Review: Part 1 Rule 14a-8 Shareholder Proposals. Shareholders submit the highest number of proposals; more proposals go to a vote; but average shareholder support decreases.(go back)

3Sustainable Governance Partners. The 2022 Proxy Season: Forces Collide. Companies negotiated withdrawals of proposal types that received high support in 2021, rather than risk adverse votes. Many other proposals – particularly focused on climate – sought specific strategic action and were viewed as too “prescriptive”.(go back)

4McKinsey. Diversity wins: How inclusion matters. The performance differential between the most and least gender-diverse companies was 48% in terms of company profitability relative to industry peers.(go back)

5Jefferies. Wages & Labor Expert Series: Pay Inequality May Lead to Higher Valuations.(go back)

6As You Sow. Workplace Diversity and Financial Performance: An analysis of Equal Employment Opportunity (EEO-1) Data. The two indicators most closely linked to analyst sentiment, Long-Term Future Growth Rate and PEG Ratio 12-month Forecast, had slight negative—albeit not statistically significant—associations with most of the diversity metrics, out of alignment with company performance. This implies that analyst-derived metrics may reflect a level of bias against diversity in management. In other words, greater BIPOC representation in management was shown to have a positive relationship with superior performance measures but is not always valued accordingly by brokers.(go back)