Print

PrintBrad Goldberg and Jaime L. Chase are Partners and Asher Herzog is an Associate at Cooley LLP. This post is based on a Cooley memorandum by Mr. Goldberg, Ms. Chase, Mr. Herzog, Cydney Posner, Reid Hooper, and Stephanie Gambino. Related research from the Program on Corporate Governance includes Short-Termism and Capital Flows (discussed on the Forum here) by Jesse M. Fried, and Charles C.Y. Wang; and Share Repurchases, Equity Issuances, and the Optimal Design of Executive Pay (discussed on the Forum here) by Jesse M. Fried.

On May 3, 2023, the Securities and Exchange Commission (SEC) voted at an open meeting to adopt final rules to require enhanced disclosure about issuer share repurchases under the Securities Exchange Act of 1934, as amended. The final rules will:

- Require tabular disclosure to be filed quarterly [1] in an exhibit to Forms 10-Q and 10-K of an issuer’s [2] repurchase activity aggregated on a daily basis, replacing the current requirements in Item 703 of Regulation S-K to disclose monthly repurchase data. Foreign private issuers (FPIs) filing on forms available exclusively to FPIs will have to disclose quarterly the same daily repurchase data on a new Form F-SR, in place of the current requirements in Item 16E of Form 20-F to disclose monthly repurchase data.

- Require a company to disclose quarterly via a checkbox whether any of its Section 16 officers or directors – or senior management or directors for FPIs – purchased or sold shares (or other units) that are the subject of a company share repurchase plan or program within four business days before or after the announcement of the plan or program.

- Revise and expand Item 703 to require a company to disclose in its Forms 10-Q and 10-K:

- The objectives or rationales for its share repurchases and the process or criteria used to determine the amount of repurchases.

- Any policies and procedures relating to purchases and sales of the company’s securities by its officers and directors during a repurchase program, including any restrictions on those transactions.

For FPIs, corresponding narrative disclosure requirements also will be added to Item 16E of Form 20-F.

- Add new Item 408(d) to Regulation S-K to require quarterly disclosure in Forms 10-Q and 10-K of a company’s adoption, material modification or termination of Rule 10b5-1 trading arrangements, as well as a description of the material terms of the trading arrangements.

Companies that file on domestic forms will be required to comply with the amendments to Forms 10-Q and 10-K (for their fourth fiscal quarter) beginning with the first filing that covers the first full fiscal quarter beginning on or after October 1, 2023. Therefore, for calendar year-end companies, the first report requiring compliance with the amendments will be the 2023 Form 10-K filed in 2024, as it relates to repurchases made during the quarter ending December 31, 2023. FPIs that file on FPI forms will be required to comply with the amendments in a new form, Form F-SR, beginning with the Form F-SR that covers the first full fiscal quarter beginning on or after April 1, 2024. For calendar year-end companies, the first Form F-SR would, therefore, have to be filed beginning with the quarter ending June 30, 2024. The amendments to the Form 20-F narrative disclosure will be required starting in the first Form 20-F filed after the FPI’s first Form F-SR has been filed.

Please see the SEC press release for the final rules and the condensed fact sheet for further details. For more background on the final rules and information on the SEC commissioners’ views and statements regarding the rules, which passed by a vote of 3 – 2 along party lines, see our May 2023 PubCo blog post.

Final amendments

Disclosure of daily repurchase activity

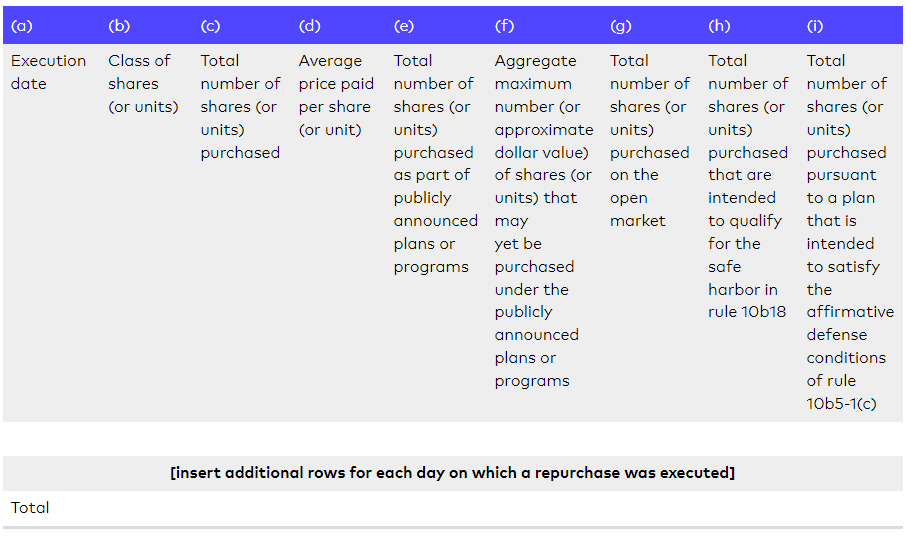

The final rules will require tabular disclosure on a quarterly basis of an issuer’s repurchase activity aggregated on a daily basis. For each day, the table will include:

- The purchase execution date.

- The class of shares.

- Total number of shares purchased.

- Average price paid per share.

- Total number of shares purchased on that date as part of publicly announced repurchase plans or programs.

- Aggregate maximum number of shares (or approximate dollar value) that may yet be purchased under a publicly announced plan.

- Total number of shares purchased on the open market.

- Total number of shares purchased that are intended to qualify for the safe harbor in Rule 10b-18.

- Total number of shares purchased pursuant to a plan that is intended to satisfy the affirmative defense conditions of Rule 10b5-1(c).

The final rules also require companies to disclose in a footnote to the table the date of adoption, material modification or termination of any trading plan for the repurchased shares that is intended to satisfy the affirmative defense conditions of Rule 10b5-1(c).

For companies filing on domestic forms, this daily repurchase data will be filed in a new exhibit to Forms 10-Q and 10-K. A copy of the required format for this table appears as an exhibit to this client alert and is set forth with the related rules in Item 601 (Exhibits) of Regulation S-K. In contrast, for FPIs that file on FPI forms, the data will be provided quarterly in a new Form F-SR, which must be filed within 45 days after the end of the FPI’s fiscal quarter. Notably, Form F-SR contains an instruction stating that the information on the form relates to the FPI’s securities in ordinary share form, whether the FPI has repurchased the shares itself or depositary receipts that represent the shares. In addition, an FPI that is required to disclose share repurchase information in its home country and furnishes that information on Form 6-K can incorporate by reference its Form 6-K disclosures into its Form F-SR.

As part of this requirement to aggregate the data by day, the final rules will eliminate the current requirements in Item 703(a) and Item 16E of Form 20-F to disclose monthly repurchase data in periodic reports.

In a change from the proposal, the daily quantitative repurchase data will be treated as “filed” instead of “furnished,” with the result that the new repurchase disclosure will be subject to liability under Section 18 of the Exchange Act and Section 11 of the Securities Act of 1933, as a result of potential incorporation by reference into Securities Act filings.

Checkbox regarding trading by officers or directors surrounding announcement of repurchase program

The final rules also will require companies to disclose quarterly via a checkbox whether any of its Section 16 officers or directors – or senior management or directors for FPIs – purchased or sold shares (or other units) that are the subject of a company share repurchase plan or program within four business days before or after the announcement of the plan or program, or the announcement of an increase in the size of an existing share repurchase plan or program. For companies filing on domestic forms, the checkbox will be included above the tabular disclosure of the daily repurchase data, while FPIs that file on FPI forms will check the box in new Form F-SR.

In addition, the release notes that a domestic filer may rely on filed Section 16 reports in determining whether it should check the box, provided that the reliance is reasonable. Because FPIs are exempt from Section 16 reporting, Form F-SR permits an FPI to rely on written representations from its senior management and directors in making this determination, provided that the reliance is reasonable.

Enhanced narrative disclosure

The final rules will revise and expand Item 703 of Regulation S-K to require a company to disclose in its Forms 10-Q and 10-K:

- The objectives or rationales for its share repurchases and the process or criteria used to determine the amount of repurchases.

- Any policies and procedures relating to purchases and sales of the company’s securities by its officers and directors during a repurchase program, including any restrictions on those transactions.

Corresponding narrative disclosure changes also will be made to Item 16E of Form 20-F. In response to comments expressing concern about potential exposure of confidential information, the SEC contended that, although the disclosure requirements “should convey a thorough understanding of the [company’s] objectives or rationales for the repurchases, and the process or criteria it used in determining the amount of the repurchase, the final amendments do not require [companies] to provide disclosure at a level of granularity that would reveal any competitive or sensitive information beyond what may already be gleaned from other disclosures regarding the business and financial condition of the [company].”

Notably, the existing requirements in Item 703 to disclose in a footnote to the monthly table the principal terms of all publicly announced repurchase plans or programs – and the number of shares purchased other than through a publicly announced plan or program, including the nature of the transaction – will still apply. However, this disclosure will now be required in the main text of the narrative discussion since the monthly table has been eliminated.

Disclosure regarding Rule 10b5-1 trading arrangements

The final rules will add new Item 408(d) to Regulation S-K, which will require companies to disclose on Forms 10-Q and 10-K their adoption, material modification [3] or termination during the covered quarter of a Rule 10b5-1 trading plan or arrangement regarding their own securities. Companies also will be required, pursuant to Item 408(d)(1), to provide a description of the material terms of the trading arrangement (other than pricing terms) – such as the date of adoption, material modification or termination, duration of the arrangement and the aggregate number of securities to be purchased or sold pursuant to the arrangement. Furthermore, to prevent potential duplication, a note is included in Item 408(d)(1) stating that, if the disclosure provided pursuant to Item 703 contains disclosure that would satisfy the requirements of Item 408(d)(1), a cross-reference to that disclosure will satisfy the Item 408(d)(1) requirements. FPIs are not required to provide disclosure under Item 408(d).

Importantly, unlike the rules relating to trading arrangements entered into by individuals, the final rules do not require disclosure of any company “non-Rule 10b5-1 trading arrangements.”

New Item 408(d) will be added to Part II, Item 5, “Other Information” of Form 10-Q and Part II, Item 9(b), “Other Information” of Form 10-K.

Inline XBRL

Consistent with other recent disclosure rules proposed and adopted by the SEC, the final rules require companies to “tag” information disclosed pursuant to Items 601 and 703 of Regulation S-K, Form F-SR and Item 16E of Form 20-F using Inline XBRL. The requirements include detail tagging of quantitative amounts disclosed within the tabular disclosures, as well as block text tagging and detail tagging of required narrative and quantitative information.

Observations and commentary

- The final rules depart from the initial proposal – mostly in a company-friendly way. Perhaps due to the large number of comments received that opposed the proposed rules, the final rules made changes from the proposal that are largely beneficial to companies. Most importantly, the final amendments require disclosure of the daily repurchase data to be filed quarterly, instead of one business day after execution of a share repurchase, as was contemplated by the proposal. This change should greatly reduce the administrative burden of this rulemaking, especially given that companies are already accustomed to providing repurchase information in periodic filings. The final rules also modified the period used to determine the need to check the box for trading surrounding the announcement of a repurchase program from 10 business days to four business days.

- Companies should review and update internal controls as they relate to share repurchases. Although companies should already have disclosure controls and procedures in place regarding share repurchases, these controls and procedures will likely require updating to reflect the changes in the final rules from aggregating the repurchase data on a monthly basis to aggregating on a daily basis. In addition, in order to determine whether to check the box relating to trading surrounding the announcement of a repurchase program, companies will need to establish controls to ensure that Section 16 filings are reviewed on a timely basis – or, for FPIs, that written representations from senior management and directors are timely received.Furthermore, recent SEC enforcement actions have applied the internal control provisions of the Exchange Act expansively to include policies and procedures concerning the handling of material nonpublic information. This trend – combined with the fact that daily repurchase information will now be readily available to scrutinize the timing of a company’s repurchases – makes it even more critical that companies have internal controls and processes in place that are reasonably designed to ascertain whether the company may be in possession of material nonpublic information at the time of any share repurchase.

- FPIs hit with quarterly disclosure requirement. Although the final rules were better than expected for domestic filers, they present a dramatic change to the reporting requirements for FPIs. Until now, the long-standing approach of the SEC was to generally defer to an FPI’s home country requirements, requiring only the annual filing of a Form 20-F and Form 6-K under specified circumstances. With the adoption of the disclosure requirement for daily repurchase data on Form F-SR, FPIs will now be subject to regular quarterly reporting that will require careful preparation and additional ongoing work. In addition, to the extent that FPIs are subject to home country disclosure rules regarding share repurchases, they might now also be subject to multiple, differing or even conflicting disclosure regimes.

- Board approvals of share repurchase programs should contemplate the final rules. Given the expanded disclosure requirements regarding an company’s rationale for each repurchase plan or program, and the process or criteria used to determine the amount of repurchases, the board of directors should consider these issues and think about documenting such consideration in the resolutions or minutes when approving a share repurchase program. In addition, management responsible for a company’s SEC disclosures should review the resolutions and/or minutes from the applicable board meeting when crafting the required disclosure to ensure it is accurate and supported by the company’s records.

Exhibit: Tabular disclosure of daily repurchase data

Issuer purchases of equity securities

Use the checkbox to indicate if any officer or director reporting pursuant to Section 16(a) of the Exchange Act (15 U.S.C. 78p(a)), or for foreign private issuers as defined by Rule 3b-4(c) (§ 240.3b-4(c) of this chapter), any director or member of senior management who would be identified pursuant to Item 1 of Form 20-F (§ 249.220f of this chapter) purchased or sold shares or other units of the class of the issuer’s equity securities that are registered pursuant to section 12 of the Exchange Act and subject of a publicly announced plan or program within four (4) business days before or after the issuer’s announcement of such repurchase plan or program or the announcement of an increase of an existing share repurchase plan or program.

Endnotes

1Other than for listed closed-end funds, for whom the final rules are different and not addressed throughout this alert.(go back)

2For purposes of this alert, the term “issuer” includes affiliated purchasers and any person acting on behalf of the issuer or an affiliated purchaser.(go back)

3A material modification is a modification or change to the amount, price or timing of the purchase or sale of the securities underlying a Rule 10b5-1 trading plan or arrangement.(go back)