Print

PrintMaria Castañón Moats is Leader, Paul DeNicola is Principal, and Matt DiGuiseppe is Managing Director at the Governance Insights Center at PricewaterhouseCoopers LLP. This post is based on their PwC memorandum.

When done right, director-shareholder engagement can pay dividends for both the investor and the company. We identify the key steps for directors—and investors—to get the most out of these exchanges.

Years ago, “shareholder engagement” was an earnings call led by the company’s CEO and CFO, or a

meeting with the investor relations team. Any contact was handled by company management.

Today, the picture is quite different. In PwC’s 2021 Annual Corporate Directors Survey, more than half (53%) of directors say that board members (other than the CEO) engaged directly with the company’s shareholders during the prior year.

Part of this shift in engagement relates to investors’ recent focus on environmental, social and governance (ESG) concerns, and the desire to hear from directors about how the company is approaching those issues. In 2021, ESG topped strategy as the most common discussion topic, it was raised in 43% of discussions, up from 23% in 2020. [1] Directors can be well-positioned to give investors a long-term view of the company’s plans.

The engagement can often be beneficial for both parties. Shareholders can express their concerns about the company and hear directors’ perspectives. They test out the rigor of the board’s oversight and gain insight into the company’s strategic plan. For their part, directors can learn about shareholders’ priorities and their concerns about the company.

Largely, it is about building a relationship. With that foundation in place, an investor may find that the company is more open to hearing its views and suggestions. From the company’s perspective, having the relationship in place could help if an activist investor comes along. Directors will already understand how key shareholders feel about company strategy, board composition, the management team and other issues. Essentially, a board with good shareholder relationships may be able to build up credit that it can draw on if times get tough.

Directors are much more comfortable with engagement than they used to be. Back in 2014, 42% of directors very much agreed that shareholder engagement presented too great a risk of disclosing non-public information and violating Regulation FD (Fair Disclosure). By 2018, that figure had dropped to 19%. And only 6% very much agreed that directors don’t have time to meet with investors—down from 19% in 2014. [2]

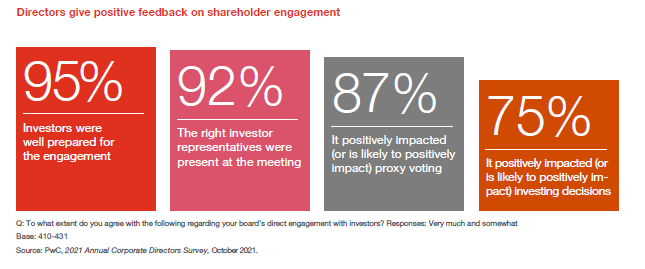

Directors also report positive views of shareholder engagement, by and large. The vast majority believe the right investor representatives are at the meetings, investors are well prepared, and the engagement has positive effects on proxy voting and investment decisions.

But even with all of the improvements in the process, both directors and investors still report some frustration. Even with all the right intentions, the parties sometimes come away thinking that the engagement was a waste of time.

So how can investors, directors and management ensure their engagements are a success? Here, we outline three key steps for getting the most out of shareholder engagement.

Looking ahead on shareholder engagement

As the nature of shareholder engagement continues to evolve, directors will need to be more agile and more responsive. The number of engagements requiring director participation will likely grow, as will the scope and breadth of topics covered. And directors will play a part not just in the pre-planned meetings, but also in emergency communications during times of crisis. To meet the challenge, well-prepared boards will work closely with a cross-functional management team, and will have not just one camera-ready director, but several.

Step 1: Lay the groundwork

Focus on the proxy statement and company website

The foundation of shareholder engagement is the proxy statement. In the past, it was primarily viewed as a compliance document. Lawyers encouraged streamlined disclosures, and boilerplate language was the norm. Now, many companies see that it can also be a valuable communications tool.

If it’s written well, the proxy can provide shareholders with more transparency and better insight into the company and the board. Such transparency can build greater trust. More companies are also clarifying and simplifying information. They’re using executive summaries, graphics and tables. Some are even including answers to the frequently asked questions they get from investors in the executive summary. And they are taking the opportunity to highlight the good work the company is doing.

Directors rarely have much involvement with proxy statements, even though the audit and compensation committees have to include reports that confirm they carried out specific responsibilities. Management drafts these reports, often using standard language, and then asks the committees to approve them.

By getting involved earlier in the process, directors may be able to encourage management to improve the proxy disclosure. Trends we are seeing include:

- Compensation committees are supporting simplification of the compensation discussion and analysis (CD&A) by encouraging management to present the information in executive summaries, charts and

graphs. - Audit committees are responding to pressure from investors for more information on external audit oversight. [3]

- Nominating and governance committees are pressing for better proxy descriptions in areas like board composition, board recruitment, succession planning and board performance assessments.

- Directors are encouraging management to provide additional disclosure on key issues like cybersecurity oversight and how the company is addressing ESG risks.

But the proxy statement can’t cover everything. The company’s website can serve as an important resource for information that doesn’t naturally fit into the proxy. This includes matters like social or environmental initiatives at the company.

Clear and informative proxy disclosure makes shareholder meetings more efficient. Investors come with a well-defined picture of the board’s key oversight processes and how the company’s executive compensation plans operate. That saves directors from having to spend time clarifying basic information.

Tip: Seek constructive feedback on the proxy statement. Shareholders may have helpful tips about how it could be revised to better convey what the company is doing.

Time the engagement properly

For companies, shareholder engagement is likely to be top of mind during the one or two months before the annual shareholders’ meeting. Management wants to avoid surprises on key votes. That can mean talking to shareholders about their concerns.

Most companies hold their annual meetings in the late spring. Since institutional investors are responsible for voting shares at thousands of companies, they are extremely busy just at the time engagement requests from companies start flooding in. So it’s not a great time to try to build relationships. And generally shareholders will have to decline engagement requests unless there’s a vote where they need additional information—like a proxy contest.

Instead, the most effective shareholder engagement ideally occurs during a relatively calm time, outside of proxy season. Directors and investors can get to know one another and build trust. This gives shareholders more time to think about the company’s specific issues, and gives directors the chance to explain the company’s strategy and perspective. If the first conversation comes instead when the company faces a “crisis” (such as an activist threat), shareholders may be more skeptical about the outreach. And a director’s message could be inherently less credible.

Sometimes, engagement isn’t needed. The company may make the offer to investors and find that they aren’t interested in meeting with directors. Shareholders don’t have the time to meet with every company in their portfolio. But even if they decline the offer, they’ll usually make note of it, and that alone can benefit shareholder relations.

Tip: Make every effort to engage and build relationships with shareholders during the calm times. Those relationships will pay dividends when the company is facing an activist or other crisis scenario.

Creating a strategic plan to get started on shareholder engagement

- Get directors involved. If a shareholder specifically asks for director participation, the board needs to respond to that request. If shareholders have not asked, consider offering the opportunity.

- Target shareholders. Many companies reach out to just their top handful of investors every year. While these investors are important, companies may be overlooking other key shareholders, such as pension funds, who are often proactive leaders in corporate governance.

- Prepare with dry runs. For directors new to shareholder engagement, a dry run with the general counsel and investor relations team can be helpful to understanding the scope of the conversation and to feeling comfortable within the confines of Regulation FD.

Step 2: Prepare properly for the meeting

Do your research

Investors and directors alike tell us that meetings work best when everyone prepares.

First, agree on an agenda. If investors have specific issues they would like to discuss, be prepared to respond to each one. If the company is proposing the meeting, offer a specific agenda with strong reasoning for the inclusion of each item. In either case, make sure both parties are fully on board with the agenda.

Once the agenda’s confirmed, management can send relevant materials to the shareholder in advance. Summaries of board makeup, company strategy or executive compensation can help, as long as they don’t end up disclosing material nonpublic information. Shareholders can use those resources and their own research to update their knowledge about the company, its governance policies and the directors who’ll attend.

Management and the directors involved will do their own homework, first by understanding the investor’s stock holdings (including whether they’re indexed). Then, research their views on governance. Most of the large institutional shareholders publish their own policies, and do not rely on proxy advisory firms for guidance.

The directors can also beef up their understanding of the board’s decisions on relevant matters so they’ll be able to explain them clearly in the meeting. If, for example, the investor wants to talk about the company’s ESG strategy, directors will benefit from meeting with the chief sustainability officer (or other executive heading up efforts) to really understand what the company is doing, before talking with the shareholder. If the meeting is happening in the context of an upcoming vote, reviewing the proxy statement prior to the meeting is also recommended.

Tip: Mutual agreement on the agenda is crucial. Both parties need to come to the meeting with a clear view as to what will, and what will not, be discussed.

Invite the right participants

A successful meeting requires gathering the right people. From the company’s perspective, the agenda drives which directors will attend. If the matter to discuss is executive compensation, for example, it’ll be the compensation committee chair. If the subject is board composition, the nominating and governance committee chair or lead director will attend. In some cases, more than one director may end up participating.

That said, the fact is that not all directors are equally adept at communicating. So pick a director who is “camera ready.” Often that can mean someone who was (or is) a CEO or CFO. They have experience addressing investors and analysts, and a good sense of what to say and how—and perhaps more importantly, what not to say. Any director engaging with shareholders needs to be diligent about avoiding disclosure of material nonpublic information that would violate Regulation Fair Disclosure (Reg FD). No company—and no investor—wants to create a Reg FD problem.

Tip: Prepare and practice for the meeting. Directors may even conduct dry runs with the legal and investor relations teams.

On the investor side, the question is whether the portfolio managers or the stewardship teams (or both) should be involved. For many investors, these teams occupy separate silos. The portfolio manager attends earnings calls and the stewardship and proxy voting professionals execute the voting process’s. If an investor holds the company’s stock through index or exchange traded funds, it’s likely less important for the portfolio manager to attend. Why? Because no amount of engagement with directors will change any investment decisions. But for shareholders with active fund managers, involving both the relevant portfolio managers and the stewardship and proxy voting teams can signal that the engagement has broader consequences than just proxy voting.

Tip: Confirm all attendees at the meeting and understand each person’s specific role so you can prepare accordingly. The content of the meeting will be different if, for example, the portfolio manager is attending.

Step 3: Conduct an effective meeting—and follow up

Find the right balance

Both shareholders and directors tell us that the engagement is most productive when the shareholder does more of the talking. Directors’ perspectives are important. But for many investors, their priority is to make sure the board understands their concerns.

By really listening to what shareholders have to say, directors can learn what issues their shareholders are focusing on and perhaps get an early signal of problems—issues that could spark a shareholder proposal or even draw an activist in the future.

Tip: Listen more than you talk.

Come with an open mind

It can be uncomfortable to hear criticisms of the company, or to feel that the board’s decisions are being second-guessed by an outsider. It’s natural for a person to become defensive, and even reject such views outright. But for directors, the skill of listening to shareholder concerns about the company with an open mind, rather than a defensive posture, will benefit the board and the company. Sure, the investor doesn’t have the same level of detailed understanding of the company that the board and management does. But investors do offer another perspective, one that is often carefully researched and thought through. There perspectives are also influenced by the hundreds, or thousands, of meetings they hold each year. And they may offer some very useful ideas for the director to bring back to the boardroom—or at least signal areas where the company may want to improve its disclosure.

The role of shareholder proposals

Directors often think of a shareholder proposal as a line of attack, or an escalation tactic. But some investors think of it as a first step in engagement. Once they open the line of communication with the company, they may be very willing to discuss the issue and come to a resolution that results in them withdrawing the proposal.

Follow up

The actual meeting is important, but engagement just for the sake of engagement misses the mark. For the experience to really be impactful, there is more work to be done after the meeting.

Directors who met with the shareholder can bring any suggestions or concerns they heard back to the boardroom. Then the full board can discuss the feedback. Even if the board ultimately doesn’t agree with the shareholder’s view, it can be helpful to look at issues from that perspective.

Investors, for their part, can incorporate the information they learned during the meeting into their proxy voting decisions. Or the meeting may alter the way they apply their voting guidelines to the company.

After the meeting, in addition to delivering on any follow-up requests from the shareholder, management can think about how to reflect the engagement in the proxy statement. Investors will know what their own engagement experience with the company has been, but they don’t have a picture of the company’s broader outreach. And proxy advisors don’t have any visibility into private engagement at all. A fulsome description of the shareholder engagement process in the proxy statement helps to provide that context.

Some companies detail the number or proportion of shareholders they met with and whether directors

participated in the engagement. They list topics or items discussed during the meetings. And they may note either the changes that the company is implementing (or considering implementing) as a result of the discussions, or its reasons against making changes. By putting some thought into the description of the engagement process, the company can demonstrate that it views the process as a useful experience, rather than a check-the-box exercise. Shareholders may be much more receptive to future engagement if they can see how past engagements made a difference at the company.

Tip: The engagement is not over when the meeting concludes. Ensure that the full board receives a report on the engagement. Incorporate relevant disclosure into the proxy statement, and bring the engagement full circle by realizing any necessary changes at the company or the board.

Making the connection between shareholder engagement and board member skills

Describing how and why the board engages in shareholder outreach is a crucial first step in improving proxy disclosure on the topic. But savvy companies take it further by making the connection to their board composition. When investors read that directors are discussing certain topics with shareholders, they want to know what makes those directors qualified on that topic. If they discussed executive performance—does the director have specific expertise in executive talent management? If they discussed the company’s cyber strategy—does the director have a cyber background? By leveraging disclosure about directors (including any skills matrix), companies can draw these connections and illustrate what the directors bring to the discussion.

Conclusion

When done thoughtfully, engagement can be incredibly useful for both the company and the investor. Investors have a chance to share their concerns with some of the key decision-makers at the company. And for boards, the benefits are often even greater. Not only can they learn from their investors, but they are building and solidifying a key stakeholder relationship. If and when the next company crisis hits, having that relationship in place can be a significant benefit for the company.

Endnotes

1PwC, 2021 Annual Corporate Directors Survey, October 2021.(go back)

2PwC, 2018 Annual Corporate Directors Survey, October 2018.(go back)

3See the Center for Audit Quality’s Audit Committee Transparency Barometer.(go back)