Print

PrintBrian Tayan is a researcher with the Corporate Governance Research Initiative and David F. Larcker is the James Irvin Miller Professor of Accounting, Emeritus, at Stanford Graduate School of Business. This post is based on their recent paper. Related research from the Program on Corporate Governance includes Paying for long-term performance (discussed on the Forum here) by Lucian Bebchuk and Jesse M. Fried.

We recently published a paper on SSRN (“Mega Grants: Why Would A Board Approve Nine-Figure CEO Pay?”) that examines the practice of awarding “mega grants” to CEOs.

Mega grants are large, one-time equity awards with long vesting periods (up to 10 years) granted in lieu of or in addition to annual awards with the intended purpose of providing significant incentive to achieve long-term targets. Mega grants were popular in the late 1990s (having been awarded to the CEOs of Oracle, Walt Disney, IAC/Interactive, and others) but fell out of favor in response to shareholder criticism. A 2005 accounting change that required companies to record the fair value of equity awards in the financial statements further decreased the attractiveness of large-scale option awards.

This trend has reversed in recent years, with executives receiving nine-figure awards once again appearing on annual lists of the highest paid CEOs. The reasons behind this change are unclear. Some see a turning point following the decision of Apple to grant a one-time equity award (with 5- and 10-year vesting provisions) valued at $376 million to CEO Tim Cook in the first year he succeeded Steve Jobs as CEO. The board explained its decision: “In light of Cook’s experience with the company, including his leadership during Jobs’s prior leaves of absence, the board views his retention as CEO as critical to the company’s success and smooth leadership transition.” In subsequent years, the CEOs of other large technology companies succeeding long-time founders—such as those of Microsoft and Alphabet—also received mega grants.

Another turning point occurred in 2018 when the board of Tesla awarded CEO Elon Musk a performance-vested stock-option package valued at up to $56 billion, based on achieving an aggressive series of market capitalization, revenue, and cash flow targets over a 10-year period. Musk already had significant incentive to perform, owning 22 percent of the company (worth $13 billion). Nevertheless, the company’s chairman described the award as a case of “heads you win, tails you don’t lose” with shareholders benefitting from significant share-price appreciation in the event of success and zero payout to Musk otherwise. Musk ultimately achieved many of the performance goals (despite experts describing them as “laughably impossible”), catapulting the company’s valuation above $1 trillion and Musk’s net worth for a time above $200 billion. Subsequent years witnessed a small surge of technology company CEOs (including founder CEOs) receiving nine-figure mega grants, which Bloomberg described as “Elon Musk copycats,” presumably in their hopes of achieving similar outcomes.

Nevertheless, mega grants are highly controversial. Critics of CEO compensation, who already find average annual pay levels objectionable, balk at a determination to grant one-time awards valued at many multiples of annual levels. Mega grants are criticized when they vest based on a single performance trigger (such as stock price) or no performance trigger at all (time-based vesting). Others dislike aggressive payout structures for their potential to encourage excessive risk-taking—the pursuit of high-risk, high-reward projects whose failure cause severe damage to the company. Mega grants can also pose public-relations problems. For example, some questioned the decision of Alphabet’s board to grant a $226 million one-time equity award to its CEO three months after laying off 12,000 employees.

Proxy advisory firms take a skeptical view of mega grants. Glass Lewis advises that “shareholders should be generally wary of awards granted outside of the standard incentive schemes.” The firm requires that companies provide “a thorough description of the awards, including a cogent and convincing explanation of their necessity and why existing awards do not provide sufficient motivation and a discussion of how the quantum of the award and its structure were determined.” ISS cautions that

“Very large awards that are intended to cover future years of incentive pay limit the board’s ability to meaningfully adjust future pay opportunities in the event of unforeseen events or changes in either performance of strategic focus. For this reason, ISS is unlikely to support grants that cover more than four years (i.e., the grant year plus three future years). Commitments not to grant additional awards over the covered period should be firm.”

Friestedt and Nwankwo (2019) find that ISS recommends against a company’s say-on-pay 80 percent of the time in a small sample of companies that awarded mega grants. ISS also recommends against the reelection of at least one member of the compensation committee 69 percent of the time among these companies.

Not surprising, lawsuits have been filed against boards issuing mega grants. Examples include a suit against Mullen Automotive for offering compensation “completely out-of-line with not only peer compensation arrangements, but compensation arrangements at the largest companies;” against the board of Masimo for “abdicating their fiduciary duties” in approving compensation that is “unmatched in its overreach;” and Cloudflare for concealing details of vesting provisions from shareholders when asking their approval of a mega grant.

Despite the opposition, a notable number of companies have awarded mega grants to their CEOs in recent years. Given the controversy surrounding them, why does this occur? In this Closer Look, we examine the types of awards granted, the circumstances of their grant, and shareholder reaction.

Mega Grants

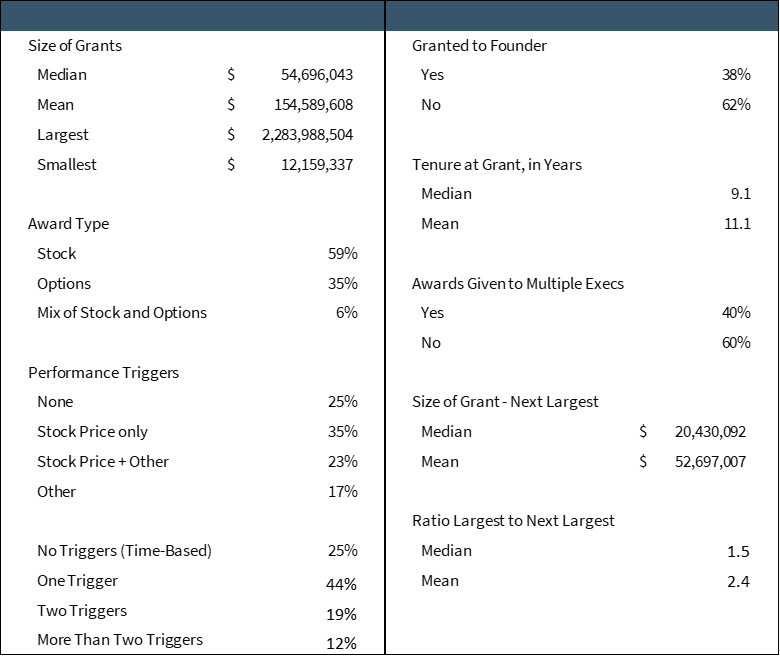

Our sample includes 52 mega grants valued at $10 million or more between 2016 and 2022 (as identified by Equilar). Three companies in our sample (Alphabet, NVR, and Oracle) issued more than one mega grant during this period, and so our sample includes 48 individual companies. See Exhibit 1 for descriptive statistics.

Primary recipient. Mega grants are usually given to the CEO. In our sample, 88 percent of grants were issued to the CEO. In some cases (12 percent), the primary recipient was the executive chairman, president, or chief financial officer. (We describe the practice of issuing mega grants to more than one named executive officer below.)

A surprisingly large percentage of mega grants are given to company founders. 38 percent of recipients are the founder of the company. This is surprising because founders generally already have significant incentive to perform. For example, Oracle routinely gives mega grants to founder and Chairman Larry Ellison, despite his large personal ownership in the company (43 percent). He is not the lone example. In our sample, the CEOs of LendingTree, Enstar, CrowdStrike, Regeneron Pharmaceuticals, and other founder CEOs received special grants.

Tenure at grant. Furthermore, mega grants are not (typically) given to newly appointed CEOs. In our sample, the recipient has been CEO for a median 9.1 years (average 11.1 years). Only 13 percent of recipients (7 out of 52) were CEO for less than 1 year at the grant date. This suggests that grants are not primarily given as part of a new employment contract or to meaningfully step up the ownership stake of a newly appointed CEO.

Size. Grant sizes vary significantly across companies. The smallest mega grant in our sample was given to the CEO of Liberty Broadband in 2020 ($12.1 million) while the largest was given to Elon Musk at Tesla in 2018 ($2.3 billion). In our sample, the median size is $54.7 million, and average size is $154.6 million. These values represent the fair-market value on the grant date, as determined by the company and disclosed in the financial statements and proxy.

While large in absolute dollars, these values are not extreme relative to the market capitalization of the company as a whole. The median (average) mega grant as a percentage of the market capitalization of the company is only 0.67 percent (1.78 percent). Still, a few mega grants in our sample are notable for their large value relative to market capitalization:

- Axon Enterprise (2018): 16 percent, $246.0 million

- Stereotaxis (2021): 11 percent, $57 million

- Affirm (2021): 5 percent, $451 million

- Sorrento Therapeutics (2020): 4 percent, $150 million

- Tesla (2018): 3.8 percent, $2.3 billion

Equity. Grants are more likely to take the form of stock (restricted or performance-vested) than options. 59 percent of grants are stock compared with 35 percent options, whereas 6 percent include a mix of stock and options.

Term. Despite their reputation for being “long-term,” mega grants are surprisingly short in duration. Both the median and average term in our sample is only 5 years. Only 8 of the 52 grants (15 percent) have a term of 10 years. 10 of the 52 grants (19 percent) have a term of just 3 years. For example, a $19 million grant stock grant to the CEO of MSCI in 2016 had a 3-year term with absolute and relative total shareholder return targets.

Performance triggers. Mega grants also have surprisingly few performance-vesting conditions. 25 percent of grants have no performance conditions (i.e., they have pure time-based vesting), 44 percent have one performance trigger, 19 percent two triggers, and 12 percent have more than two triggers. For example, Alphabet granted its CEO two mega grants during the measurement period—valued at $198.7 million and $276.6 million—consisting of simple 4-year time- vested stock. By contrast, Oracle granted its chairman two mega grants—valued at $103.7 million and $129.3 million—but these consisted of 5-year performance-vested options with six performance metrics (based on stock price, market capitalization, revenue, gross margins, divisional performance, and other non-financial metrics).

Performance triggers are predominantly based on stock price. 35 percent of mega grants have one or more stock-price hurdles, and 23 percent have stock-price hurdles in combination with other hurdles. The following are examples of stock-price targets:

- Microsemi (2016). 25 percent of shares vest if stock price exceeds $50 for 20 consecutive trading days, 50 percent of shares vest above $60, and 25 percent above $70. These amounts represent 38 percent, 65 percent, and 95 percent increases over the grant date price of $36.30.

- Sweetgreen (2021). 7 tranches of shares, vesting one year after the IPO date at stock prices of $30, $37.50, $45, $52.50, $60, $67.50, and $75. The award was granted prior to IPO, with an expected IPO price range of $23 to $25.

- Regeneron (2020). Performance share units with absolute and relative total shareholder return (TSR) targets. Shares are awarded based on 9 TSR targets ranging from a minimum 50 percent payout for a 5-year cumulative return of 31.3 percent to a maximum 250 percent payout for a 5-year TSR of 140 percent. If the minimum threshold is not achieved, the CEO can earn the minimum payout if the company’s stock price return exceeds the return of the Nasdaq Biotech Index by at least 200 basis points. The relative TSR goal is intended to protect the CEO “in the case of a recession or industry-wide developments outside management’s control.”

Only 17 percent of grants in our sample have financial and operational triggers not based on stock-price performance. For example, in 2020 the CEO of Freshpet received a $19.9 million stock-option grant with 4-year performance vesting based on revenue and EBITDA goals. The company did not disclose the specific goals “for competitive purposes,” stating instead that “they will be disclosed upon the conclusion of the four-year performance period.” In 2021, the CEO of Stereotaxis received a 10-year stock award that would vest only if the company’s market capitalization increased to $1 billion, and continued to increase “in additional $500 million increments up to $5.5 billion” subject to minimum-trading day thresholds.

Sharing the wealth. In most cases (60 percent), a mega grant is given to only one recipient. In 40 percent of cases (21 grants), mega grants are also issued to other named officers along with the CEO. When grants are given to multiple officers, they are given on average to two other named executives. (It might be the case that executives other than named executive officers also receive special grants; if so, this information is not public.)

The median (average) size of these additional mega grants is $20.4 million ($52.7 million) in our sample. The size of the median CEO grant is approximately 1.5 times larger (2.4 on average) than that of the number two recipient.

Reason. Companies provide relatively nondescript explanations of why they issue mega grants. Most often, the grant is intended to provide “incentive” for performance, to encourage “superior” performance, to encourage “long-term” performance, and to better align pay with shareholder objectives (i.e., share price appreciation). In some cases, the grant is intended to encourage growth post-IPO, after a merger, or following a strategic review. Other companies disclose that the grant is part of an employment agreement (new or renewed) or for retention. A few companies award large grants every few years, in lieu of annual grants. Examples of these include Kinder Morgan, NVR, and Oracle.

Generally, the justification for mega grants is not significantly different from the language used by a typical company to describe its annual compensation program and does not seem to meet proxy advisory requirements for a “cogent and convincing explanation of their necessity.”

Equity awards following mega grants. Mega grants are often granted in lieu of annual awards, and indeed proxy advisory firms tend to recommend against companies that do not make a firm commitment to abstain from offering additional awards while the term of the mega grant is outstanding. Still, we find that approximately a quarter (23 percent) of companies that issue a mega grant continue to offer annual equity awards to their CEO.

Compensation consultant. A broad mix of compensation consultants recommend mega grants. In our sample, we find 15 different compensation consultants named. The three most frequently named are Compensia (28 percent), Semler Brossy (19 percent), and Frederic W. Cook (13 percent).

Of note, Compensia advised on 59 percent of mega grants valued over $100 million in our sample. This might be because Compensia has large market share among technology startups where large equity grants are often issued. Or it might be related to the fact that Compensia was the consultant that advised on Tesla’s 2018 mega grant and companies looking to replicate Tesla’s program contracted with Compensia.

Stock price reaction. Finally, we studied the stock-price reaction to the issuance of a mega grant, using the date the grant was disclosed on Form 4 as the announcement date. We find shareholders have a small positive reaction to mega grants on the announcement date, with median (average) market-adjusted returns of 0.12 percent (0.39 percent). (Market-adjusted returns are calculated as the change in stock price minus the change in price of the market over the measurement period.) This is inconsistent with investors being concerned about dilution of their ownership position or with the mega grant being a manifestation of a board of directors that is overly influenced by senior management.

Positive returns tend to precede the announcement, with median (average) three day returns up to and including the announcement date of 0.33 percent (3.09 percent). Returns are negative when measured as the three days following the announcement, -0.58 percent (-0.50 percent). Over an extended period of time, the impact on shareholders is approximately zero, even when the mega grant has an expected value of approximately 1 percent of the company.

Why This Matters

- The annual compensation paid to the CEOs of the largest publicly traded companies in the United States is controversial, with shareholder groups, proxy advisory firms, and other experts criticizing executives for receiving multi-million dollar pay packages. And yet recent years have seen an increase in the number of companies awarding “mega grants” to their CEOs that are many times larger than annual pay levels. Why would a board draw attention (and controversy) to itself by awarding a grant that puts the CEO at the top of the list of most highly paid CEOs—particularly when the CEO’s pay might otherwise go unrecognized if annual awards were granted instead? Why subject the company to the difficulty of garnering a positive say-on-pay recommendation from proxy advisory firms or risk low say-on-pay support from shareholders?

- Companies offer annual equity compensation because of the incentive value it offers for executives to pursue operating, financial, and shareholder-value objectives. Annual awards also give the board flexibility to adjust equity compensation in response to executive performance and company prospects. What added incentive does a CEO receive from a one-time, large award instead of multiple annual awards over time?

- Stock price returns on the day the company announces a mega grant are modestly positive. Over longer trading windows they are closer to zero. Does this suggest that large equity grants—despite their size and dilution—have negligible impact on CEO incentives and company performance?

- Bloomberg describes CEOs who receive mega grants as “Elon Musk copy-cats.” How many instances of CEO’s receiving mega grants are driven by copy-cat behavior instigated by the CEO? Should shareholders be concerned that conversations between a board and CEO regarding a mega grant might be initiated by this type of behavior? Who actually initiates a discussion about a potential mega grant: the CEO or the board? What does this suggest about the power of the CEO relative to the board when it comes to setting compensation?

- Many mega grants include performance-vesting features. What are the implications for the firm and its shareholders if targets are missed? If a large incentive is required to encourage long-term growth, what motivation will a CEO have if he or she perceives no chance of achieving the target? Does this encourage excessive risk taking that is potentially harmful to shareholders? Does this put pressure on the board to grant additional equity awards to refresh the incentives?

Exhibit 1: CEO Mega Grants, Descriptive Statistics

Source: Sample of 52 mega grants issued between 2016 and 2022. Research by the authors.