Print

PrintFrederik Otto is Executive Director, Jeannette Lichner is Senior Advisor, and Adélaïde Levassor is Advisor of The Sustainability Board (TSB). This post is based on the 2023 Annual ESG Preparedness Report by Mr. Otto, Ms. Lichner, Ms. Levassor, and Vicky Moffatt. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance (discussed on the Forum here) by Lucian Bebchuk and Roberto Tallarita; Does Enlightened Shareholder Value add Value (discussed on the Forum here) by Lucian Bebchuk, Kobi Kastiel, and Roberto Tallarita; How Twitter Pushed Stakeholders Under The Bus (discussed on the Forum here) by Lucian A. Bebchuk, Kobi Kastiel, and Anna Toniolo; and Restoration: The Role Stakeholder Governance Must Play in Recreating a Fair and Sustainable American Economy – A Reply to Professor Rock (discussed on the Forum here) by Leo E. Strine, Jr.

1. Sustainability Governance is increasing ‘On Paper’

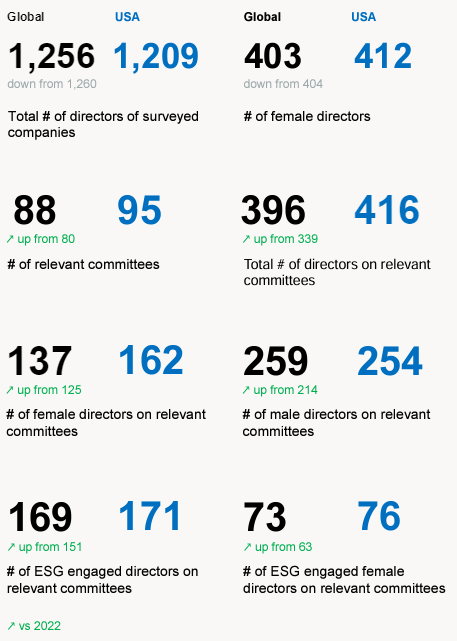

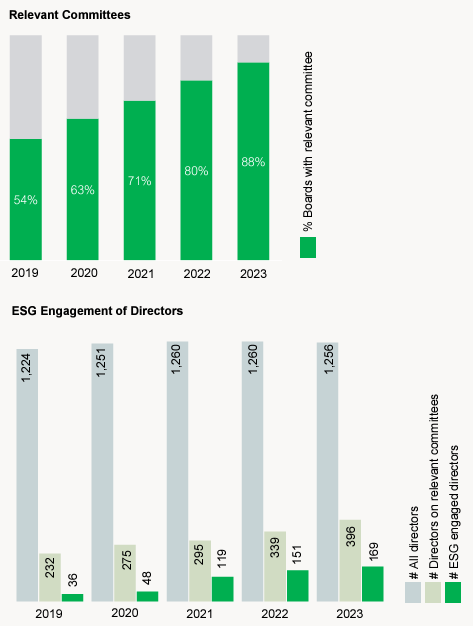

In 2019, just over half of the businesses had a board policy for ESG oversight. This number increased to 88% globally in 2023, and almost all US companies onboard except for five.

ESG oversight is primarily measured by the presence of a board committee that addresses environmental, social, and governance (ESG) issues in its charter. We also source some of this information from proxy reports, corporate governance guidelines, and annual reports. It is important to note that we often see dramatic differences in disclosure between these documents. That means that a somewhat comprehensive approach to governance stipulated in the sustainability report might not translate into the relevant committee charter, or other documents or vice versa.![]()

Further, we see a trend toward more participation of the whole board in relevant committees. Statistically almost every 3rd director is specifically part of sustainability oversight, up from slightly above every 4th in 2022.

2. ESG Engagement of Directors stagnates

Another crucial metric is the ESG engagement of directors responsible for oversight. These directors either have memberships in relevant committees and display sustainability knowledge (ESG consciousness) or have the capability for effective action (ESG competence). From 2019 to 2022, ESG engagement levels of directors rose dramatically from 16% to 45%. Yet, our current data shows a global decline to 43%, with the US at 41%. This suggests a possible stagnation, and future studies will determine if we are approaching a concerning ‘engagement ceiling’ where fewer than half of directors engage in sustainability governance.

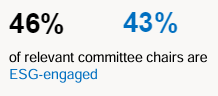

Additionally, this year we have assessed the ESG engagement of committee chairs for the first time. The findings indicate that their engagement levels are akin to the rest of the directors on relevant committees. Globally, 46% of committee chairs are ESG engaged, compared to 43% in the US. It’s worth noting that one might expect directors chairing the committees responsible for ESG oversight to be particularly engaged.

3. Women remain at the Forefront of Sustainability Governance

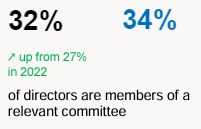

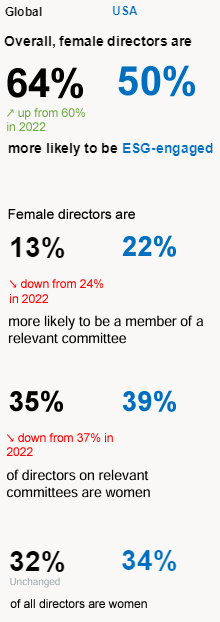

Our third major data point focuses on female board directors and their role in driving ESG engagement. While the difference is decreasing, with women now 13% more likely than last year’s 24% to be part of a relevant committee, they are still 64% more likely to be ESG engaged than their male counterparts. This is a slight increase from 60% the previous year. In the US, the engagement level for women is 50%.

Women constitute 35% of all directors on pertinent committees globally and 39% in the US. These percentages are marginally above the global gender diversity average on boards, which is 32% globally and 34% for the US.

4. Sustainable Management experience remains the main driver for ESG engagement

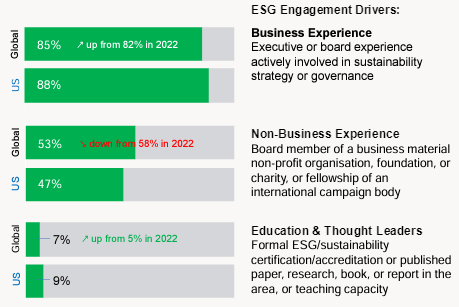

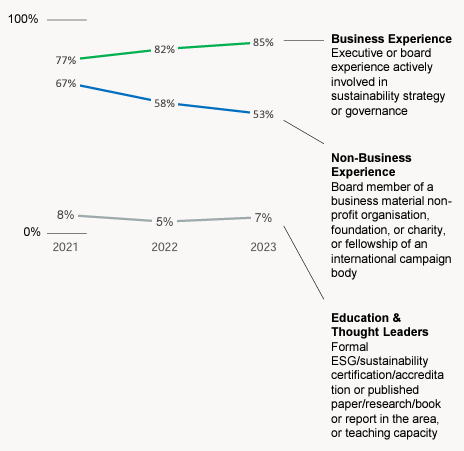

The engagement of directors with ESG criteria is evaluated using a checklist, which assesses them based on three distinct criteria (see page 26). A director is considered ESG-engaged if they meet at least one of these criteria.

85% of directors worldwide and 88% in the US qualify as ESG-engaged due to their corporate experience in sustainability strategy. This engagement largely stems from their roles as either a current or retired CEO.

We also look at whether the director is a member of a relevant non-profit organisation dedicated to industry specific sustainability issues.

The share of directors who satisfy this criterion has declined from 58% in 2022 to 53% in 2023 and is at 47% in the US.

The criterion with the least representation is formal certifications or credentials, with only 7% of directors meeting it. Not much progress has been made over the last 3 years in this area (also see page 20). Within this category, we also include lecturers, professors, and other faculty members who teach sustainability topics. Interestingly, these educators outnumber the individuals who possess formal certifications or credentials in the field.

5. Most Boards, and notably US Boards, are embracing ESG in their Committee Charters

We assess the presence of board ESG policy through the presence of a relevant board committee that stipulates ESG issues in its committee charter, proxy, corporate governance, or annual report.

So long as sustainability oversight is clearly stipulated in their policies these are referred to as ’relevant committees’.

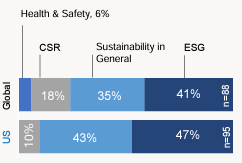

We then screen the policy (mostly committee charters) for narrative. There are four options: Health & Safety: Primarily focused on technical labour safety. CSR (Corporate Social Responsibility): Mainly focuses on employee well-being in a corporate setting. Sustainability in General: Does not exclusively detail ESG factors. ESG (Environmental, Social, Governance): Abbreviated or fully spelled out.

Narrative of Relevant Committee’s Charter

There is a rise in stipulating ESG specifically in committee charters increasing from 34% to 41% globally. Interestingly, almost half of all US boards in our sample have an ESG narrative in their relevant committee charters, despite the current political pushback on the practice.

Committees tasked with Sustainability Oversight

In the US, 51% of committees were specifically dedicated to sustainability oversight in 2023. Globally, the figure is higher at 63%, but lower compared to 2022 at 69%. Shared committees are represented by 36% in 2023 globally compared to 29% in 2022. In contrast, in the US, these committees accounted for a significantly higher 48%.

Recommendations

Our 3-Step Recommendations

The implementation of a solid sustainability strategy, informed by the principles of ESG (environmental, social and governance) is a leading concern with most boards.

Boards need to be able to identify, assess and monitor all that the strategy will impact, considering a short-and long-term perspective.

We recommend the following approach to structure an informed and cogent approach to sustainability governance:

Step 1: Identify

It is important to understand what the material sustainability issues are and who is tasked with oversight.

As mentioned in the foreword, in addition to climate and social issues, we have seen concerns emerge about Human Rights, AI & Emerging Technology, Nature & Biodiversity, and Geopolitics and Conflict and we expect this trend to endure and evolve with constantly changing macro factors.

The next step is identifying the knowledge level of the ESG engaged directors, and the entire board including its chair.

Although we have found women are driving the sustainability agenda, they are still underrepresented on most boards, typically by over 50%.

Therefore, by increasing female representation on the board and within leadership teams, businesses can naturally enhance their commitment to sustainability.

After identifying key sustainability concerns and accountability, the board’s next step is to assess the potential impacts of these issues, both from a short-and long-term perspective.

Step 2: Assess

Board directors should acquire a deeper understanding of sustainability related issues and technological innovations, and thus increase their ESG engagement. This is particularly urgent for committee chairs. Directors may need to upskill and keep abreast of new developments in a wide area of issues affecting sustainable business. That is the common environmental & social concerns as well as emerging topics as mentioned above.

Scenario planning is a useful exercise to imagine plausible futures within these areas.

Step 3: Monitor

Boards might want to seek a ‘reality check’ by identifying the business’ position in key areas previously identified and assessed.

These include material sustainability issues and assurance of the governance structure’s soundness.

It is advisable to mandate an independent third party to provide an assessment of the current oversight processes and overall ESG preparedness.

This snapshot could be used as a starting point to build the implementation plan and its monitoring framework.

Tactics

KPIs

To monitor the implementation or operationalisation of a business’ sustainability commitments, boards should employ quantitative and qualitative key performance indicators (KPIs). These can be designed to help identify any gaps or discrepancies in the business’ efforts to implement the board’s strategy. Qualitative KPIs should, further, be designed to capture the necessary evolution of the organisation’s culture, as this will underpin all transformation.

Frequency of monitoring

Boards might want to closely and more frequently monitor the strategy and its implementation. This will detect hurdles and hidden obstacles in the organisation’s actions early on, such as red flags in client engagement, or dubious products.

Most boards still only meet four times a year. Considering the urgency and impact of the sustainability challenge— meeting frequency might need to be increased.

It might also be necessary to give directors access to ‘aides’ sitting in different divisions of the business, and to external educational and other resources.

Extended Data & Historical Comparison

2023 Total Sample Drill-Down

2023 Global Historic Comparison

Global ESG Engagement Drivers 2021-2023

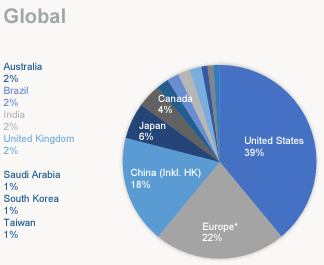

Geographical Scope 2023