Print

PrintMerel Spierings is Senior Researcher for the ESG Center at The Conference Board. This post is based on an upcoming Conference Board report, which was developed using data from ESG analytics firm ESGAUGE and produced in collaboration with Russell Reynolds Associates and Rutgers Center for Corporate Law and Governance.

Companies and major institutional investors are interested in finding common ground with each other as they deal with a random assortment of shareholder proposals this year amid ardent pro- and anti-ESG pressures. This article touches on the key developments we should be watching heading into the new proxy season.

With shareholder proposals becoming more prescriptive and costly to implement, investors are willing listen to companies’ explanations of the cost-benefit analysis of proposals.

Last year’s record number of shareholder proposals led to “proposal fatigue” among major institutional investors and corporations alike – and proposals’ deteriorating quality led to declining support. Rather than being discouraged after two years of declining average support, however, shareholders submitting proposals are responding by adjusting their proposals (e.g., trying somewhat different angles to an issue they raised before) or adopting new issues (e.g., by piggybacking on a more successful proposal submitted by someone else in a previous year). As a result, along with topics such as Artificial Intelligence, the 2024 proxy season is seeing a proliferation of new types of shareholder proposals, including on the clean energy (“green versus brown”) financing ratio at financial institutions; treating shareholder nominees for the board on par with company nominees; imposing new resignation obligations on directors failing to obtain a majority vote for two years in a row.

Nonetheless, support levels, especially for E&S proposals, may yet again decline in the 2024 proxy season. Thus far in 2024, proposals have garnered 15% average support, compared to 23% during the same timeframe last year. To help investors, who are under enormous pro-ESG pressure from some upstream clients, justify their position when they vote against a proposal, companies can provide specific information in the proxy statement on the costs, unintended consequences, and limited benefits of implementing the proposal.

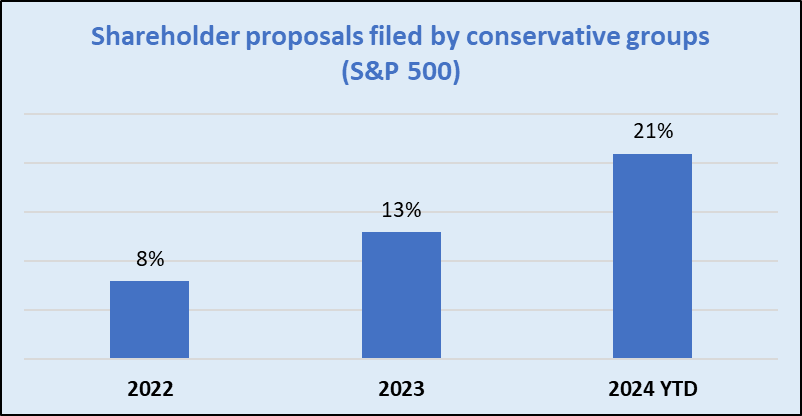

Groups on both ends on the political spectrum are ramping up their proposal activity to generate attention amid the federal election year.

For example, in the S&P 500, 21% of shareholder proposals that have appeared thus far in 2024 proxy statements have been filed by self-described conservative groups, compared to 13% in all of 2023 and 8% in 2022.

In this highly polarized environment, it’s imperative for company executives to:

- have a clear and consistent message in all of their communications and shareholders engagements;

- link the company’s positions to shareholder value; and

- ensure they follow through on commitments.

Source: ESGAUGE / The Conference Board, 2024.

Source: ESGAUGE / The Conference Board, 2024.

The nominating/governance chair position is increasingly becoming a target for investor concerns with companies’ board composition and governance practices.

In 2023, average support for nom/gov committee chairs in the Russell 3000 fell below 90%, often because of a lack of board diversity, overboarding, bylaw amendments, and exculpation provisions.

Source: ESGAUGE / The Conference Board, 2024.

Source: ESGAUGE / The Conference Board, 2024.

While support for compensation committee chairs held steady at 92% last year, this may fall in 2024, as some investors add to negative votes on say-on-pay proposals with votes against compensation committee chairs and members. For example, the chart below shows that average support for compensation committee chairs at companies that failed their say-on-pay vote (<50%) is significantly lower than average support for compensation committee chairs at companies receiving 70% or more for their say-on-pay. In fact, some compensation committee chairs at companies with low support for say-on-pay were barely re-elected in 2023, including at CME Group, Expedia Group, and Broadcom.

Source: ESGAUGE / The Conference Board, 2024.

Source: ESGAUGE / The Conference Board, 2024.

Say-on-pay may be of waning usefulness – especially as an annual exercise.

Average support for company say-on-pay proposals rose from 89% in 2022 to 90% in 2023. At the same time, more voted ended up in the 70-90% average support range. Early 2024 results indicate a strong opening of the year for say-on-pay, with average support of 93% and none of the votes dropping below the 70% threshold. According to some investors, however, say-on-pay may have outlived its usefulness, especially as an annual exercise, for several reasons:

- Treated as another routine vote, it’s not encouraging compensation committees to have more periodic and meaningful discussions of what’s working and what isn’t working.

- Some companies are seemingly indifferent about negative say-on-pay votes.

Bringing in directors on engagement calls can backfire if there isn’t a substantial reason for their involvement.

According to major institutional investors, the quality and effectiveness of engagements with corporations have improved over time. But there are some things companies can to enhance them: (i) have a clear purpose and agenda when engaging with investors, especially when corporate directors are involved, (ii) avoid “ESG pandering” (that is, showing how you are addressing all the investor’s ESG criteria – the investors already likely know how the company measures up and they are more interested in hearing in the company’s own words how ESG fits into the company’s strategy), and (iii) recognize that investors do not expect directors to be experts on every issue, but they (and not management) should address questions that are especially under the board’s purview (e.g., CEO succession or compensation).

Companies should consider scaling back disclosures in their proxy statement to improve readability.

Over the past several years, companies have shifted from viewing the proxy statement as a “compliance” filing that satisfies SEC regulations to a one-stop “communications” document for investors. But this can overload the proxy statement. Companies can consider – and investors would likely welcome – shifting detailed discussions on topics such as cybersecurity from the proxy statement to the Form 10-K.

Pass-through voting should not change the way companies engage with large asset managers – at least not yet.

So far, major institutional investors haven’t seen a significant adoption of pass-through (or client-directed) voting, which involves the opportunity for certain upstream clients – including retail investors – to direct or otherwise participate in proxy voting decisions by instructing the asset manager how to vote their shares on specific issues. Major asset managers therefore advise companies to continue to approach shareholder engagement as they have in recent years; that is, by focusing on discussions with major asset managers.

Having said that, both companies and investors should remain alert to the concern that providing upstream investors with voting policies provided by proxy advisory firms could increase the influence of those firms. Furthermore, pass-through voting could also create a need for – yet not provide a vehicle for – direct engagement between companies and upstream clients with specific goals.

While neither asset managers nor companies identified significant adjustments they need to take right now in light of pass-through voting, they need to remain attuned to the potential risks, and companies may need to adjust their communication and engagement strategies in the future if pass-through voting gains more traction.

About This Post

In January 2024, The Conference Board ESG Center held Chatham House Rule sessions with executives from the investor community representing over 15 trillion dollars in assets under management (January 18) and chief legal officers and corporate secretaries at leading companies (January 22) to discuss what the shareholder voting trends from the 2023 proxy season, as well as other recent developments, portend for the 2024 proxy season. This post provides insights into the 2024 proxy season based on those sessions, as well as a recent webcast hosted in collaboration with Cleary Gottlieb Steen & Hamilton, and a review of 2022 and 2023 management and shareholder proposals at Russell 3000 companies conducted by The Conference Board and ESG data analytics firm ESGAUGE.