Print

PrintLinda Pappas is Principal, Christine Skizas is a Managing Partner, and Olivia Wakefield is a Partner at Pay Governance LLC. This post is based on their Pay Governance memorandum. Related research from the Program on Corporate Governance includes The Perils and Questionable Promise of ESG-Based Compensation (discussed on the Forum here) by Lucian A. Bebchuk and Roberto Tallarita and Paying for Long-Term Performance (discussed on the Forum here) by Lucian A. Bebchuk and Jesse M. Fried.

Executive Summary

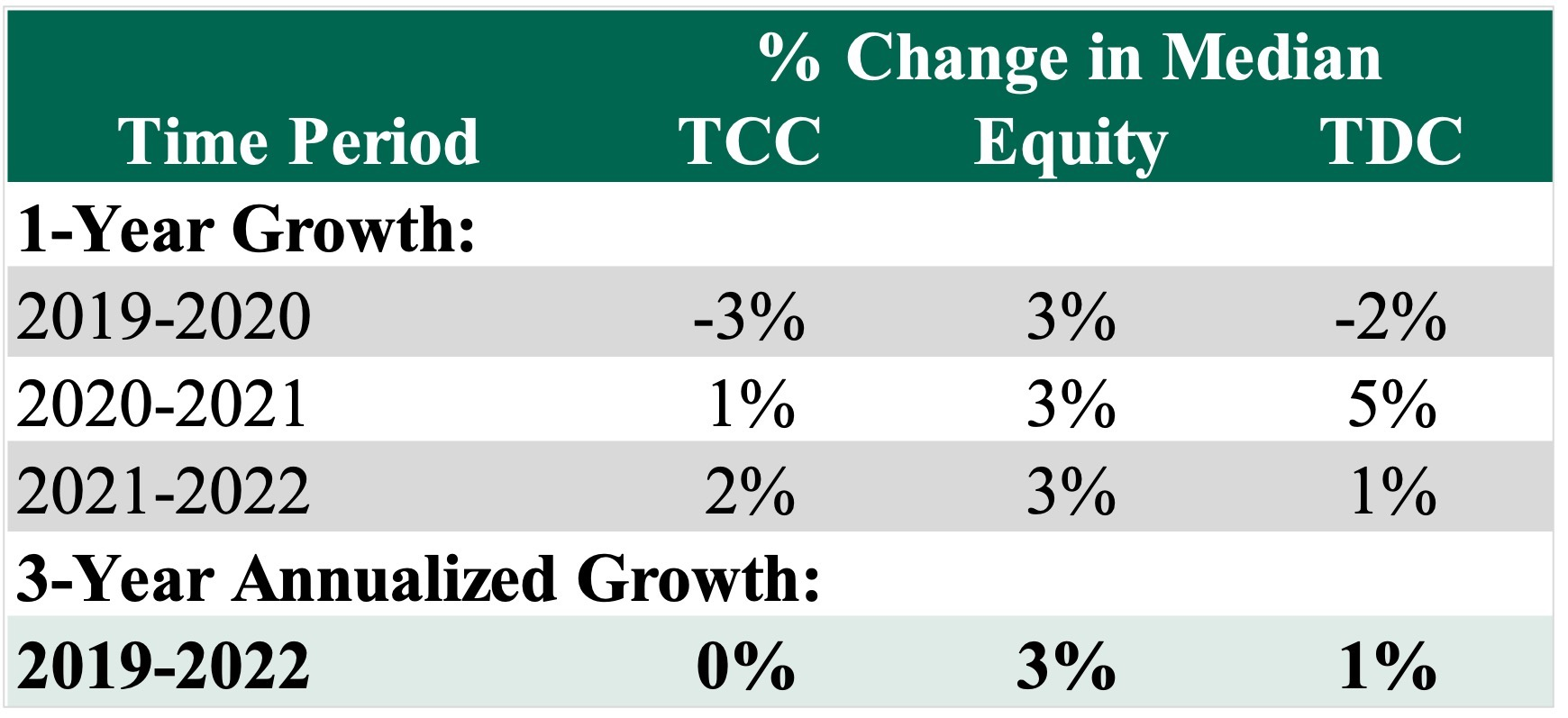

- Over the last three years, median S&P 500 pay level increases for non-employee directors of the board (“directors”) have been minimal compared to prior years, with total cash compensation (TCC or cash retainers plus meeting fees) remaining flat, annual equity retainers up by +3%, and total direct compensation (TDC or sum of cash plus equity) up by +1%.

- When observed over the longer term, S&P 500 director TDC has increased +2% on an annualized basis since 2015.

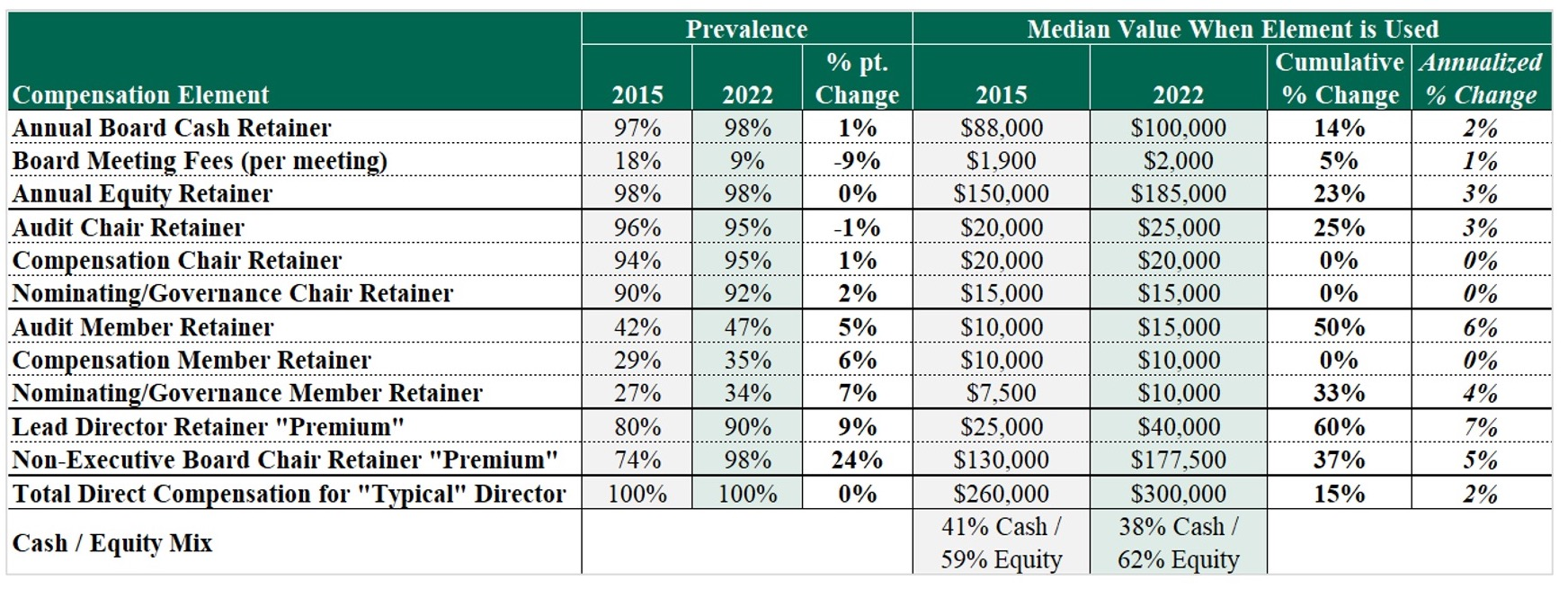

- Structural director pay trends observed since 2015 include the decrease of meeting fee prevalence: used by 18% of the S&P 500 in 2015 compared to 9% as reported in proxy filings to date.

- Premiums for both Non-Executive Board Chair roles and Lead Director roles have also increased in prevalence and quantum since 2015, potentially indicating an increased emphasis of these roles on corporate governance matters.

- Of S&P 500 companies, 70% have established director pay limits with a median value of $750,000.

Introduction

Board of Director remit has expanded over recent years as outlined below. This has resulted in greater accountability and oversight for emerging areas of investor attention in addition to the corporate governance and fiduciary responsibilities to shareholders, community stakeholders, employees, and other key constituents, including:

- ESG issues

- Diversity, equity, belonging, and inclusion with requirements to analyze and report gender pay parity and pay transparency in select geographies

- Human capital, succession planning, and talent management

- Cyber security, digital, and privacy issues relating to artificial intelligence and machine learning

While the responsibilities of the Board continue to evolve and expand, director compensation increases have remained generally modest with a +1% annualized increase since 2020. Pay Governance reviewed non-employee director compensation levels for S&P 500 companies over the last three years using information within the most recent proxy disclosures.[1] Our observations generally reflect compensation for fiscal years 2020, 2021, and 2022. In addition, we compared 2022 director pay information to findings from 2015 from our previously published Viewpoint titled “Board of Directors Compensation: Past, Present and Future” in an effort to identify long-term trends in both director pay levels and design.[2]

Key Findings & Trends

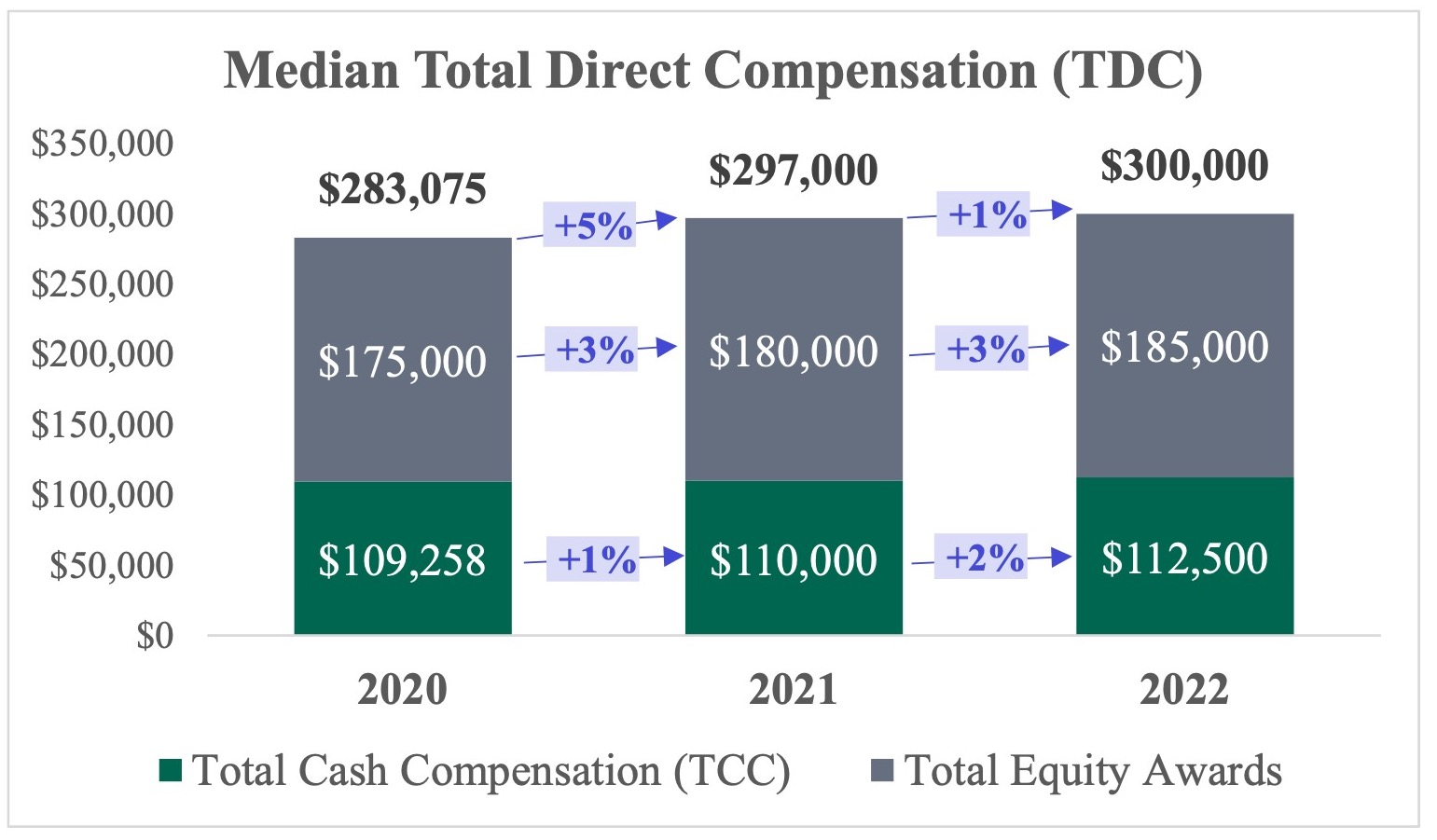

Over the last three years, median S&P 500 director pay levels have increased at a modest pace. Total cash compensation (TCC)—or the sum of Board and Committee member retainers and Board and Committee meeting fees—was flat, while annual equity retainers increased by +3% each year. Total direct compensation (TDC)—or the sum of total cash and equity retainers—increased by +1% on an annualized basis. When analyzing year-to-year trends, we observed a dip of -2% in median TDC in 2020 (as disclosed in proxy statements filed in 2021), followed by a rebound of +5% in 2021 median TDC and then a modest increase of +1% in 2022 median TDC. This likely reflects the impact of temporary COVID-related pay reductions many Boards elected to take during 2020.

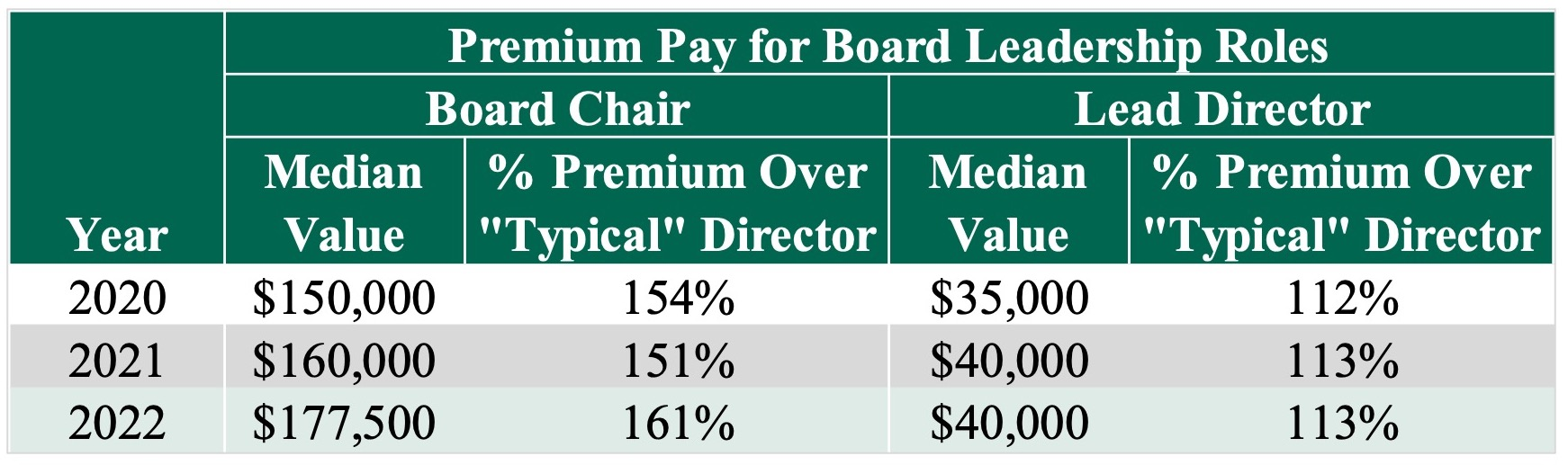

When we take a longer look back at historical director compensation levels, the trend is consistent with our more recent observations. Since 2015, median TDC increased by +2% on an annualized basis. The median value of premium fees for leadership roles, namely Lead Independent Director and Non-Executive Board Chair incremental fees, have increased at a quicker pace than total pay for a “typical” director (i.e., a director who is not in a board or committee leadership role). Lead Director incremental fees increased by +7% on an annualized basis, while Non-Executive Board Chair incremental fees increased by +5% on an annualized basis.

Note: TDC for a “Typical Director” reflects the sum of Board cash retainers, Committee member retainers, Board and Committee meeting fees, and annual equity retainers. Incremental fees for Board and Committee leadership roles are excluded (e.g., Committee Chair Retainers, Lead Director Retainers, Non-Executive Board Chair Retainers).

Note: TDC for a “Typical Director” reflects the sum of Board cash retainers, Committee member retainers, Board and Committee meeting fees, and annual equity retainers. Incremental fees for Board and Committee leadership roles are excluded (e.g., Committee Chair Retainers, Lead Director Retainers, Non-Executive Board Chair Retainers).

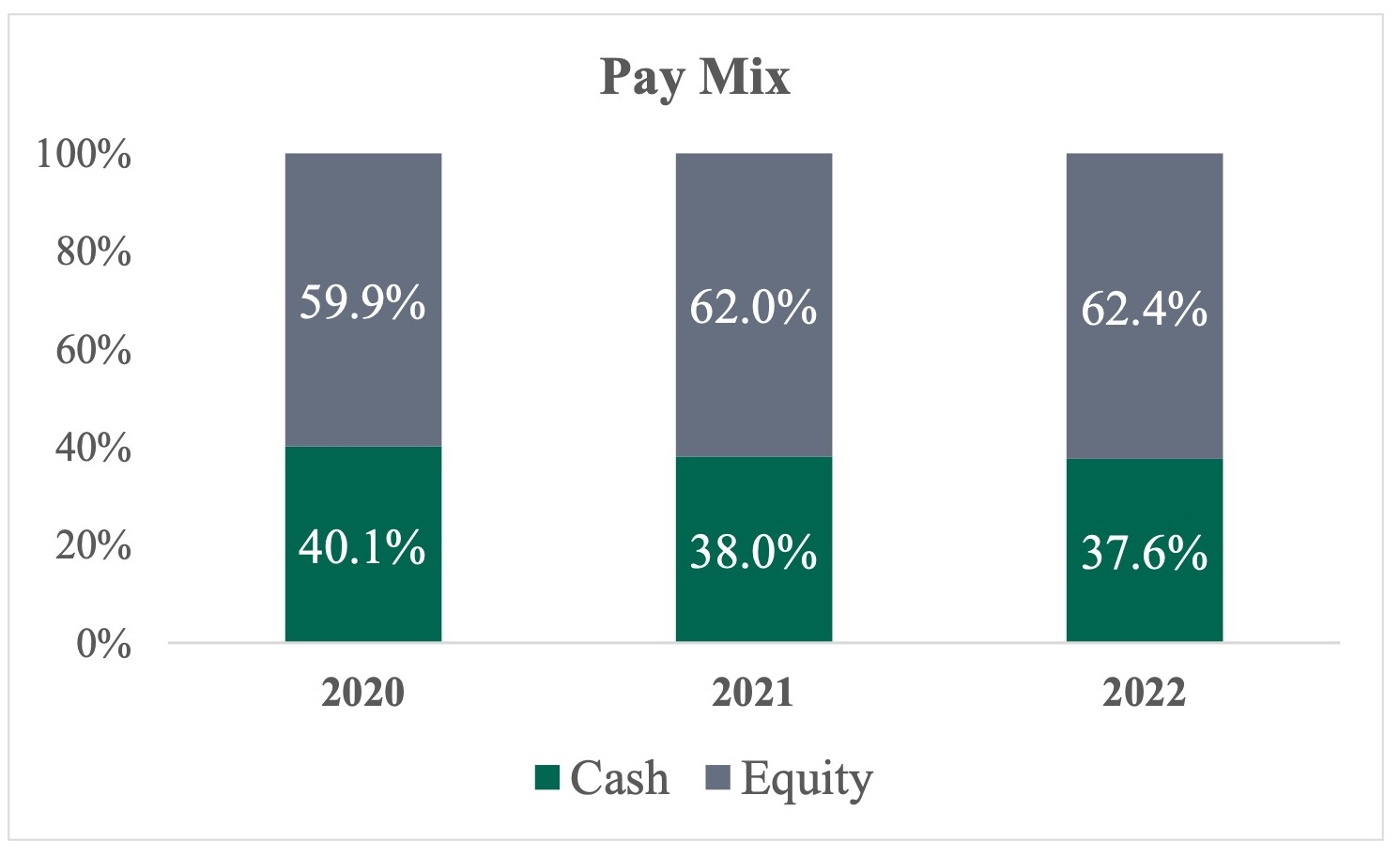

Board Service Pay Mix

The portion of total compensation delivered in cash versus equity, or overall pay mix, has been relatively stable at approximately 40% cash and 60% equity. Over the last two years, we have seen the proportion delivered in equity inch slightly higher (to 62% equity), as meaningful increases in director compensation are more commonly provided through equity than through cash-based compensation.

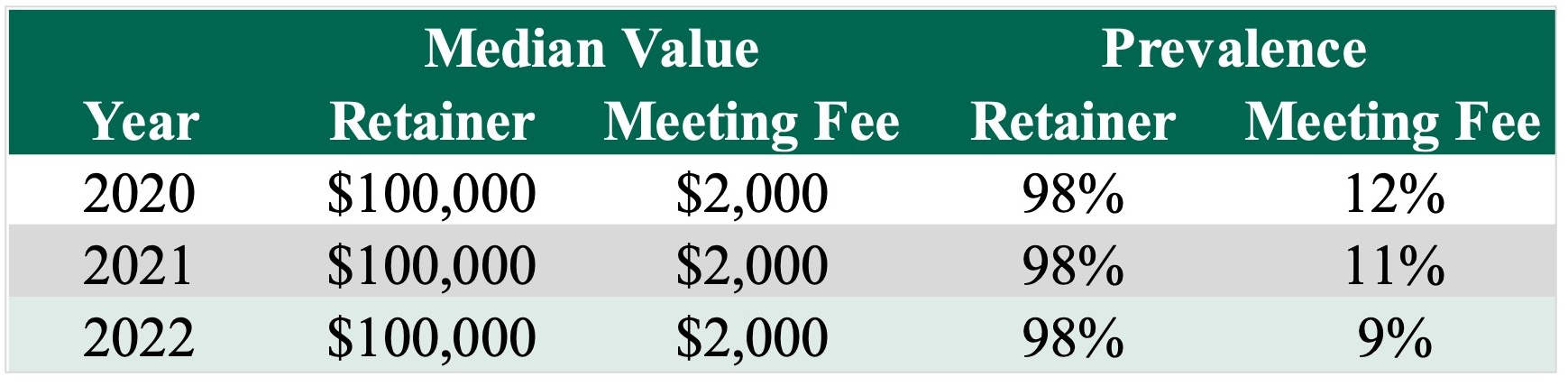

Cash Fees for Board Service

The median value of annual cash retainers for board service has remained constant at $100,000 over the last three years. We continue to observe fewer S&P 500 companies providing meeting fees, with the most recent prevalence at 9% (compared to 12% prevalence in 2020 and 18% prevalence in 2015). However, we note that the decline in the use of meeting fees is somewhat offset by the increase in committee member retainers. Among companies that provide a fee for each board meeting attended, the median value of $2,000 per meeting has remained constant over the last three years.

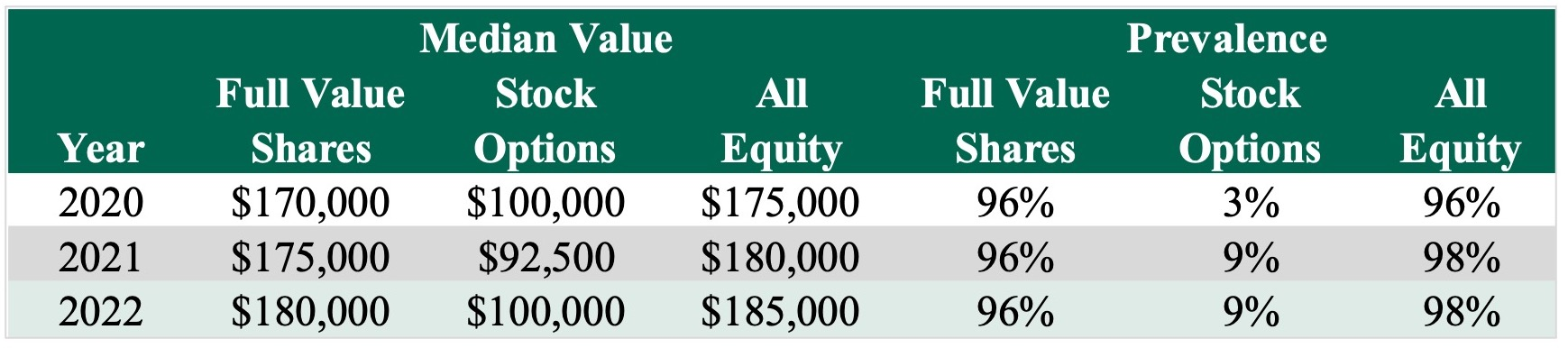

Equity-Based Awards

The median value of total equity awards has steadily increased over the last three years, with the most recent median value equal to $185,000. Although full value shares (e.g., restricted shares/stock units, deferred shares/stock units, common stock) remain nearly universal in prevalence (provided by 96% of S&P 500 companies), the use of stock options has increased slightly since 2020 (provided by 9% of S&P 500 companies in both 2021 and 2022).

TDC for a “Typical” Director

The median sum of all cash-based and equity-based fees to a director who is not in a board or committee leadership role (a “typical” director) was $300,000 for 2022 and reflects a modest increase of +1% compared to 2021 median TDC. This followed a higher increase of +5% between 2020 and 2021. Many companies froze or deferred increases to director compensation levels during the pandemic but resumed increases for 2021 as observed in 2022 proxy filings.

Note: Independently arrayed, will not sum to total

Note: Independently arrayed, will not sum to total

Fees for Committee Service

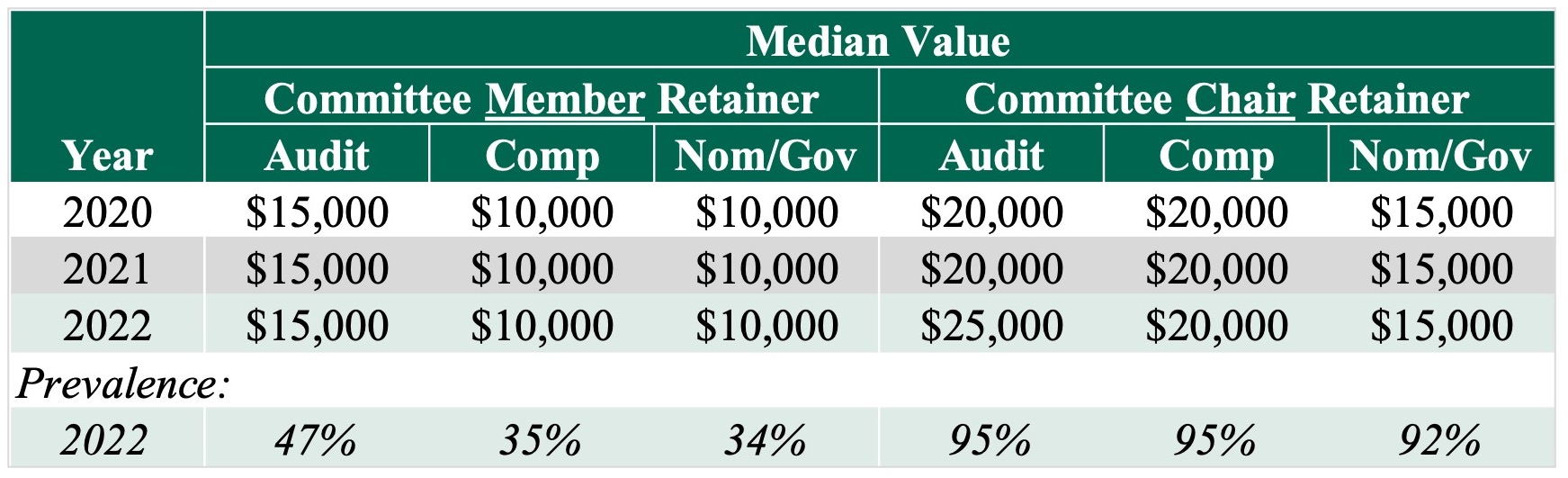

Additional retainers provided to committee members and chairs have remained stable over the last three years. The only increase observed at the median was for Audit Committee Chairs, where the median value increased from $20,000 to $25,000 in 2022. This reflects a differentiation from Compensation Committee Chair retainers where the median value remained at $20,000. The Chair of the Nominating and Governance Committee continues to have a median retainer of $15,000. When additional fees are provided for committee service, members of Audit Committees typically receive a higher retainer (median value of $15,000) than members of other committees (median value of $10,000).

Fees for Board Leadership Roles

In the last three years, we observed a steady increase in premium pay for Non-Executive Board Chairs and a modest increase in premium pay for Lead Independent Directors. The median value of incremental fees for Non-Executive Board Chairs was $177,500 in 2022 and represents 161% of the total pay that is provided to a “typical” director. The median value of incremental fees for Lead Independent Directors was $40,000 in 2022 and represents 113% of the total pay that is provided to a “typical” director.

Director Stock Ownership Guidelines

There has been very little change in S&P 500 stock ownership requirements for directors over the last three years. Prevalence is nearly universal, with guidelines in place at 95% of the S&P 500 companies. The most common stock ownership guideline is 5X the annual board cash retainer with a time requirement of five years.

Director Pay Limits

Approximately 70% of S&P 500 companies have established annual limits on non-employee director compensation, which reflects significant growth in prevalence over the last 10 years. An increase in the number of lawsuits brought against companies asserting that directors were breaching their fiduciary duties and awarding themselves “excessive” compensation, especially in the form of equity compensation, led many companies to establish “meaningful” director pay limits over the past decade. These limits are typically found within new or amended stock plans that are specifically applicable to non-employee directors and are typically substantially lower than the individual limits under stock plans related to all employees. Practice is split between defining annual limits as equity-based awards only or defining limits as a total of all cash and equity-based compensation. Both definitions have a median value of $750,000. A limited number of S&P 500 companies define cash-only annual non-employee director pay limits with a median value of $500,000.

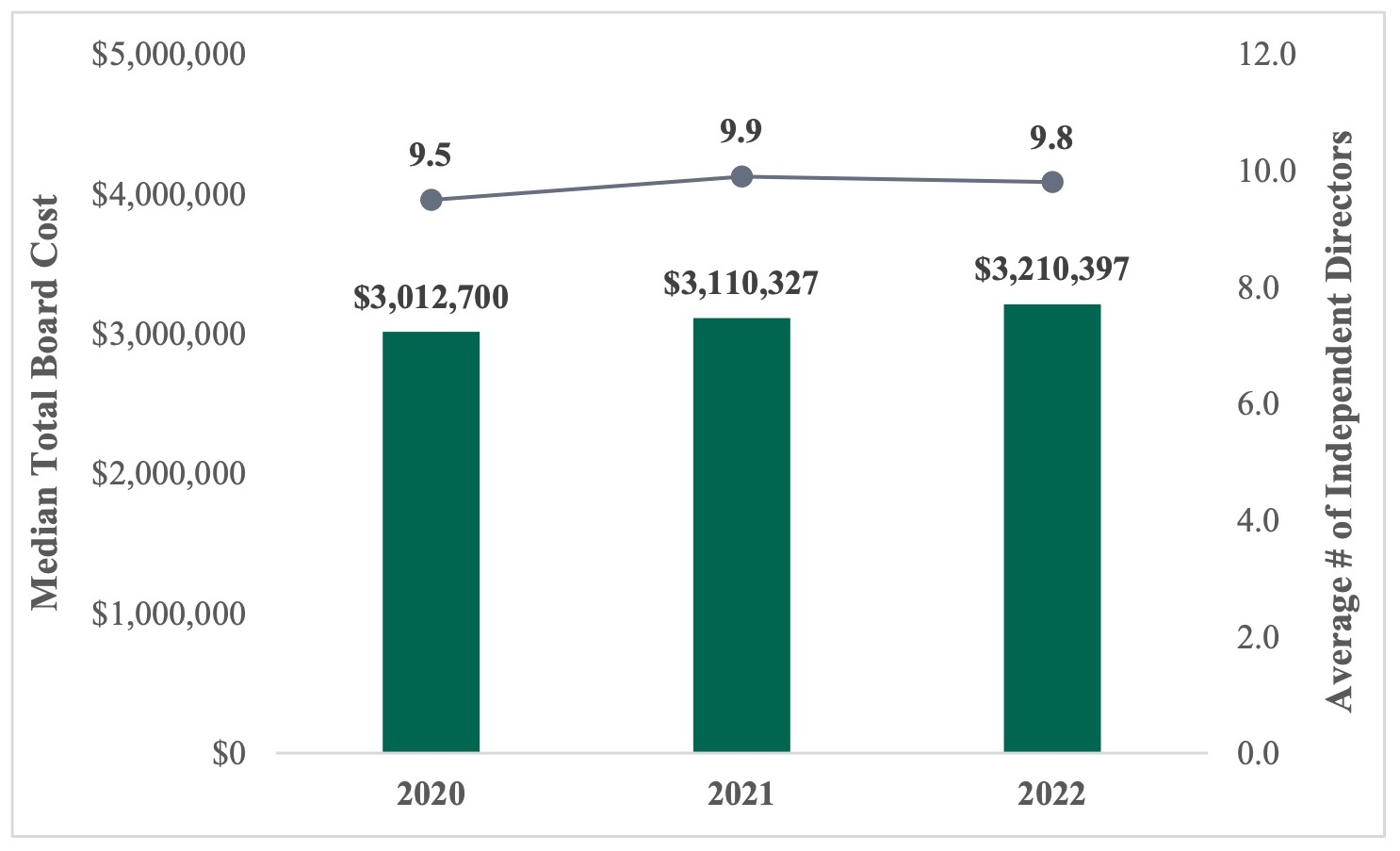

Total Board Cost

The size of S&P 500 boards has remained relatively stable over the last three years, with an average of about 10 independent directors serving on the board. The median total board cost, or the aggregate of all cash and equity-based fees plus “all other compensation” actually paid to all non-employee directors as reported in the proxy statement’s “Director Compensation Table,” increased to about $3.2 million in 2022. This represents an increase of about +3% over the 2021 total board cost and, over the last three years, reflects an annualized increase of +2%.

Conclusion

In recent years, the core profile of an S&P 500 director pay program has remained generally consistent. Although the remit of a director may be expanding, increases in median “typical director” TDC of +1% are modest. The delivery of total pay to directors split as 40% cash and 60% equity has also remained generally constant. Where more movement has been observed is in the continued trend away from meeting fees and increased differentiation in total pay for board leadership roles.

Perhaps it is not surprising that director compensation has increased so modestly. While the role of a director today balances shareholder value creation with increasingly complex stakeholder priorities against a digital backdrop that provides a platform for both greater transparency and potential communication pitfalls, the fundamental purpose of a director is to be an independent, experienced operator who can partner with and, in some cases, coach leadership teams to execute on long-term business strategy while sustaining near-term business performance. For this reason, directors should be compensated fairly for their experience and time dedicated to their Board role without being perceived as being excessively compensated for the role; hence the wider use of Director Pay Limits over the past decade.

Endnotes

1Board of Director compensation data collected from Main Data Group for constituents of the S&P 500 Index.(go back)

2Board of Directors Compensation: Past, Present and Future. Pay Governance. March 2, 2017. https://www.paygovernance.com/viewpoints/board-of-directors-compensation-past-present-and-future.(go back)