Print

PrintJose Furman is a Consultant at FW Cook. This post is based on an FW Cook memorandum by Mr. Furman, Ian Kim, and Michael Kenney.

EXECUTIVE SUMMARY

Our 2024 Annual Incentive Plan Report provides a comprehensive review of the annual incentive plans of the top 250 largest companies in the S&P 500 by market capitalization. Annual incentive plans are critical tools used to align executive compensation with a company’s short-term goals and support talent attraction, motivation and retention objectives. This report examines trends in financial and non-financial metrics, goal-setting practices, and actual payouts, comparing findings over 2-year and 5-year periods, which coincide with our 2022 and 2019 reports. ESG trends are analyzed based on findings from the last 3 years, corresponding with our 2023 and 2022 Use of ESG in Incentive Plans Reports.

Please note that while this report references 2024 as the publication year, it primarily reflects 2023 compensation practices. Similarly, references to 2023, 2022 and 2019 publication years correspond to 2022, 2021 and 2018 compensation practices, respectively.

Plan Design

- Increased Use of Formulaic Plan Design: 93% of the top 250 companies use a formulaic annual incentive plan design with predetermined metrics and weightings, up from 88% in 2022 and 83% in 2019. Formulaic plans are preferred by proxy advisory firms and shareholders as they provide a clear link between pay and performance.

- Multiple Measures are Common: Companies continue to use multiple financial measures in annual incentive plans, with 64% of companies using two or three financial measures in 2024. We observe a growing trend of companies using a scorecard approach of four or more metrics to measure performance. A multiple-metric approach provides a balanced performance assessment and mitigates the risks associated with reliance on a single measure.

- Profitability measures continue to be the most common and have the highest weightings: Companies prioritize profitability measures, which are typically weighted 50%. Profitability is most often paired with a revenue measure. These measures are frequently communicated to investors and are critical indicators of a company’s financial health and growth potential, making them highly relevant for annual incentive plans. The average weightings for all measures have remained relatively stable over a 2- and 5-year period.

- Non-financial measures remain common and critical: The use of non-financial measures continues to be a significant component of annual incentive plans, with 79% of companies incorporating them in 2024, consistent with prior years. While overall weighting remains stable at ~20%, there is a noticeable shift away from individual performance measures toward team-wide strategic initiatives (67% in 2024, up from 42% in 2019).

- Individual performance metrics are most commonly incorporated as modifiers as opposed to standalone weighted measures: The use of individual performance weighted measures decreased from 47% in 2019 to 36% in 2024, while the use of individual performance modifiers increased from 46% in 2022 to 64% in 2024.

- ESG measures remain prevalent, but areas of focus have shifted: 77% of the top 250 companies included ESG measures in some form in their annual incentive plans in 2024, an increase from 73% in the prior year. However, the focus within ESG is shifting, with a decline in the prevalence of Diversity & Inclusion measures (73% in 2024, down from 79% in 2022) and slightly increased emphasis on Environmental & Sustainability (62%) and Human Capital & Culture (63%) metrics. This trend suggests that while companies are maintaining their commitment to ESG, they may be reassessing and adjusting the specific areas of focus.

- Payout ranges remain consistent with prior years, other than a slight uptick in 0% threshold payouts: Maximum payouts ranges remain largely stable, commonly set at 200% of target and used by ~70% of companies in 2024, consistent across the past three studies. However, there is a growing trend in threshold payouts, with 0% threshold payouts steadily increasing since 2019, reaching 37% in 2024. This trend suggests that companies are increasingly building in more downside protection for below-target performance.

Goal-Setting

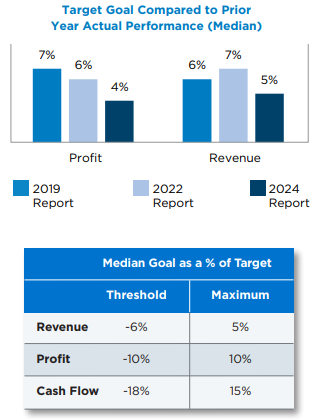

- Most companies set more challenging target goals in 2023 relative to prior year actual results: In 2023, profit targets were set 4% higher than the actual profit performance in 2022, and revenue targets were set 5% higher than the actual performance of 2022. This approach is slightly more conservative compared to the goal setting observed in prior reports, reflecting a more cautious approach amid potential uncertainty. Setting targets above prior year actual performance is becoming a growing area of scrutiny from proxy advisors, who evaluate goal-setting rigor as part of their qualitative review of executive compensation plans.

- Threshold and maximum goal-setting performance ranges remain tied to confidence in forecasting accuracy: Performance ranges around target (threshold to maximum) remained generally consistent in 2024 vs. prior studies. Median performance range for profit metrics was -10% at threshold to +10% at maximum (as a % of target). For revenue, threshold goals were set at -6%, and maximum goals at +5%. For cash flow measures, threshold and maximum were set at -18% and +15%. The width of the performance range is directly tied to the level of confidence management has in the goals they set. Narrower ranges suggest a higher degree of confidence, whereas companies will often widen ranges if they predict more potential volatility in financial performance in the year ahead. Performance ranges should be set with a realistic view of operational performance, ensuring that targets are set at challenging but achievable levels.

Plan Payouts

- A majority of company payouts exceeded target performance in 2023: 2023 was a strong year for the Top 250 companies as they recovered from a volatile 2022 during which median TSR was -7%. In 2023, top-line and bottomline growth were positive, each increasing by 7% year-over-year, and median TSR was +16%. The median CEO annual incentive payout was 127% of target, which aligns with overall company performance. Notably, the median CEO payout exceeded 100% of target across all industry sectors, reflecting that companies generally met or exceeded their performance goals for the year.

Link to full report can be found here.