Print

PrintJason Frankl and Brian G. Kushner are Senior Managing Directors, and Kurt Moeller is a Managing Director at FTI Consulting. This post is based on a FTI Consulting memorandum by Mr. Frankl, Mr. Kushner, Mr. Moeller, Tom Kim, Ryan Chiang, and Middleton Griffin.

Introduction & Market Update

As the year draws to a close, there is a growing sense of optimism for M&A activity in 2025, with an anticipated change in the regulatory environment following the elections – one that market commentators believe will be less restrictive. A friendlier M&A backdrop could underpin a pickup in the number of activist campaigns in 2025. For the nine-months ended September 30, 2024, there have been 40 activist campaigns with explicit demands for M&A, up 17% over the same period in the prior year, suggesting the optimism may begin to materialize. [1] Technology, Media and Telecommunications (“TMT”) and Financials Institutions have been the most actively targeted sectors by activists year-to-date, and we believe that they are likely to remain vulnerable to activists in the coming year.

Notable Campaigns We’ve Tracked

Southwest Airlines

LUV down 2.3% during campaign [2]

Elliott Investment Management (“Elliott”) secured five board seats at Southwest Airlines Co. (“Southwest”) as part of a settlement, after building an 11% stake and calling for substantial changes to the business. [3] Elliott, which had earlier nominated a 10-person slate to overhaul Southwest’s Board, began pushing for Board, leadership and strategy changes in June 2024. [4] In a multi-step process, Southwest agreed that seven directors (out of 14 from the 2024 annual meeting) would depart, including Executive Chairman and former CEO Gary Kelly. [5] Southwest announced plans to introduce assigned seating and premium seating on their aircrafts in 2026, which was among the changes sought by Elliott. [6] Elliott continued to pressure Southwest, including calling for a special meeting before the end of the year. [7] However, the late October settlement led Elliott to express confidence that the changes agreed to by Southwest would boost operational performance, resulting in a withdraw of its special meeting request. [8] Since the settlement, Southwest has appointed Rakesh Gangwal, founder of InterGlobe Aviation Limited, as Chair of the Board. [9]

Pfizer

PFE down 10.7% since start of campaign

Starboard Value LP (“Starboard”) built a $1 billion stake in Pfizer, Inc. (“Pfizer”) to push for strategic changes, as Pfizer struggled with declining demand for its COVID-19 vaccines. Starboard approached former Pfizer executives Ian Read and Frank D’Amelio, who reportedly initially expressed interest in working with Starboard, later withdrew their support, citing alignment with CEO Albert Bourla. [10] Starboard criticized Pfizer for poor shareholder returns and weak innovation since 2019, urging greater R&D profitability and management accountability. [11] In response, Pfizer appointed former Vanguard CEO Tim Buckley to its Board. [12] Pfizer is exploring the sale of its hospital drugs unit to boost returns and address Starboard’s concerns over R&D investment strategies, and appointing former Chief Oncology Officer Chris Boshoff as Chief Scientific Officer to lead R&D efforts, with CEO Albert Bourla praising his proven success in developing impactful medicines. [13], [14]

Masimo

MASI up 23.2% since start of campaign

Politan Capital Management LP (“Politan”) launched a second proxy campaign at Masimo Corporation (“Masimo”), securing two additional Board seats after gaining two Board seats last year. [15] Masimo initially offered one seat to avoid another dispute, but Politan pressed forward, seeking a majority of Masimo’s six directors. [16] As it warned of a potential “mass exodus” of employees, the company postponed its AGM to September; nevertheless, proxy advisors Glass Lewis and Institutional Shareholder Services (“ISS”) supported Politan’s nominees, for which shareholders supported. [17], [18] This resulted in a leadership shake-up, with CEO Joe Kiani resigning, but other top executives staying. Masimo also filed a lawsuit against Kiani, alleging that he colluded with RTW Investments LP to improperly influence voting outcomes – the firm is reportedly now under investigation by the SEC. [19], [20]

Cheesecake Factory

CAKE up 19.3% since start of campaign

JCP Investment Management LLC (“JCP”) built a 2% stake in Cheesecake Factory, Inc. (“Cheesecake Factory”) and is pressuring the restaurant chain to spin off its North Italia, Flower Child and Culinary Dropout brands into a separate, growth-focused company. JCP, which disclosed its initial investment in August, has urged Cheesecake Factory leadership to consider the move and offered capital for the new entity. The activist believes separate management teams would better drive financial performance and has called for a strategic review of other, smaller assets. [21] However, during an October 29 earnings call, Cheesecake Factory rejected JCP’s demands. CFO Matt Clark expressed confidence in the current strategy and emphasized that the company’s scale provides benefits such as lower costs on commodities and insurance.

Squarespace

SQSP up 4.9% during campaign

After agreeing to a sale to private equity firm Permira Advisors LLP (“Permira”) in May, Squarespace, Inc. (“Squarespace”) faced opposition from Glazer Capital LLC (“Glazer”), which argued that the $44 per share deal undervalued the company. Glazer claimed that the sale process omitted key valuation analyses that would have placed the value above $49.30 per share. In response to investor pushback and a recommendation from ISS against the deal, Permira raised its offer to $46.50 per share. The revised agreement also eliminated the ability of shareholders to vote on the deal, as it was structured as a tender offer. The tender offer received support from 97.5% of shares, and it became effective in October.

Activism Update

Overview of 3Q24 Activism Activity and Emerging Trends

Activist investor activity experienced a seasonal dip after a very active first half of 2024. This trend aligns with typical patterns. There were 56 campaigns initiated in 3Q24, closely mirroring previous years’ activity levels for the same period. [22]

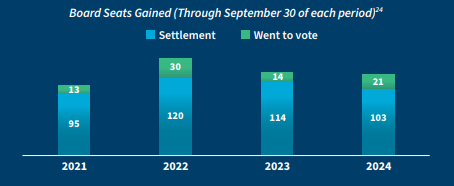

Board seats gained by activists in U.S. companies through September 30, 2024, remained relatively steady compared to the same period in 2023. However, the pathways to these seats shifted, with fewer board seats achieved through settlements and a slight uptick in board seats won through proxy contests. [23]

Activists publicly sought one or more board seats 147 times during the first three quarters of 2024, up from 112 at the same point last year. However, their success rate declined, with only 53% of these demands resulting in board seats, down from 63% in the same period last year. [25] This suggests that while activists’ appetite for board influence has grown, companies are becoming more resistant or discerning in negotiating settlements.

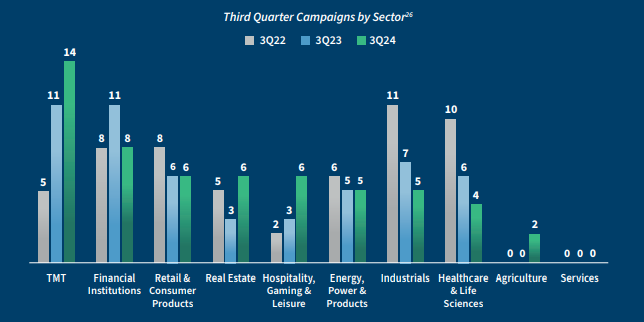

The most frequently targeted sectors this quarter were TMT, with 14 campaigns, followed by Financial Institutions, with eight. These sectors continue to face activist pressure in the fourth quarter, with nine new campaigns in TMT and six in Financial Institutions launched between October 1 and November 1, 2024. [27] This persistent vulnerability reflects ongoing strategic and operational challenges, particularly in TMT, where we see evolving market dynamics, regulatory scrutiny and volatile financial results. Notable recent campaigns in these sectors highlight activists’ focus on areas such as digital transformation, restructuring efforts and cost-reduction initiatives.

— Engine Capital Management LP (“Engine”), a 3.5% investor in Upwork Inc. (“Upwork”), urged Upwork’s Board to improve shareholder value by refreshing certain directors and holding management more accountable. In a September 13 letter, Engine cited issues with strategic focus, execution and capital allocation. It suggested declassifying the Board to allow annual director elections. Engine also recommended that Upwork optimize costs, reduce stock-based compensation dilution and use excess capital for share buybacks. [28] On October 24, Upwork announced a restructuring plan that included a 21% reduction in its workforce, cost optimization and strategy realignment. [29]

— Breach Inlet Capital Management LLC (“Breach Inlet”), a 2% shareholder, argued in a September 4 statement that International Money Express, Inc. (“IMXI”) is undervalued in public markets and could achieve better growth privately. It noted strong profit growth, but a low valuation multiple compared to peers. Breach Inlet suggested that IMXI would attract private equity interest due to its growth potential, low capital needs and underleveraged balance sheet. [30] On September 5, Voss Capital filed a Schedule 13-D indicating that it had urged the Board and management to examine ways to maximize shareholder value, including, but not limited to, a sale of the company. [31] IMXI announced in its November 8 earnings release that it had retained a financial advisor to assess strategic initiatives, which could include a sale. [32]

Performance Challenges in TMT Sector Activismm

Despite the significant attention on the TMT sector, activists have struggled to achieve their objectives in 2024, with only 22% of campaigns in TMT resulting in activist victories, far lower than the 42% success rate in 2023’s TMT campaigns. [33] This decline may stem from the complexities inherent in TMT companies, such as long lead times for R&D, high regulatory oversight and high capital requirements. However, as many campaigns in this sector are still ongoing, these success rates could shift by year-end. [34] If activists focused on TMT companies succeed in their pending campaigns, we may see continued momentum in TMT sector activism moving into 2025, particularly amid ongoing antitrust challenges and other disruption. [35]

Market Segment Shift: Mid-Cap Companies Capture Activist Interest

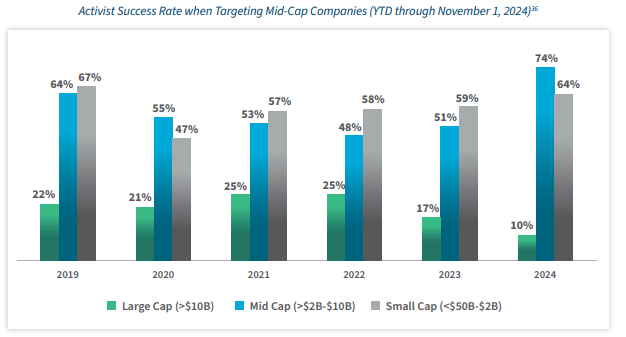

Mid-cap companies, in particular, have seen a surge in activist interest, accounting for 25% of total campaigns in 3Q24, compared to just 10% a year earlier. [37] This shift is not without reason: year-to-date through November 1, activists are achieving higher success rates in the mid-cap segment, with an impressive 74% of concluded mid-cap campaigns delivering favorable outcomes for activists in 2024, up from 51% during the same period last year.

A notable mid-cap campaign initiated in 3Q24 was Starboard’s engagement with Match Group, Inc. (“Match”):

— In July, Starboard announced a 6.6% stake in Match and urged the company to boost profitability, buy back shares or explore a sale. [38] Match was approached separately by both Elliott and Anson Funds Management LP earlier this year and added two directors to its Board following engagement with Elliott. [39], [40] It has faced challenges, including a decline in paying users on key platforms like Tinder. [41]

In response to Starboard, Match announced a 6% workforce reduction and an exit from live-streaming services to streamline operations, moves that are expected to save $13 million in costs but result in a revenue loss of $60 million. [42] Starboard also has pushed for an aggressive share repurchase plan, arguing that Match’s stock is undervalued compared to its peers. [43] In October, Match appointed Steven Bailey as its new CFO, emphasizing a commitment to “driving long-term strategic growth and exercising strong cost discipline.” [44]

M&A Pressure Intensifies as Interest Rate Environment Stabilizes

Continuing a trend highlighted in our previous report, activists are maintaining pressure on companies to consider M&A opportunities. Through 3Q24, there have been 40 campaigns with explicit demands for M&A transactions, compared to 34 during the same period last year. [45] This persistent and increased focus on M&A may reflect activists’ interest in capitalizing on improving conditions in the current economic environment, particularly as interest rates have begun to decline and future rate paths become more predictable. Lower rates can improve access to affordable capital, making acquisitions and other strategic transactions more feasible.

— Continuing the discussion from our previous report, Ancora Advisors LLC (“Ancora”) is urging Forward Air Corporation (“Forward Air”) to explore a sale, arguing that its operational and financial challenges — exacerbated by the debt-heavy Omni Logistics LLC (“Omni”) acquisition — are better addressed in private ownership. [46] Forward Air acknowledged it has undergone a “significant transformation” after the tumultuous Omni deal, which resulted in nearly $1 billion in Q2 net losses, layoffs, and a wave of executive departures, including its CEO, CFO, and Board compensation chair. While the company initiated a portfolio review to identify non-core assets, investors like Ancora and Clearlake Capital Group (“Clearlake”) argue that a sale or other strategic alternatives are necessary to protect shareholder value. [47] Ancora, with a history of Board involvement at Forward Air, joins Clearlake and Irenic Capital Management LP, and recently Alta Fox Capital Management LLC, in pressing for decisive action, though navigating the company’s $1.6 billion debt and securing support from key shareholder Ridgemont Equity Partners, which has two Board seats, remain significant hurdles. [48]

M&A Activity

M&A activity has been softer due to the uncertainty around the magnitude of rate cuts anticipated in 2024 and perceptions of a restrictive regulatory environment. With greater clarity on the direction of interest rates and a recalibration of expectations around the cost of capital, we expect deal flow to pick up over the next 12 months. A potential, if not likely, change in the Federal Trade Commission should also bode well for corporate M&A.

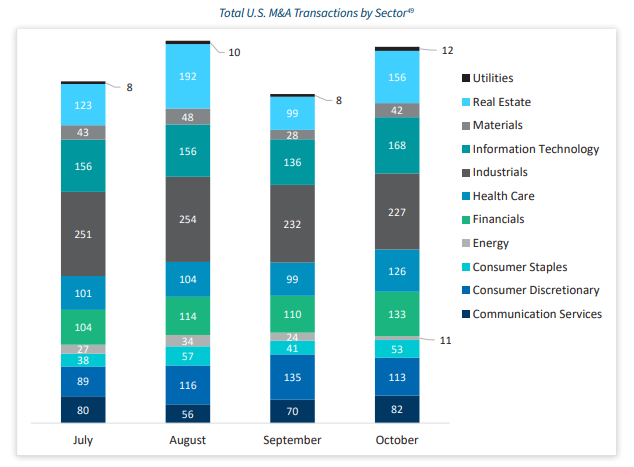

According to FTI Consulting’s September M&A Market Pulse report, after three months of rising U.S. transaction volumes, September saw a nearly 14% drop from August and a 5% decline year-over-year. Total 3Q volume was also down about 2% year-over-year. However, average transaction values in September spiked, largely due to a $103 billion mega-deal in the Communication Services sector. Without this deal, average values stayed stable compared to September 2023. [50]

The third quarter revealed notable shifts in transaction activity across sectors. Health Care saw an 8% year-over-year decline in deal volume, with Financials experiencing an even sharper drop of nearly 15%. In contrast, Communication Services stood out with an 11% increase over the same period. Meanwhile, the most active sectors, Industrials and Information Technology, remained steady, showing little change from last year. [51]

Screener Results and Relevant Campaigns

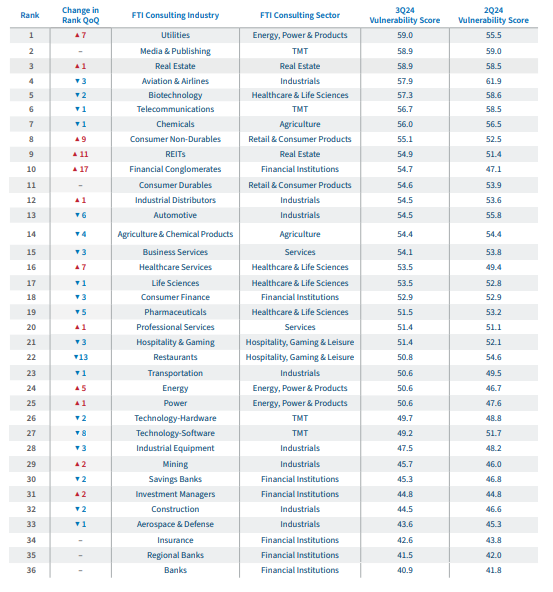

The latest rankings reveal significant volatility, with seven industries shifting by seven or more positions, including three that moved more than ten spots. The Utilities industry climbed seven places to become the most vulnerable sector to shareholder activism, while Media & Publishing maintained its hold on second place, and Real Estate edged up one position to complete the top three.

Utilities

After two consecutive quarters of improvement, the Utilities sector reclaimed its title as the most vulnerable industry to shareholder activism for the second time in the past four quarters. This rise, driven primarily by weaker Total Shareholder Returns (“TSR”), Governance and Operating Performance, saw Utilities climb seven spots in the rankings. Breaking down the Utilities industry a bit further, strong share price gains in the Electric Utilities and Gas Distributors sub-industries were partially offset by weaker returns of Alternative Power Generation and Water Utilities. Interestingly, the improved Operating Performance scores for Alternative Power Generation and Water Utilities were outweighed by the deteriorating scores of Electric Utilities and Gas Distributors.

Restaurants

The Restaurants industry experienced a beneficial reversal, dropping 13 spots to 22nd in the rankings after its previous quarter’s 10-spot climb. This decline resulted from improvements across all scoring categories, including Governance, TSR, Balance Sheet, and Operating Performance. TSR in particular remained strong through 3Q24 and continued into 4Q24, benefiting from improving economic conditions that support consumer spending. Restaurant Brands International’s CEO Josh Kobza highlighted factors such as reduced gas prices, moderating inflation and easing interest rates as key drivers enhancing financial accessibility for consumers. [52] Further, multiple chains, such as Burger King and Noodles & Company, are executing on turnaround and restructuring plans that have improved operating costs, but a difficult consumer environment has spurred increased levels of discount and promotion. [53], [54] If macroeconomic catalysts continue to improve while chains execute on their proactive operational improvement initiatives, we expect the Restaurants industry will continue to move down the vulnerability rankings.

Real Estate Investment Trusts (“REITs”)

After showing robust improvement in the previous quarter, REITs moved up by 11 spots in the rankings to reach 9th place, with notably weaker Governance, TSR, Balance Sheet, and Operating Performance results. This rise was primarily fueled by substantial increases in TSR and Balance Sheet vulnerabilities. REITs posted impressive returns in 3Q24, drawing investor interest; however, this momentum has since moderated, likely due to concerns over election uncertainty and adjusted interest rate expectations that have cooled enthusiasm. [55] Investors now anticipate fewer rate cuts in 2024 than initially expected, prompting a more cautious approach that could stabilize REIT performance in the coming quarters. [56]

Financial Conglomerates

Continuing its increasingly vulnerable trajectory, the Financial Conglomerates sector jumped 17 spots to reach 10th place in the rankings this quarter. This significant rise is attributed to weakened TSR and Balance Sheet scores, which can heighten the sector’s attractiveness to activist investors. As TSR declines can signal potential undervaluation, activists may view Financial Conglomerates as a strategic opportunity for targeted campaigns to unlock shareholder value. The upward shift for Financial Conglomerates illustrates the increased scrutiny that poor performance metrics can attract, especially in a fluctuating market environment.

Election Results Likely to Impact Investor Returns, Finalize Proxy Advisor Regulations

Last month’s election saw Republicans gain control of the U.S. Presidency, the U.S. Senate and retain its slim majority in the U.S. House of Representatives. Historically, Republicans have been perceived as friendlier toward investors and business. While longer term evidence is mixed, both the S&P 500 and the Russell 2000 generated a stronger TSR during the first Trump Administration than during either Democratic-led administration surrounding it.

Within the world of shareholder activism, a six-year process of potentially imposing new regulations on proxy advisors, such as ISS and Glass Lewis, seems likely to conclude. [57] The Trump Administration in 2020 implemented several new rules, including categorizing proxy advisors’ voting generally as a solicitation and requiring proxy advisors to report to their clients any company responses regarding their voting advice. [58] The rule was scheduled to become effective on December 1, 2021, but the Biden Administration rescinded it before it went into effect. [59] The National Association of Manufacturers (“NAM”) sued, seeking to restore the 2020 rule. The most recent court ruling, in June 2024 by the U.S. Fifth Circuit Court of Appeals, agreed with the NAM. [60] It seems likely that a Republican-led SEC will not challenge that ruling. As such, the 2020 rules will remain in place, finalizing a long-running question for proxy advisors, their clients and the companies upon which they opine.

Market commentators suggest that M&A deal flow should be more ebullient under the incoming Trump Administration. While we tend to think there is cause to be more optimistic, we note that from 2013 through 2023, the number of U.S. publicly traded companies acquired for $1 billion or more has proceeded at a relatively steady pace, no matter which party held the Presidency. [61] During President Obama’s second Administration, 75 acquisitions per year were announced. From 2017 to 2019, during the Trump Administration before the COVID-19 pandemic, an average of 78 such companies per year were acquired. During the first three years of the Biden Administration, an average of 73 such mergers were announced each year. [62] Thus, while M&A activity was less than the prior Trump administration, it was not as if M&A came to a standstill in recent years.

What This Means

The third quarter of 2024 reflected both predictable and evolving patterns in activist investor behavior. Activists continued to concentrate on TMT and Financial Institutions, where strategic and operational challenges, regulatory scrutiny, and volatility have presented both obstacles and opportunities. While TMT activism has faced limited success, the sector’s high visibility and complexity keep it a focal point, particularly as unresolved campaigns have the potential to impact results by year-end. The mid-cap segment’s growing appeal underscores activists’ shift toward companies where they have better odds of success, as demonstrated by the significant yearover-year increase in favorable outcomes.

As M&A interest remains strong, it will be interesting to watch how the new U.S. administration approaches transactions in 2025. Going forward, activists’ campaigns are likely to intensify in sectors with high vulnerability scores, particularly in industries like Utilities and Media & Publishing, where shareholder expectations for strategic pivots remain high.

1FTI Consulting analysis of Diligent market data as of November 1, 2024.(go back)

2FactSet market data for each tracked campaign as of December 2, 2024.(go back)

3Rohan Goswami, Leslie Josephs, “Elliott, Southwest in early settlement talks for significant board representation, sources say”, CNBC (October 20, 2024), https://www.cnbc.com/2024/10/20/southwest-luv-elliott-activist-settlement.html. (go back)

4Lauren Thomas, Alison Sider, “Elliott Takes Big Stake in Southwest Airlines”, The Wall Street Journal (June 10, 2024), https://www.wsj.com/finance/elliott-takes-big-stake-in-southwest-airlines-bce80796.(go back)

5“Southwest Airlines Announces Appointment of Six New Independent Directors”, Southwest Airlines press release (October 24, 2024), https://www.swamedia.com/news-and-stories/news-release/southwest-airlines-announces-appointment-of-six-new-independent-directors-MCZKTFFNFSURF3PCQ3DVHITYEKGM.(go back)

6“Southwest Airlines Launches Enhancements To Transform Customer Experience And Improve Financial Performance”, Southwest Airlines press release (July 25, 2024), https://www.southwestairlinesinvestorrelations.com/news-and-events/news-releases/2024/07-25-2024-110102603.(go back)

7Svea Herbst-Bayliss, “Elliott takes Southwest fight to shareholders, nominates eight directors”, Reuters (October 14, 2024), https://www.reuters.com/business/aerospace-defense/elliott-requests-special-meeting-with-southwest-airlines-bloomberg-news-reports-2024-10-14/.(go back)

8Rohan Goswami, Leslie Josephs, “Elliott, Southwest in early settlement talks for significant board representation, sources say”, CNBC (October 20, 2024), https://www.cnbc.com/2024/10/20/southwest-luv-elliott-activist-settlement.html.(go back)

9“Southwest Airlines Names Rakesh Gangwal Chair of the Board and Announces New Committee Chairs”, Southwest Airlines (November 4, 2024), https://www.swamedia.com/news-and-stories/news-release/southwest-airlines-names-rakesh-gangwal-chair-of-the-board-and-announces-new-comMCALDKIEOGBBAKVMICDTO4FDVHTQ#:~:text=New%20Committee%20Chairs-,Southwest%20Airlines%20Names%20Rakesh%20Gangwal%20Chair%20of,and%20Announces%20New%20Committee%20Chairs&text=DALLAS%2C%20November%204%2C%202024%20%E2%80%93%20Southwest%20Airlines%20Co.(go back)

10Lauren Thomas, “Activist Starboard Value Takes $1 Billion Stake in Pfizer”, The Wall Street Journal (October 6, 2024), https://www.wsj.com/health/pharma/activist-starboard-value-takes-1-billion-stake-in-pfizer-89591cb6.(go back)

11Michael Erman, “Pfizer management looks to show turnaround as Starboard looms”, Reuters (October 28, 2024), https://www.reuters.com/business/healthcare-pharmaceuticals/pfizer-management-looks-show-turnaround-starboard-looms-2024-10-28/.(go back)

12“Tim Buckley Elected to Pfizer’s Board of Directors”, Pfizer press release (October 15, 2024), https://www.pfizer.com/news/press-release/press-release-detail/tim-buckley-elected-pfizers-board-directors.(go back)

13“Pfizer explores sale of hospital drugs unit, sources say”, Reuters (November 12, 2024), https://www.reuters.com/business/healthcare-pharmaceuticals/pfizer-explores-sale-hospital-drugs-unit-sources-say-2024-11-12/.(go back)

14“Pfizer Announces New Chief Scientific Officer and President, Research & Development”, Pfizer press release (November 20, 2024), https://www.pfizer.com/news/press-release/press-release-detail/pfizer-announces-new-chief-scientific-officer-and-president.(go back)

15“Activist Politan seeks more seats on Masimo’s board to boost presence”, Reuters (March 25, 2024), https://www.reuters.com/business/activist-investor-politan-plans-second-proxy-battle-masimo-wsj-reports-2024-03-25/.(go back)

16Christy Santhosh, Pratik Jain, “Masimo prepared to provide one board seat if activist Politan drops proxy contest”, Reuters (May 9, 2024), https://www.reuters.com/business/healthcare-pharmaceuticals/masimo-says-prepared-provide-one-board-seat-activist-politan-2024-05-09/.(go back)

17“Masimo Has the Right Leadership and Strategy to Drive Long-Term Value Creation”, Masimo Investor Relations (August 26, 2024), https://investor.masimo.com/news/news-details/2024/Masimo-Has-the-Right-Leadership-and-Strategy-to-Drive-Long-Term-Value-Creation/default.aspx.(go back)

18Svea Herbst-Bayliss, “Masimo shareholders elect both Politan nominees in bitter boardroom battle”, Reuters (September 20, 2024), https://www.reuters.com/business/healthcare-pharmaceuticals/masimo-shareholders-elect-both-politan-nominees-bitter-boardroom-battle-2024-09-19/.(go back)

19Rohan Goswami, “Masimo CEO Joe Kiani ousted from board after proxy fight; Politan wins two seats”, CNBC (September 19, 2024), https://www.cnbc.com/2024/09/19/masimo-ceo-joe-kiani-ousted-from-board-politan-wins-two-seats.html.(go back)

20Katherine Burton, “Hedge Fund RTW Probed by SEC Over Role in Masimo Proxy Fight”, Bloomberg (November 27, 2024), https://www.bloomberg.com/news/articles/2024-11-26/hedge-fund-rtw-probed-by-sec-over-role-in-masimo-proxy-fight.(go back)

21Lauren Thomas, “Activist Urges Cheesecake Factory to Consider Breakup”, The Wall Street Journal (October 21, 2024), https://www.wsj.com/business/deals/activist-urges-cheesecake-factory-to-consider-breakup-c805ddf9.(go back)

22FTI Consulting analysis of Diligent market data as of November 1, 2024.(go back)

23Ibid.(go back)

24Ibid.(go back)

25Ibid.(go back)

26Ibid.(go back)

27Ibid.(go back)

28“Engine Capital Sends Letter to Upwork’s Board of Directors Regarding Opportunities to Substantially Increase Shareholder Value”, Engine Capital press release (September 13, 2024), https://enginecap.com/category/press-releases/.(go back)

29“Upwork Announces Organizational Changes to Drive Continued Profitable Growth and Provides Preliminary Third Quarter 2024 Results Above Financial Guidance”, Upwork press release (October 23, 2024), https://investors.upwork.com/news-releases/news-release-details/upwork-announces-organizational-changes-drive-continued.(go back)

30“Breach Inlet Capital Sends Public Letter to Board of International Money Express”, Business Wire (September 4, 2024), https://www.businesswire.com/news/home/20240904791096/en/Breach-Inlet-Capital-Sends-Public-Letter-to-Board-of-International-Money-Express.(go back)

31International Money Express, Inc. Schedule 13D filed with the SEC on September 5, 2024.(go back)

32“Intermex Reports Third-Quarter Results”, Intermex International Money Express press release (November 8, 2024), https://investors.intermexonline.com/news-releases/news-release-details/intermex-reports-third-quarter-results-0.(go back)

33FTI Consulting analysis of Diligent market data as of November 1, 2024.(go back)

34Ibid.(go back)

35Leah Nylen, Josh Sisco, “DOJ Will Push Google to Sell Chrome to Break Search Monopoly”, Bloomberg (November 18, 2024), https://www.bloomberg.com/news/articles/2024-11-18/doj-will-push-google-to-sell-off-chrome-to-break-search-monopoly?sref=p5QwRxCz.(go back)

36FTI Consulting analysis of Diligent market data as of November 1, 2024.(go back)

37Ibid.(go back)

38Jeffrey Smith, Starboard Value web site (July 15, 2024), https://www.starboardvalue.com/wp-content/uploads/Starboard_Value_LP_Letter_to_MTCH_07.16.2024.pdf.(go back)

39Rohan Goswami, “Match adds two directors in deal with activist investor Elliott Management”, CNBC (March 25, 2024), https://www.cnbc.com/2024/03/25/match-adds-two-directors-in-deal-with-activist-investor.html.(go back)

40Crystal Tse, Natalie Lung, “Match Group Attracts Second Activist, Anson Funds”, Bloomberg (March 14, 2024), https://www.bloomberg.com/news/articles/2024-03-14/match-group-is-said-to-attract-to-second-activist-anson-funds?sref=p5QwRxCz.(go back)

41Jeffrey Smith, Starboard Value (July 15, 2024), https://www.starboardvalue.com/wp-content/uploads/Starboard_Value_LP_Letter_to_MTCH_07.16.2024.pdf.(go back)

42Natalie Lung, “Match Jumps Most Since 2022 After 6% Job Cuts, Upbeat Earnings”, Bloomberg (July 30, 2024), https://www.bloomberg.com/news/articles/2024-07-30/match-group-s-tinder-payer-decline-worsens-amid-activist-push?sref=p5QwRxCz.(go back)

43Jeffrey Smith, Starboard Value (July 15, 2024), https://www.starboardvalue.com/wp-content/uploads/Starboard_Value_LP_Letter_to_MTCH_07.16.2024.pdf.(go back)

44“Match Group Promotes Steven Bailey as Chief Financial Officer; Gary Swidler to Continue as President”, Match Group press release (October 7, 2024), https://ir.mtch.com/investor-relations/news-events/news-events/news-details/2024/Match-Group-Promotes-Steven-Bailey-as-Chief-Financial-Officer-Gary-Swidler-to-Continue-as-President/default.aspx.(go back)

45FTI Consulting analysis of Diligent market data as of November 1, 2024.(go back)

46Kenneth Squire, “Activist Ancora joins investors’ calls for a strategic review at Forward Air. Here’s what may happen next”, CNBC (September 7, 2024), https://www.cnbc.com/2024/09/07/activist-ancora-joins-investors-calls-for-a-strategic-review-at-forward-air.html.(go back)

47Larry Avila, “Forward Air investors push for company sale”, Trucking Dive (October 10, 2024), https://www.truckingdive.com/news/alta-fox-capital-pushes-sale-forwardair/729269/.(go back)

48Kenneth Squire, “Activist Ancora joins investors’ calls for a strategic review at Forward Air. Here’s what may happen next”, CNBC (September 7, 2024), https://www.cnbc.com/2024/09/07/activist-ancora-joins-investors-calls-for-a-strategic-review-at-forward-air.html.(go back)

49FTI Consulting analysis of Capital IQ market data.(go back)

50“M&A Market Pulse”, FTI Consulting (September 30, 2024), https://images.now.fticonsulting.com/Web/FTIConsultingInc/%7Bf8b11494-e8f7-4299-8a81-f3105b79257c%7D_September_MA_Report.pdf.(go back)

51FTI Consulting analysis of Capital IQ market data.(go back)

52Amelia Lucas, “Burger King parent Restaurant Brands falls short of third-quarter expectations“, CNBC (November 5, 2024), https://www.cnbc.com/2024/11/05/restaurant-brands-international-qsr-earnings-q3-2024.html.(go back)

53Ibid.(go back)

54Alicia Kelso, “Noodles & Company impacted by ‘significant’ drop in third-party delivery sales“, Nation’s Restaurant News (November 7, 2024), https://www.nrn.com/fast-casual/noodles-company-impacted-significant-drop-third-party-delivery-sales.(go back)

55Rich Hill, “The Real Estate Reel: A closer look at Q3’s historically strong listed REIT returns”, Cohen & Steers (October 2024), https://www.cohenandsteers.com/insights/the-real-estate-reel-a-closer-look-at-q3s-historically-strong-listed-reit-returns/.(go back)

56“Fed Rate Cuts Are Still Likely to Be Modest Overall in This Easing Cycle”, Fitch Ratings (September 23, 2024), https://www.fitchratings.com/research/sovereigns/fed-rate-cuts-are-still-likely-to-be-modest-overall-in-this-easing-cycle-23-09-2024#:~:text=We%20now%20expect%20the%20federal,September%202024%20Global%20Economic%20Outlook.(go back)

57“SEC Publishes New Guidance on Investment Advisers’ Proxy Voting Responsibilities and Reliance on Proxy Advisors”, Sidley (August 27, 2019), https://www.sidley.com/en/insights/newsupdates/2019/08/sec-publishes-new-guidance-on-investment-advisers-proxy-voting.(go back)

58“SEC Adopts Proxy Rule Amendments Relating to Proxy Voting Advice Businesses”, Skadden (July 27, 2020), https://www.skadden.com/insights/publications/2020/07/sec-adopts-proxy-rule-amendments.(go back)

59“Fifth Circuit Vacates the SEC’s Rescission of its Proxy Advisor Notice-and-Awareness Requirements”, Buchanan (July 3, 2024), https://www.bipc.com/fifth-circuit-vacates-the-sec%E2%80%99s-rescission-of-its-proxy-advisor-notice-and-awareness-requirements.(go back)

60“Manufacturers Victorious Over SEC in Fifth Circuit Proxy Firm Case”, The National Association of Manufacturers (June 27, 2024), https://nam.org/manufacturers-victorious-over-sec-in-fifth-circuit-proxy-firm-case-31466/?stream=news-insights.(go back)

61FTI Consulting analysis of FactSet market data.(go back)

62Ibid.(go back)