Print

PrintTiziana Londero is a Policy Analyst at OECD. This post is based on the new 2025 edition of the OECD Corporate Governance Factbook.

As capital markets evolve, so do shareholder rights. Trends such as increasing ownership concentration, the growing dominance of institutional investors and new share structures are reshaping the corporate landscape. While there is widespread consensus that protecting shareholder rights remains a cornerstone of sound corporate governance, the ways in which they are exercised and safeguarded continue to evolve with new market realities.

The latest edition of the OECD Corporate Governance Factbook provides insights into recent developments on shareholder rights globally. It covers all G20 and OECD economies, and for the first time provides detailed country notes on each of them.

I. The rising role of institutional investors and stewardship responsibilities

Today institutional investors hold nearly half of all listed equity globally, giving them an outsized role in corporate governance. Countries have responded by strengthening disclosure and stewardship frameworks.

In 2024, nearly 90% of jurisdictions analysed in the Factbook required or encouraged institutional investors to disclose their voting policies. A decade ago, that figure stood at just over 50%. At the same time, jurisdictions requiring them to report on how they actually voted nearly doubled, reaching 73% in 2024. And almost all (98%) now mandate policies to address conflicts of interest, compared to 59% in 2014.

In parallel, 40% of jurisdictions now have stewardship codes or principles that encourage institutional investors to actively engage with investee companies and report on their activities. In many markets these codes are set by industry groups (e.g. Canada, the Netherlands, Singapore), while in others, regulators have taken the lead (e.g. Japan, Spain, the United Kingdom). Overall, these voluntary codes complement formal rules by encouraging both domestic and foreign institutional owners to actively monitor and engage with their investee firms.

With institutional investors’ votes carrying increasing weight, proxy advisory firms have become crucial intermediaries. Yet only about half of jurisdictions have a framework in place to regulate them. Recognising this gap, the OECD is undertaking additional work on the governance of proxy advisors and other capital market service providers.

II. Rethinking voting rights: Beyond the one-share-one-vote principle

A growing number of jurisdictions are abandoning the traditional one-share-one-vote principle and embracing more flexible capital structures.

The G20/OECD Principles of Corporate Governance acknowledge that companies may issue different classes of shares, as long as shareholders within each class are treated equally, that the use of such structures is disclosed, and that any changes in economic or voting rights are subject to approval by those classes of shares which are negatively affected.

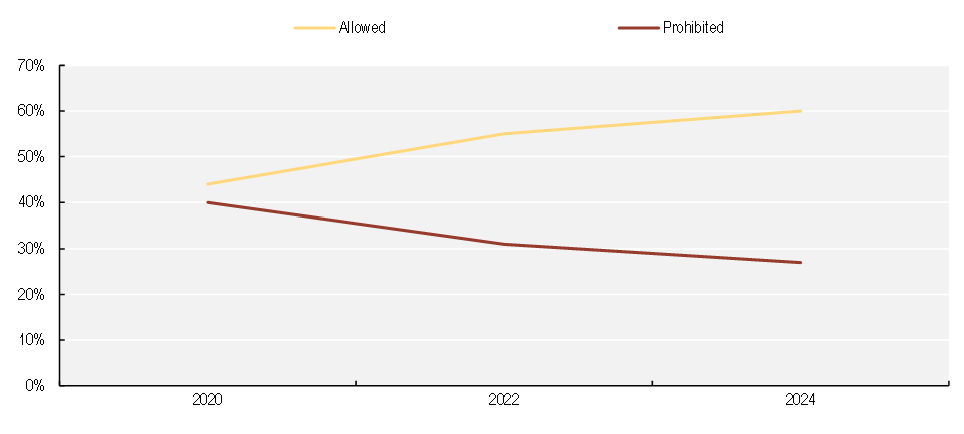

While such arrangements were once widely restricted, today 60% of countries allow companies to issue shares with different voting power, up from 44% in 2020. For example, the People’s Republic of China (hereafter ‘China’), Ireland, Mexico and Saudi Arabia all recently updated their frameworks to allow multiple voting rights. Meanwhile, the share of jurisdictions that prohibit multiple voting rights dropped from 40% in 2020 to 27% in 2024.

Figure 1. Issuance of shares with a different number of votes per share, 2020-24

Note: The data are for 52 jurisdictions in 2024, 49 in 2022 and 50 in 2020. “Allowed” includes jurisdictions where shares with a different number of votes per share are allowed upon condition. In 13% of jurisdictions there is no explicit framework.

Source: OECD (2025), OECD Corporate Governance Factbook 2025, OECD Publishing, Paris, https://doi.org/10.1787/f4f43735-en.

Two key motivations lie behind this change. The first is to encourage IPO activity and capital formation. Different voting structures can encourage founders and early investors to tap public markets while retaining strategic control. The second is to curb short-termism by rewarding long-term shareholders, typically through loyalty shares, such as in France and Spain.

Countries have implemented a variety of safeguards to balance the advantages of multiple voting rights with the protection of shareholders. For instance, Sweden caps multiple voting rights shares at 10% of a company’s share capital. Many markets restrict these share structures before the IPO, such as China and Italy.

Additional safeguards are time limits (sunset clauses) or review conditions on multiple voting rights, ensuring these are reassessed as companies mature. For loyalty shares, companies often need to renew the scheme through shareholder approval every few years.

With countries adopting different approaches, a degree of regulatory competition has also emerged, as companies look for the listing venue or incorporation jurisdiction that best suits their desired capital structure.

There is a growing consensus that investor safeguards should accompany the rise of multiple voting rights shares. The challenge ahead will be calibrating them so that capital markets remain both attractive to issuers and fair to investors.

III. Stronger safeguards for related party transactions in an era of concentrated ownership

Corporate ownership is becoming increasingly concentrated. This raises critical questions about how to protect minority investors from undue influence. With the top three shareholders controlling over half the equity in nearly half of listed companies worldwide, regulators are strengthening related party transaction (RPT) safeguards to better protect minority investors.

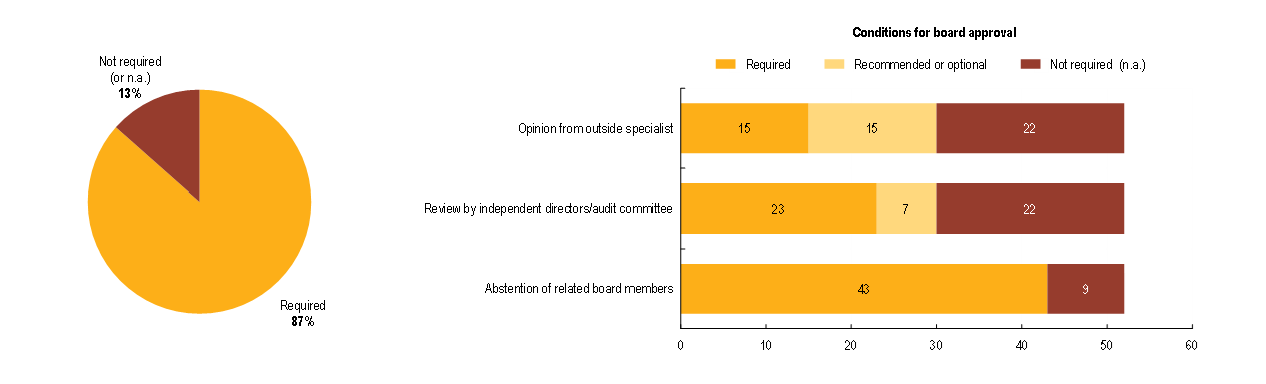

The share of jurisdictions requiring board approval for significant RPTs jumped from 54% in 2014 to 87% in 2024, and those mandating immediate disclosure of material RPTs soared from about half in 2016 to nearly all in 2024.

To curb the risk of entrenchment, most jurisdictions have introduced layered safeguards. For example, two-thirds require shareholders to approve RPTs if specific conditions apply, in addition or as an alternative to board approval. Interested parties must abstain from voting in 83% of jurisdictions, compared to just 30% in 2014. A review by independent board members and audit committees is required in 44%, while opinions from external auditors or outside specialists in 29% help ensure such deals are conducted fairly and at arm’s length.

Figure 2. Board approval for certain types of related party transactions

Source: OECD (2025), OECD Corporate Governance Factbook 2025, OECD Publishing, Paris, https://doi.org/10.1787/f4f43735-en.

IV. Shareholder participation in annual general meetings

Digitalisation is also impacting shareholder rights, notably concerning participation in annual general meetings (AGMs). Virtual-only meetings are now permitted in 85% of jurisdictions, and hybrid meetings in 94%, an increase of 10 percentage points for both since 2022.

As they become more widespread, virtual and hybrid meetings must remain inclusive and uphold equal access to information and participation. While this shift has helped broaden access to AGMs, especially for retail and geographically distant shareholders, robust safeguards are needed to ensure shareholders can fully exercise their rights in remote settings.

The OECD report Shareholder Meetings and Corporate Governance, published earlier this year, explores these developments in depth, including how jurisdictions provide safeguards to ensure meetings remain inclusive.

Looking ahead

As capital markets evolve and ownership structures become more complex or concentrated, policies for shareholder treatment will require careful calibration of checks and balances. Governance frameworks must remain strong enough to protect minority shareholders, while flexible to support innovation, capital formation and market competitiveness. Striking this balance is key to sustaining trust, resilience and long-term value in corporate governance.

The 2025 OECD Corporate Governance Factbook offers a resource to inform these policy decisions, helping policymakers, practitioners and market participants navigate the path forward.

Link to the full report can be found here.