Print

PrintLauren Peek is a Partner and Joanna Czyzewski is a Principal at Compensation Advisory Partners. This post is based on their CAP memorandum.

CAP reviewed chief executive officer (CEO) pay levels among 50 companies with fiscal years ending between August and October 2025 (defined as the Early Filers). 2025 financial performance was generally flat to up, which resulted in median bonus payouts of around target. Total compensation for the CEO was up +8% due to an increase in the grant date value of long-term incentives (LTI). This report covers 2025 financial performance, CEO actual pay levels and annual incentive payouts for the Early Filers.

Key Findings

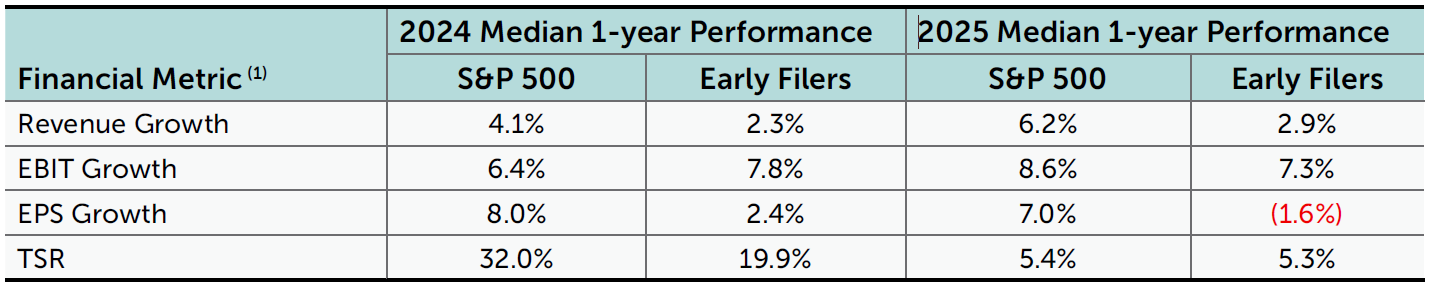

Performance: 2025 median financial performance – as measured by revenue, earnings before interest and taxes (EBIT), and earnings per share (EPS) – was generally flat to up. In 2025, median revenue grew slightly (+2.9%), EBIT grew modestly (+7.3%) and EPS was down slightly (-1.6%). One-year total shareholder return (TSR) was up modestly (+5.3%) and generally aligned with overall financial performance.

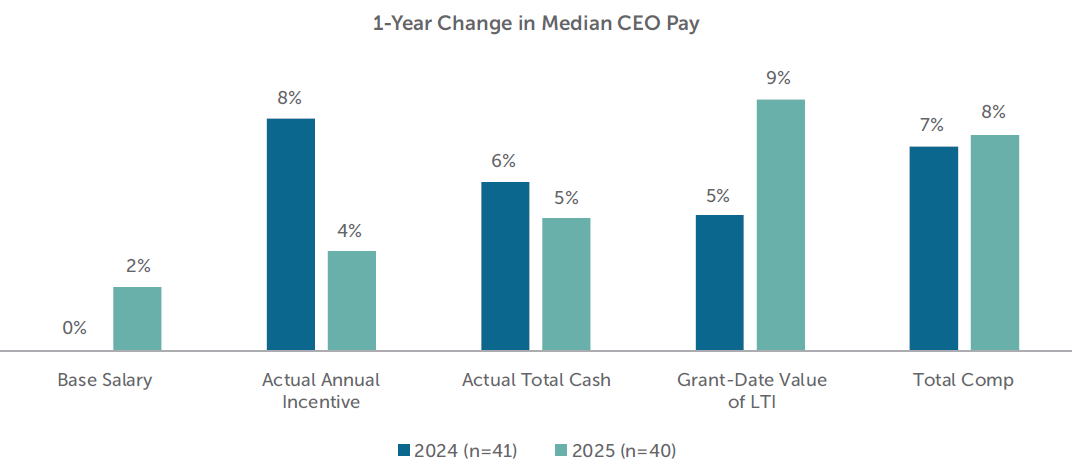

CEO Pay: Median CEO total direct compensation increased +8% year over year, driven by a +9% increase in the grant-date value of long-term incentives (LTI). Annual incentive payout was up +4% generally due to increases in the target opportunity.

Annual Incentive Payout: For the third year in a row, the median bonus payout for CEOs was around target (i.e., 98% of target). While median and 75th percentile payouts were consistent with the prior two years, we saw a modest rise in the 25th percentile payout due, in part, to fewer companies having a payout below 50% of target than in prior years. About 25% of companies increased the CEO’s bonus payout above the corporate funded amount through either individual performance or positive committee discretion.

2025 Performance

Financial performance was flat to up for the Early Filers. Median revenue was up +2.9%, EBIT was up +7.3% and EPS was slightly down -1.6%. Median S&P 500 performance for the metrics reviewed was up modestly over the same period.

Median TSR performance was up moderately for Early Filers and generally aligned with 1-year financial performance. At median, TSR was up +5.3% year over year; the S&P 500 had similar median TSR performance over the same period (+5.4%). We measure TSR through a company’s fiscal year end for the Early Filers and through September 30th for the S&P 500. The index returns for calendar year 2025 were around 17%, influenced by the larger technology companies that saw Q4 stock price performance increase with the AI boom.

(1) Reflects companies in the S&P 500 as of February 2026. For the S&P 500, financial performance and TSR are as of September 30, 2025 and September 30, 2024. For Early Filers, financial performance and TSR are as of each company’s fiscal year end.

2025 CEO Actual Total Direct Compensation

CEO pay increased in 2025. Median CEO total direct compensation – base salary plus actual bonus payout plus grant-date value of LTI – was up +8%. This increase was largely delivered in the form of LTI which was up +9% year over year. LTI awards are generally approved in the first quarter (i.e., September 2024 – January 2025 for Early Filers), and increases in award value are typically to recognize strong company and/or individual performance from the prior year. Long-term incentive pay eventually realized by CEOs may be higher or lower than the target amounts.

Median salary was up 2.3% in 2025 (slightly behind merit budget increases for 2025). Annual incentive payout was up +4% year over year. This increase in the annual incentive payout was generally due to increases in the target bonus opportunity.

Note: Reflects same incumbent CEOs.

Annual Incentive Plan Payout

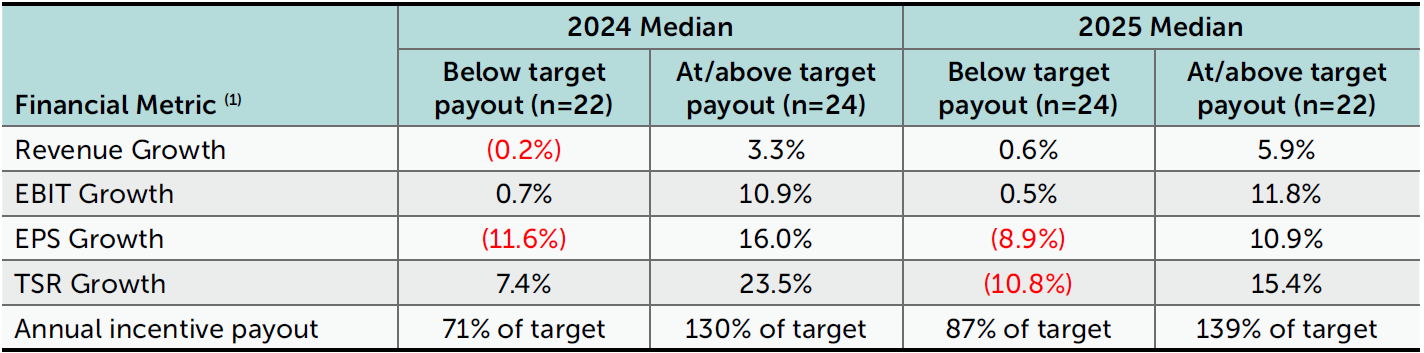

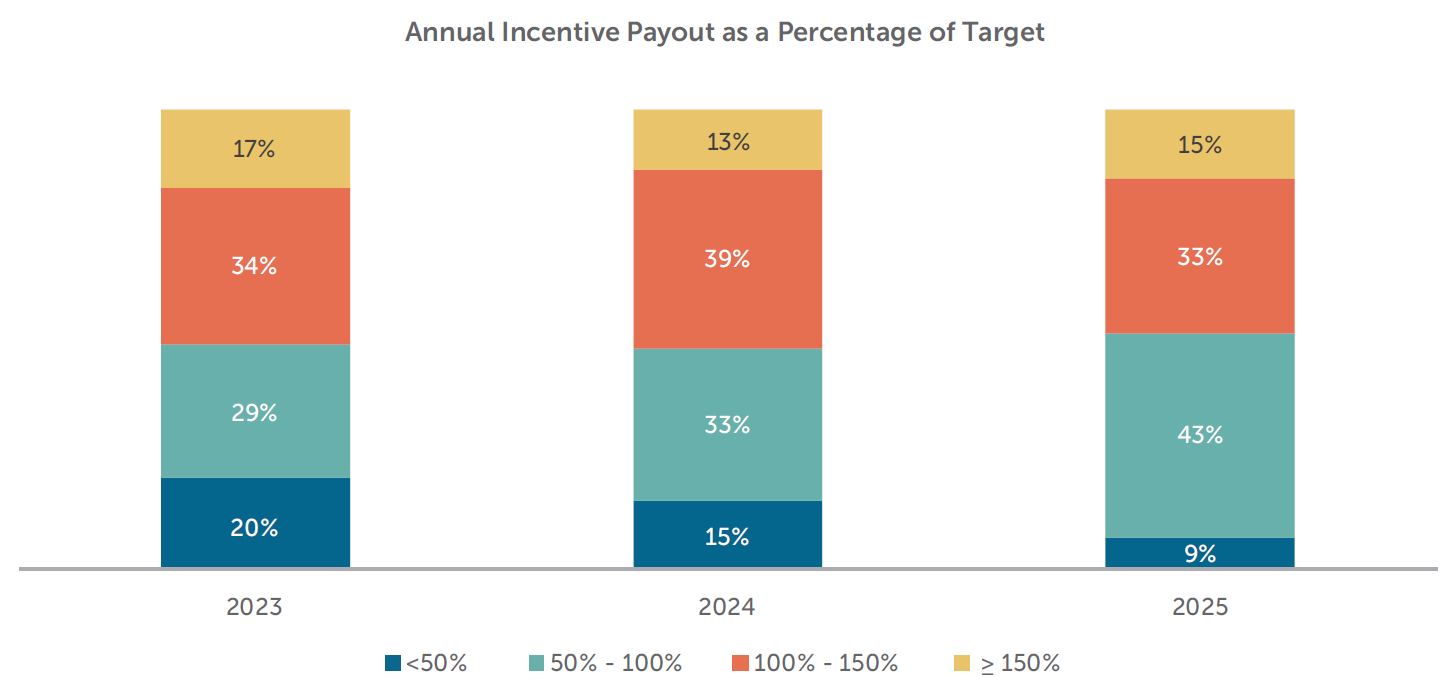

For a third year in a row, the median annual incentive payout was around target (98% in 2025). Median and 75th percentile payouts as a percentage of target were generally flat when compared to 2023 and 2024. However, in 2025, we saw a modest increase in the 25th percentile bonus payout (87% of target in 2025 vs. 77% of target in 2024 and 76% in 2023).

Approximately 50% of the companies in our sample achieved annual incentive payouts at or above target (median payout for these companies was 139% of target). These organizations demonstrated robust performance, including a notable increase in revenue and double-digit growth in EBIT, EPS, and TSR.

In contrast, companies with below target payouts experienced flat or declining financial results. The median payout for this group was 87% of target.

(1) 1-year financial performance and TSR is as of each company’s fiscal year end.

Nearly 80% of the companies studied provided a bonus payout that was between 50 – 150% of target. We saw more companies providing a payout just below target as well as fewer companies having a payout below 50% of target which resulted in a higher 25th percentile payout (87% of target) among the Early Filers.

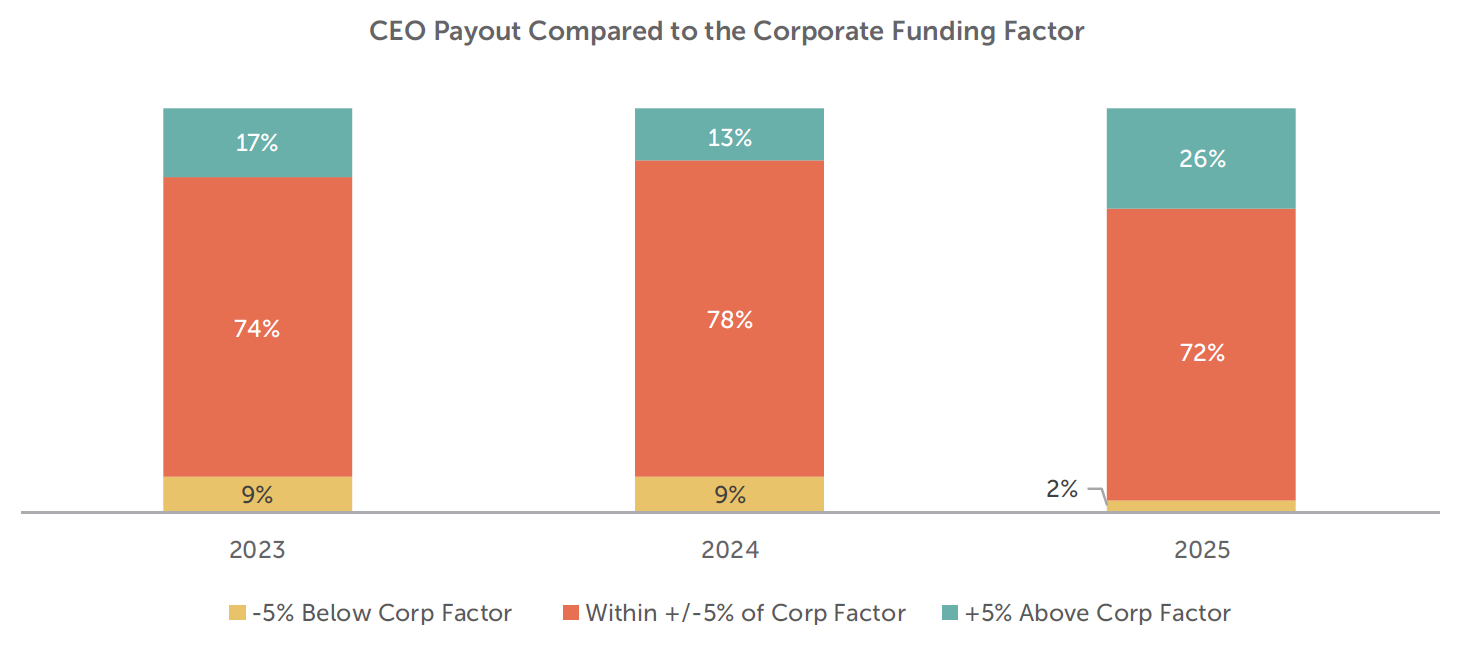

Note: N = 46. Reflects corporate payout factor and excludes companies with a discretionary bonus plan.

Most companies provided a payout to the CEO that was +/-5 percentage points from the corporate funding factor (i.e., the percentage at which the annual incentive funds based on company performance). If a company wanted to adjust an executive’s payout, as approximately 30% of the Early Filers did, there are a couple of ways in which it could be accomplished – through individual performance or discretionary adjustment. 30% of the Early Filers use individual performance as a component of the annual incentive payout for the CEO. Companies use individual performance to align the incentive payout with an executive’s contribution to the company and the results can raise or lower an executive’s payout relative to corporate performance. Alternatively, companies may make discretionary adjustments to recognize overall company performance (more broadly than incentive plan or financial metrics), particularly if an individual component is not part of the annual incentive plan design.

In 2025, about a quarter of companies increased the CEO’s payout above the corporate funding factor. The average increase ranged from 8 – 50 percentage points above the funding factor. Most of these increases were provided through an individual performance component although some companies did so through a discretionary adjustment. When a company provides a positive discretionary adjustment, it typically does not raise a below target payout to above target. Only one company reduced the CEO’s payout in 2025.

Looking Ahead

2025 was a year of uncertainty, largely defined by tariffs which impacted both financial performance and stock price performance. For the Early Filers, tariffs were enacted after their Q1 began which means that annual incentive goals were established and set before tariffs were implemented. Despite the challenges, median annual incentive payout for companies was around median. CEO total compensation was up year over year driven by increases in LTI awards given strong TSR performance in the prior year.

There is continued uncertainty for 2026 because of tariffs and its impact on the global supply chain. We anticipate that goal setting will continue to be a challenge for companies, particularly given the recent Supreme Court ruling on tariffs. When there is economic uncertainty, companies typically take two approaches for incentives: either through goal setting at the beginning or determining final payout at the end of the performance period. During the goal setting process, companies will try to address it by widening the performance leverage curve, flattening the payout range around target or setting more conservative growth goals. At the time of payout, other companies may deal with uncertainty by adjusting the final results to exclude the impact of tariffs or use Compensation Committee discretion to adjust the final payout. At the time of writing, the war in Iran recently began and is adding uncertainty to the economy. Most companies (including fiscal year companies) have set their budgets and incentive plan goals for 2026. The impact of the war is yet to be seen and may not affect all companies. Depending on the length of the war, we would expect that companies that are greatly impacted would be more likely to make adjustments while others may take a wait and see approach.

Given the moderate increase in TSR performance in 2025, we would expect to see modest increases in LTI award values for 2026 to align with stock price performance. In the broader market, we may see larger increases in LTI for 2026, particularly at AI or technology companies, given the significant stock price appreciation towards the end of 2025.

Early Filer’s Company Sample

CAP’s study reflects 50 companies with fiscal years ending between August and October 2025. Industry sectors reviewed include: Communication Services, Consumer Discretionary, Consumer Staples, Financials, Health Care, Industrials, Information Technology and Materials. Revenues for these companies ranged from $1.1 billion – $416 billion (median revenues of $11.5 billion); median fiscal-year-end market capitalization was $16.2 billion.

Grace Tan and Bhavika Podduturi provided research assistance for this report.